Totally Porter's Five Forces Analysis

Don't Miss the Bigger Picture

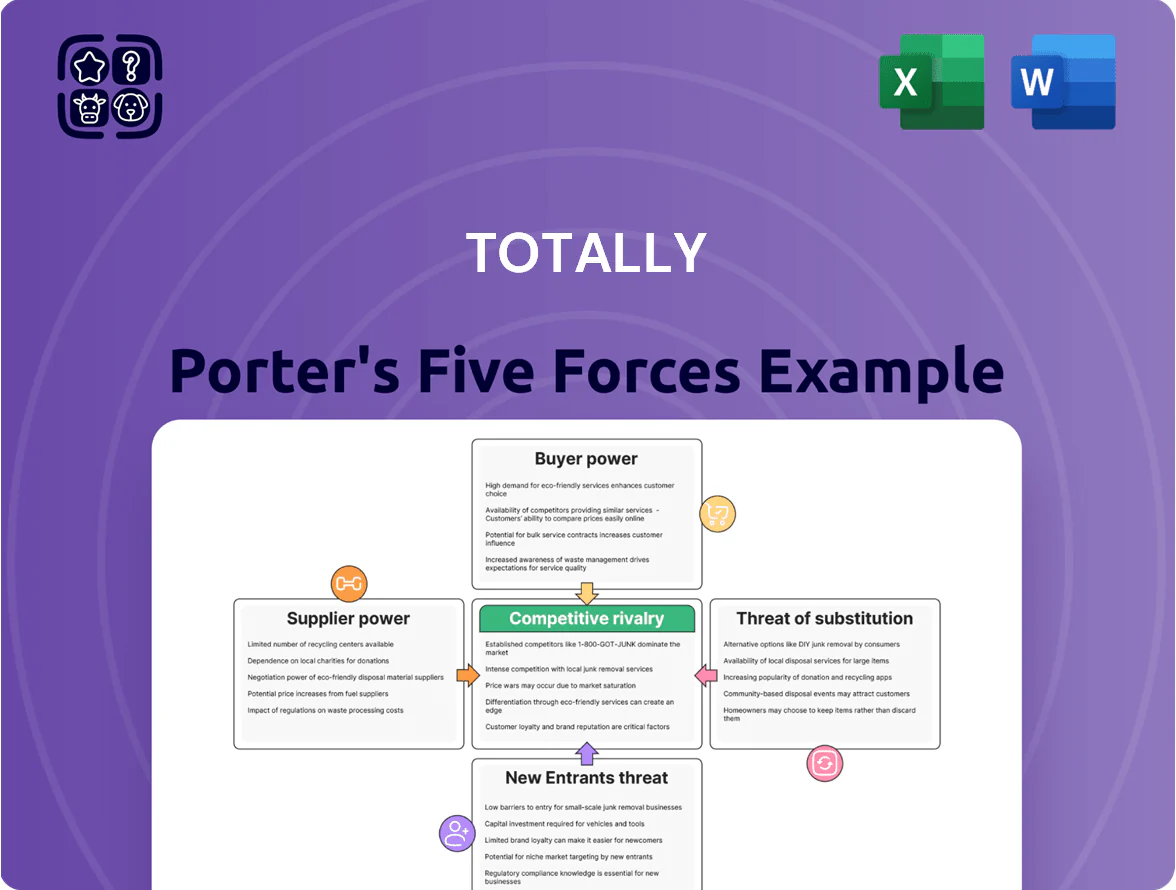

Totally’s snapshot reveals initial pressure points—supplier leverage, buyer sensitivity, and newcomer risks—that shape competitive intensity and margins.

This brief just scratches the surface; unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable implications tailored to Totally for smarter strategy and investment decisions.

Suppliers Bargaining Power

Clinical Labor Scarcity

The UK faces a chronic shortfall of clinical staff—NHS vacancies hit 133,000 in Sept 2025—giving doctors and nurses leverage over providers; Totally plc must compete with the NHS and private firms for this scarce pool.

Scarcity pushes up pay: agency nursing rates rose ~35% between 2021–2024 and median locum doctor day rates reached ~£650 in 2024, forcing higher operating costs for Totally.

Specialized Medical Equipment

The company depends on a handful of global makers for high-end diagnostic and elective-care gear; the top three suppliers control about 68% of the market for MRI/robotic systems (2024), giving them pricing and delivery leverage. Their proprietary tech and multi-year maintenance contracts (avg. 7–10 years, often with 15–20% annual escalation clauses) are hard to exit, raising switching costs. A 2023 supply shock showed 12–18% service delays, directly cutting specialized service capacity and revenue.

Pharmaceutical Pricing

As an urgent and elective care provider, Totally faces supplier price power from major pharmaceutical wholesalers that set list prices and volume discounts; in 2024 UK drug wholesale margins averaged 6–8% while list price inflation ran about 4.5% year-on-year, raising consumable costs.

Although the NHS negotiates national rates—saving roughly £1.2bn via single-source deals in 2023—private providers like Totally absorb fluctuating meds costs, since NHS contract prices often stay fixed for 12–24 months.

That mismatch can compress margins: a 5% rise in drug costs could cut operating margin by ~1.5 percentage points on a typical private clinic with 30% gross margin, so supplier pricing power materially threatens profitability.

Digital Infrastructure Partners

The shift to integrated care makes third-party digital infrastructure partners critical; global health IT spending hit an estimated $250B in 2024, concentrating power with firms that host EHRs and data platforms.

High migration complexity and switching costs—often $5M–$50M per large hospital system and 12–24 months—give suppliers leverage and raise vendor-lock risks.

Reliable partners are essential to meet HIPAA, GDPR and NIST requirements; breaches cost healthcare a mean $10.1M per incident in 2023, so security capability drives supplier bargaining power.

- Global health IT spend ≈ $250B (2024)

- Hospital migration cost $5M–$50M

- Migration 12–24 months

- Avg breach cost $10.1M (2023)

Facility and Estate Management

Totally plc relies heavily on leased clinical space, so landlord power matters: UK commercial rent index rose 6.8% in 2024, squeezing margins and raising operating costs.

Specialized medical fit-outs cost £450–700 per sqm (NHS benchmark 2023), limiting quick relocations and increasing capex needs.

Long-term leases secure patient continuity but lock the firm into locations and reduce agility.

- Rent inflation 6.8% (UK, 2024)

- Fit-out £450–700/sqm (NHS 2023)

- Long leases = continuity vs agility trade-off

Supplier power squeezes Totally plc: staffing shortages, concentrated vendors and rising costs

Suppliers hold strong leverage over Totally plc: clinical staff shortages (NHS vacancies 133,000 Sept 2025) and 35% rise in agency nursing (2021–24) drive labor costs; top 3 MRI/robotics suppliers control ~68% (2024), while drug list-price inflation ~4.5% (2024) and £450–700/sqm fit-out costs plus 6.8% rent inflation (UK, 2024) raise switching costs and compress margins.

| Metric | Value |

|---|---|

| NHS vacancies | 133,000 (Sep 2025) |

| Agency nursing rise | ~35% (2021–24) |

| Top-3 suppliers | ~68% market (MRI/robotics, 2024) |

| Drug inflation | ~4.5% (2024) |

| Rent inflation | 6.8% (UK, 2024) |

| Fit-out cost | £450–700/sqm (NHS 2023) |

What is included in the product

Comprehensive Five Forces assessment for Totally that quantifies competitive intensity, buyer/supplier power, substitute threats, and entry barriers, highlighting disruptive risks and strategic levers to defend market share—delivered in an editable format for investor decks and internal strategy use.

Interactive Porter’s Five Forces one-sheet that quantifies competitive pressure, letting teams quickly pinpoint and mitigate strategic risks with customizable scores and a ready-to-use radar chart for presentations.

Customers Bargaining Power

NHS Monopsony Power

The NHS is Totally’s dominant buyer: in 2024 about 70–80% of UK community healthcare spend routes through the NHS, giving it monopsony leverage in contracting.

Integrated Care Boards set price caps and quality targets; failing to meet them risks losing multi-year contracts that made up 82% of Totally’s 2023 revenue.

Concentrated NHS buying power constrains Totally’s pricing freedom—price increases are capped by annual NHS budget settlements (0.4% real-terms change in 2024/25).

Stringent Performance Metrics

Contracts with public health bodies tie payments to KPIs like 18-week referral-to-treatment targets and 92% A&E 4-hour waits; in 2024 UK trusts faced £150m+ in penalties for missed targets, so failure risks fines or non-renewal of lucrative contracts. This bargaining power forces Totally to focus on efficiency and quality—Totally must meet targets or lose up to an estimated 10–20% of contract value, so operational metrics drive strategy.

Patient Choice Initiatives

Patient Choice Initiatives shift power to individuals in elective care: 48% of UK elective patients (2024 NHS report) now can pick providers, so Totally can win higher referral share but must spend—marketing budgets may need 3–6% of revenue (industry benchmark) to maintain visibility. A 0.5-point drop in satisfaction (Net Promoter Score) can cut volumes by ~8% within 12 months, moving business to private or public rivals, so reputation management is critical.

Budgetary Constraints of ICBs

The financial health of Integrated Care Boards (ICBs) drives outsourced volume: NHS England reported 42% of ICBs in 2024 had deficits, shrinking discretionary spend and lowering contract awards to private providers.

When public funding tightens, buyers may in-source services or demand double-digit price cuts at tenders—NHS procurement saw average margin compression of 6–12% in 2023–24.

Revenue for private providers thus tracks national fiscal policy and NHS settlements, creating volatility in cashflow and capacity planning.

- 42% of ICBs in deficit (NHS England 2024)

- 6–12% average margin compression in procurement (2023–24)

- High sensitivity to annual NHS funding settlements

Transparency in Tendering

The public nature of healthcare procurement lets buyers compare costs and outcomes across providers, increasing transparency; in 2024 UK NHS tender data showed average price variance of 22% across shortlisted suppliers, making it easy to spot lower-cost options.

This competitive bidding limits Totally’s ability to sustain high margins, as procurement teams routinely award contracts to bids 10–15% below incumbents; margin compression is visible in sector-wide average gross margins falling from 28% (2019) to 20% (2023).

Buyers demand clear value-for-money evidence—cost per patient, outcome metrics, and real-world evidence—so Totally faces constant pressure to justify pricing and demonstrate measurable savings or outcomes.

- Public tenders enable direct cost/outcome comparisons

- 2024 tender variance ~22%, making low bids easy to find

- Contracts often awarded 10–15% below incumbents

- Sector gross margins fell from 28% (2019) to 20% (2023)

- Procurement requires strong cost-per-outcome proof

NHS monopsony squeezes Totally: margins compressed as ICB deficits force efficiency

The NHS is Totally’s dominant monopsony buyer (70–80% community spend, 2024), constraining prices via ICB-set caps and KPI-linked contracts (82% of Totally’s 2023 revenue). Financial strain in ICBs (42% in deficit, 2024) and procurement-driven margin compression (6–12% tender pressure; sector gross margins 28%→20% 2019–23) force efficiency, outcomes evidence, and marketing to protect elective volumes.

| Metric | Value |

|---|---|

| NHS share of spend (2024) | 70–80% |

| Totally revenue from multi‑year contracts (2023) | 82% |

| ICBs in deficit (2024) | 42% |

| Procurement margin compression (2023–24) | 6–12% |

| Sector gross margin 2019→2023 | 28%→20% |

Full Version Awaits

Totally Porter's Five Forces Analysis

This preview shows the exact Totally Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted, professional, and ready to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Totally’s snapshot reveals initial pressure points—supplier leverage, buyer sensitivity, and newcomer risks—that shape competitive intensity and margins.

This brief just scratches the surface; unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable implications tailored to Totally for smarter strategy and investment decisions.

Suppliers Bargaining Power

Clinical Labor Scarcity

The UK faces a chronic shortfall of clinical staff—NHS vacancies hit 133,000 in Sept 2025—giving doctors and nurses leverage over providers; Totally plc must compete with the NHS and private firms for this scarce pool.

Scarcity pushes up pay: agency nursing rates rose ~35% between 2021–2024 and median locum doctor day rates reached ~£650 in 2024, forcing higher operating costs for Totally.

Specialized Medical Equipment

The company depends on a handful of global makers for high-end diagnostic and elective-care gear; the top three suppliers control about 68% of the market for MRI/robotic systems (2024), giving them pricing and delivery leverage. Their proprietary tech and multi-year maintenance contracts (avg. 7–10 years, often with 15–20% annual escalation clauses) are hard to exit, raising switching costs. A 2023 supply shock showed 12–18% service delays, directly cutting specialized service capacity and revenue.

Pharmaceutical Pricing

As an urgent and elective care provider, Totally faces supplier price power from major pharmaceutical wholesalers that set list prices and volume discounts; in 2024 UK drug wholesale margins averaged 6–8% while list price inflation ran about 4.5% year-on-year, raising consumable costs.

Although the NHS negotiates national rates—saving roughly £1.2bn via single-source deals in 2023—private providers like Totally absorb fluctuating meds costs, since NHS contract prices often stay fixed for 12–24 months.

That mismatch can compress margins: a 5% rise in drug costs could cut operating margin by ~1.5 percentage points on a typical private clinic with 30% gross margin, so supplier pricing power materially threatens profitability.

Digital Infrastructure Partners

The shift to integrated care makes third-party digital infrastructure partners critical; global health IT spending hit an estimated $250B in 2024, concentrating power with firms that host EHRs and data platforms.

High migration complexity and switching costs—often $5M–$50M per large hospital system and 12–24 months—give suppliers leverage and raise vendor-lock risks.

Reliable partners are essential to meet HIPAA, GDPR and NIST requirements; breaches cost healthcare a mean $10.1M per incident in 2023, so security capability drives supplier bargaining power.

- Global health IT spend ≈ $250B (2024)

- Hospital migration cost $5M–$50M

- Migration 12–24 months

- Avg breach cost $10.1M (2023)

Facility and Estate Management

Totally plc relies heavily on leased clinical space, so landlord power matters: UK commercial rent index rose 6.8% in 2024, squeezing margins and raising operating costs.

Specialized medical fit-outs cost £450–700 per sqm (NHS benchmark 2023), limiting quick relocations and increasing capex needs.

Long-term leases secure patient continuity but lock the firm into locations and reduce agility.

- Rent inflation 6.8% (UK, 2024)

- Fit-out £450–700/sqm (NHS 2023)

- Long leases = continuity vs agility trade-off

Supplier power squeezes Totally plc: staffing shortages, concentrated vendors and rising costs

Suppliers hold strong leverage over Totally plc: clinical staff shortages (NHS vacancies 133,000 Sept 2025) and 35% rise in agency nursing (2021–24) drive labor costs; top 3 MRI/robotics suppliers control ~68% (2024), while drug list-price inflation ~4.5% (2024) and £450–700/sqm fit-out costs plus 6.8% rent inflation (UK, 2024) raise switching costs and compress margins.

| Metric | Value |

|---|---|

| NHS vacancies | 133,000 (Sep 2025) |

| Agency nursing rise | ~35% (2021–24) |

| Top-3 suppliers | ~68% market (MRI/robotics, 2024) |

| Drug inflation | ~4.5% (2024) |

| Rent inflation | 6.8% (UK, 2024) |

| Fit-out cost | £450–700/sqm (NHS 2023) |

What is included in the product

Comprehensive Five Forces assessment for Totally that quantifies competitive intensity, buyer/supplier power, substitute threats, and entry barriers, highlighting disruptive risks and strategic levers to defend market share—delivered in an editable format for investor decks and internal strategy use.

Interactive Porter’s Five Forces one-sheet that quantifies competitive pressure, letting teams quickly pinpoint and mitigate strategic risks with customizable scores and a ready-to-use radar chart for presentations.

Customers Bargaining Power

NHS Monopsony Power

The NHS is Totally’s dominant buyer: in 2024 about 70–80% of UK community healthcare spend routes through the NHS, giving it monopsony leverage in contracting.

Integrated Care Boards set price caps and quality targets; failing to meet them risks losing multi-year contracts that made up 82% of Totally’s 2023 revenue.

Concentrated NHS buying power constrains Totally’s pricing freedom—price increases are capped by annual NHS budget settlements (0.4% real-terms change in 2024/25).

Stringent Performance Metrics

Contracts with public health bodies tie payments to KPIs like 18-week referral-to-treatment targets and 92% A&E 4-hour waits; in 2024 UK trusts faced £150m+ in penalties for missed targets, so failure risks fines or non-renewal of lucrative contracts. This bargaining power forces Totally to focus on efficiency and quality—Totally must meet targets or lose up to an estimated 10–20% of contract value, so operational metrics drive strategy.

Patient Choice Initiatives

Patient Choice Initiatives shift power to individuals in elective care: 48% of UK elective patients (2024 NHS report) now can pick providers, so Totally can win higher referral share but must spend—marketing budgets may need 3–6% of revenue (industry benchmark) to maintain visibility. A 0.5-point drop in satisfaction (Net Promoter Score) can cut volumes by ~8% within 12 months, moving business to private or public rivals, so reputation management is critical.

Budgetary Constraints of ICBs

The financial health of Integrated Care Boards (ICBs) drives outsourced volume: NHS England reported 42% of ICBs in 2024 had deficits, shrinking discretionary spend and lowering contract awards to private providers.

When public funding tightens, buyers may in-source services or demand double-digit price cuts at tenders—NHS procurement saw average margin compression of 6–12% in 2023–24.

Revenue for private providers thus tracks national fiscal policy and NHS settlements, creating volatility in cashflow and capacity planning.

- 42% of ICBs in deficit (NHS England 2024)

- 6–12% average margin compression in procurement (2023–24)

- High sensitivity to annual NHS funding settlements

Transparency in Tendering

The public nature of healthcare procurement lets buyers compare costs and outcomes across providers, increasing transparency; in 2024 UK NHS tender data showed average price variance of 22% across shortlisted suppliers, making it easy to spot lower-cost options.

This competitive bidding limits Totally’s ability to sustain high margins, as procurement teams routinely award contracts to bids 10–15% below incumbents; margin compression is visible in sector-wide average gross margins falling from 28% (2019) to 20% (2023).

Buyers demand clear value-for-money evidence—cost per patient, outcome metrics, and real-world evidence—so Totally faces constant pressure to justify pricing and demonstrate measurable savings or outcomes.

- Public tenders enable direct cost/outcome comparisons

- 2024 tender variance ~22%, making low bids easy to find

- Contracts often awarded 10–15% below incumbents

- Sector gross margins fell from 28% (2019) to 20% (2023)

- Procurement requires strong cost-per-outcome proof

NHS monopsony squeezes Totally: margins compressed as ICB deficits force efficiency

The NHS is Totally’s dominant monopsony buyer (70–80% community spend, 2024), constraining prices via ICB-set caps and KPI-linked contracts (82% of Totally’s 2023 revenue). Financial strain in ICBs (42% in deficit, 2024) and procurement-driven margin compression (6–12% tender pressure; sector gross margins 28%→20% 2019–23) force efficiency, outcomes evidence, and marketing to protect elective volumes.

| Metric | Value |

|---|---|

| NHS share of spend (2024) | 70–80% |

| Totally revenue from multi‑year contracts (2023) | 82% |

| ICBs in deficit (2024) | 42% |

| Procurement margin compression (2023–24) | 6–12% |

| Sector gross margin 2019→2023 | 28%→20% |

Full Version Awaits

Totally Porter's Five Forces Analysis

This preview shows the exact Totally Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted, professional, and ready to download and use the moment you buy.