Toray Industries Boston Consulting Group Matrix

Download Your Competitive Advantage

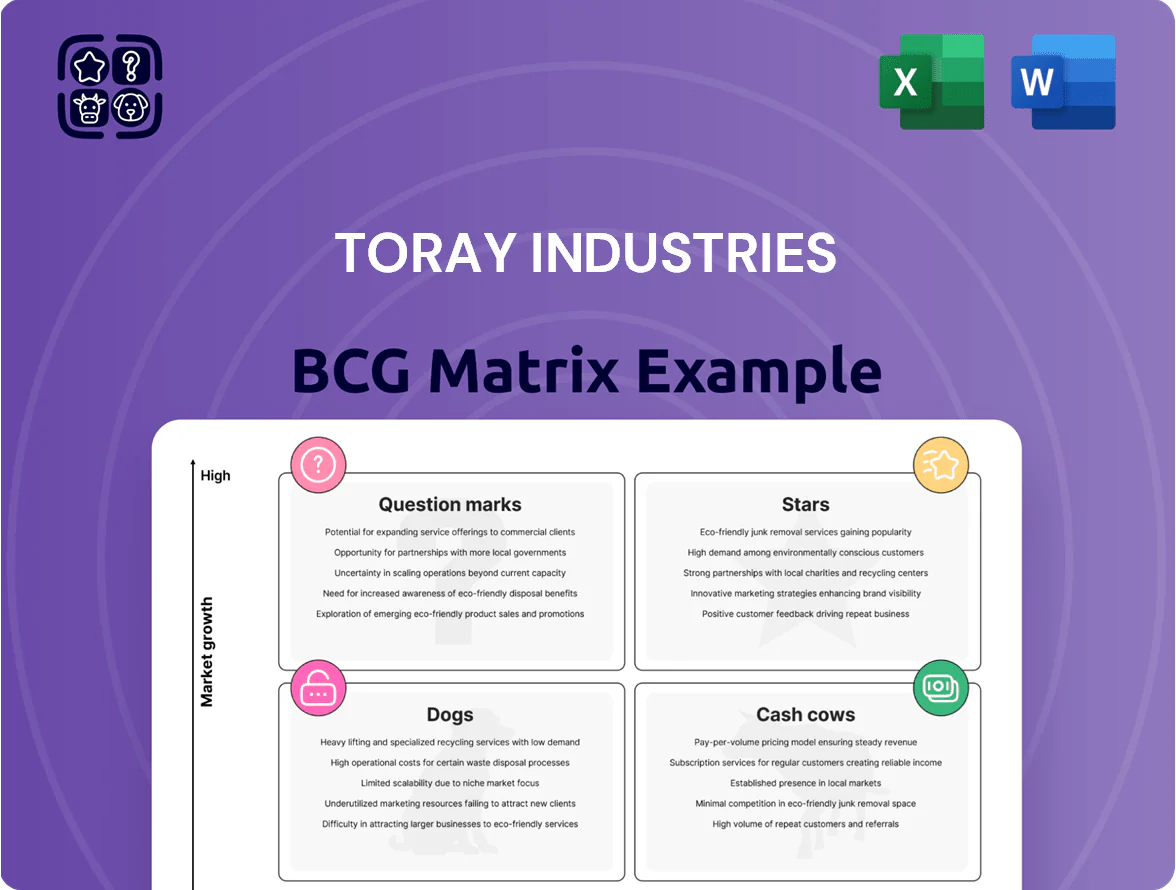

Toray Industries sits at a complex crossroads of advanced materials, fibers, and composite technologies—our BCG Matrix preview highlights likely Stars in carbon fiber composites, Cash Cows in established textile segments, and Question Marks across emerging biotech and electronic materials. This snapshot teases data-driven quadrant placements and high-level implications for R&D and capital allocation. Purchase the full BCG Matrix for a complete quadrant breakdown, actionable strategies, and ready-to-use Word and Excel deliverables to guide investment and portfolio decisions.

Stars

Aerospace Carbon Fiber Composites

Toray holds roughly 70% of the global high-performance carbon fiber market and is the primary supplier for Boeing 777X and 787 airframes, underpinning its Star position in aerospace composites.

With commercial aviation RPKs up ~45% from 2022 to 2024 and airlines prioritizing fuel-efficient, lightweight frames, demand growth for Toray’s carbon fibers is accelerating at an estimated CAGR of 8–10% through 2028.

Scaling capacity needs heavy capex—Toray committed ¥120 billion in 2023–2025 expansions—but as aircraft production rates normalize, these units are set to convert into high-margin cash cows.

Battery Separator Films

The EV shift drives ~12–15% CAGR demand for lithium-ion separator films; Toray reported separator sales of ¥120.4bn in FY2024 (ended Mar 2024), holding top-3 global share due to proprietary coating tech and >30% EBITDA margin on product lines.

High R&D and capex: Toray invested ¥45bn in battery-related capex in FY2023–24 and runs multi-year expansion to meet projected 2030 demand of ~1.2TWh equivalent, pressuring free cash flow but securing strategic positioning.

Semiconductor Coating Materials

Toray’s Semiconductor Coating Materials—notably photosensitive polyimides for advanced packaging—are in strong demand from AI and HPC makers; Toray’s electronic materials division posted JPY 128.4 billion revenue in FY2024, up 14% year-on-year, driven by packaging demand.

The segment holds leading market share in specialized formulations for next-gen chip fab processes, supplying key players in substrate and fan-out packaging where precision chemistries command 20–30% premiums.

Rapid tech change forces continuous R&D and capex; Toray spent JPY 42.7 billion on R&D in FY2024, and sustaining leadership will require similar or higher reinvestment cadence.

Green Hydrogen Components

Toray, using its polymer chemistry, leads in hydrocarbon electrolyte membranes for electrolysis and fuel cells, serving a market projected to reach $2.5B by 2030 (2025 base growth >20% CAGR).

The global decarbonization push and hydrogen infrastructure buildout—~$200B announced public/private projects by 2025—give these materials high-growth potential.

As a first-to-market innovator, Toray is ramping capex (¥30–40B 2024–25 guidance) to capture market share in the clean hydrogen economy.

- Leading tech: hydrocarbon membranes, lower cost vs PFSA

- Market: ~$2.5B by 2030, >20% CAGR from 2025

- Demand driver: ~$200B H2 projects announced by 2025

- Investment: Toray capex ¥30–40B (2024–25)

High-Performance PPS Resins

Polyphenylene sulfide (PPS) resins deliver high heat resistance and chemical durability critical for EV connectors, battery housings, and motor components; demand rose ~9% CAGR 2019–2024, driven by electrification. Toray Industries (Tokyo: 3402) is the global leader with ~22% market share in PPS as of 2024 and revenue exposure of roughly ¥60–80 billion annually in high-performance polymers.

This BCG Stars segment needs heavy support—priority capital for global supply-chain placement, capacity expansions, and qualifying lines for auto OEMs—but offers long-term dominance as ICE-to-EV share shifts: EV penetration hit 14% global new-car sales in 2024 and forecasts show 30%+ by 2030.

- High demand: ~9% CAGR 2019–2024

- Toray share: ~22% global (2024)

- Revenue: ¥60–80B p.a. in polymers

- EVs: 14% new-car sales (2024), 30%+ by 2030

- Action: invest in global capacity & supply security

Toray: Carbon‑fiber leader (≈70%) fueling high‑margin growth amid heavy capex risk

Toray’s Stars: dominant carbon-fiber (≈70% global share) and high-margin battery/separator and semiconductor materials driving 8–15% CAGR growth; FY2024 separator sales ¥120.4bn, electronic materials ¥128.4bn, R&D ¥42.7bn; heavy capex (¥120bn 2023–25) to scale capacity. Key risks: capex strain on FCF and rapid tech change requiring sustained reinvestment.

| Metric | Value |

|---|---|

| Carbon fiber share | ≈70% |

| Separator sales FY2024 | ¥120.4bn |

| Electronic materials FY2024 | ¥128.4bn |

| R&D FY2024 | ¥42.7bn |

| Capex 2023–25 | ¥120bn |

What is included in the product

Comprehensive BCG Matrix of Toray: identifies Stars, Cash Cows, Question Marks, Dogs with strategic moves, investment priorities, risks, and trend impacts.

One-page Toray Industries BCG Matrix placing each business unit in a quadrant for executive clarity

Cash Cows

Polyester Fibers and Textiles

Polyester fibers and textiles are Toray Industries’ foundational cash cow, holding high global market share in a mature, low-growth market where industry CAGR is ~1–2% (2024–25); sales were about ¥440 billion in FY2024 for Fibers & Textiles, providing steady margin and scale.

These operations deliver consistent, large cash flow with limited need for heavy marketing or capex—Toray’s segment operating income was ¥52.3 billion in FY2024—so management harvests excess cash.

That harvested cash funds R&D and capex in high-growth areas: Toray spent ¥103.6 billion on R&D in FY2024, supporting expansion into carbon fiber composites and biotechnology where revenue growth prospects exceed 10% annually.

RO Membranes for Water Treatment

Toray Industries leads global reverse osmosis (RO) membranes for desalination and wastewater reuse, holding roughly 30%–35% market share as of 2024 and shipping membranes to 60+ countries.

The RO market is mature; replacement demand drives ~8% annual volume growth for Toray’s membrane sales and long-term contracts provide predictable revenue through 2028.

High manufacturing efficiency yields stable gross margins near 28% in FY2024, funding dividends and covering interest on ¥500–¥600 billion net debt.

Industrial Plastic Films

Standard polyester films for packaging and industrial use sit as a high-market-share cash cow for Toray, with global PET film demand growth ~2% CAGR 2020–2025 and Toray capturing an estimated ~18% share in key markets as of 2024.

Toray’s optimized lines deliver strong margins — reported film segment operating margin ~14% in FY2024 — driven by scale, energy-efficient processes, and vertical feedstock integration.

Technology plateaued: little capex needed beyond maintenance (capital expenditure ~1–2% of segment sales in 2024), so films generate steady free cash flow and fund higher-growth R&D and investments elsewhere.

Apparel-use Nylon Fibers

Toray’s apparel-use nylon fibers lead Japan and rank among top global suppliers, generating steady revenue—about ¥120–140 billion annual sales in textile fibers for FY2024—driven by loyal brands and integrated upstream polymer to downstream yarn operations.

Market growth for traditional apparel nylon is low (mid-single-digit % CAGR), so Toray treats it as a cash cow, prioritizing process gains, yield improvements and cost cuts to protect ~20–25% operating margin in the segment.

- Market leader, integrated supply chain

- FY2024 sales ~¥120–140B

- Low growth, mid-single-digit CAGR

- Segment margin ~20–25%

- Focus on incremental process improvement

Cigarette Filter Tow

Toray’s cigarette filter tow (cellulose acetate) remains a cash cow: despite a 4.0% annual decline in global smoking prevalence since 2010, Toray holds a high market share—estimated ~30% of global acetate tow capacity in 2024—yielding steady EBITDA margins above 18% and strong free cash flow.

The segment is mature with low CAGR (≈‑1% to 0% through 2028) but limited competition and high switching costs keep pricing stable, so minimal promo spend is needed and operating cash funds other growth units.

- High share: ~30% global capacity (2024)

- Margins: EBITDA ~18%+

- Growth: market CAGR ~‑1%–0% to 2028

- Promo spend: negligible; cash redeployed

Toray’s high‑margin industrial staples fund ¥103.6B R&D and growth capex

Toray’s cash cows—polyester fibers/textiles (FY2024 sales ~¥440B, seg. op. income ¥52.3B), RO membranes (~30–35% share, ~8% volume growth), PET films (share ~18%, film margin ~14%), nylon fibers (sales ~¥130B, margin ~20–25%), acetate tow (~30% capacity, EBITDA >18%)—generate steady free cash flow supporting ¥103.6B R&D and new-growth capex.

| Product | FY2024 | Share/Growth | Margin |

|---|---|---|---|

| Fibers/Textiles | ¥440B/¥52.3B | 1–2% CAGR | — |

| RO membranes | — | 30–35%/8% vol | 28% gross |

| PET films | — | ~18% share/2% CAGR | 14% |

| Nylon fibers | ¥130B | mid‑single % | 20–25% |

| Acetate tow | — | ~30% cap./‑1–0% CAGR | EBITDA >18% |

Preview = Final Product

Toray Industries BCG Matrix

The file you're previewing is the final Toray Industries BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report tailored for clarity and professional presentation.

This preview reflects the exact same analysis-backed BCG Matrix report delivered post-purchase, crafted with precision to support strategic decision-making on Toray’s business units and market positions.

What you see is the actual downloadable document available immediately after buying, editable and print-ready for inclusion in presentations, board meetings, or client deliverables.

The report is designed by strategy experts and formatted for immediate use—no surprises, no revisions needed—so you can plug it directly into your planning and competitive analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Toray Industries sits at a complex crossroads of advanced materials, fibers, and composite technologies—our BCG Matrix preview highlights likely Stars in carbon fiber composites, Cash Cows in established textile segments, and Question Marks across emerging biotech and electronic materials. This snapshot teases data-driven quadrant placements and high-level implications for R&D and capital allocation. Purchase the full BCG Matrix for a complete quadrant breakdown, actionable strategies, and ready-to-use Word and Excel deliverables to guide investment and portfolio decisions.

Stars

Aerospace Carbon Fiber Composites

Toray holds roughly 70% of the global high-performance carbon fiber market and is the primary supplier for Boeing 777X and 787 airframes, underpinning its Star position in aerospace composites.

With commercial aviation RPKs up ~45% from 2022 to 2024 and airlines prioritizing fuel-efficient, lightweight frames, demand growth for Toray’s carbon fibers is accelerating at an estimated CAGR of 8–10% through 2028.

Scaling capacity needs heavy capex—Toray committed ¥120 billion in 2023–2025 expansions—but as aircraft production rates normalize, these units are set to convert into high-margin cash cows.

Battery Separator Films

The EV shift drives ~12–15% CAGR demand for lithium-ion separator films; Toray reported separator sales of ¥120.4bn in FY2024 (ended Mar 2024), holding top-3 global share due to proprietary coating tech and >30% EBITDA margin on product lines.

High R&D and capex: Toray invested ¥45bn in battery-related capex in FY2023–24 and runs multi-year expansion to meet projected 2030 demand of ~1.2TWh equivalent, pressuring free cash flow but securing strategic positioning.

Semiconductor Coating Materials

Toray’s Semiconductor Coating Materials—notably photosensitive polyimides for advanced packaging—are in strong demand from AI and HPC makers; Toray’s electronic materials division posted JPY 128.4 billion revenue in FY2024, up 14% year-on-year, driven by packaging demand.

The segment holds leading market share in specialized formulations for next-gen chip fab processes, supplying key players in substrate and fan-out packaging where precision chemistries command 20–30% premiums.

Rapid tech change forces continuous R&D and capex; Toray spent JPY 42.7 billion on R&D in FY2024, and sustaining leadership will require similar or higher reinvestment cadence.

Green Hydrogen Components

Toray, using its polymer chemistry, leads in hydrocarbon electrolyte membranes for electrolysis and fuel cells, serving a market projected to reach $2.5B by 2030 (2025 base growth >20% CAGR).

The global decarbonization push and hydrogen infrastructure buildout—~$200B announced public/private projects by 2025—give these materials high-growth potential.

As a first-to-market innovator, Toray is ramping capex (¥30–40B 2024–25 guidance) to capture market share in the clean hydrogen economy.

- Leading tech: hydrocarbon membranes, lower cost vs PFSA

- Market: ~$2.5B by 2030, >20% CAGR from 2025

- Demand driver: ~$200B H2 projects announced by 2025

- Investment: Toray capex ¥30–40B (2024–25)

High-Performance PPS Resins

Polyphenylene sulfide (PPS) resins deliver high heat resistance and chemical durability critical for EV connectors, battery housings, and motor components; demand rose ~9% CAGR 2019–2024, driven by electrification. Toray Industries (Tokyo: 3402) is the global leader with ~22% market share in PPS as of 2024 and revenue exposure of roughly ¥60–80 billion annually in high-performance polymers.

This BCG Stars segment needs heavy support—priority capital for global supply-chain placement, capacity expansions, and qualifying lines for auto OEMs—but offers long-term dominance as ICE-to-EV share shifts: EV penetration hit 14% global new-car sales in 2024 and forecasts show 30%+ by 2030.

- High demand: ~9% CAGR 2019–2024

- Toray share: ~22% global (2024)

- Revenue: ¥60–80B p.a. in polymers

- EVs: 14% new-car sales (2024), 30%+ by 2030

- Action: invest in global capacity & supply security

Toray: Carbon‑fiber leader (≈70%) fueling high‑margin growth amid heavy capex risk

Toray’s Stars: dominant carbon-fiber (≈70% global share) and high-margin battery/separator and semiconductor materials driving 8–15% CAGR growth; FY2024 separator sales ¥120.4bn, electronic materials ¥128.4bn, R&D ¥42.7bn; heavy capex (¥120bn 2023–25) to scale capacity. Key risks: capex strain on FCF and rapid tech change requiring sustained reinvestment.

| Metric | Value |

|---|---|

| Carbon fiber share | ≈70% |

| Separator sales FY2024 | ¥120.4bn |

| Electronic materials FY2024 | ¥128.4bn |

| R&D FY2024 | ¥42.7bn |

| Capex 2023–25 | ¥120bn |

What is included in the product

Comprehensive BCG Matrix of Toray: identifies Stars, Cash Cows, Question Marks, Dogs with strategic moves, investment priorities, risks, and trend impacts.

One-page Toray Industries BCG Matrix placing each business unit in a quadrant for executive clarity

Cash Cows

Polyester Fibers and Textiles

Polyester fibers and textiles are Toray Industries’ foundational cash cow, holding high global market share in a mature, low-growth market where industry CAGR is ~1–2% (2024–25); sales were about ¥440 billion in FY2024 for Fibers & Textiles, providing steady margin and scale.

These operations deliver consistent, large cash flow with limited need for heavy marketing or capex—Toray’s segment operating income was ¥52.3 billion in FY2024—so management harvests excess cash.

That harvested cash funds R&D and capex in high-growth areas: Toray spent ¥103.6 billion on R&D in FY2024, supporting expansion into carbon fiber composites and biotechnology where revenue growth prospects exceed 10% annually.

RO Membranes for Water Treatment

Toray Industries leads global reverse osmosis (RO) membranes for desalination and wastewater reuse, holding roughly 30%–35% market share as of 2024 and shipping membranes to 60+ countries.

The RO market is mature; replacement demand drives ~8% annual volume growth for Toray’s membrane sales and long-term contracts provide predictable revenue through 2028.

High manufacturing efficiency yields stable gross margins near 28% in FY2024, funding dividends and covering interest on ¥500–¥600 billion net debt.

Industrial Plastic Films

Standard polyester films for packaging and industrial use sit as a high-market-share cash cow for Toray, with global PET film demand growth ~2% CAGR 2020–2025 and Toray capturing an estimated ~18% share in key markets as of 2024.

Toray’s optimized lines deliver strong margins — reported film segment operating margin ~14% in FY2024 — driven by scale, energy-efficient processes, and vertical feedstock integration.

Technology plateaued: little capex needed beyond maintenance (capital expenditure ~1–2% of segment sales in 2024), so films generate steady free cash flow and fund higher-growth R&D and investments elsewhere.

Apparel-use Nylon Fibers

Toray’s apparel-use nylon fibers lead Japan and rank among top global suppliers, generating steady revenue—about ¥120–140 billion annual sales in textile fibers for FY2024—driven by loyal brands and integrated upstream polymer to downstream yarn operations.

Market growth for traditional apparel nylon is low (mid-single-digit % CAGR), so Toray treats it as a cash cow, prioritizing process gains, yield improvements and cost cuts to protect ~20–25% operating margin in the segment.

- Market leader, integrated supply chain

- FY2024 sales ~¥120–140B

- Low growth, mid-single-digit CAGR

- Segment margin ~20–25%

- Focus on incremental process improvement

Cigarette Filter Tow

Toray’s cigarette filter tow (cellulose acetate) remains a cash cow: despite a 4.0% annual decline in global smoking prevalence since 2010, Toray holds a high market share—estimated ~30% of global acetate tow capacity in 2024—yielding steady EBITDA margins above 18% and strong free cash flow.

The segment is mature with low CAGR (≈‑1% to 0% through 2028) but limited competition and high switching costs keep pricing stable, so minimal promo spend is needed and operating cash funds other growth units.

- High share: ~30% global capacity (2024)

- Margins: EBITDA ~18%+

- Growth: market CAGR ~‑1%–0% to 2028

- Promo spend: negligible; cash redeployed

Toray’s high‑margin industrial staples fund ¥103.6B R&D and growth capex

Toray’s cash cows—polyester fibers/textiles (FY2024 sales ~¥440B, seg. op. income ¥52.3B), RO membranes (~30–35% share, ~8% volume growth), PET films (share ~18%, film margin ~14%), nylon fibers (sales ~¥130B, margin ~20–25%), acetate tow (~30% capacity, EBITDA >18%)—generate steady free cash flow supporting ¥103.6B R&D and new-growth capex.

| Product | FY2024 | Share/Growth | Margin |

|---|---|---|---|

| Fibers/Textiles | ¥440B/¥52.3B | 1–2% CAGR | — |

| RO membranes | — | 30–35%/8% vol | 28% gross |

| PET films | — | ~18% share/2% CAGR | 14% |

| Nylon fibers | ¥130B | mid‑single % | 20–25% |

| Acetate tow | — | ~30% cap./‑1–0% CAGR | EBITDA >18% |

Preview = Final Product

Toray Industries BCG Matrix

The file you're previewing is the final Toray Industries BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report tailored for clarity and professional presentation.

This preview reflects the exact same analysis-backed BCG Matrix report delivered post-purchase, crafted with precision to support strategic decision-making on Toray’s business units and market positions.

What you see is the actual downloadable document available immediately after buying, editable and print-ready for inclusion in presentations, board meetings, or client deliverables.

The report is designed by strategy experts and formatted for immediate use—no surprises, no revisions needed—so you can plug it directly into your planning and competitive analysis.