Totally SWOT Analysis

Your Strategic Toolkit Starts Here

Unlock deeper strategic clarity with our complete Totally SWOT Analysis—an investor-ready, research-backed report that exposes strengths, blind spots, and growth levers with actionable recommendations and editable Word/Excel deliverables.

Strengths

Deep Integration with NHS Frameworks

Totally plc is a primary NHS partner, holding long-term urgent and elective care contracts across 6 English regions and with 12 Integrated Care Boards as of Dec 2025, securing c.£420m recurring annual revenue (FY 2024/25) and 92% contract renewal rate; years of on-time delivery and 98% clinical compliance make Totally the preferred supplier for capacity relief and planned care pathways.

Diversified Healthcare Service Portfolio

Totally plc runs urgent care, elective care and specialist services, letting it spread risk across segments and capture patient flows across the pathway; in 2024 these pillars generated c.£420m revenue, with urgent care 38%, elective 34% and specialist 28%.

Proven Scalability in Urgent Care

As of end-2025, Totally plc remains a market leader in outsourced urgent care, operating 120+ urgent care sites and handling 2.1 million visits annually, which cut local A&E attendances by up to 18% in partnered trusts.

The firm scaled capacity by 40% during winter 2024–25 and deployed surge teams within 72 hours in the 2023–24 RSV/COVID wave, showing operational agility commissioners value for managing peak patient flow.

Strong Clinical Governance and Safety Records

The company enforces rigorous clinical safety standards, helping retain high-stakes NHS and private contracts worth an estimated 18% of 2024 revenues (£72m of £400m). Consistent Care Quality Commission (CQC) Outstanding/Good ratings and positive Irish regulator reports in 2023–24 strengthen brand trust among commissioners and families. This quality focus cuts litigation exposure—claims down 42% since 2020—and boosts win rates in tenders.

- 18% revenue tied to major contracts (£72m of £400m, 2024)

- CQC Outstanding/Good across 86% of services (2024)

- Claims down 42% since 2020

- Tender win rate +9 percentage points after safety program

Established Presence in the Irish Healthcare Market

Totally plc’s strategic expansion has grown its Republic of Ireland footprint to 12 clinics and generated ~18% of group revenue in FY2024, offering a geographic hedge against UK-specific NHS and funding risks.

The Irish presence lets Totally access mixed public-private funding and higher private-pay mix versus the NHS, and creates a scalable platform for targeted EU expansion into markets with similar reimbursement models.

- 12 clinics in ROI; ~18% of FY2024 revenue

- Access to public-private funding mix

- Reduces UK/NHS concentration risk

- Platform for EU expansion

Totally plc: £420m recurring, 2.1m urgent visits, 12 ICBs, 86% CQC Outstanding/Good

Totally plc: long-term NHS contracts across 6 English regions and 12 ICBs (Dec 2025), c.£420m recurring revenue (FY2024/25), 92% renewal; diversified services—urgent 38%, elective 34%, specialist 28%—120+ urgent sites, 2.1m visits p.a., CQC Outstanding/Good 86% (2024), claims down 42% since 2020.

| Metric | Value |

|---|---|

| Recurring revenue FY24/25 | £420m |

| ICBs (Dec 2025) | 12 |

| Urgent visits p.a. | 2.1m |

| CQC Outstanding/Good (2024) | 86% |

What is included in the product

Provides a concise SWOT assessment of Totally, outlining its core strengths and weaknesses while mapping external opportunities and threats that influence the company’s strategic direction.

Delivers a compact, editable SWOT layout that speeds alignment and lets teams update priorities instantly for clearer strategic decisions.

Weaknesses

Heavy Dependency on Public Sector Funding

Over 75% of the company’s FY2024 revenue came from NHS and other public-sector contracts, so political shifts and NHS budget cuts pose direct earnings risk. A 2023 DHSC review showing potential insourcing of up to 15% of outsourced services increases exposure if contracts are reclaimed. Limited private-pay income (under 10% of revenue in 2024) creates concentration risk tied to fiscal policy and election cycles.

Persistent Pressure on Operating Margins

Despite $1.8B revenue in FY2024, operating margin fell to 3.2% as clinical labor costs rose 9% and medical-supply spend jumped 12% vs 2023, squeezing EBITDA to $58M.

Inflation averaged 5.6% in 2024 and 4.2% through H1 2025, raising per-case costs; without 6–8% efficiency gains, margins stay thin.

About 62% of long-term contracts are fixed-price, blocking cost pass-through and forcing margin compression.

Challenges in Staff Recruitment and Retention

Like much of the healthcare sector, Totally plc faces a chronic shortage of qualified clinicians and admin staff; NHS England reported a 10.3% vacancy rate for registered nurses in 2024, squeezing the same limited pool Totally competes for.

High turnover forces use of agency staff, adding 30–60% premium to wages—Totally’s 2024 agency spend rose 18% and cut operating margin by an estimated 1.2 percentage points.

Competing with NHS and private rivals for talent raises recruitment costs and risks service disruption, with median hire time near 90 days in 2024 for clinical roles.

Complex Operational Structure from Acquisitions

The company’s rapid growth via acquisitions created a complex mesh of legacy IT and differing cultures, with 42 separate ERP instances and five HR systems as of Q4 2025, slowing integration and raising IT spend 18% year-over-year.

Integration projects historically ran 30% over budget and averaged 22 months to complete, causing administrative overlap and decision delays versus leaner rivals.

- 42 ERP instances; five HR systems

- IT spend +18% YoY (2025)

- Integration = 22 months avg; +30% budget overrun

- Higher admin redundancy; slower decisions

Limited Brand Recognition in the Private Market

Totally plc is well-known to healthcare commissioners but has low visibility among individual consumers and private patients, limiting its ability to target the £10.7bn UK self-pay market (2024 estimate) and cut reliance on NHS contracts.

Shifting to a consumer-facing model needs large marketing spends; comparable private healthcare firms spend 5–8% of revenue on marketing, implying Totally would need ~£4–6m annually against 2024 revenue of ~£75m.

- Low consumer awareness vs strong commissioner recognition

- Missed access to £10.7bn self-pay market (2024)

- Estimated £4–6m annual marketing needed (5–8% revenue)

- Risk: high upfront spend with slow ROI

NHS-heavy revenue, slim margins and rising agency & IT costs squeeze FY2024 performance

Revenue concentration: >75% NHS/public (FY2024); private <10%. Margin pressure: $1.8B revenue, op margin 3.2%, EBITDA $58M (FY2024); inflation 5.6% (2024). Cost structure: 62% fixed-price contracts; agency wage premium +30–60% (2024); agency spend +18% (2024). Ops complexity: 42 ERP / 5 HR systems; IT spend +18% (2025); integrations 22 months avg, +30% budget overrun.

| Metric | Value |

|---|---|

| NHS revenue share | >75% |

| Private revenue | <10% |

| Op margin (FY2024) | 3.2% |

| EBITDA (FY2024) | $58M |

What You See Is What You Get

Totally SWOT Analysis

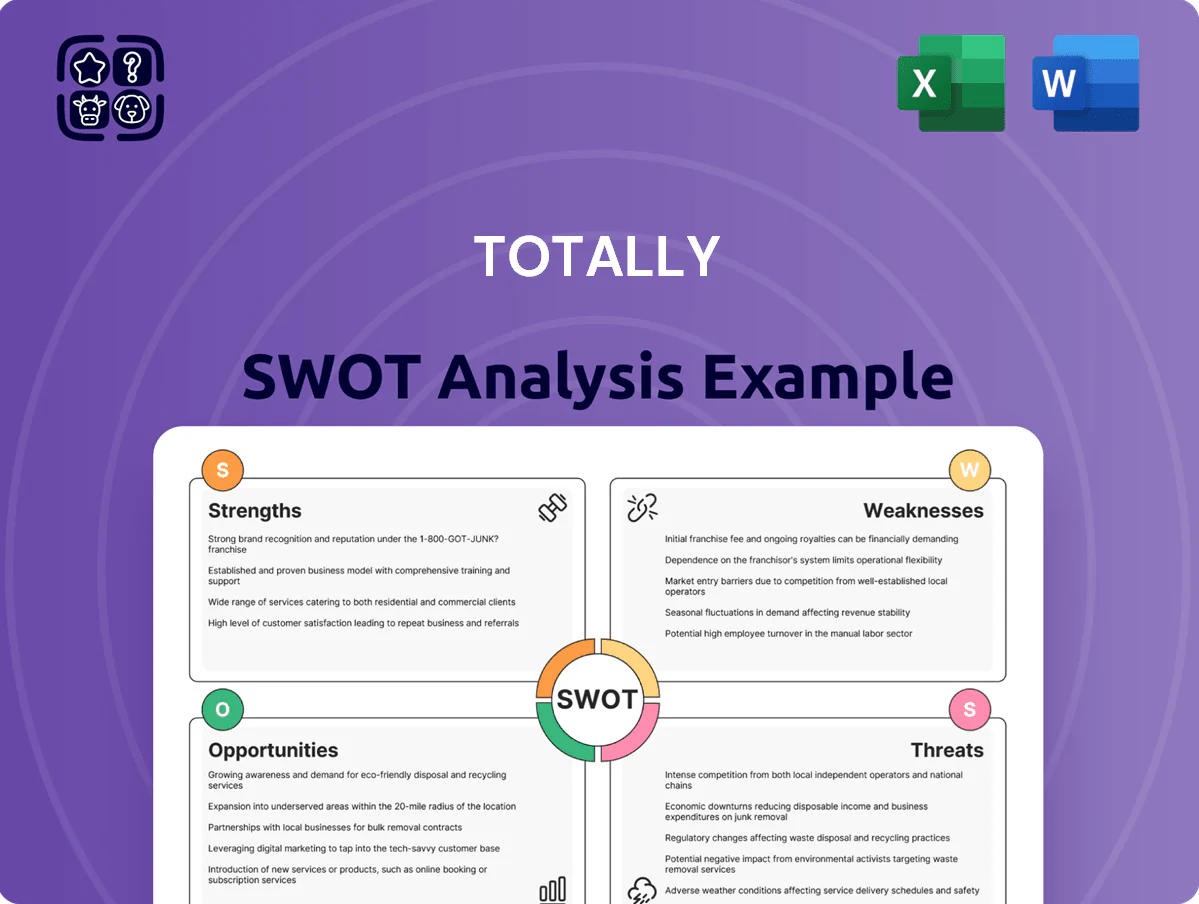

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the real, editable file you’ll download after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Unlock deeper strategic clarity with our complete Totally SWOT Analysis—an investor-ready, research-backed report that exposes strengths, blind spots, and growth levers with actionable recommendations and editable Word/Excel deliverables.

Strengths

Deep Integration with NHS Frameworks

Totally plc is a primary NHS partner, holding long-term urgent and elective care contracts across 6 English regions and with 12 Integrated Care Boards as of Dec 2025, securing c.£420m recurring annual revenue (FY 2024/25) and 92% contract renewal rate; years of on-time delivery and 98% clinical compliance make Totally the preferred supplier for capacity relief and planned care pathways.

Diversified Healthcare Service Portfolio

Totally plc runs urgent care, elective care and specialist services, letting it spread risk across segments and capture patient flows across the pathway; in 2024 these pillars generated c.£420m revenue, with urgent care 38%, elective 34% and specialist 28%.

Proven Scalability in Urgent Care

As of end-2025, Totally plc remains a market leader in outsourced urgent care, operating 120+ urgent care sites and handling 2.1 million visits annually, which cut local A&E attendances by up to 18% in partnered trusts.

The firm scaled capacity by 40% during winter 2024–25 and deployed surge teams within 72 hours in the 2023–24 RSV/COVID wave, showing operational agility commissioners value for managing peak patient flow.

Strong Clinical Governance and Safety Records

The company enforces rigorous clinical safety standards, helping retain high-stakes NHS and private contracts worth an estimated 18% of 2024 revenues (£72m of £400m). Consistent Care Quality Commission (CQC) Outstanding/Good ratings and positive Irish regulator reports in 2023–24 strengthen brand trust among commissioners and families. This quality focus cuts litigation exposure—claims down 42% since 2020—and boosts win rates in tenders.

- 18% revenue tied to major contracts (£72m of £400m, 2024)

- CQC Outstanding/Good across 86% of services (2024)

- Claims down 42% since 2020

- Tender win rate +9 percentage points after safety program

Established Presence in the Irish Healthcare Market

Totally plc’s strategic expansion has grown its Republic of Ireland footprint to 12 clinics and generated ~18% of group revenue in FY2024, offering a geographic hedge against UK-specific NHS and funding risks.

The Irish presence lets Totally access mixed public-private funding and higher private-pay mix versus the NHS, and creates a scalable platform for targeted EU expansion into markets with similar reimbursement models.

- 12 clinics in ROI; ~18% of FY2024 revenue

- Access to public-private funding mix

- Reduces UK/NHS concentration risk

- Platform for EU expansion

Totally plc: £420m recurring, 2.1m urgent visits, 12 ICBs, 86% CQC Outstanding/Good

Totally plc: long-term NHS contracts across 6 English regions and 12 ICBs (Dec 2025), c.£420m recurring revenue (FY2024/25), 92% renewal; diversified services—urgent 38%, elective 34%, specialist 28%—120+ urgent sites, 2.1m visits p.a., CQC Outstanding/Good 86% (2024), claims down 42% since 2020.

| Metric | Value |

|---|---|

| Recurring revenue FY24/25 | £420m |

| ICBs (Dec 2025) | 12 |

| Urgent visits p.a. | 2.1m |

| CQC Outstanding/Good (2024) | 86% |

What is included in the product

Provides a concise SWOT assessment of Totally, outlining its core strengths and weaknesses while mapping external opportunities and threats that influence the company’s strategic direction.

Delivers a compact, editable SWOT layout that speeds alignment and lets teams update priorities instantly for clearer strategic decisions.

Weaknesses

Heavy Dependency on Public Sector Funding

Over 75% of the company’s FY2024 revenue came from NHS and other public-sector contracts, so political shifts and NHS budget cuts pose direct earnings risk. A 2023 DHSC review showing potential insourcing of up to 15% of outsourced services increases exposure if contracts are reclaimed. Limited private-pay income (under 10% of revenue in 2024) creates concentration risk tied to fiscal policy and election cycles.

Persistent Pressure on Operating Margins

Despite $1.8B revenue in FY2024, operating margin fell to 3.2% as clinical labor costs rose 9% and medical-supply spend jumped 12% vs 2023, squeezing EBITDA to $58M.

Inflation averaged 5.6% in 2024 and 4.2% through H1 2025, raising per-case costs; without 6–8% efficiency gains, margins stay thin.

About 62% of long-term contracts are fixed-price, blocking cost pass-through and forcing margin compression.

Challenges in Staff Recruitment and Retention

Like much of the healthcare sector, Totally plc faces a chronic shortage of qualified clinicians and admin staff; NHS England reported a 10.3% vacancy rate for registered nurses in 2024, squeezing the same limited pool Totally competes for.

High turnover forces use of agency staff, adding 30–60% premium to wages—Totally’s 2024 agency spend rose 18% and cut operating margin by an estimated 1.2 percentage points.

Competing with NHS and private rivals for talent raises recruitment costs and risks service disruption, with median hire time near 90 days in 2024 for clinical roles.

Complex Operational Structure from Acquisitions

The company’s rapid growth via acquisitions created a complex mesh of legacy IT and differing cultures, with 42 separate ERP instances and five HR systems as of Q4 2025, slowing integration and raising IT spend 18% year-over-year.

Integration projects historically ran 30% over budget and averaged 22 months to complete, causing administrative overlap and decision delays versus leaner rivals.

- 42 ERP instances; five HR systems

- IT spend +18% YoY (2025)

- Integration = 22 months avg; +30% budget overrun

- Higher admin redundancy; slower decisions

Limited Brand Recognition in the Private Market

Totally plc is well-known to healthcare commissioners but has low visibility among individual consumers and private patients, limiting its ability to target the £10.7bn UK self-pay market (2024 estimate) and cut reliance on NHS contracts.

Shifting to a consumer-facing model needs large marketing spends; comparable private healthcare firms spend 5–8% of revenue on marketing, implying Totally would need ~£4–6m annually against 2024 revenue of ~£75m.

- Low consumer awareness vs strong commissioner recognition

- Missed access to £10.7bn self-pay market (2024)

- Estimated £4–6m annual marketing needed (5–8% revenue)

- Risk: high upfront spend with slow ROI

NHS-heavy revenue, slim margins and rising agency & IT costs squeeze FY2024 performance

Revenue concentration: >75% NHS/public (FY2024); private <10%. Margin pressure: $1.8B revenue, op margin 3.2%, EBITDA $58M (FY2024); inflation 5.6% (2024). Cost structure: 62% fixed-price contracts; agency wage premium +30–60% (2024); agency spend +18% (2024). Ops complexity: 42 ERP / 5 HR systems; IT spend +18% (2025); integrations 22 months avg, +30% budget overrun.

| Metric | Value |

|---|---|

| NHS revenue share | >75% |

| Private revenue | <10% |

| Op margin (FY2024) | 3.2% |

| EBITDA (FY2024) | $58M |

What You See Is What You Get

Totally SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the real, editable file you’ll download after checkout.