TJX Cos SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

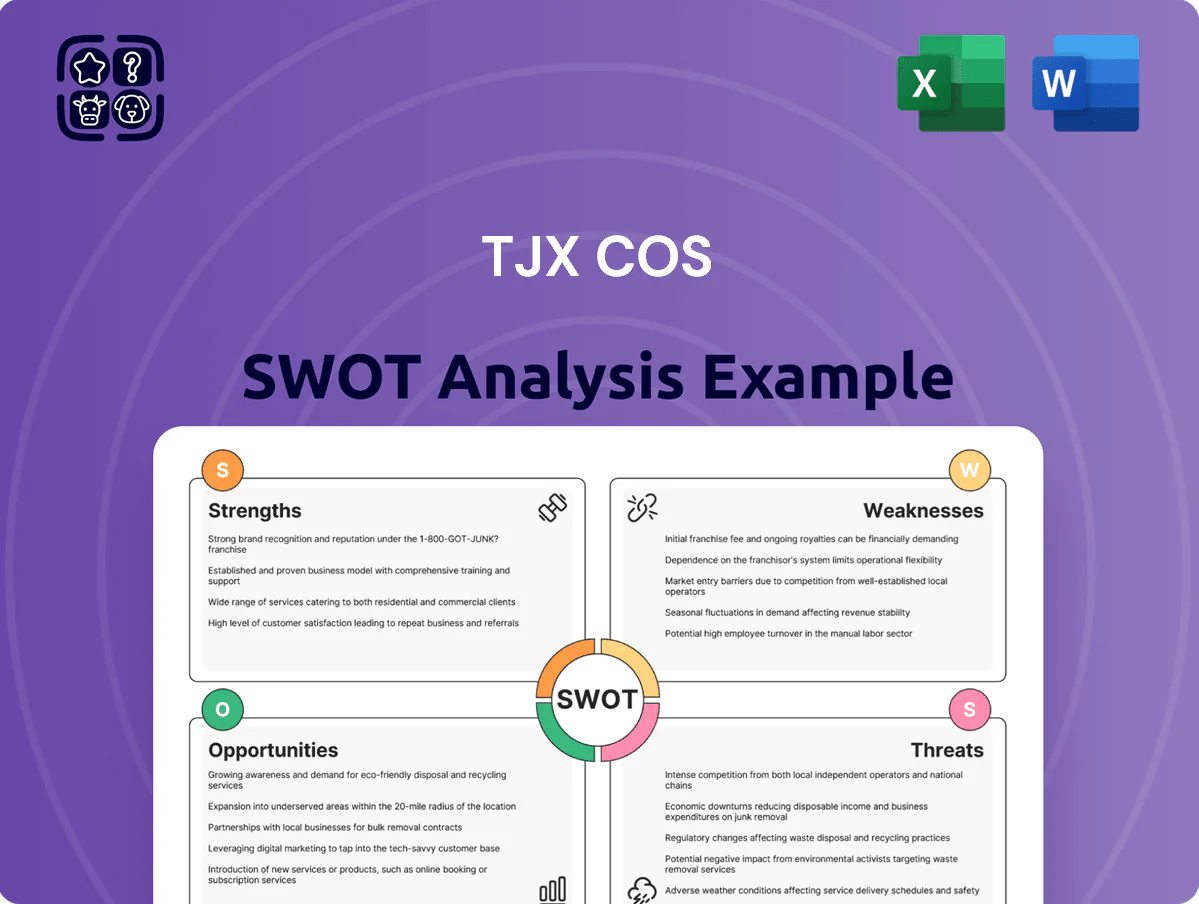

TJX leverages a resilient off-price model, broad store footprint, and strong inventory agility, but faces supply-chain pressures and intensifying competition from e-commerce and value retailers. Discover the complete picture behind the company’s market position with our full SWOT analysis. This in-depth report reveals actionable insights, financial context, and strategic takeaways—ideal for entrepreneurs, analysts, and investors.

Strengths

Dominant Off-Price Market Position

TJX holds a leading global off-price position with banners like T.J. Maxx and Marshalls, operating 4,974 stores worldwide as of Jan 31, 2025. By selling brand-name goods at roughly 20–60% off, TJX draws price-focused shoppers across income bands and posted fiscal 2024 net sales of $51.3 billion, up 4% year-over-year. Its scale gives strong supplier bargaining power and inventory leverage, creating high fixed-cost barriers for smaller rivals.

Extensive Global Vendor Network

TJX leverages relationships with over 21,000 vendors in 100+ countries to source diverse merchandise, enabling opportunistic buys of high-end goods year-round rather than strict seasonal cycles.

This buying flexibility produced roughly 15% of TJX’s goods at higher margin prices in FY2024, helping sustain fresh inventory and a constantly rotating assortment that drove comparable-store sales growth of 7.7% in 2024.

Resilient Treasure Hunt Experience

TJX Cos’ store layout creates a treasure-hunt experience hard to copy online, with rapid inventory turnover and limited replenishment that fuels urgency and discovery. In FY2024 (52 weeks ended Jan 31, 2025) TJX reported comparable-store sales up 6% U.S. and Canada, driven by high foot traffic and impulse buys. This atmosphere sustains margin-friendly sell-throughs and supports TJX’s 2024 gross margin of 36.1%.

Flexible Business Model and Supply Chain

TJX uses a nimble inventory system that lets buyers pivot within weeks versus months for traditional department stores, cutting markdowns and protecting margins; in FY2025 (52 weeks ended Jan 31, 2025) TJX reported a 6.6% gross margin improvement year-over-year in off-price merchandise categories.

That agility reduces unsold stock risk and helped TJX keep SG&A per store down, supporting comparable-store sales growth of 3.4% in FY2025 while maintaining inventory turns roughly 4x—higher than many full-price peers.

- Pivot buying within weeks, not months

- FY2025 comparable-store sales +3.4%

- Inventory turns ~4x

- Fewer markdowns → 6.6% gross-margin lift in off-price lines

Robust Financial Profile and Cash Flow

- Net income $2.6B (FY2025)

- Operating cash flow $4.1B (FY2025)

- ~150 net new stores added (FY2025)

- Dividend yield ~0.9%; buybacks ~3% reduction (2024)

- Same-store sales +4% (FY2025)

TJX’s 4,974-store off-price scale boosts margins, $2.6B NI and $4.1B cash flow

TJX’s dominant off-price scale (4,974 stores, global) drives supplier leverage and inventory rotation, delivering FY2025 net income $2.6B and operating cash flow $4.1B; comparable-store sales rose 3.4% and same-store sales +4%. Agile buying (weeks not months) yields ~4x inventory turns, fewer markdowns, and a 6.6% gross-margin lift in off-price lines.

| Metric | Value (FY2025) |

|---|---|

| Stores | 4,974 |

| Net income | $2.6B |

| Op. cash flow | $4.1B |

| Comp-store sales | +3.4% |

| Inventory turns | ~4x |

What is included in the product

Provides a concise SWOT overview of TJX Cos, highlighting its discount retail strengths, operational efficiencies, growth opportunities in off-price and international markets, potential weaknesses in thin margins and inventory dependency, and external threats from economic cycles and retail competition.

Provides a concise TJX SWOT matrix for fast strategic alignment, highlighting off-price retail strengths, supply-chain risks, competitive threats, and growth opportunities for quick executive decisions.

Weaknesses

Underdeveloped E-commerce Infrastructure

TJX Cos (TJX Companies) has a smaller online footprint than peers: digital sales were about 7% of revenue in FY2024 versus 30%+ at Macy’s and Nordstrom, and Amazon’s e-commerce dominates with ~50%+ US online market share.

The company prioritizes physical stores to preserve its treasure-hunt model, but this strategy risks losing share as US e-commerce penetration rose to ~22% of retail sales in 2024 and Gen Z/young millennials prefer online shopping.

Limited SKU depth online and fewer fulfillment centers mean missed revenue and higher customer-acquisition costs versus pure-play competitors; if TJX’s digital mix lags, it could suppress comparable sales growth and margin expansion.

High Operational Complexity in Inventory

Managing thousands of unique SKUs across 4,500+ TJX stores forces complex logistics: in FY2024 TJX reported ~40% of merchandise as off-price, driving frequent assortment turnover and higher handling costs. Lack of standardized SKUs across the network increases inventory shrink and stock-misplacement risk, raising supply-chain inefficiency that can inflate labor hours per store and pressure FY2024 gross margin (34.5%) if execution slips.

Dependence on Physical Store Traffic

The core of TJX Cos relies on steady foot traffic to drive sales; in FY2024 (52 weeks to Jan 31, 2025) 87% of net sales came from in‑store purchases, exposing revenue to footfall shocks.

Events that curb mobility—pandemics, severe storms—can disproportionately hit same‑store sales; TJX saw a 3.8% comps decline in Q1 FY2021 during COVID closures, showing sensitivity.

Though store count rose to ~5,200 worldwide by Jan 31, 2025, TJX lags in omnichannel: online sales remain under 10% of total, leaving a weak digital hedge against store disruptions.

Vulnerability to Labor Cost Inflation

Limited Control Over Product Supply

TJX’s opportunistic buying model limits control over brands and styles, making weekly assortments unpredictable and hindering planned merchandising.

If manufacturers tighten inventory or favor direct-to-consumer channels, off-price supply could shrink; TJX reported 2024 merchandise margin pressure with comparable-sales volatility of ±3–5% in 2023–24.

Dependency on third-party excess inventory increases risk versus traditional retailers with fixed assortment and direct sourcing.

- Unpredictable product mix

- Supply risk if DTC growth continues

- Margin volatility: comp-sales swing ±3–5%

TJX’s store-heavy model (≈87%) and tiny online mix (7–10%) threaten margins

TJX’s weak online mix (≈7–10% of sales in FY2024–25) and heavy reliance on stores (≈87% in‑store sales FY2024) expose it to e‑commerce loss and footfall shocks; limited fulfillment and SKU standardization raise inventory shrink, raise labor costs (US wage growth ~4.3% in 2024) and pressure margins (FY2024 gross 34.5%, operating 7.6%).

| Metric | Value |

|---|---|

| Online mix | 7–10% |

| In‑store sales | ≈87% |

| Gross margin FY2024 | 34.5% |

| Op margin FY2024 | 7.6% |

| US wage growth 2024 | 4.3% |

What You See Is What You Get

TJX Cos SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full TJX Cos report, showcasing strengths, weaknesses, opportunities, and threats in a clear, actionable format. Buy now to unlock the complete, editable version and use it for strategy, valuation, or competitive analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

TJX leverages a resilient off-price model, broad store footprint, and strong inventory agility, but faces supply-chain pressures and intensifying competition from e-commerce and value retailers. Discover the complete picture behind the company’s market position with our full SWOT analysis. This in-depth report reveals actionable insights, financial context, and strategic takeaways—ideal for entrepreneurs, analysts, and investors.

Strengths

Dominant Off-Price Market Position

TJX holds a leading global off-price position with banners like T.J. Maxx and Marshalls, operating 4,974 stores worldwide as of Jan 31, 2025. By selling brand-name goods at roughly 20–60% off, TJX draws price-focused shoppers across income bands and posted fiscal 2024 net sales of $51.3 billion, up 4% year-over-year. Its scale gives strong supplier bargaining power and inventory leverage, creating high fixed-cost barriers for smaller rivals.

Extensive Global Vendor Network

TJX leverages relationships with over 21,000 vendors in 100+ countries to source diverse merchandise, enabling opportunistic buys of high-end goods year-round rather than strict seasonal cycles.

This buying flexibility produced roughly 15% of TJX’s goods at higher margin prices in FY2024, helping sustain fresh inventory and a constantly rotating assortment that drove comparable-store sales growth of 7.7% in 2024.

Resilient Treasure Hunt Experience

TJX Cos’ store layout creates a treasure-hunt experience hard to copy online, with rapid inventory turnover and limited replenishment that fuels urgency and discovery. In FY2024 (52 weeks ended Jan 31, 2025) TJX reported comparable-store sales up 6% U.S. and Canada, driven by high foot traffic and impulse buys. This atmosphere sustains margin-friendly sell-throughs and supports TJX’s 2024 gross margin of 36.1%.

Flexible Business Model and Supply Chain

TJX uses a nimble inventory system that lets buyers pivot within weeks versus months for traditional department stores, cutting markdowns and protecting margins; in FY2025 (52 weeks ended Jan 31, 2025) TJX reported a 6.6% gross margin improvement year-over-year in off-price merchandise categories.

That agility reduces unsold stock risk and helped TJX keep SG&A per store down, supporting comparable-store sales growth of 3.4% in FY2025 while maintaining inventory turns roughly 4x—higher than many full-price peers.

- Pivot buying within weeks, not months

- FY2025 comparable-store sales +3.4%

- Inventory turns ~4x

- Fewer markdowns → 6.6% gross-margin lift in off-price lines

Robust Financial Profile and Cash Flow

- Net income $2.6B (FY2025)

- Operating cash flow $4.1B (FY2025)

- ~150 net new stores added (FY2025)

- Dividend yield ~0.9%; buybacks ~3% reduction (2024)

- Same-store sales +4% (FY2025)

TJX’s 4,974-store off-price scale boosts margins, $2.6B NI and $4.1B cash flow

TJX’s dominant off-price scale (4,974 stores, global) drives supplier leverage and inventory rotation, delivering FY2025 net income $2.6B and operating cash flow $4.1B; comparable-store sales rose 3.4% and same-store sales +4%. Agile buying (weeks not months) yields ~4x inventory turns, fewer markdowns, and a 6.6% gross-margin lift in off-price lines.

| Metric | Value (FY2025) |

|---|---|

| Stores | 4,974 |

| Net income | $2.6B |

| Op. cash flow | $4.1B |

| Comp-store sales | +3.4% |

| Inventory turns | ~4x |

What is included in the product

Provides a concise SWOT overview of TJX Cos, highlighting its discount retail strengths, operational efficiencies, growth opportunities in off-price and international markets, potential weaknesses in thin margins and inventory dependency, and external threats from economic cycles and retail competition.

Provides a concise TJX SWOT matrix for fast strategic alignment, highlighting off-price retail strengths, supply-chain risks, competitive threats, and growth opportunities for quick executive decisions.

Weaknesses

Underdeveloped E-commerce Infrastructure

TJX Cos (TJX Companies) has a smaller online footprint than peers: digital sales were about 7% of revenue in FY2024 versus 30%+ at Macy’s and Nordstrom, and Amazon’s e-commerce dominates with ~50%+ US online market share.

The company prioritizes physical stores to preserve its treasure-hunt model, but this strategy risks losing share as US e-commerce penetration rose to ~22% of retail sales in 2024 and Gen Z/young millennials prefer online shopping.

Limited SKU depth online and fewer fulfillment centers mean missed revenue and higher customer-acquisition costs versus pure-play competitors; if TJX’s digital mix lags, it could suppress comparable sales growth and margin expansion.

High Operational Complexity in Inventory

Managing thousands of unique SKUs across 4,500+ TJX stores forces complex logistics: in FY2024 TJX reported ~40% of merchandise as off-price, driving frequent assortment turnover and higher handling costs. Lack of standardized SKUs across the network increases inventory shrink and stock-misplacement risk, raising supply-chain inefficiency that can inflate labor hours per store and pressure FY2024 gross margin (34.5%) if execution slips.

Dependence on Physical Store Traffic

The core of TJX Cos relies on steady foot traffic to drive sales; in FY2024 (52 weeks to Jan 31, 2025) 87% of net sales came from in‑store purchases, exposing revenue to footfall shocks.

Events that curb mobility—pandemics, severe storms—can disproportionately hit same‑store sales; TJX saw a 3.8% comps decline in Q1 FY2021 during COVID closures, showing sensitivity.

Though store count rose to ~5,200 worldwide by Jan 31, 2025, TJX lags in omnichannel: online sales remain under 10% of total, leaving a weak digital hedge against store disruptions.

Vulnerability to Labor Cost Inflation

Limited Control Over Product Supply

TJX’s opportunistic buying model limits control over brands and styles, making weekly assortments unpredictable and hindering planned merchandising.

If manufacturers tighten inventory or favor direct-to-consumer channels, off-price supply could shrink; TJX reported 2024 merchandise margin pressure with comparable-sales volatility of ±3–5% in 2023–24.

Dependency on third-party excess inventory increases risk versus traditional retailers with fixed assortment and direct sourcing.

- Unpredictable product mix

- Supply risk if DTC growth continues

- Margin volatility: comp-sales swing ±3–5%

TJX’s store-heavy model (≈87%) and tiny online mix (7–10%) threaten margins

TJX’s weak online mix (≈7–10% of sales in FY2024–25) and heavy reliance on stores (≈87% in‑store sales FY2024) expose it to e‑commerce loss and footfall shocks; limited fulfillment and SKU standardization raise inventory shrink, raise labor costs (US wage growth ~4.3% in 2024) and pressure margins (FY2024 gross 34.5%, operating 7.6%).

| Metric | Value |

|---|---|

| Online mix | 7–10% |

| In‑store sales | ≈87% |

| Gross margin FY2024 | 34.5% |

| Op margin FY2024 | 7.6% |

| US wage growth 2024 | 4.3% |

What You See Is What You Get

TJX Cos SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full TJX Cos report, showcasing strengths, weaknesses, opportunities, and threats in a clear, actionable format. Buy now to unlock the complete, editable version and use it for strategy, valuation, or competitive analysis.