Torrid Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

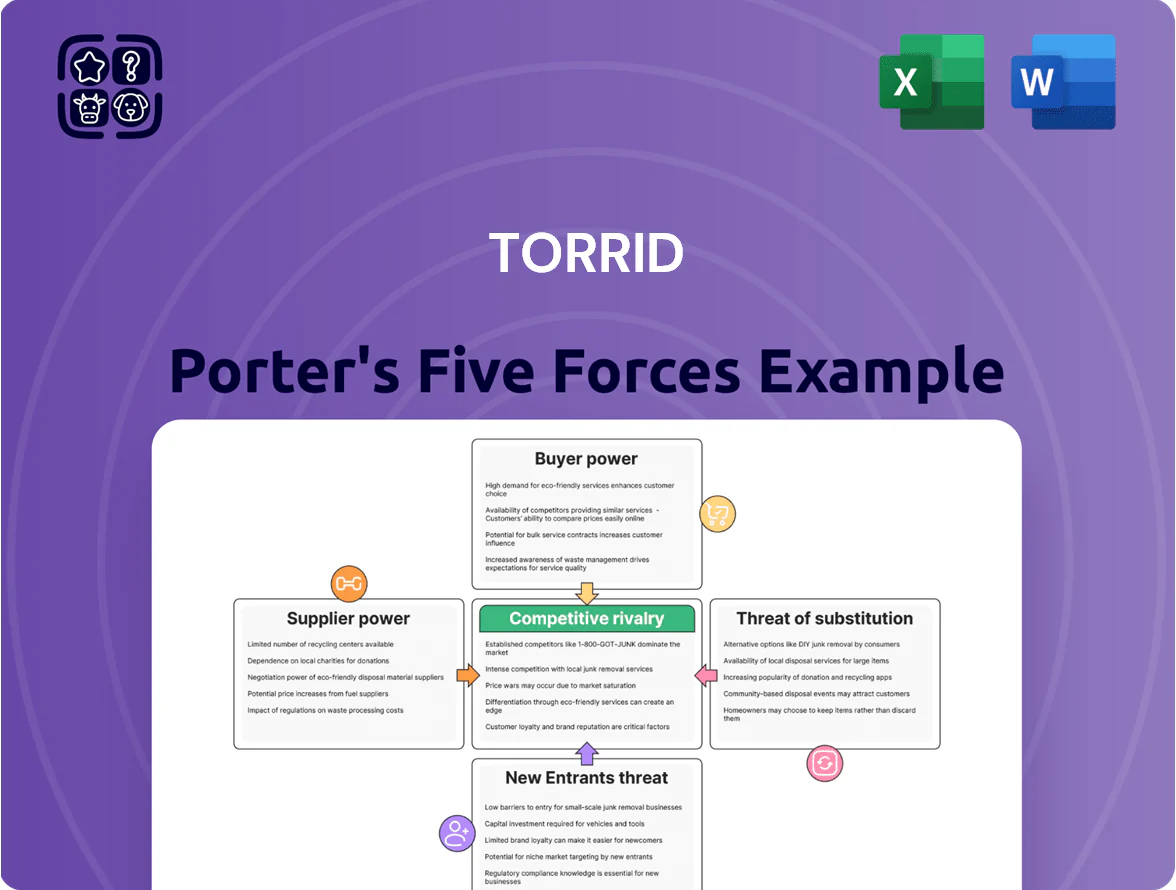

Torrid faces moderate buyer power and niche differentiation, with supplier leverage limited by scale but elevated by specialty sourcing; threats from new entrants are muted by brand and scale, while substitutes and competitive rivalry demand continual product and omni‑channel innovation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Torrid’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Manufacturing Base

The apparel industry has about 60–70% of global garment manufacturing concentrated in Southeast Asia and China, creating a fragmented supplier base that limits individual leverage. Torrid sources from a diverse vendor pool, enabling it to reallocate orders—reducing exposure when tariffs or wage inflation hit, like the 2023 8–12% cost uptick in parts of Vietnam. Fragmentation keeps most suppliers as price-takers competing for contracts from US retailers with combined buying power exceeding $200 billion annually.

Specialized Technical Fit Requirements

Because Torrid targets sizes 10–30, suppliers need niche skills in plus-size patternmaking and fit consistency, shrinking the qualified pool to an estimated 15–25% of apparel factories capable of meeting these specs.

This narrows supply options, creating moderate dependency on high-quality manufacturers; Torrid reported ~62% of women’s bottoms returned for fit issues industrywide, so tight fit control matters for margins.

Switching costs rise versus standard-size retailers, raising supplier leverage slightly, though no single supplier holds absolute power given Torrid’s multi-vendor sourcing strategy.

Raw Material Price Volatility

Suppliers face volatile cotton, synthetic fiber and dye costs—cotton jumped ~40% in 2021–22 and global polyester feedstock rose ~28% in 2021–23—squeezing margins and prompting price renegotiations. Torrid’s scale and $1.2B 2024 revenue give it negotiating power, but commodity spikes (e.g., 2024–25 inflation) let suppliers pass costs through, raising COGS and pressuring margins by several percentage points.

Geopolitical and Logistics Influence

Suppliers in geopolitically unstable regions or those tied to narrow shipping corridors can raise costs or delay goods; in 2024, container rates spiked 60% on some Asia–US routes during port congestion events, hitting apparel imports.

Torrid’s heavy reliance on overseas shipping means container and port capacity often govern inventory flow more than manufacturers; 2025 forecasts showed US port dwell times up 12% year-over-year, shifting leverage to carriers.

As a result, logistics providers and large manufacturing conglomerates that control end-to-end production and shipping hold outsized bargaining power over Torrid’s supply chain and margins.

- Container rate volatility: +60% peak (2024)

- US port dwell times: +12% YoY (2025 forecast)

- Logistics firms control scheduling, fees, capacity

- Large manufacturers offer bundled production+shipping

Lack of Forward Integration

Most Torrid suppliers lack brand equity, US retail footprints, and marketing skill to sell direct; as of FY2024 Torrid reported ~65% of its assortment sourced from such vendors, keeping suppliers dependent on Torrid’s channels.

This inability to forward-integrate keeps bargaining power with Torrid: suppliers focus on cost and efficiency, not consumer marketing, so Torrid controls pricing, placement, and promotion.

- ~65% assortment from non-retail suppliers

- Suppliers prioritize unit-cost cuts over branding

- Torrid controls US distribution and promotion

Torrid’s $1.2B scale vs. supplier squeeze: fit limits and soaring commodity/logistics costs

Torrid faces moderate supplier power: diverse Southeast Asia sourcing and $1.2B 2024 revenue give negotiating clout, but plus-size fit requirements (15–25% capable factories) and 2024–25 commodity/container shocks (cotton +40% in 2021–22; polyester feedstock +28% 2021–23; container rates +60% peak 2024; US port dwell +12% 2025 forecast) raise supplier/logistics leverage.

| Metric | Value |

|---|---|

| 2024 revenue | $1.2B |

| Qualified factories | 15–25% |

| Cotton price change | +40% (2021–22) |

| Polyester feedstock | +28% (2021–23) |

| Container rate spike | +60% (2024 peak) |

| US port dwell forecast | +12% (2025) |

What is included in the product

Tailored Porter’s Five Forces analysis for Torrid that uncovers competitive drivers, supplier and buyer influence, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

Concise Porter's Five Forces summary tailored for Torrid—rapidly assess competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Low Switching Costs for Fashion Consumers

Shoppers in apparel face almost no financial or logistical barriers to switch from Torrid; online conversion rates show 60% of plus-size buyers research multiple retailers before purchase and 45% cite price as the main switch trigger (2024 survey, Coresight Research).

A single click or mall visit lets customers reach competitors—ASOS Curve, Lane Bryant, and Amazon Fashion—so Torrid must invest in loyalty and consistent fit to reduce churn, which rose 2.1% in 2023 without such focus (Torrid investor report, 2024).

High Price Sensitivity in a Soft Economy

Information Transparency and Social Proof

The rise of social media and review sites gives shoppers instant data on Torrid’s fit and quality; 72% of consumers say reviews influence purchases and Torrid saw a 2024 Q4 sales dip after viral fit complaints. A single viral post can sway thousands fast, so Torrid must keep strict QC and respond on channels—Instagram, TikTok, Yelp—to protect brand value and reduce churn.

Expansion of Inclusive Sizing by Mainstream Brands

The entry of Target, Old Navy, and major department stores into extended sizes (Target launched plus-inclusive lines in 2023; Old Navy expanded sizes to 30 in 2024) has widened choices for plus-size shoppers, cutting into Torrid’s niche leverage and increasing buyer bargaining power.

When mainstream brands sell comparable styles at lower prices—Target’s average dress price ~$25 vs Torrid’s ~$60—customers can demand better value, forcing Torrid to defend its premium through fit, exclusive designs, or loyalty perks.

Efficacy of Loyalty Programs

Torrid’s extensive loyalty program targets high buyer power by driving repeat purchases with points, VIP tiers, and member-only deals; in 2024 loyalty members accounted for about 58% of online sales, per company disclosures.

Gamified offers and personalized discounts reduce switching by increasing lifetime value (LTV), though success hinges on perceived reward value versus competitors’ lower prices and fast-fashion promotions.

- 58% of online sales from loyalty members (2024)

- Points, VIP tiers, exclusive deals reduce churn

- Personalization raises AOV (average order value)

- Risk: competitors’ lower prices can erode perceived value

Buyers Hold the Cards: 48% Promo Share, 62% Wait for Deals, 58% Loyalty Online

Buyers have strong leverage: low switching costs, high price sensitivity (62% wait for promos, Kantar 2025), and review-driven churn (viral fit complaints hit Torrid Q4 2024 sales), pushing promo share to 48% of U.S. revenue in FY2024 and loyalty members to 58% of online sales (2024).

| Metric | Value |

|---|---|

| Promo share FY2024 | 48% |

| Loyalty online sales (2024) | 58% |

| Shoppers who wait for promos (2025) | 62% |

| Torrid revenue (2024) | ~$800M |

Full Version Awaits

Torrid Porter's Five Forces Analysis

This preview shows the exact Torrid Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Torrid faces moderate buyer power and niche differentiation, with supplier leverage limited by scale but elevated by specialty sourcing; threats from new entrants are muted by brand and scale, while substitutes and competitive rivalry demand continual product and omni‑channel innovation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Torrid’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Manufacturing Base

The apparel industry has about 60–70% of global garment manufacturing concentrated in Southeast Asia and China, creating a fragmented supplier base that limits individual leverage. Torrid sources from a diverse vendor pool, enabling it to reallocate orders—reducing exposure when tariffs or wage inflation hit, like the 2023 8–12% cost uptick in parts of Vietnam. Fragmentation keeps most suppliers as price-takers competing for contracts from US retailers with combined buying power exceeding $200 billion annually.

Specialized Technical Fit Requirements

Because Torrid targets sizes 10–30, suppliers need niche skills in plus-size patternmaking and fit consistency, shrinking the qualified pool to an estimated 15–25% of apparel factories capable of meeting these specs.

This narrows supply options, creating moderate dependency on high-quality manufacturers; Torrid reported ~62% of women’s bottoms returned for fit issues industrywide, so tight fit control matters for margins.

Switching costs rise versus standard-size retailers, raising supplier leverage slightly, though no single supplier holds absolute power given Torrid’s multi-vendor sourcing strategy.

Raw Material Price Volatility

Suppliers face volatile cotton, synthetic fiber and dye costs—cotton jumped ~40% in 2021–22 and global polyester feedstock rose ~28% in 2021–23—squeezing margins and prompting price renegotiations. Torrid’s scale and $1.2B 2024 revenue give it negotiating power, but commodity spikes (e.g., 2024–25 inflation) let suppliers pass costs through, raising COGS and pressuring margins by several percentage points.

Geopolitical and Logistics Influence

Suppliers in geopolitically unstable regions or those tied to narrow shipping corridors can raise costs or delay goods; in 2024, container rates spiked 60% on some Asia–US routes during port congestion events, hitting apparel imports.

Torrid’s heavy reliance on overseas shipping means container and port capacity often govern inventory flow more than manufacturers; 2025 forecasts showed US port dwell times up 12% year-over-year, shifting leverage to carriers.

As a result, logistics providers and large manufacturing conglomerates that control end-to-end production and shipping hold outsized bargaining power over Torrid’s supply chain and margins.

- Container rate volatility: +60% peak (2024)

- US port dwell times: +12% YoY (2025 forecast)

- Logistics firms control scheduling, fees, capacity

- Large manufacturers offer bundled production+shipping

Lack of Forward Integration

Most Torrid suppliers lack brand equity, US retail footprints, and marketing skill to sell direct; as of FY2024 Torrid reported ~65% of its assortment sourced from such vendors, keeping suppliers dependent on Torrid’s channels.

This inability to forward-integrate keeps bargaining power with Torrid: suppliers focus on cost and efficiency, not consumer marketing, so Torrid controls pricing, placement, and promotion.

- ~65% assortment from non-retail suppliers

- Suppliers prioritize unit-cost cuts over branding

- Torrid controls US distribution and promotion

Torrid’s $1.2B scale vs. supplier squeeze: fit limits and soaring commodity/logistics costs

Torrid faces moderate supplier power: diverse Southeast Asia sourcing and $1.2B 2024 revenue give negotiating clout, but plus-size fit requirements (15–25% capable factories) and 2024–25 commodity/container shocks (cotton +40% in 2021–22; polyester feedstock +28% 2021–23; container rates +60% peak 2024; US port dwell +12% 2025 forecast) raise supplier/logistics leverage.

| Metric | Value |

|---|---|

| 2024 revenue | $1.2B |

| Qualified factories | 15–25% |

| Cotton price change | +40% (2021–22) |

| Polyester feedstock | +28% (2021–23) |

| Container rate spike | +60% (2024 peak) |

| US port dwell forecast | +12% (2025) |

What is included in the product

Tailored Porter’s Five Forces analysis for Torrid that uncovers competitive drivers, supplier and buyer influence, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

Concise Porter's Five Forces summary tailored for Torrid—rapidly assess competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Low Switching Costs for Fashion Consumers

Shoppers in apparel face almost no financial or logistical barriers to switch from Torrid; online conversion rates show 60% of plus-size buyers research multiple retailers before purchase and 45% cite price as the main switch trigger (2024 survey, Coresight Research).

A single click or mall visit lets customers reach competitors—ASOS Curve, Lane Bryant, and Amazon Fashion—so Torrid must invest in loyalty and consistent fit to reduce churn, which rose 2.1% in 2023 without such focus (Torrid investor report, 2024).

High Price Sensitivity in a Soft Economy

Information Transparency and Social Proof

The rise of social media and review sites gives shoppers instant data on Torrid’s fit and quality; 72% of consumers say reviews influence purchases and Torrid saw a 2024 Q4 sales dip after viral fit complaints. A single viral post can sway thousands fast, so Torrid must keep strict QC and respond on channels—Instagram, TikTok, Yelp—to protect brand value and reduce churn.

Expansion of Inclusive Sizing by Mainstream Brands

The entry of Target, Old Navy, and major department stores into extended sizes (Target launched plus-inclusive lines in 2023; Old Navy expanded sizes to 30 in 2024) has widened choices for plus-size shoppers, cutting into Torrid’s niche leverage and increasing buyer bargaining power.

When mainstream brands sell comparable styles at lower prices—Target’s average dress price ~$25 vs Torrid’s ~$60—customers can demand better value, forcing Torrid to defend its premium through fit, exclusive designs, or loyalty perks.

Efficacy of Loyalty Programs

Torrid’s extensive loyalty program targets high buyer power by driving repeat purchases with points, VIP tiers, and member-only deals; in 2024 loyalty members accounted for about 58% of online sales, per company disclosures.

Gamified offers and personalized discounts reduce switching by increasing lifetime value (LTV), though success hinges on perceived reward value versus competitors’ lower prices and fast-fashion promotions.

- 58% of online sales from loyalty members (2024)

- Points, VIP tiers, exclusive deals reduce churn

- Personalization raises AOV (average order value)

- Risk: competitors’ lower prices can erode perceived value

Buyers Hold the Cards: 48% Promo Share, 62% Wait for Deals, 58% Loyalty Online

Buyers have strong leverage: low switching costs, high price sensitivity (62% wait for promos, Kantar 2025), and review-driven churn (viral fit complaints hit Torrid Q4 2024 sales), pushing promo share to 48% of U.S. revenue in FY2024 and loyalty members to 58% of online sales (2024).

| Metric | Value |

|---|---|

| Promo share FY2024 | 48% |

| Loyalty online sales (2024) | 58% |

| Shoppers who wait for promos (2025) | 62% |

| Torrid revenue (2024) | ~$800M |

Full Version Awaits

Torrid Porter's Five Forces Analysis

This preview shows the exact Torrid Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or samples.