Tompkins Financial Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Tompkins Financial operates in a dynamic banking landscape, facing pressures from established competitors and the ever-present threat of new digital entrants. Understanding the intensity of buyer bargaining power and the availability of substitute financial products is crucial for their strategic positioning.

The complete report reveals the real forces shaping Tompkins Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Core Technology Providers

Tompkins Financial's reliance on specialized financial software, core banking systems, and cybersecurity solutions from a limited number of vendors significantly influences supplier power. For instance, in 2024, the financial services industry continued to see consolidation among key technology providers, meaning fewer options for essential infrastructure. This dependence can grant these technology suppliers considerable leverage, especially if their offerings are critical and difficult to replace.

When a supplier provides unique or indispensable technology, Tompkins Financial's ability to negotiate favorable terms diminishes. High switching costs associated with migrating core banking systems, for example, can lock the company into existing relationships, further strengthening the supplier's bargaining position. This reality means that the cost and complexity of changing providers are major factors in Tompkins Financial's supplier relationships.

Availability of Human Capital

The demand for skilled financial professionals, particularly in compliance, data analytics, and digital banking, is high, giving these employees considerable bargaining power. This means Tompkins Financial, like many in the industry, faces situations where talented individuals can command better compensation and benefits, impacting labor costs.

A shortage of qualified talent within Tompkins Financial's specific operating regions directly translates into increased bargaining power for available human capital. For instance, in 2024, the U.S. financial services sector continued to experience a tight labor market for specialized roles, with reports indicating salary increases of 5-10% for in-demand positions.

This scarcity can lead to higher recruitment expenses and longer hiring timelines for Tompkins Financial, as they compete for a limited pool of experienced professionals. The need to attract and retain top talent in these critical areas directly influences the bank's operational efficiency and cost structure.

Cost of Data and Information Services

Financial institutions like Tompkins Financial rely significantly on data and information service providers for crucial functions such as market analysis, credit scoring, and regulatory compliance. The cost of these essential services directly influences operational expenses. For example, in 2024, the global market for financial data and analytics was valued at over $30 billion, indicating substantial spending by firms in this sector.

When data providers offer highly specialized or unique datasets, or if the market for certain types of financial data is concentrated among a few suppliers, these suppliers gain considerable bargaining power. This allows them to potentially charge premium prices for their services, directly impacting Tompkins Financial's cost structure and profitability.

Regulatory Compliance Service Providers

The bargaining power of regulatory compliance service providers for Tompkins Financial is significant due to the intricate and constantly changing landscape of financial regulations. Adherence to these rules, whether it's for banking operations, investment advisory, or capital markets, often necessitates specialized legal and consulting expertise.

A limited pool of firms possesses the deep, niche knowledge required for specific compliance areas, granting them considerable leverage. For instance, as of early 2024, the cost of specialized financial regulatory consulting can range from several hundred to over a thousand dollars per hour, depending on the firm's reputation and the complexity of the service.

- Specialized Expertise: Firms with proven track records in areas like anti-money laundering (AML) or Know Your Customer (KYC) regulations command higher fees.

- Regulatory Changes: The ongoing updates to regulations, such as those impacting data privacy or capital requirements, create a continuous demand for expert guidance.

- Limited Alternatives: For highly specific or emerging regulatory challenges, the number of qualified service providers can be very small, reducing Tompkins Financial's ability to negotiate favorable terms.

Infrastructure and Utility Providers

While infrastructure and utility providers might seem like basic commodities, their role in ensuring reliable and secure operations for financial institutions like Tompkins Financial is paramount. This includes everything from stable internet connectivity and consistent power supply to the physical security of branches.

In specific geographic regions, the availability of high-quality, redundant services from these providers can be limited. This scarcity can grant these essential utility suppliers a degree of bargaining power, as Tompkins Financial, like other banks, relies heavily on uninterrupted service to maintain customer trust and operational efficiency.

For instance, in 2024, the increasing demand for robust cloud infrastructure and cybersecurity services, coupled with potential localized supply chain disruptions impacting hardware availability, could strengthen the position of key providers. Financial institutions are often locked into contracts with these providers, further limiting their ability to switch easily and thus enhancing supplier leverage.

- Critical Reliance: Financial institutions depend on uninterrupted infrastructure services for daily operations and customer access.

- Limited Alternatives: In certain areas, the choice of high-quality, redundant utility providers is restricted.

- 2024 Market Dynamics: Increased demand for cloud and cybersecurity, alongside potential supply chain issues, can bolster supplier bargaining power.

- Contractual Lock-in: Existing agreements often make switching providers difficult, reinforcing supplier leverage.

Supplier Power Dynamics: Tompkins Financial's 2024 Strategic Challenge

Tompkins Financial's bargaining power with suppliers is influenced by the concentration of providers for critical services like core banking software and cybersecurity. In 2024, industry consolidation meant fewer options for essential technology, giving these suppliers significant leverage, especially when their solutions are difficult to replace.

The cost and complexity of switching providers, particularly for core banking systems, often result in contractual lock-in. This dependence limits Tompkins Financial's ability to negotiate favorable terms, as the switching costs can be substantial, reinforcing the supplier's strong position.

The bargaining power of suppliers for Tompkins Financial is amplified when they offer unique or indispensable technology. High switching costs associated with essential systems like core banking platforms can lock the company into existing relationships, thereby strengthening the supplier's leverage and impacting negotiation outcomes.

| Supplier Type | Key Factors Influencing Bargaining Power | Impact on Tompkins Financial | 2024 Market Trend |

| Technology Providers (Core Banking, Cybersecurity) | Limited number of vendors, high switching costs, specialized offerings | Reduced negotiation leverage, potentially higher costs | Industry consolidation, increased demand for advanced solutions |

| Data & Analytics Providers | Concentrated market for specialized data, unique datasets | Potential for premium pricing, impact on operational costs | Market value exceeding $30 billion globally, focus on AI-driven insights |

| Regulatory Compliance Services | Niche expertise, complex and evolving regulations, limited qualified firms | Higher hourly rates for specialized consulting, continuous demand for guidance | Costs ranging from $300-$1000+ per hour for expert advice |

What is included in the product

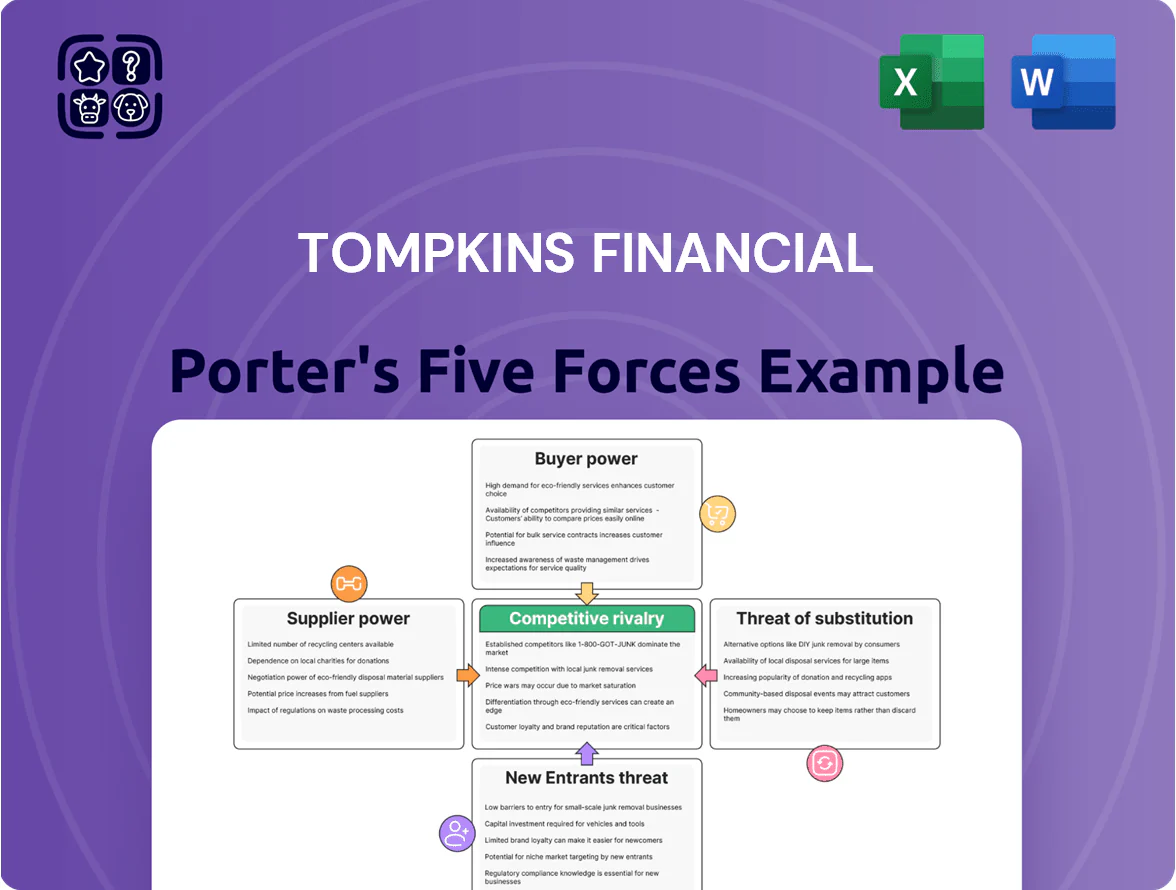

This Porter's Five Forces analysis provides a comprehensive examination of the competitive landscape for Tompkins Financial, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly identify and address competitive pressures with a dynamic, visual representation of each force, simplifying complex market dynamics.

Customers Bargaining Power

Low Switching Costs for Standard Products

For standard banking products, the ease with which customers can switch providers significantly amplifies their bargaining power. This is particularly true for basic offerings like checking accounts, savings accounts, and common loan types. For example, in 2024, the average consumer holds over four bank accounts, indicating a willingness to spread their business and switch providers if better terms are available.

This low barrier to entry for customers means Tompkins Financial must actively compete on price and service quality. If a competitor offers a higher interest rate on savings or lower fees on checking, customers can readily move their funds. This dynamic forces Tompkins Financial to maintain competitive pricing and invest in customer service to prevent attrition and retain its customer base.

Access to Information and Price Transparency

Customers today have an unprecedented amount of information at their fingertips. Online resources provide easy access to comparative data on interest rates, fees, and product features offered by various financial institutions, including Tompkins Financial. This readily available price transparency empowers consumers to make informed decisions and seek out the best value, directly impacting the bank's pricing strategies.

Commoditization of Basic Financial Services

Many fundamental banking services are viewed by customers as interchangeable commodities. This perception means decisions often hinge on price or ease of access, directly boosting customer bargaining power. For instance, in 2024, the average interest rate on a savings account across major US banks hovered around 0.40%, highlighting how price competition drives customer choices in basic offerings.

Concentration of Large Commercial Clients

While Tompkins Financial serves a broad base of local communities, the concentration of its commercial loan portfolio or deposit accounts among a few large businesses can grant these clients significant bargaining power. Such large commercial clients, often possessing substantial financial resources, can leverage their importance to Tompkins by negotiating for more favorable loan rates, lower deposit fees, or enhanced service packages. This ability to demand better terms directly impacts the bank's net interest margin and overall profitability, as these key clients can exert considerable pressure on pricing and service levels.

For instance, if a single large corporate client represents over 5% of Tompkins' total commercial loans, their departure or demand for significantly reduced rates could have a noticeable effect. In 2024, the banking sector generally saw continued competition for large commercial deposits, with some institutions offering tiered rates that favored higher balances, a trend that could empower large clients to seek out the most advantageous terms.

- Concentrated Commercial Client Base: A few large businesses holding a significant portion of Tompkins' commercial loans or deposits can wield considerable influence.

- Negotiating Favorable Terms: These clients can negotiate for lower interest rates on loans or better terms on deposits, impacting Tompkins' profitability.

- Impact on Profitability: The ability of large clients to secure preferential treatment can directly affect the bank's net interest margin and fee income.

- Industry Trends: In 2024, competition for large commercial deposits intensified, potentially increasing the bargaining power of these clients.

Rise of Digital-First Banking Options

The proliferation of digital-first banking options significantly amplifies customer bargaining power. Online-only banks and fintech platforms, often operating with lower overheads, can offer more attractive terms, such as reduced fees and higher interest rates on deposits. This readily available alternative compels traditional institutions like Tompkins Financial to be more competitive.

For instance, in 2024, the digital banking sector continued its rapid expansion, with neobanks and challenger banks attracting millions of new customers by offering streamlined user experiences and cost advantages. This increased customer mobility means they can easily switch providers if their current bank doesn't meet their expectations for fees, rates, or service quality, thereby increasing their leverage.

- Increased Choice: Customers have a wider array of banking providers to choose from, moving beyond traditional brick-and-mortar institutions.

- Fee Sensitivity: Digital banks often advertise minimal or no monthly maintenance fees, making customers more sensitive to fees charged by traditional banks.

- Rate Competition: The ability to easily compare interest rates on savings accounts and loans online empowers customers to seek out the best yields.

- Switching Ease: Many digital platforms facilitate quick and easy account opening and closing, reducing the friction associated with changing banks.

Empowered Customers: The New Banking Reality

Customers have substantial bargaining power, especially for commoditized banking products where switching is easy. This is evident in 2024, with consumers holding multiple accounts, signaling a willingness to switch for better terms.

Price transparency through online comparison tools further empowers customers to seek the best value, forcing institutions like Tompkins Financial to remain competitive on rates and fees.

The rise of digital-first banks with lower overheads offers customers attractive alternatives, increasing their leverage and encouraging traditional banks to improve their offerings.

| Factor | Impact on Tompkins Financial | Supporting Data (2024 Estimates) |

|---|---|---|

| Ease of Switching | High customer leverage, pressure on pricing and service. | Average consumer holds 4+ bank accounts. |

| Information Availability | Empowers customers to compare rates and fees, impacting pricing strategy. | Increased online financial comparison site usage. |

| Digital Banking Competition | Drives need for competitive digital offerings and lower fees. | Neobanks attracting millions of new customers. |

| Concentrated Commercial Clients | Significant influence from large clients on loan rates and deposit terms. | Potential for large clients to demand rates below market average. |

Preview Before You Purchase

Tompkins Financial Porter's Five Forces Analysis

This preview showcases the complete Tompkins Financial Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape within its industry. The document you see here is precisely what you will receive immediately after purchase, ensuring full transparency and no hidden content. This detailed analysis is professionally formatted and ready for immediate use, providing actionable insights into the strategic positioning of Tompkins Financial.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Tompkins Financial operates in a dynamic banking landscape, facing pressures from established competitors and the ever-present threat of new digital entrants. Understanding the intensity of buyer bargaining power and the availability of substitute financial products is crucial for their strategic positioning.

The complete report reveals the real forces shaping Tompkins Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Core Technology Providers

Tompkins Financial's reliance on specialized financial software, core banking systems, and cybersecurity solutions from a limited number of vendors significantly influences supplier power. For instance, in 2024, the financial services industry continued to see consolidation among key technology providers, meaning fewer options for essential infrastructure. This dependence can grant these technology suppliers considerable leverage, especially if their offerings are critical and difficult to replace.

When a supplier provides unique or indispensable technology, Tompkins Financial's ability to negotiate favorable terms diminishes. High switching costs associated with migrating core banking systems, for example, can lock the company into existing relationships, further strengthening the supplier's bargaining position. This reality means that the cost and complexity of changing providers are major factors in Tompkins Financial's supplier relationships.

Availability of Human Capital

The demand for skilled financial professionals, particularly in compliance, data analytics, and digital banking, is high, giving these employees considerable bargaining power. This means Tompkins Financial, like many in the industry, faces situations where talented individuals can command better compensation and benefits, impacting labor costs.

A shortage of qualified talent within Tompkins Financial's specific operating regions directly translates into increased bargaining power for available human capital. For instance, in 2024, the U.S. financial services sector continued to experience a tight labor market for specialized roles, with reports indicating salary increases of 5-10% for in-demand positions.

This scarcity can lead to higher recruitment expenses and longer hiring timelines for Tompkins Financial, as they compete for a limited pool of experienced professionals. The need to attract and retain top talent in these critical areas directly influences the bank's operational efficiency and cost structure.

Cost of Data and Information Services

Financial institutions like Tompkins Financial rely significantly on data and information service providers for crucial functions such as market analysis, credit scoring, and regulatory compliance. The cost of these essential services directly influences operational expenses. For example, in 2024, the global market for financial data and analytics was valued at over $30 billion, indicating substantial spending by firms in this sector.

When data providers offer highly specialized or unique datasets, or if the market for certain types of financial data is concentrated among a few suppliers, these suppliers gain considerable bargaining power. This allows them to potentially charge premium prices for their services, directly impacting Tompkins Financial's cost structure and profitability.

Regulatory Compliance Service Providers

The bargaining power of regulatory compliance service providers for Tompkins Financial is significant due to the intricate and constantly changing landscape of financial regulations. Adherence to these rules, whether it's for banking operations, investment advisory, or capital markets, often necessitates specialized legal and consulting expertise.

A limited pool of firms possesses the deep, niche knowledge required for specific compliance areas, granting them considerable leverage. For instance, as of early 2024, the cost of specialized financial regulatory consulting can range from several hundred to over a thousand dollars per hour, depending on the firm's reputation and the complexity of the service.

- Specialized Expertise: Firms with proven track records in areas like anti-money laundering (AML) or Know Your Customer (KYC) regulations command higher fees.

- Regulatory Changes: The ongoing updates to regulations, such as those impacting data privacy or capital requirements, create a continuous demand for expert guidance.

- Limited Alternatives: For highly specific or emerging regulatory challenges, the number of qualified service providers can be very small, reducing Tompkins Financial's ability to negotiate favorable terms.

Infrastructure and Utility Providers

While infrastructure and utility providers might seem like basic commodities, their role in ensuring reliable and secure operations for financial institutions like Tompkins Financial is paramount. This includes everything from stable internet connectivity and consistent power supply to the physical security of branches.

In specific geographic regions, the availability of high-quality, redundant services from these providers can be limited. This scarcity can grant these essential utility suppliers a degree of bargaining power, as Tompkins Financial, like other banks, relies heavily on uninterrupted service to maintain customer trust and operational efficiency.

For instance, in 2024, the increasing demand for robust cloud infrastructure and cybersecurity services, coupled with potential localized supply chain disruptions impacting hardware availability, could strengthen the position of key providers. Financial institutions are often locked into contracts with these providers, further limiting their ability to switch easily and thus enhancing supplier leverage.

- Critical Reliance: Financial institutions depend on uninterrupted infrastructure services for daily operations and customer access.

- Limited Alternatives: In certain areas, the choice of high-quality, redundant utility providers is restricted.

- 2024 Market Dynamics: Increased demand for cloud and cybersecurity, alongside potential supply chain issues, can bolster supplier bargaining power.

- Contractual Lock-in: Existing agreements often make switching providers difficult, reinforcing supplier leverage.

Supplier Power Dynamics: Tompkins Financial's 2024 Strategic Challenge

Tompkins Financial's bargaining power with suppliers is influenced by the concentration of providers for critical services like core banking software and cybersecurity. In 2024, industry consolidation meant fewer options for essential technology, giving these suppliers significant leverage, especially when their solutions are difficult to replace.

The cost and complexity of switching providers, particularly for core banking systems, often result in contractual lock-in. This dependence limits Tompkins Financial's ability to negotiate favorable terms, as the switching costs can be substantial, reinforcing the supplier's strong position.

The bargaining power of suppliers for Tompkins Financial is amplified when they offer unique or indispensable technology. High switching costs associated with essential systems like core banking platforms can lock the company into existing relationships, thereby strengthening the supplier's leverage and impacting negotiation outcomes.

| Supplier Type | Key Factors Influencing Bargaining Power | Impact on Tompkins Financial | 2024 Market Trend |

| Technology Providers (Core Banking, Cybersecurity) | Limited number of vendors, high switching costs, specialized offerings | Reduced negotiation leverage, potentially higher costs | Industry consolidation, increased demand for advanced solutions |

| Data & Analytics Providers | Concentrated market for specialized data, unique datasets | Potential for premium pricing, impact on operational costs | Market value exceeding $30 billion globally, focus on AI-driven insights |

| Regulatory Compliance Services | Niche expertise, complex and evolving regulations, limited qualified firms | Higher hourly rates for specialized consulting, continuous demand for guidance | Costs ranging from $300-$1000+ per hour for expert advice |

What is included in the product

This Porter's Five Forces analysis provides a comprehensive examination of the competitive landscape for Tompkins Financial, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly identify and address competitive pressures with a dynamic, visual representation of each force, simplifying complex market dynamics.

Customers Bargaining Power

Low Switching Costs for Standard Products

For standard banking products, the ease with which customers can switch providers significantly amplifies their bargaining power. This is particularly true for basic offerings like checking accounts, savings accounts, and common loan types. For example, in 2024, the average consumer holds over four bank accounts, indicating a willingness to spread their business and switch providers if better terms are available.

This low barrier to entry for customers means Tompkins Financial must actively compete on price and service quality. If a competitor offers a higher interest rate on savings or lower fees on checking, customers can readily move their funds. This dynamic forces Tompkins Financial to maintain competitive pricing and invest in customer service to prevent attrition and retain its customer base.

Access to Information and Price Transparency

Customers today have an unprecedented amount of information at their fingertips. Online resources provide easy access to comparative data on interest rates, fees, and product features offered by various financial institutions, including Tompkins Financial. This readily available price transparency empowers consumers to make informed decisions and seek out the best value, directly impacting the bank's pricing strategies.

Commoditization of Basic Financial Services

Many fundamental banking services are viewed by customers as interchangeable commodities. This perception means decisions often hinge on price or ease of access, directly boosting customer bargaining power. For instance, in 2024, the average interest rate on a savings account across major US banks hovered around 0.40%, highlighting how price competition drives customer choices in basic offerings.

Concentration of Large Commercial Clients

While Tompkins Financial serves a broad base of local communities, the concentration of its commercial loan portfolio or deposit accounts among a few large businesses can grant these clients significant bargaining power. Such large commercial clients, often possessing substantial financial resources, can leverage their importance to Tompkins by negotiating for more favorable loan rates, lower deposit fees, or enhanced service packages. This ability to demand better terms directly impacts the bank's net interest margin and overall profitability, as these key clients can exert considerable pressure on pricing and service levels.

For instance, if a single large corporate client represents over 5% of Tompkins' total commercial loans, their departure or demand for significantly reduced rates could have a noticeable effect. In 2024, the banking sector generally saw continued competition for large commercial deposits, with some institutions offering tiered rates that favored higher balances, a trend that could empower large clients to seek out the most advantageous terms.

- Concentrated Commercial Client Base: A few large businesses holding a significant portion of Tompkins' commercial loans or deposits can wield considerable influence.

- Negotiating Favorable Terms: These clients can negotiate for lower interest rates on loans or better terms on deposits, impacting Tompkins' profitability.

- Impact on Profitability: The ability of large clients to secure preferential treatment can directly affect the bank's net interest margin and fee income.

- Industry Trends: In 2024, competition for large commercial deposits intensified, potentially increasing the bargaining power of these clients.

Rise of Digital-First Banking Options

The proliferation of digital-first banking options significantly amplifies customer bargaining power. Online-only banks and fintech platforms, often operating with lower overheads, can offer more attractive terms, such as reduced fees and higher interest rates on deposits. This readily available alternative compels traditional institutions like Tompkins Financial to be more competitive.

For instance, in 2024, the digital banking sector continued its rapid expansion, with neobanks and challenger banks attracting millions of new customers by offering streamlined user experiences and cost advantages. This increased customer mobility means they can easily switch providers if their current bank doesn't meet their expectations for fees, rates, or service quality, thereby increasing their leverage.

- Increased Choice: Customers have a wider array of banking providers to choose from, moving beyond traditional brick-and-mortar institutions.

- Fee Sensitivity: Digital banks often advertise minimal or no monthly maintenance fees, making customers more sensitive to fees charged by traditional banks.

- Rate Competition: The ability to easily compare interest rates on savings accounts and loans online empowers customers to seek out the best yields.

- Switching Ease: Many digital platforms facilitate quick and easy account opening and closing, reducing the friction associated with changing banks.

Empowered Customers: The New Banking Reality

Customers have substantial bargaining power, especially for commoditized banking products where switching is easy. This is evident in 2024, with consumers holding multiple accounts, signaling a willingness to switch for better terms.

Price transparency through online comparison tools further empowers customers to seek the best value, forcing institutions like Tompkins Financial to remain competitive on rates and fees.

The rise of digital-first banks with lower overheads offers customers attractive alternatives, increasing their leverage and encouraging traditional banks to improve their offerings.

| Factor | Impact on Tompkins Financial | Supporting Data (2024 Estimates) |

|---|---|---|

| Ease of Switching | High customer leverage, pressure on pricing and service. | Average consumer holds 4+ bank accounts. |

| Information Availability | Empowers customers to compare rates and fees, impacting pricing strategy. | Increased online financial comparison site usage. |

| Digital Banking Competition | Drives need for competitive digital offerings and lower fees. | Neobanks attracting millions of new customers. |

| Concentrated Commercial Clients | Significant influence from large clients on loan rates and deposit terms. | Potential for large clients to demand rates below market average. |

Preview Before You Purchase

Tompkins Financial Porter's Five Forces Analysis

This preview showcases the complete Tompkins Financial Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape within its industry. The document you see here is precisely what you will receive immediately after purchase, ensuring full transparency and no hidden content. This detailed analysis is professionally formatted and ready for immediate use, providing actionable insights into the strategic positioning of Tompkins Financial.