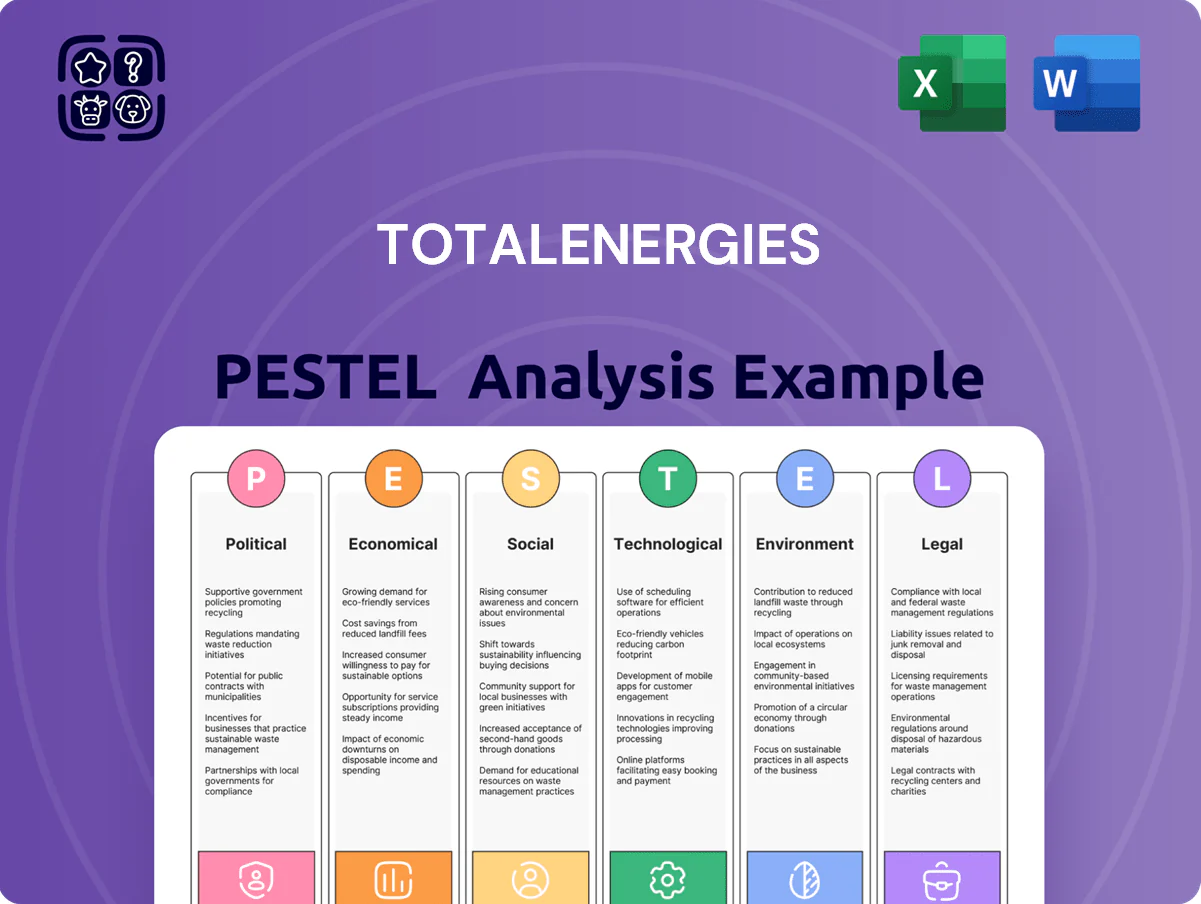

TotalEnergies PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the shifting energy landscape with our PESTLE Analysis of TotalEnergies—concise, data-driven insights on political, economic, social, technological, legal, and environmental forces shaping its strategy; buy the full report to access deep dives, scenario implications, and ready-to-use slides for investment or strategic planning.

Political factors

Geopolitical instability in core production regions

Geopolitical risks remain a primary concern for TotalEnergies as it operates in volatile Middle East and Africa regions where in 2024 roughly 30% of its upstream production was exposed to higher political risk ratings, heightening disruption potential.

Sudden shifts in local governance or regional conflicts can disrupt supply chains and jeopardize physical security of extraction assets, with TotalEnergies reporting security-related outages that impacted ~2–4% of 2023 production in affected fields.

The company must diversify its portfolio across stable jurisdictions—TotalEnergies increased low-risk-region investments by ~15% between 2021–2024—while maintaining delicate diplomatic ties with host governments to protect access and mitigate operational disruptions.

European energy sovereignty and policy alignment

As a French-headquartered major, TotalEnergies is directly affected by EU energy sovereignty drives—Brussels pledged €300bn for energy security 2024–27, boosting LNG terminals and grid upgrades that favor the company’s gas and renewables investments.

Political backing for LNG infrastructure and renewables—EU imports diversification targets cut Russian gas share from 40% in 2021 to ~9% by 2024—supports TotalEnergies’ project pipeline and FID readiness.

Alignment with EU decarbonization increases regulatory pressure: Fit for 55 and REPowerEU push faster hydrocarbon phase-downs, risking asset stranding and accelerating capex shift; TotalEnergies reported €11bn renewables/gas investment guidance for 2024–26.

Strategic partnerships with national oil companies

Maintaining access to low-cost reserves pushes TotalEnergies to cement long-term alliances with national oil companies in Qatar and the UAE, where QatarEnergy and ADNOC control roughly 30% of global LNG export capacity; TotalEnergies holds stakes in projects like QatarEnergy’s North Field expansion supporting its 2024–2026 growth plan.

Influence of global trade sanctions and export controls

International sanctions and export controls limit TotalEnergies exploration and production geography; for example, sanctions on Russia since 2022 cut the company’s Russian oil exposure, contributing to group upstream capex reallocation and a 2023 impairment charge of about €2.8bn tied to geopolitical asset risks.

Strict compliance is essential to avoid fines and preserve banking access—global AML/sanctions enforcement actions rose 18% in 2024—forcing robust screening across ~$70bn annual revenues to prevent market exclusion.

Operational agility is required as geopolitical shifts can freeze assets or close markets overnight, prompting rapid portfolio pivots and accelerated divestments to protect cash flow and credit ratings.

- Sanctions reshape project scope and capex allocation

- Compliance prevents legal, financial and market-access penalties

- Need for rapid operational pivoting and divestment capability

Government incentives for the multi-energy transition

- IRA and EU Green Deal: material IRR uplift for low-carbon projects

- Subsidies de-risk high CAPEX tech like green H2 (est. $1,500–3,000/ton)

- ~€8bn/year renewables CAPEX (2024) focused on incentive-heavy regions

TotalEnergies shifts €11bn to gas/renewables as geopolitics, EU €300bn reshape energy

Geopolitical risk: ~30% upstream exposure to higher-risk ME/Africa (2024); security outages hit ~2–4% 2023 production; EU energy funds €300bn (2024–27) and Russian gas share fell ~40%→9% (2021→2024) boosting LNG/renewables; TotalEnergies guiding ~€11bn (2024–26) to gas/renewables, ~€8bn/year renewables CAPEX (2024); sanctions prompted €2.8bn 2023 impairment.

| Metric | Value |

|---|---|

| High-risk upstream % | ~30% |

| Security outage impact | 2–4% |

| EU energy fund | €300bn (24–27) |

| Renewables CAPEX | ~€8bn/yr (2024) |

| 2023 impairment | €2.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect TotalEnergies across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategy implications for energy transition and global operations.

A concise, visually segmented PESTLE summary of TotalEnergies that’s easy to drop into presentations, share across teams, and annotate for specific regions or business lines to streamline risk discussions and strategic planning.

Economic factors

Volatility in global hydrocarbon and LNG prices

Fluctuations in oil, gas and LNG prices directly affect TotalEnergies cash flow for its energy transition; 2024 average Brent ~USD 84/bbl and Henry Hub ~USD 3.5/MMBtu boosted 2023–24 free cash flow to EUR 20.5bn, enabling renewables and hydrogen investments.

High commodity prices increase liquidity for green expansion, but price shocks—Brent dropping 20% in late 2024—can compress margins and force reprioritization of capex and project timelines.

TotalEnergies maintains a low-breakeven production mix (break-even ≈USD 30–35/bbl for many assets) to preserve resilience across cycles and protect funding for transition projects.

Impact of interest rates on renewable project financing

The cost of capital critically affects profitability for TotalEnergies’ capital‑intensive wind and solar fleets; rising global benchmark rates in 2023–2024 pushed typical project hurdle rates from ~6–7% to 8–10%, raising LCOE pressure and requiring tighter execution to protect returns. TotalEnergies’ A‑/BBB+ style investment‑grade rating enabled access to ~100–200 bps cheaper debt than smaller pure‑plays, lowering financing costs on large projects.

Currency exchange risks between the Euro and US Dollar

TotalEnergies reports in euros while most hydrocarbon sales are dollar-priced, exposing it to EUR/USD translation risk; a 10% EUR appreciation vs USD in 2023 would have reduced dollar-denominated revenues materially, given 2023 consolidated gross margin ~€115 billion.

EUR/USD swings drive volatility in reported earnings and international asset valuations—FX effects accounted for a €2–3 billion swing in adjusted net income in recent years.

The group uses dynamic hedging, commodity collars, and matches debt currency to revenue mix; as of end-2024, about 60% of its net debt was euro-denominated, aligning financing with euro reporting to reduce currency mismatches.

Economic growth patterns in emerging markets

Economic growth in Asia and Africa is driving future energy demand; IMF projects 2024 GDP growth of 4.6% for emerging markets vs 2.9% for advanced economies, with Africa forecast at ~4.0% in 2024.

TotalEnergies is targeting this via integrated LNG-to-power and retail networks, citing ~€6–8bn annual capex in low-carbon and gas projects (2024 guidance range context) to expand footprint.

Success hinges on macro stability and uptake of modern energy; disruptions or slower electrification would materially affect project IRRs and gas-to-power demand curves.

- IMF 2024 EM growth ~4.6%

- Africa GDP ~4.0% (2024)

- TotalEnergies capex shift ~€6–8bn annual in gas/low-carbon (2024 context)

- Risk: macro instability, slow electrification impacts IRR

Cost competitiveness of low-carbon energy vs traditional sources

The pace of TotalEnergies portfolio shift is driven by falling LCOE for renewables: global utility-scale solar LCOE fell to about $28–$35/MWh and onshore wind to $30–$40/MWh in 2024, versus many thermal plants at $60–$120/MWh, making replacement increasingly economic.

Technological gains and scale reduced solar module costs ~20% from 2020–2024 and wind turbine CAPEX down ~15–20%, strengthening the case to displace thermal generation.

TotalEnergies pursues operational excellence—lowering project costs and improving capacity factors—to keep green offers competitive for price-sensitive industrial and retail clients, supporting its 2030 low-carbon capacity targets.

- 2024 solar LCOE ~28–35 $/MWh; onshore wind ~30–40 $/MWh

- Thermal avg. cost range ~$60–120 $/MWh

- Solar module costs down ~20% (2020–2024); wind CAPEX down ~15–20%

- Operational focus to meet 2030 low-carbon capacity goals

Strong oil prices and low LCOE drive €20.5bn FCF, funding low‑carbon growth

Oil/gas price swings drive cash flow (Brent 2024 ~USD84/bbl; Henry Hub ~USD3.5/MMBtu), enabling €20.5bn 2023–24 FCF for low‑carbon capex; break‑even ~USD30–35/bbl preserves resilience. Rising rates lifted project hurdle rates to 8–10% (2023–24); TotalEnergies’ A‑/BBB+ rating lowers funding costs. EM growth (~4.6% 2024) and falling LCOE (solar $28–35/MWh) support gas-to-power and renewables expansion.

| Metric | 2024 value |

|---|---|

| Brent | ~USD84/bbl |

| Henry Hub | ~USD3.5/MMBtu |

| FCF | €20.5bn (2023–24) |

| Solar LCOE | $28–35/MWh |

Preview the Actual Deliverable

TotalEnergies PESTLE Analysis

The preview shown here is the exact TotalEnergies PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or reporting.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the shifting energy landscape with our PESTLE Analysis of TotalEnergies—concise, data-driven insights on political, economic, social, technological, legal, and environmental forces shaping its strategy; buy the full report to access deep dives, scenario implications, and ready-to-use slides for investment or strategic planning.

Political factors

Geopolitical instability in core production regions

Geopolitical risks remain a primary concern for TotalEnergies as it operates in volatile Middle East and Africa regions where in 2024 roughly 30% of its upstream production was exposed to higher political risk ratings, heightening disruption potential.

Sudden shifts in local governance or regional conflicts can disrupt supply chains and jeopardize physical security of extraction assets, with TotalEnergies reporting security-related outages that impacted ~2–4% of 2023 production in affected fields.

The company must diversify its portfolio across stable jurisdictions—TotalEnergies increased low-risk-region investments by ~15% between 2021–2024—while maintaining delicate diplomatic ties with host governments to protect access and mitigate operational disruptions.

European energy sovereignty and policy alignment

As a French-headquartered major, TotalEnergies is directly affected by EU energy sovereignty drives—Brussels pledged €300bn for energy security 2024–27, boosting LNG terminals and grid upgrades that favor the company’s gas and renewables investments.

Political backing for LNG infrastructure and renewables—EU imports diversification targets cut Russian gas share from 40% in 2021 to ~9% by 2024—supports TotalEnergies’ project pipeline and FID readiness.

Alignment with EU decarbonization increases regulatory pressure: Fit for 55 and REPowerEU push faster hydrocarbon phase-downs, risking asset stranding and accelerating capex shift; TotalEnergies reported €11bn renewables/gas investment guidance for 2024–26.

Strategic partnerships with national oil companies

Maintaining access to low-cost reserves pushes TotalEnergies to cement long-term alliances with national oil companies in Qatar and the UAE, where QatarEnergy and ADNOC control roughly 30% of global LNG export capacity; TotalEnergies holds stakes in projects like QatarEnergy’s North Field expansion supporting its 2024–2026 growth plan.

Influence of global trade sanctions and export controls

International sanctions and export controls limit TotalEnergies exploration and production geography; for example, sanctions on Russia since 2022 cut the company’s Russian oil exposure, contributing to group upstream capex reallocation and a 2023 impairment charge of about €2.8bn tied to geopolitical asset risks.

Strict compliance is essential to avoid fines and preserve banking access—global AML/sanctions enforcement actions rose 18% in 2024—forcing robust screening across ~$70bn annual revenues to prevent market exclusion.

Operational agility is required as geopolitical shifts can freeze assets or close markets overnight, prompting rapid portfolio pivots and accelerated divestments to protect cash flow and credit ratings.

- Sanctions reshape project scope and capex allocation

- Compliance prevents legal, financial and market-access penalties

- Need for rapid operational pivoting and divestment capability

Government incentives for the multi-energy transition

- IRA and EU Green Deal: material IRR uplift for low-carbon projects

- Subsidies de-risk high CAPEX tech like green H2 (est. $1,500–3,000/ton)

- ~€8bn/year renewables CAPEX (2024) focused on incentive-heavy regions

TotalEnergies shifts €11bn to gas/renewables as geopolitics, EU €300bn reshape energy

Geopolitical risk: ~30% upstream exposure to higher-risk ME/Africa (2024); security outages hit ~2–4% 2023 production; EU energy funds €300bn (2024–27) and Russian gas share fell ~40%→9% (2021→2024) boosting LNG/renewables; TotalEnergies guiding ~€11bn (2024–26) to gas/renewables, ~€8bn/year renewables CAPEX (2024); sanctions prompted €2.8bn 2023 impairment.

| Metric | Value |

|---|---|

| High-risk upstream % | ~30% |

| Security outage impact | 2–4% |

| EU energy fund | €300bn (24–27) |

| Renewables CAPEX | ~€8bn/yr (2024) |

| 2023 impairment | €2.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect TotalEnergies across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategy implications for energy transition and global operations.

A concise, visually segmented PESTLE summary of TotalEnergies that’s easy to drop into presentations, share across teams, and annotate for specific regions or business lines to streamline risk discussions and strategic planning.

Economic factors

Volatility in global hydrocarbon and LNG prices

Fluctuations in oil, gas and LNG prices directly affect TotalEnergies cash flow for its energy transition; 2024 average Brent ~USD 84/bbl and Henry Hub ~USD 3.5/MMBtu boosted 2023–24 free cash flow to EUR 20.5bn, enabling renewables and hydrogen investments.

High commodity prices increase liquidity for green expansion, but price shocks—Brent dropping 20% in late 2024—can compress margins and force reprioritization of capex and project timelines.

TotalEnergies maintains a low-breakeven production mix (break-even ≈USD 30–35/bbl for many assets) to preserve resilience across cycles and protect funding for transition projects.

Impact of interest rates on renewable project financing

The cost of capital critically affects profitability for TotalEnergies’ capital‑intensive wind and solar fleets; rising global benchmark rates in 2023–2024 pushed typical project hurdle rates from ~6–7% to 8–10%, raising LCOE pressure and requiring tighter execution to protect returns. TotalEnergies’ A‑/BBB+ style investment‑grade rating enabled access to ~100–200 bps cheaper debt than smaller pure‑plays, lowering financing costs on large projects.

Currency exchange risks between the Euro and US Dollar

TotalEnergies reports in euros while most hydrocarbon sales are dollar-priced, exposing it to EUR/USD translation risk; a 10% EUR appreciation vs USD in 2023 would have reduced dollar-denominated revenues materially, given 2023 consolidated gross margin ~€115 billion.

EUR/USD swings drive volatility in reported earnings and international asset valuations—FX effects accounted for a €2–3 billion swing in adjusted net income in recent years.

The group uses dynamic hedging, commodity collars, and matches debt currency to revenue mix; as of end-2024, about 60% of its net debt was euro-denominated, aligning financing with euro reporting to reduce currency mismatches.

Economic growth patterns in emerging markets

Economic growth in Asia and Africa is driving future energy demand; IMF projects 2024 GDP growth of 4.6% for emerging markets vs 2.9% for advanced economies, with Africa forecast at ~4.0% in 2024.

TotalEnergies is targeting this via integrated LNG-to-power and retail networks, citing ~€6–8bn annual capex in low-carbon and gas projects (2024 guidance range context) to expand footprint.

Success hinges on macro stability and uptake of modern energy; disruptions or slower electrification would materially affect project IRRs and gas-to-power demand curves.

- IMF 2024 EM growth ~4.6%

- Africa GDP ~4.0% (2024)

- TotalEnergies capex shift ~€6–8bn annual in gas/low-carbon (2024 context)

- Risk: macro instability, slow electrification impacts IRR

Cost competitiveness of low-carbon energy vs traditional sources

The pace of TotalEnergies portfolio shift is driven by falling LCOE for renewables: global utility-scale solar LCOE fell to about $28–$35/MWh and onshore wind to $30–$40/MWh in 2024, versus many thermal plants at $60–$120/MWh, making replacement increasingly economic.

Technological gains and scale reduced solar module costs ~20% from 2020–2024 and wind turbine CAPEX down ~15–20%, strengthening the case to displace thermal generation.

TotalEnergies pursues operational excellence—lowering project costs and improving capacity factors—to keep green offers competitive for price-sensitive industrial and retail clients, supporting its 2030 low-carbon capacity targets.

- 2024 solar LCOE ~28–35 $/MWh; onshore wind ~30–40 $/MWh

- Thermal avg. cost range ~$60–120 $/MWh

- Solar module costs down ~20% (2020–2024); wind CAPEX down ~15–20%

- Operational focus to meet 2030 low-carbon capacity goals

Strong oil prices and low LCOE drive €20.5bn FCF, funding low‑carbon growth

Oil/gas price swings drive cash flow (Brent 2024 ~USD84/bbl; Henry Hub ~USD3.5/MMBtu), enabling €20.5bn 2023–24 FCF for low‑carbon capex; break‑even ~USD30–35/bbl preserves resilience. Rising rates lifted project hurdle rates to 8–10% (2023–24); TotalEnergies’ A‑/BBB+ rating lowers funding costs. EM growth (~4.6% 2024) and falling LCOE (solar $28–35/MWh) support gas-to-power and renewables expansion.

| Metric | 2024 value |

|---|---|

| Brent | ~USD84/bbl |

| Henry Hub | ~USD3.5/MMBtu |

| FCF | €20.5bn (2023–24) |

| Solar LCOE | $28–35/MWh |

Preview the Actual Deliverable

TotalEnergies PESTLE Analysis

The preview shown here is the exact TotalEnergies PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or reporting.