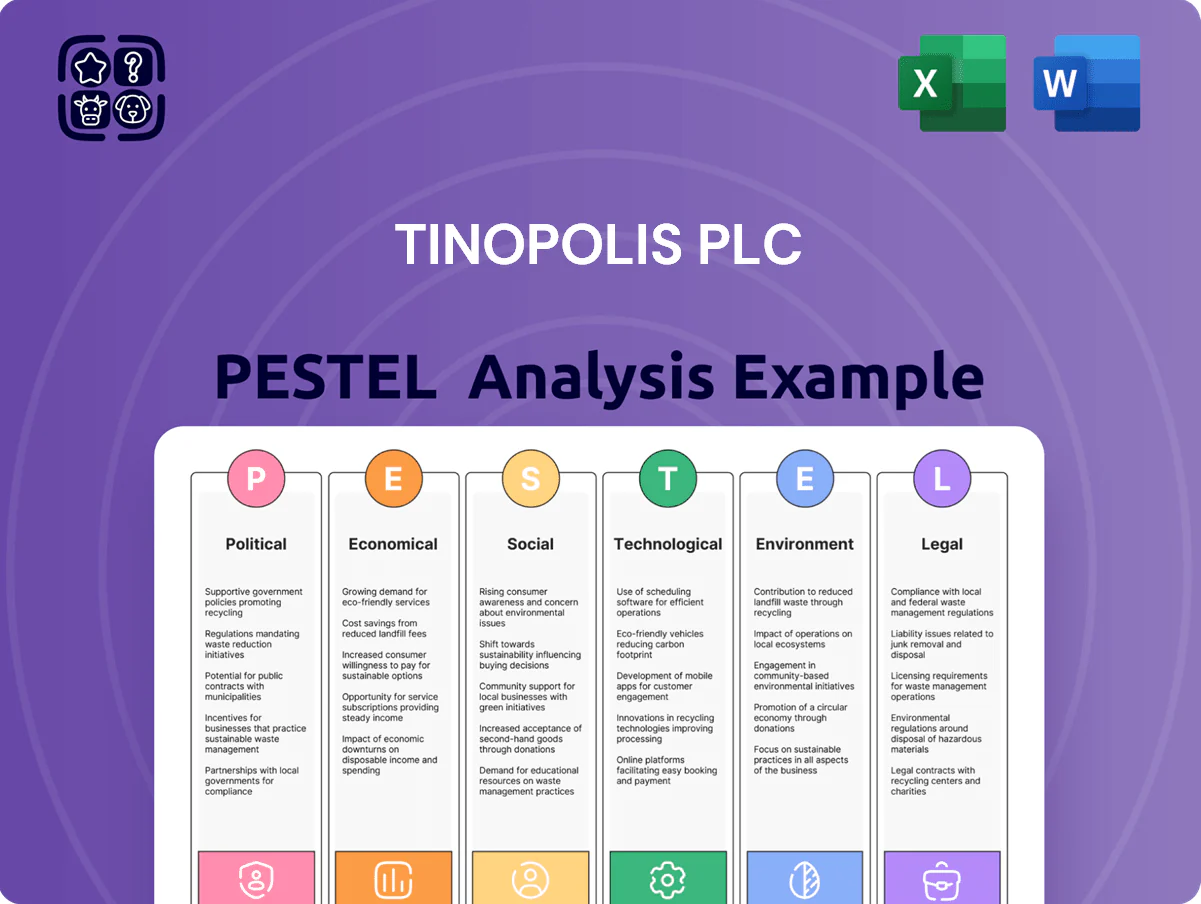

Tinopolis PLC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are shaping Tinopolis PLC’s trajectory—our concise PESTLE snapshot highlights key external forces and strategic implications; buy the full analysis to access detailed data, actionable recommendations, and editable charts for immediate use.

Political factors

Public Service Broadcasting Funding

The stability of the BBC license fee and government funding directly affects Tinopolis’s production pipeline; the BBC’s £3.75bn annual license fee (2024/25) underpins circa 25% of UK commission spend, and cuts or a shifted remit could reduce commissioning for independents like Tinopolis by an estimated 10–20% of UK revenues. Political moves away from traditional funding models have prompted contingency planning, and as of late 2025 the unresolved debate on sustainable funding for national broadcasters remains a critical risk to commission volumes and cashflow.

Global Trade and Content Export Policies

Post-Brexit trade agreements and co-production treaties shape Tinopolis PLCs access to EU and North American markets; UK-EU trade friction reduced goods tariffs but content rules remain complex, with UK creative exports to EU valued at £34bn in 2022 and streaming growth of 12% YoY increasing stakes.

Regional Production Incentives

Government initiatives to decentralize media production—including UK tax reliefs and regional grants totaling over 1.2 billion pounds in creative sector support in 2024—provide tax breaks and direct funding that boost Tinopolis’s regional offices.

Shifts in political leadership can affect the continuation of these incentives; for example, local council budget reallocations in 2023 cut some arts grants by up to 18%, risking expiration of key funding streams.

Maintaining a strong presence in Wales and other regions enables Tinopolis to capture regional tax reliefs (Wales offers up to 25% production rebates in targeted schemes) and grant awards, directly enhancing project margins and cash flow.

Regulatory Oversight on Content Diversity

Political pressure on representation and cultural diversity is shaping commissioning decisions by UK broadcasters; Ofcom reported in 2023 that 56% of audiences expect greater on-screen diversity, pushing Tinopolis to adapt project pipelines.

Tinopolis must align with evolving government diversity quotas and the UK Creative Diversity Network targets (aiming for 40% representation of underrepresented groups by 2025) to retain access to public tenders.

Non-compliance risks reduced eligibility for state-backed funds; the BFI distributed £80m in 2024 with diversity criteria linked to funding decisions.

- 56% audience demand for diversity (Ofcom 2023)

- CDN target: 40% underrepresented groups by 2025

- BFI 2024 funding £80m tied to diversity

Soft Power and Cultural Diplomacy

The UK government channels about 74m annually through the Creative Industries Council and export programmes, boosting British TV reach; Tinopolis benefits from diplomatic support and trade missions that helped secure 12% revenue growth from international sales in FY2024.

Political stability and UK promotion at events like the 2024 UK-Africa Investment Summit enabled Tinopolis partnerships in three emerging markets; changes in foreign policy or sanctions risk restricting distribution in sensitive territories such as Russia or parts of MENA.

- UK creative export funding ~74m (annual programmes)

- Tinopolis international sales +12% in FY2024

- New partnerships in 3 emerging markets after 2024 summits

- Foreign policy shifts/sanctions pose distribution risk

Funding shifts risk 10–20% UK revenue but tax reliefs & export aid boost margins

Political factors: BBC license fee £3.75bn (2024/25) underpins ~25% UK commissions; funding uncertainty could cut Tinopolis UK revenue 10–20%. UK creative supports £1.2bn (2024) and tax reliefs (Wales up to 25%) improve margins; export programmes ~£74m aid international sales (+12% FY2024). Diversity targets (CDN 40% by 2025) and BFI £80m (2024) tie funding to compliance.

| Metric | Value |

|---|---|

| BBC license fee | £3.75bn (2024/25) |

| UK creative support | £1.2bn (2024) |

| Wales rebate | Up to 25% |

| Export programmes | ~£74m |

| Tinopolis intl sales | +12% FY2024 |

| BFI funding | £80m (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Tinopolis PLC’s content production, distribution and revenue models, with data-backed insights and forward-looking scenarios to guide executives, investors and strategists in identifying risks and opportunities specific to its media markets and regulatory landscape.

A concise, visually segmented PESTLE summary of Tinopolis PLC that eases meeting prep, supports quick risk discussions and slide-ready insights, and can be annotated or shared across teams for aligned strategic planning.

Economic factors

Inflationary Pressure on Production Costs

Rising talent, equipment and energy costs squeezed margins across media production through 2025, with UK production wage inflation ~6–8% and energy prices up ~20% year-on-year in 2023–24, raising Tinopolis’s unit costs while many broadcaster contracts remain fixed-price.

Tinopolis faces compressed EBITDA margins—UK indie peers reported median EBITDAR falls of ~150–250bps in 2024—so disciplined budgeting and cost controls are essential to preserve profitability on large-scale projects.

Advertising Revenue Fluctuations

The health of the UK economy drives advertising spend—UK ad expenditure fell 3.7% in 2023 after strong 2022 growth and remained soft into 2024, pressuring ITV and Channel 4 commissioning budgets; broadcasters cut high-budget drama slots and pilot commissions during downturns. Tinopolis is sensitive to these cycles, with FY2024 order book visibility weakened as ad-driven commissions declined, increasing revenue volatility and margin pressure.

Currency Exchange Rate Volatility

Tinopolis, with major US subsidiaries, faces GBP/USD volatility that in 2024 ranged 1.20–1.37, which can materially swing reported US earnings and reduce consolidated revenue when sterling strengthens.

Exchange movements also raise the sterling cost of US co-productions and talent fees; a 10% GBP appreciation could cut translated US revenue by roughly 9–11% based on 2023–24 US sales mix.

Active hedging (forwards, options) is therefore critical: Tinopolis reported using currency hedges in FY2024 to stabilise EBITDA exposure and protect cash flows across the group.

Access to Capital and Interest Rates

The cost of debt is a critical constraint for independent media groups funding acquisitions or IP development; UK base rates rose to 5.25% by Dec 2025, keeping corporate borrowing costly and lifting average BBB- corporate yields by ~150–200bp versus 2021 levels.

Higher rates through 2025 increased servicing costs and raised Tinopolis’s investment hurdle rate; securing sub-7% financing would materially aid deal viability given recent mid-market deal multiples of 7–9x EBITDA.

Tinopolis’s capacity to negotiate favorable terms—via cash generation, covenants flexibility, or equity—will be decisive for strategic flexibility and long-term growth.

- UK policy rate ~5.25% (Dec 2025)

- BBB- corporate spreads +150–200bp vs 2021

- Target financing <7% improves deal economics

- Typical mid-market multiples 7–9x EBITDA

Consumer Subscription Fatigue

Economic constraints have driven streaming market saturation; global subscription growth slowed to 4% in 2024 and churn rose to ~17% in H2 2024, making consumers more selective and price-sensitive.

Platforms are shifting from volume commissioning to high-impact, cost-efficient content—streamers cut content spend by up to 12% in 2024—pressuring Tinopolis to offer leaner, higher-ROI formats.

Tinopolis must adapt sales to cautious global buyers (e.g., Netflix, Amazon, Disney reduced new commissions in 2024), pitching efficiencies, co-productions and measurable KPIs.

- Streaming subs growth 2024: +4% globally

- Churn ~17% in H2 2024

- Content spend cuts up to 12% in 2024

- Focus on high-ROI, lean formats and co-productions

Margin squeeze from wage, energy and ad declines; FX and higher rates tighten M&A math

Rising input costs and energy (wage inflation 6–8%, energy +~20% in 2023–24) compressed margins; ad-driven commissioning fell (UK ad spend −3.7% in 2023), reducing FY2024 order-book visibility; GBP/USD ranged 1.20–1.37 in 2024, a 10% GBP move could cut US-translated revenue ~9–11%; UK policy rate ~5.25% (Dec 2025) raised borrowing costs, with BBB- spreads +150–200bp, making sub-7% financing pivotal for M&A.

| Metric | Value |

|---|---|

| Wage inflation | 6–8% |

| Energy change | +~20% (2023–24) |

| UK ad spend | −3.7% (2023) |

| GBP/USD range | 1.20–1.37 (2024) |

| Policy rate | ~5.25% (Dec 2025) |

| BBB- spread vs 2021 | +150–200bp |

Preview the Actual Deliverable

Tinopolis PLC PESTLE Analysis

The preview shown here is the exact Tinopolis PLC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are shaping Tinopolis PLC’s trajectory—our concise PESTLE snapshot highlights key external forces and strategic implications; buy the full analysis to access detailed data, actionable recommendations, and editable charts for immediate use.

Political factors

Public Service Broadcasting Funding

The stability of the BBC license fee and government funding directly affects Tinopolis’s production pipeline; the BBC’s £3.75bn annual license fee (2024/25) underpins circa 25% of UK commission spend, and cuts or a shifted remit could reduce commissioning for independents like Tinopolis by an estimated 10–20% of UK revenues. Political moves away from traditional funding models have prompted contingency planning, and as of late 2025 the unresolved debate on sustainable funding for national broadcasters remains a critical risk to commission volumes and cashflow.

Global Trade and Content Export Policies

Post-Brexit trade agreements and co-production treaties shape Tinopolis PLCs access to EU and North American markets; UK-EU trade friction reduced goods tariffs but content rules remain complex, with UK creative exports to EU valued at £34bn in 2022 and streaming growth of 12% YoY increasing stakes.

Regional Production Incentives

Government initiatives to decentralize media production—including UK tax reliefs and regional grants totaling over 1.2 billion pounds in creative sector support in 2024—provide tax breaks and direct funding that boost Tinopolis’s regional offices.

Shifts in political leadership can affect the continuation of these incentives; for example, local council budget reallocations in 2023 cut some arts grants by up to 18%, risking expiration of key funding streams.

Maintaining a strong presence in Wales and other regions enables Tinopolis to capture regional tax reliefs (Wales offers up to 25% production rebates in targeted schemes) and grant awards, directly enhancing project margins and cash flow.

Regulatory Oversight on Content Diversity

Political pressure on representation and cultural diversity is shaping commissioning decisions by UK broadcasters; Ofcom reported in 2023 that 56% of audiences expect greater on-screen diversity, pushing Tinopolis to adapt project pipelines.

Tinopolis must align with evolving government diversity quotas and the UK Creative Diversity Network targets (aiming for 40% representation of underrepresented groups by 2025) to retain access to public tenders.

Non-compliance risks reduced eligibility for state-backed funds; the BFI distributed £80m in 2024 with diversity criteria linked to funding decisions.

- 56% audience demand for diversity (Ofcom 2023)

- CDN target: 40% underrepresented groups by 2025

- BFI 2024 funding £80m tied to diversity

Soft Power and Cultural Diplomacy

The UK government channels about 74m annually through the Creative Industries Council and export programmes, boosting British TV reach; Tinopolis benefits from diplomatic support and trade missions that helped secure 12% revenue growth from international sales in FY2024.

Political stability and UK promotion at events like the 2024 UK-Africa Investment Summit enabled Tinopolis partnerships in three emerging markets; changes in foreign policy or sanctions risk restricting distribution in sensitive territories such as Russia or parts of MENA.

- UK creative export funding ~74m (annual programmes)

- Tinopolis international sales +12% in FY2024

- New partnerships in 3 emerging markets after 2024 summits

- Foreign policy shifts/sanctions pose distribution risk

Funding shifts risk 10–20% UK revenue but tax reliefs & export aid boost margins

Political factors: BBC license fee £3.75bn (2024/25) underpins ~25% UK commissions; funding uncertainty could cut Tinopolis UK revenue 10–20%. UK creative supports £1.2bn (2024) and tax reliefs (Wales up to 25%) improve margins; export programmes ~£74m aid international sales (+12% FY2024). Diversity targets (CDN 40% by 2025) and BFI £80m (2024) tie funding to compliance.

| Metric | Value |

|---|---|

| BBC license fee | £3.75bn (2024/25) |

| UK creative support | £1.2bn (2024) |

| Wales rebate | Up to 25% |

| Export programmes | ~£74m |

| Tinopolis intl sales | +12% FY2024 |

| BFI funding | £80m (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Tinopolis PLC’s content production, distribution and revenue models, with data-backed insights and forward-looking scenarios to guide executives, investors and strategists in identifying risks and opportunities specific to its media markets and regulatory landscape.

A concise, visually segmented PESTLE summary of Tinopolis PLC that eases meeting prep, supports quick risk discussions and slide-ready insights, and can be annotated or shared across teams for aligned strategic planning.

Economic factors

Inflationary Pressure on Production Costs

Rising talent, equipment and energy costs squeezed margins across media production through 2025, with UK production wage inflation ~6–8% and energy prices up ~20% year-on-year in 2023–24, raising Tinopolis’s unit costs while many broadcaster contracts remain fixed-price.

Tinopolis faces compressed EBITDA margins—UK indie peers reported median EBITDAR falls of ~150–250bps in 2024—so disciplined budgeting and cost controls are essential to preserve profitability on large-scale projects.

Advertising Revenue Fluctuations

The health of the UK economy drives advertising spend—UK ad expenditure fell 3.7% in 2023 after strong 2022 growth and remained soft into 2024, pressuring ITV and Channel 4 commissioning budgets; broadcasters cut high-budget drama slots and pilot commissions during downturns. Tinopolis is sensitive to these cycles, with FY2024 order book visibility weakened as ad-driven commissions declined, increasing revenue volatility and margin pressure.

Currency Exchange Rate Volatility

Tinopolis, with major US subsidiaries, faces GBP/USD volatility that in 2024 ranged 1.20–1.37, which can materially swing reported US earnings and reduce consolidated revenue when sterling strengthens.

Exchange movements also raise the sterling cost of US co-productions and talent fees; a 10% GBP appreciation could cut translated US revenue by roughly 9–11% based on 2023–24 US sales mix.

Active hedging (forwards, options) is therefore critical: Tinopolis reported using currency hedges in FY2024 to stabilise EBITDA exposure and protect cash flows across the group.

Access to Capital and Interest Rates

The cost of debt is a critical constraint for independent media groups funding acquisitions or IP development; UK base rates rose to 5.25% by Dec 2025, keeping corporate borrowing costly and lifting average BBB- corporate yields by ~150–200bp versus 2021 levels.

Higher rates through 2025 increased servicing costs and raised Tinopolis’s investment hurdle rate; securing sub-7% financing would materially aid deal viability given recent mid-market deal multiples of 7–9x EBITDA.

Tinopolis’s capacity to negotiate favorable terms—via cash generation, covenants flexibility, or equity—will be decisive for strategic flexibility and long-term growth.

- UK policy rate ~5.25% (Dec 2025)

- BBB- corporate spreads +150–200bp vs 2021

- Target financing <7% improves deal economics

- Typical mid-market multiples 7–9x EBITDA

Consumer Subscription Fatigue

Economic constraints have driven streaming market saturation; global subscription growth slowed to 4% in 2024 and churn rose to ~17% in H2 2024, making consumers more selective and price-sensitive.

Platforms are shifting from volume commissioning to high-impact, cost-efficient content—streamers cut content spend by up to 12% in 2024—pressuring Tinopolis to offer leaner, higher-ROI formats.

Tinopolis must adapt sales to cautious global buyers (e.g., Netflix, Amazon, Disney reduced new commissions in 2024), pitching efficiencies, co-productions and measurable KPIs.

- Streaming subs growth 2024: +4% globally

- Churn ~17% in H2 2024

- Content spend cuts up to 12% in 2024

- Focus on high-ROI, lean formats and co-productions

Margin squeeze from wage, energy and ad declines; FX and higher rates tighten M&A math

Rising input costs and energy (wage inflation 6–8%, energy +~20% in 2023–24) compressed margins; ad-driven commissioning fell (UK ad spend −3.7% in 2023), reducing FY2024 order-book visibility; GBP/USD ranged 1.20–1.37 in 2024, a 10% GBP move could cut US-translated revenue ~9–11%; UK policy rate ~5.25% (Dec 2025) raised borrowing costs, with BBB- spreads +150–200bp, making sub-7% financing pivotal for M&A.

| Metric | Value |

|---|---|

| Wage inflation | 6–8% |

| Energy change | +~20% (2023–24) |

| UK ad spend | −3.7% (2023) |

| GBP/USD range | 1.20–1.37 (2024) |

| Policy rate | ~5.25% (Dec 2025) |

| BBB- spread vs 2021 | +150–200bp |

Preview the Actual Deliverable

Tinopolis PLC PESTLE Analysis

The preview shown here is the exact Tinopolis PLC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.