TomTom Boston Consulting Group Matrix

See the Bigger Picture

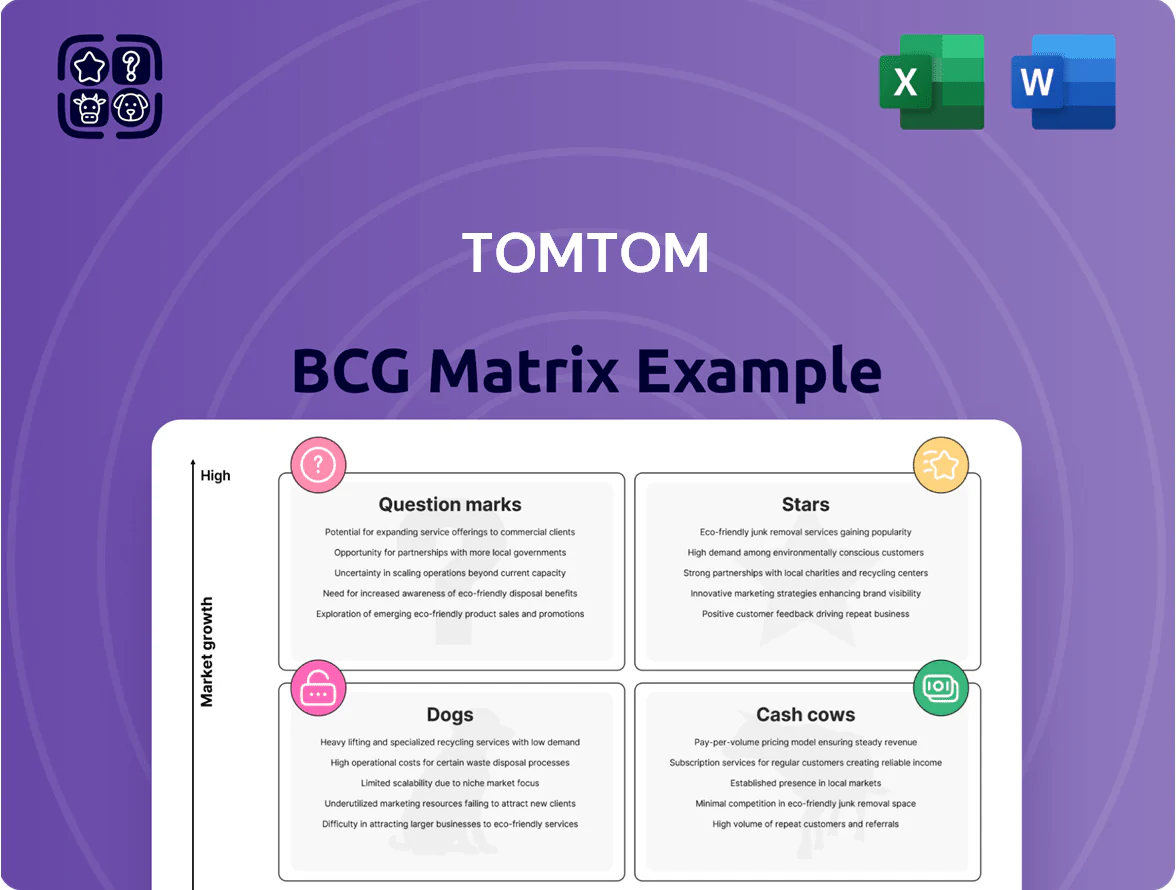

TomTom’s BCG Matrix snapshot highlights where its mapping and navigation lines likely fall among Stars, Cash Cows, Question Marks, or Dogs based on market growth and relative share—revealing which units fuel growth and which tie up capital. This preview teases quadrant placements and high-level strategic implications to help frame your next move. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, actionable recommendations, and editable Word and Excel deliverables that save you research time and guide confident investment or product decisions.

Stars

TomTom Orbis Mapping Platform

Orbis, TomTom’s high-definition collaborative map platform, integrates sensor, fleet, and crowd data and by late 2025 covers >75% of Europe’s highway km for AV-grade lanes, anchoring TomTom’s lead in the high-growth automated-driving/ADAS market (CAGR ~22% to 2030).

TomTom has funneled ~€350m into Orbis since 2021 and continues heavy R&D and cloud ops spend to make Orbis the location-data industry standard; unit revenue grew ~40% YoY in 2024–25.

As automated-vehicle deployments scale through the 2030s, Orbis is positioned to shift from star to cash cow, with implied margin expansion of 10–15 percentage points as capex intensity falls and recurring licensing rises.

HD Maps for Autonomous Driving

TomTom’s HD Maps power Level 2+ and Level 3 autonomy, supplying lane-level detail used by OEMs; as of 2025 TomTom claims ~40% share among premium European and North American OEMs and maps 25+ million km of high-definition road network.

Demand is growing: ADAS and autonomous features market expected CAGR ~15% to 2030, pushing automakers to increase sensor fusion and map reliance, so HD mapping stays strategic.

R&D is costly—TomTom spent €120m on mapping and ADAS tech in FY2024—but high switching costs and data quality give pricing power and justify prioritizing capital allocation to HD Maps.

Electric Vehicle EV Services

Electric Vehicle EV Services sits in TomTom’s BCG Matrix as a star: EV global stock topped 16.5 million in 2023 and is forecast +25% CAGR to 2030, driving high growth for navigation and range tools.

TomTom leads the niche with real-time charging availability, battery-optimized routing and topo impact analysis, supporting ~200M live users and licensing to 100+ automakers as of 2025.

With EU and UK ICE phase-outs set for 2035 and many countries following, this unit captures rising market share and strong revenue upside—EV services grew ~40% YoY in 2024.

Continued marketing and product investment are required to fend off competitors like HERE, Google and OEM in-house systems and to keep tech leadership.

Automotive Navigation Software

Automotive Navigation Software: TomTom’s embedded navigation is a core growth driver as connected, software-defined vehicles rise; the unit is in millions of new cars—TomTom reported ~5.1 million MAPS & NAV licenses in 2024—yielding high market share but needing heavy R&D and marketing to keep up with OTA and ADAS integration.

Revenue vs cash: this BU generated roughly €400–€450m revenue in 2024 but consumed capital for integrations with new vehicle architectures and SDKs, keeping free cash lower and requiring continued investment to retain OEM contracts.

- Embedded in millions of new vehicles (~5.1M licenses in 2024)

- 2024 revenue ~€400–€450m

- High market share; high R&D & marketing spend

- Drains cash for OEM integration and software-defined vehicle work

Real-time Traffic Information

TomTom's real-time traffic information leads the market, supplying automotive OEMs and 400+ government agencies for smart-city planning; TomTom reported 11 billion probe observations per day in 2024, strengthening its data quality and moat.

Demand for accurate, real-time congestion data is rising as cities target emission cuts and efficiency—global smart traffic management spending is forecast at $28.6B by 2027, keeping this segment high-growth.

TomTom's massive installed base of probes and 95% uptime for live feeds underpin competitive advantage, and continued reliance on live data for logistics and fleet optimization keeps traffic data a Star in the BCG matrix.

- Market leader: auto OEMs + 400+ agencies

- Scale: 11B probe observations/day (2024)

- Finance: smart traffic spend $28.6B by 2027

- Operations: 95% live-feed uptime

TomTom’s growth engines: Orbis HD Maps, EV services, embedded nav & 11B/day traffic

TomTom’s Stars: Orbis HD maps, EV services, embedded navigation and real-time traffic are high-growth, market-leading units—Orbis covers >75% EU highways for AV lanes by late-2025, EV services served ~200M users and grew ~40% YoY in 2024, embedded navigation sold ~5.1M licenses in 2024 (~€400–450m revenue), traffic: 11B probes/day (2024) and 95% uptime.

| Unit | 2024–25 facts | Growth/Share |

|---|---|---|

| Orbis HD Maps | >75% EU highways (late‑2025); €350m invested since 2021 | ~40% OEM share (premium) |

| EV Services | ~200M users; grew ~40% YoY (2024) | EV stock 16.5M (2023), +25% CAGR to 2030 |

| Embedded Nav | 5.1M licenses (2024); €400–450m revenue (2024) | High share; heavy R&D spend |

| Real‑time Traffic | 11B probes/day (2024); 95% uptime | 400+ agencies; smart traffic spend $28.6B by 2027 |

What is included in the product

Comprehensive BCG Matrix for TomTom: evaluates Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest recommendations.

One-page TomTom BCG Matrix placing each product line in a quadrant for quick strategic clarity and decision-making.

Cash Cows

Enterprise Map Data Licensing

Licensing core map data to tech giants and enterprise clients delivers steady, high-margin revenue—TomTom reported recurring licensing revenue of €430m in FY 2024, around 45% of total sales, underscoring stability.

The market is mature; TomTom is one of few independent global providers, holding ~10% share of the global digital mapping enterprise segment in 2024, needing minimal marketing to retain multi-year contracts with firms like Apple and Amazon.

Cash from licensing funds R&D: TomTom invested €115m in development in 2024, financing projects such as the Orbis platform and HD mapping without diluting core operations.

Legacy Automotive Service Contracts

TomTom’s legacy automotive service contracts cover millions of older vehicles needing map updates and basic telematics; they hold a high share in a mature market with estimated annual revenue ~€120m in 2024 and single-digit growth under 2% CAGR.

With infrastructure largely fully depreciated, gross margins exceed 60% and operating cash flow from this unit funded ~30% of net interest and R&D spend in 2024, providing steady liquidity for debt service and new product investment.

Static Map Content

Static Map Content remains a cash cow for TomTom, serving GIS and professional markets with non-real-time maps; global GIS spending held steady at about $6.1B in 2024, and TomTom’s map database covers 100+ countries, keeping it a leading choice.

Maintenance capex is low—TomTom reported map-related operating costs under €120M in 2024—so margins on legacy map sales stay high and free cash flow benefits the firm.

The product leverages decades of prior investment: historical mapping R&D and telemetry yield continuing licensing revenue with minimal incremental investment and limited growth but reliable profitability.

Intellectual Property and Patents

TomTom holds ~2,000 patents in navigation, routing, and location tech, and licensing generated €72m in revenue in FY2024, supplying high-margin, low-cost cash flows.

The market for these base technologies is mature; strong IP enforcement and long patent lifecycles keep TomTom's position defensible and revenues steady.

Licensing income is passive, contributes to margins and free cash flow, and helps stabilize financials during cyclical mapping and device sales swings.

- ~2,000 patents

- €72m licensing revenue FY2024

- High margin, low operational cost

- Mature, legally protected market

Location Based APIs for Developers

TomTom’s Location Based APIs for web and mobile have settled into a cash cow: steady margins near 30% and annual revenue around €120–160m in 2024, driven by devs who value privacy and non-big-tech independence.

Market growth has flattened as the app economy matured, so volume rises ~2% yearly; maintenance costs are low, freeing cash to fund speculative R&D and partnerships.

- 2024 revenue ≈ €120–160m

- gross margin ~30%

- annual growth ≈ 2%

- low maintenance, high cash generation

- strong share among privacy-focused developers

TomTom’s maps & APIs: €430m licensing cash cow, high margins, steady cash flow

TomTom’s map licensing and Location APIs are cash cows: €430m recurring licensing (45% of sales) and €120–160m API revenue in 2024, high gross margins (maps >60%, APIs ~30%), low maintenance capex (~€120m map OPEX) and €72m patent licensing—steady cash, ~2% CAGR, funds R&D and debt service.

| Metric | 2024 |

|---|---|

| Licensing revenue | €430m |

| API revenue | €120–160m |

| Patent licensing | €72m |

| Map gross margin | >60% |

| API gross margin | ~30% |

What You’re Viewing Is Included

TomTom BCG Matrix

The file you're previewing on this page is the final TomTom BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clarity and decision-making. This preview is identical to the downloadable file and reflects market-backed analysis, so the full document will arrive in your inbox with no surprises or extra revisions needed. Once purchased, you can edit, print, or present the matrix immediately to stakeholders.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

TomTom’s BCG Matrix snapshot highlights where its mapping and navigation lines likely fall among Stars, Cash Cows, Question Marks, or Dogs based on market growth and relative share—revealing which units fuel growth and which tie up capital. This preview teases quadrant placements and high-level strategic implications to help frame your next move. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, actionable recommendations, and editable Word and Excel deliverables that save you research time and guide confident investment or product decisions.

Stars

TomTom Orbis Mapping Platform

Orbis, TomTom’s high-definition collaborative map platform, integrates sensor, fleet, and crowd data and by late 2025 covers >75% of Europe’s highway km for AV-grade lanes, anchoring TomTom’s lead in the high-growth automated-driving/ADAS market (CAGR ~22% to 2030).

TomTom has funneled ~€350m into Orbis since 2021 and continues heavy R&D and cloud ops spend to make Orbis the location-data industry standard; unit revenue grew ~40% YoY in 2024–25.

As automated-vehicle deployments scale through the 2030s, Orbis is positioned to shift from star to cash cow, with implied margin expansion of 10–15 percentage points as capex intensity falls and recurring licensing rises.

HD Maps for Autonomous Driving

TomTom’s HD Maps power Level 2+ and Level 3 autonomy, supplying lane-level detail used by OEMs; as of 2025 TomTom claims ~40% share among premium European and North American OEMs and maps 25+ million km of high-definition road network.

Demand is growing: ADAS and autonomous features market expected CAGR ~15% to 2030, pushing automakers to increase sensor fusion and map reliance, so HD mapping stays strategic.

R&D is costly—TomTom spent €120m on mapping and ADAS tech in FY2024—but high switching costs and data quality give pricing power and justify prioritizing capital allocation to HD Maps.

Electric Vehicle EV Services

Electric Vehicle EV Services sits in TomTom’s BCG Matrix as a star: EV global stock topped 16.5 million in 2023 and is forecast +25% CAGR to 2030, driving high growth for navigation and range tools.

TomTom leads the niche with real-time charging availability, battery-optimized routing and topo impact analysis, supporting ~200M live users and licensing to 100+ automakers as of 2025.

With EU and UK ICE phase-outs set for 2035 and many countries following, this unit captures rising market share and strong revenue upside—EV services grew ~40% YoY in 2024.

Continued marketing and product investment are required to fend off competitors like HERE, Google and OEM in-house systems and to keep tech leadership.

Automotive Navigation Software

Automotive Navigation Software: TomTom’s embedded navigation is a core growth driver as connected, software-defined vehicles rise; the unit is in millions of new cars—TomTom reported ~5.1 million MAPS & NAV licenses in 2024—yielding high market share but needing heavy R&D and marketing to keep up with OTA and ADAS integration.

Revenue vs cash: this BU generated roughly €400–€450m revenue in 2024 but consumed capital for integrations with new vehicle architectures and SDKs, keeping free cash lower and requiring continued investment to retain OEM contracts.

- Embedded in millions of new vehicles (~5.1M licenses in 2024)

- 2024 revenue ~€400–€450m

- High market share; high R&D & marketing spend

- Drains cash for OEM integration and software-defined vehicle work

Real-time Traffic Information

TomTom's real-time traffic information leads the market, supplying automotive OEMs and 400+ government agencies for smart-city planning; TomTom reported 11 billion probe observations per day in 2024, strengthening its data quality and moat.

Demand for accurate, real-time congestion data is rising as cities target emission cuts and efficiency—global smart traffic management spending is forecast at $28.6B by 2027, keeping this segment high-growth.

TomTom's massive installed base of probes and 95% uptime for live feeds underpin competitive advantage, and continued reliance on live data for logistics and fleet optimization keeps traffic data a Star in the BCG matrix.

- Market leader: auto OEMs + 400+ agencies

- Scale: 11B probe observations/day (2024)

- Finance: smart traffic spend $28.6B by 2027

- Operations: 95% live-feed uptime

TomTom’s growth engines: Orbis HD Maps, EV services, embedded nav & 11B/day traffic

TomTom’s Stars: Orbis HD maps, EV services, embedded navigation and real-time traffic are high-growth, market-leading units—Orbis covers >75% EU highways for AV lanes by late-2025, EV services served ~200M users and grew ~40% YoY in 2024, embedded navigation sold ~5.1M licenses in 2024 (~€400–450m revenue), traffic: 11B probes/day (2024) and 95% uptime.

| Unit | 2024–25 facts | Growth/Share |

|---|---|---|

| Orbis HD Maps | >75% EU highways (late‑2025); €350m invested since 2021 | ~40% OEM share (premium) |

| EV Services | ~200M users; grew ~40% YoY (2024) | EV stock 16.5M (2023), +25% CAGR to 2030 |

| Embedded Nav | 5.1M licenses (2024); €400–450m revenue (2024) | High share; heavy R&D spend |

| Real‑time Traffic | 11B probes/day (2024); 95% uptime | 400+ agencies; smart traffic spend $28.6B by 2027 |

What is included in the product

Comprehensive BCG Matrix for TomTom: evaluates Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest recommendations.

One-page TomTom BCG Matrix placing each product line in a quadrant for quick strategic clarity and decision-making.

Cash Cows

Enterprise Map Data Licensing

Licensing core map data to tech giants and enterprise clients delivers steady, high-margin revenue—TomTom reported recurring licensing revenue of €430m in FY 2024, around 45% of total sales, underscoring stability.

The market is mature; TomTom is one of few independent global providers, holding ~10% share of the global digital mapping enterprise segment in 2024, needing minimal marketing to retain multi-year contracts with firms like Apple and Amazon.

Cash from licensing funds R&D: TomTom invested €115m in development in 2024, financing projects such as the Orbis platform and HD mapping without diluting core operations.

Legacy Automotive Service Contracts

TomTom’s legacy automotive service contracts cover millions of older vehicles needing map updates and basic telematics; they hold a high share in a mature market with estimated annual revenue ~€120m in 2024 and single-digit growth under 2% CAGR.

With infrastructure largely fully depreciated, gross margins exceed 60% and operating cash flow from this unit funded ~30% of net interest and R&D spend in 2024, providing steady liquidity for debt service and new product investment.

Static Map Content

Static Map Content remains a cash cow for TomTom, serving GIS and professional markets with non-real-time maps; global GIS spending held steady at about $6.1B in 2024, and TomTom’s map database covers 100+ countries, keeping it a leading choice.

Maintenance capex is low—TomTom reported map-related operating costs under €120M in 2024—so margins on legacy map sales stay high and free cash flow benefits the firm.

The product leverages decades of prior investment: historical mapping R&D and telemetry yield continuing licensing revenue with minimal incremental investment and limited growth but reliable profitability.

Intellectual Property and Patents

TomTom holds ~2,000 patents in navigation, routing, and location tech, and licensing generated €72m in revenue in FY2024, supplying high-margin, low-cost cash flows.

The market for these base technologies is mature; strong IP enforcement and long patent lifecycles keep TomTom's position defensible and revenues steady.

Licensing income is passive, contributes to margins and free cash flow, and helps stabilize financials during cyclical mapping and device sales swings.

- ~2,000 patents

- €72m licensing revenue FY2024

- High margin, low operational cost

- Mature, legally protected market

Location Based APIs for Developers

TomTom’s Location Based APIs for web and mobile have settled into a cash cow: steady margins near 30% and annual revenue around €120–160m in 2024, driven by devs who value privacy and non-big-tech independence.

Market growth has flattened as the app economy matured, so volume rises ~2% yearly; maintenance costs are low, freeing cash to fund speculative R&D and partnerships.

- 2024 revenue ≈ €120–160m

- gross margin ~30%

- annual growth ≈ 2%

- low maintenance, high cash generation

- strong share among privacy-focused developers

TomTom’s maps & APIs: €430m licensing cash cow, high margins, steady cash flow

TomTom’s map licensing and Location APIs are cash cows: €430m recurring licensing (45% of sales) and €120–160m API revenue in 2024, high gross margins (maps >60%, APIs ~30%), low maintenance capex (~€120m map OPEX) and €72m patent licensing—steady cash, ~2% CAGR, funds R&D and debt service.

| Metric | 2024 |

|---|---|

| Licensing revenue | €430m |

| API revenue | €120–160m |

| Patent licensing | €72m |

| Map gross margin | >60% |

| API gross margin | ~30% |

What You’re Viewing Is Included

TomTom BCG Matrix

The file you're previewing on this page is the final TomTom BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clarity and decision-making. This preview is identical to the downloadable file and reflects market-backed analysis, so the full document will arrive in your inbox with no surprises or extra revisions needed. Once purchased, you can edit, print, or present the matrix immediately to stakeholders.