Tenaga Nasional PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

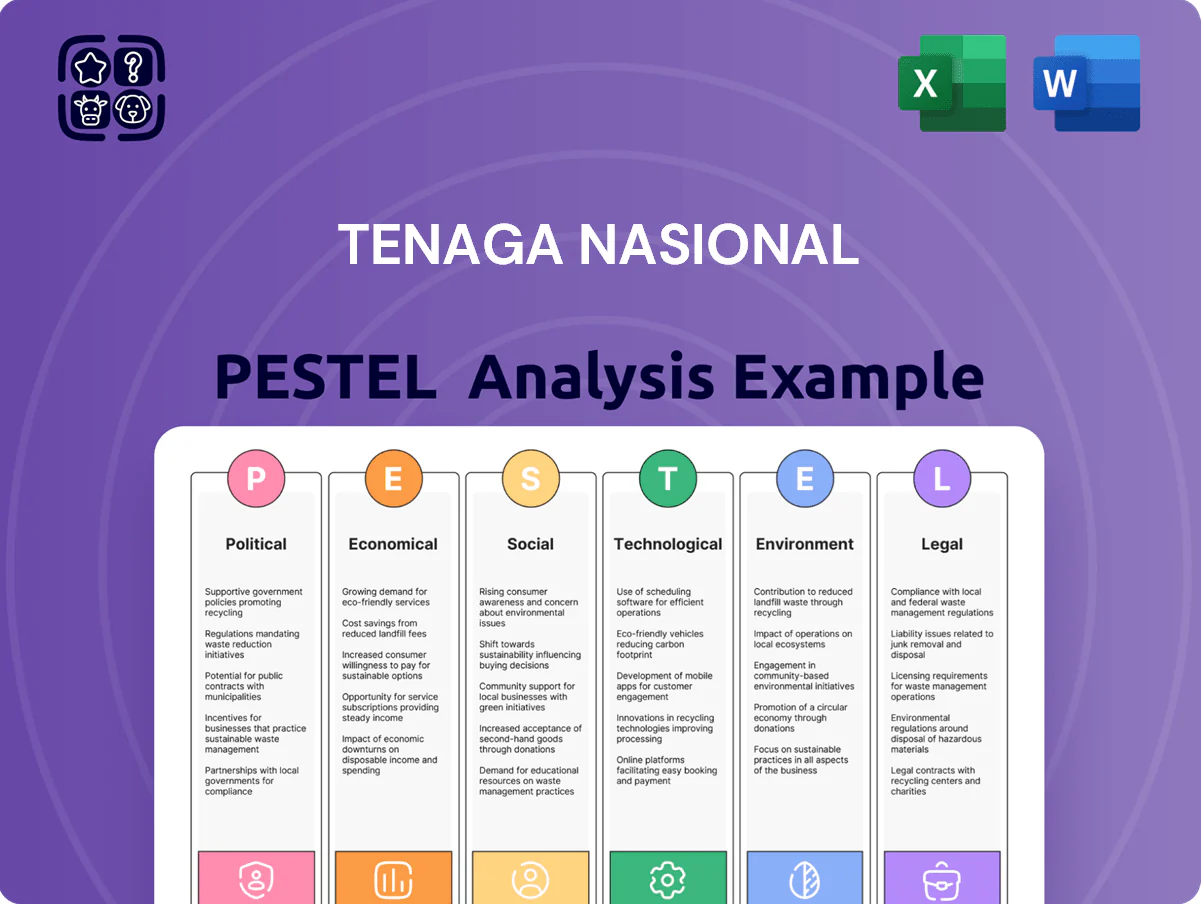

Stay ahead with our concise PESTLE snapshot of Tenaga Nasional—revealing how politics, economics, tech, and environmental trends shape its growth and risks; perfect for investors and strategists who need immediate, actionable context. Purchase the full PESTLE to access detailed drivers, implications, and ready-to-use slides that turn insight into competitive advantage.

Political factors

National Energy Transition Roadmap Alignment

TNB remains Malaysia’s primary vehicle for the National Energy Transition Roadmap as the country targets 70% renewable capacity by 2050, with TNB tasked to deliver large-scale solar and hybrid hydro-floating solar projects contributing to its 2030 interim targets; government policy channels and incentives prioritized TNB projects through end-2025. In 2024 the government allocated MYR 8.2 billion for energy transition initiatives, directing much of the grid expansion and R&D funding to TNB to integrate an expected 15–20 GW of new renewables by 2030. TNB’s strategic priority status secures preferential access to land, permits and infrastructure funding, strengthening its regulated asset base and long-term revenue visibility.

ASEAN Power Grid Integration

Political cooperation in ASEAN has deepened to enable cross-border electricity trading, with the ASEAN Power Grid target to connect 11 member states; interconnection projects grew 18% regionally in 2024. TNB is central to Malaysia’s role, leveraging government-to-government pacts to increase links with Thailand, Singapore and Laos via planned capacity transfers of up to 3–5 GW by 2030. These ties position TNB to export green energy—supporting projected export revenues of RM1.2–2.0 billion annually by mid-2020s.

Government Linked Company Status

As a major government-linked company, TNB’s strategic direction is overseen by the Ministry of Finance and the Ministry of Energy Transition and Water, aligning with national targets such as Malaysia’s 2050 net-zero goal; the government stake (among largest shareholders) supports credit ratings—TNB held an A- by S&P in 2024—facilitating cheaper funding for projects like the RM20bn grid modernization plan. However, this status forces trade-offs between profitability and socio-economic mandates, including subsidized tariffs and rural electrification commitments that can compress margins.

Energy Security and Sovereignty

The Malaysian government enforces energy sovereignty policies requiring Tenaga Nasional Berhad to diversify its fuel mix—gas, coal, hydro, and increasing solar—aiming to cut LNG import reliance (imports were about 36% of fuel mix in 2023) and target 31% renewables by 2025 under national plans.

Political mandates oblige TNB to hold strategic reserves and invest in domestic infrastructure; TNB’s planned RM32 billion grid and generation investments (2024–2026) support industrial demand growth and resilience.

These measures position TNB as a stability anchor during global volatility, reducing supply-risk exposure and supporting Malaysia’s GDP-linked energy security needs.

- Government target: 31% renewables by 2025

- TNB investments: ~RM32 billion (2024–2026)

- 2023 LNG/imports share: ~36% of fuel mix

- Mandates: strategic reserves + domestic infrastructure

Regulatory Stability and Policy Continuity

The relative political stability in Malaysia through late 2025 has supported predictable long-term utility planning, enabling Tenaga Nasional Berhad to proceed with multiyear investments such as its RM30–RM40 billion grid modernization roadmap (2023–2028).

Consistent Imbalance Cost Pass-Through policies have allowed TNB to pass on fuel-cost volatility with limited political interference; fuel-related tariff adjustments accounted for ~12% of average tariff revisions in 2024–2025.

This policy predictability underpins investor confidence, helping TNB secure financing—RM15 billion in bond issuances in 2024—critical for capital expenditure programs.

- Stable politics → predictable investment climate

- ICPT consistency → mitigated fuel-price risk (~12% tariff impact)

- Facilitated financing → RM15bn bonds (2024); RM30–40bn capex plan

TNB: Driving Malaysia’s Net‑Zero with MYR8.2bn Support, RM32–40bn Capex & 3–5GW Exports

TNB is central to Malaysia’s 2050 net-zero and 2030 interim targets, receiving policy support, preferential permits and funding (government allocated MYR 8.2bn for energy transition in 2024) while balancing social mandates that compress margins; ASEAN grid ties enable 3–5GW export potential (~RM1.2–2.0bn pa). Political stability and ICPT predictability aided RM15bn bond raises (2024) and RM32bn–RM40bn capex plans (2024–2028).

| Metric | Value |

|---|---|

| 2024 energy transition budget | MYR 8.2bn |

| Export potential | 3–5 GW / RM1.2–2.0bn pa |

| Bonds 2024 | RM15bn |

| Capex 2024–28 | RM32–40bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Tenaga Nasional across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, ready-to-use PESTLE summary of Tenaga Nasional that highlights external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Incentive Based Regulation Framework

Transition into RP4 gives TNB a defined allowable return on regulated assets—recently set at around 7–8% real post-tax—enabling recovery of MYR 25–30 billion planned capex through 2026 while preserving shareholder margins.

The transparent IBR framework supports multi-year revenue certainty, aiding long-term financial planning and contributing to TNB’s stable credit metrics (rated A-/A3 by 2025 agencies).

Data Center Driven Demand Growth

Malaysia has become a Southeast Asian data center hub, with commissioned capacity forecasted to exceed 700 MW by 2025, driving incremental national electricity demand estimated at 4–6 TWh annually; Tenaga Nasional (TNB) is a primary supplier for these facilities. TNB benefits from stable, high-load contracts as hyperscale and colocation centers prefer reliable and increasingly green power, with corporate green procurement rising ~20% YoY in 2024. This industrial segment offsets weaker residential and industrial growth, contributing material high-volume revenue and improving load-factor economics for TNB.

Fuel Price Volatility and ICPT Mechanism

Fluctuations in global coal and LNG prices pushed TNB’s fuel expense volatility, with Indonesian coal rising ~45% in 2024 and LNG Henry Hub-equivalent swings of ±30% YTD, stressing operational costs and cash flow.

The Imbalance Cost Pass-Through (ICPT), adjusted semi-annually, remains vital—ICPT helped recover MYR 1.2bn in FY2024 fuel differentials—allowing tariff alignment to actual fuel costs.

Efficient ICPT management is essential to avoid liquidity pressure when commodity price spikes occur, as sudden coal price surges in 2024 created short-term working capital gaps for generators.

Currency Exchange Rate Sensitivity

Tenaga Nasional (TNB) is exposed to MYR/USD fluctuations—Malaysia’s MYR weakened ~5% vs USD in 2023, raising coal import costs after 2022-23 global coal prices averaged $150–$200/ton; foreign-denominated debt servicing also rises, affecting margins.

TNB uses hedging (FX forwards, FX swaps, fuel price hedges) and diversified procurement to limit volatility; in FY2024 TNB reported FX gains/losses impacting net finance costs by MYR hundreds of millions.

- MYR volatility increases import and debt servicing costs

- Coal prices $150–$200/ton (2022–23) magnify exposure

- Hedging instruments and procurement diversification mitigate risk

- FX effects altered FY2024 net finance costs by MYR hundreds of millions

Capital Expenditure for Grid Modernization

The national grid upgrade to integrate 20 GW of renewables by 2035 will require multi-billion ringgit capex; estimates suggest TNB faces RM20–30 billion in transmission and smart-grid investments through 2030.

TNB must balance shareholder dividends (FY2024 payout ~RM3.5bn) with reinvestment in HV lines and digitalization to meet reliability and decarbonization targets.

Management’s 2025 priority is securing low-cost financing—green bonds and concessional loans—to lower WACC and preserve cash for capex.

- Estimated capex need RM20–30bn (to 2030)

- FY2024 dividends ~RM3.5bn

- Target: 20 GW renewables by 2035

- Focus: green bonds, concessional financing to reduce WACC

TNB: 7–8% allowed return, MYR25–30bn capex to 2026; data centers boost load

RP4 allows ~7–8% real post-tax returns enabling recovery of MYR25–30bn capex to 2026; TNB rated A-/A3 (2025). Data center demand (>700MW by 2025) adds 4–6TWh/yr, supporting load factors. Coal/LNG volatility (coal +45% in 2024) and MYR ~5% USD weakness raise fuel and FX costs; FY2024 dividends ~RM3.5bn; projected TNB transmission capex RM20–30bn to 2030.

| Metric | Value |

|---|---|

| Allowed return | 7–8% real post-tax |

| Capex (to 2026) | MYR25–30bn |

| Data center demand | 700+ MW; 4–6 TWh/yr |

| Coal change 2024 | +45% |

| Dividends FY2024 | RM3.5bn |

| Transmission capex to 2030 | RM20–30bn |

Preview Before You Purchase

Tenaga Nasional PESTLE Analysis

The preview shown here is the exact Tenaga Nasional PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Stay ahead with our concise PESTLE snapshot of Tenaga Nasional—revealing how politics, economics, tech, and environmental trends shape its growth and risks; perfect for investors and strategists who need immediate, actionable context. Purchase the full PESTLE to access detailed drivers, implications, and ready-to-use slides that turn insight into competitive advantage.

Political factors

National Energy Transition Roadmap Alignment

TNB remains Malaysia’s primary vehicle for the National Energy Transition Roadmap as the country targets 70% renewable capacity by 2050, with TNB tasked to deliver large-scale solar and hybrid hydro-floating solar projects contributing to its 2030 interim targets; government policy channels and incentives prioritized TNB projects through end-2025. In 2024 the government allocated MYR 8.2 billion for energy transition initiatives, directing much of the grid expansion and R&D funding to TNB to integrate an expected 15–20 GW of new renewables by 2030. TNB’s strategic priority status secures preferential access to land, permits and infrastructure funding, strengthening its regulated asset base and long-term revenue visibility.

ASEAN Power Grid Integration

Political cooperation in ASEAN has deepened to enable cross-border electricity trading, with the ASEAN Power Grid target to connect 11 member states; interconnection projects grew 18% regionally in 2024. TNB is central to Malaysia’s role, leveraging government-to-government pacts to increase links with Thailand, Singapore and Laos via planned capacity transfers of up to 3–5 GW by 2030. These ties position TNB to export green energy—supporting projected export revenues of RM1.2–2.0 billion annually by mid-2020s.

Government Linked Company Status

As a major government-linked company, TNB’s strategic direction is overseen by the Ministry of Finance and the Ministry of Energy Transition and Water, aligning with national targets such as Malaysia’s 2050 net-zero goal; the government stake (among largest shareholders) supports credit ratings—TNB held an A- by S&P in 2024—facilitating cheaper funding for projects like the RM20bn grid modernization plan. However, this status forces trade-offs between profitability and socio-economic mandates, including subsidized tariffs and rural electrification commitments that can compress margins.

Energy Security and Sovereignty

The Malaysian government enforces energy sovereignty policies requiring Tenaga Nasional Berhad to diversify its fuel mix—gas, coal, hydro, and increasing solar—aiming to cut LNG import reliance (imports were about 36% of fuel mix in 2023) and target 31% renewables by 2025 under national plans.

Political mandates oblige TNB to hold strategic reserves and invest in domestic infrastructure; TNB’s planned RM32 billion grid and generation investments (2024–2026) support industrial demand growth and resilience.

These measures position TNB as a stability anchor during global volatility, reducing supply-risk exposure and supporting Malaysia’s GDP-linked energy security needs.

- Government target: 31% renewables by 2025

- TNB investments: ~RM32 billion (2024–2026)

- 2023 LNG/imports share: ~36% of fuel mix

- Mandates: strategic reserves + domestic infrastructure

Regulatory Stability and Policy Continuity

The relative political stability in Malaysia through late 2025 has supported predictable long-term utility planning, enabling Tenaga Nasional Berhad to proceed with multiyear investments such as its RM30–RM40 billion grid modernization roadmap (2023–2028).

Consistent Imbalance Cost Pass-Through policies have allowed TNB to pass on fuel-cost volatility with limited political interference; fuel-related tariff adjustments accounted for ~12% of average tariff revisions in 2024–2025.

This policy predictability underpins investor confidence, helping TNB secure financing—RM15 billion in bond issuances in 2024—critical for capital expenditure programs.

- Stable politics → predictable investment climate

- ICPT consistency → mitigated fuel-price risk (~12% tariff impact)

- Facilitated financing → RM15bn bonds (2024); RM30–40bn capex plan

TNB: Driving Malaysia’s Net‑Zero with MYR8.2bn Support, RM32–40bn Capex & 3–5GW Exports

TNB is central to Malaysia’s 2050 net-zero and 2030 interim targets, receiving policy support, preferential permits and funding (government allocated MYR 8.2bn for energy transition in 2024) while balancing social mandates that compress margins; ASEAN grid ties enable 3–5GW export potential (~RM1.2–2.0bn pa). Political stability and ICPT predictability aided RM15bn bond raises (2024) and RM32bn–RM40bn capex plans (2024–2028).

| Metric | Value |

|---|---|

| 2024 energy transition budget | MYR 8.2bn |

| Export potential | 3–5 GW / RM1.2–2.0bn pa |

| Bonds 2024 | RM15bn |

| Capex 2024–28 | RM32–40bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Tenaga Nasional across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, ready-to-use PESTLE summary of Tenaga Nasional that highlights external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Incentive Based Regulation Framework

Transition into RP4 gives TNB a defined allowable return on regulated assets—recently set at around 7–8% real post-tax—enabling recovery of MYR 25–30 billion planned capex through 2026 while preserving shareholder margins.

The transparent IBR framework supports multi-year revenue certainty, aiding long-term financial planning and contributing to TNB’s stable credit metrics (rated A-/A3 by 2025 agencies).

Data Center Driven Demand Growth

Malaysia has become a Southeast Asian data center hub, with commissioned capacity forecasted to exceed 700 MW by 2025, driving incremental national electricity demand estimated at 4–6 TWh annually; Tenaga Nasional (TNB) is a primary supplier for these facilities. TNB benefits from stable, high-load contracts as hyperscale and colocation centers prefer reliable and increasingly green power, with corporate green procurement rising ~20% YoY in 2024. This industrial segment offsets weaker residential and industrial growth, contributing material high-volume revenue and improving load-factor economics for TNB.

Fuel Price Volatility and ICPT Mechanism

Fluctuations in global coal and LNG prices pushed TNB’s fuel expense volatility, with Indonesian coal rising ~45% in 2024 and LNG Henry Hub-equivalent swings of ±30% YTD, stressing operational costs and cash flow.

The Imbalance Cost Pass-Through (ICPT), adjusted semi-annually, remains vital—ICPT helped recover MYR 1.2bn in FY2024 fuel differentials—allowing tariff alignment to actual fuel costs.

Efficient ICPT management is essential to avoid liquidity pressure when commodity price spikes occur, as sudden coal price surges in 2024 created short-term working capital gaps for generators.

Currency Exchange Rate Sensitivity

Tenaga Nasional (TNB) is exposed to MYR/USD fluctuations—Malaysia’s MYR weakened ~5% vs USD in 2023, raising coal import costs after 2022-23 global coal prices averaged $150–$200/ton; foreign-denominated debt servicing also rises, affecting margins.

TNB uses hedging (FX forwards, FX swaps, fuel price hedges) and diversified procurement to limit volatility; in FY2024 TNB reported FX gains/losses impacting net finance costs by MYR hundreds of millions.

- MYR volatility increases import and debt servicing costs

- Coal prices $150–$200/ton (2022–23) magnify exposure

- Hedging instruments and procurement diversification mitigate risk

- FX effects altered FY2024 net finance costs by MYR hundreds of millions

Capital Expenditure for Grid Modernization

The national grid upgrade to integrate 20 GW of renewables by 2035 will require multi-billion ringgit capex; estimates suggest TNB faces RM20–30 billion in transmission and smart-grid investments through 2030.

TNB must balance shareholder dividends (FY2024 payout ~RM3.5bn) with reinvestment in HV lines and digitalization to meet reliability and decarbonization targets.

Management’s 2025 priority is securing low-cost financing—green bonds and concessional loans—to lower WACC and preserve cash for capex.

- Estimated capex need RM20–30bn (to 2030)

- FY2024 dividends ~RM3.5bn

- Target: 20 GW renewables by 2035

- Focus: green bonds, concessional financing to reduce WACC

TNB: 7–8% allowed return, MYR25–30bn capex to 2026; data centers boost load

RP4 allows ~7–8% real post-tax returns enabling recovery of MYR25–30bn capex to 2026; TNB rated A-/A3 (2025). Data center demand (>700MW by 2025) adds 4–6TWh/yr, supporting load factors. Coal/LNG volatility (coal +45% in 2024) and MYR ~5% USD weakness raise fuel and FX costs; FY2024 dividends ~RM3.5bn; projected TNB transmission capex RM20–30bn to 2030.

| Metric | Value |

|---|---|

| Allowed return | 7–8% real post-tax |

| Capex (to 2026) | MYR25–30bn |

| Data center demand | 700+ MW; 4–6 TWh/yr |

| Coal change 2024 | +45% |

| Dividends FY2024 | RM3.5bn |

| Transmission capex to 2030 | RM20–30bn |

Preview Before You Purchase

Tenaga Nasional PESTLE Analysis

The preview shown here is the exact Tenaga Nasional PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.