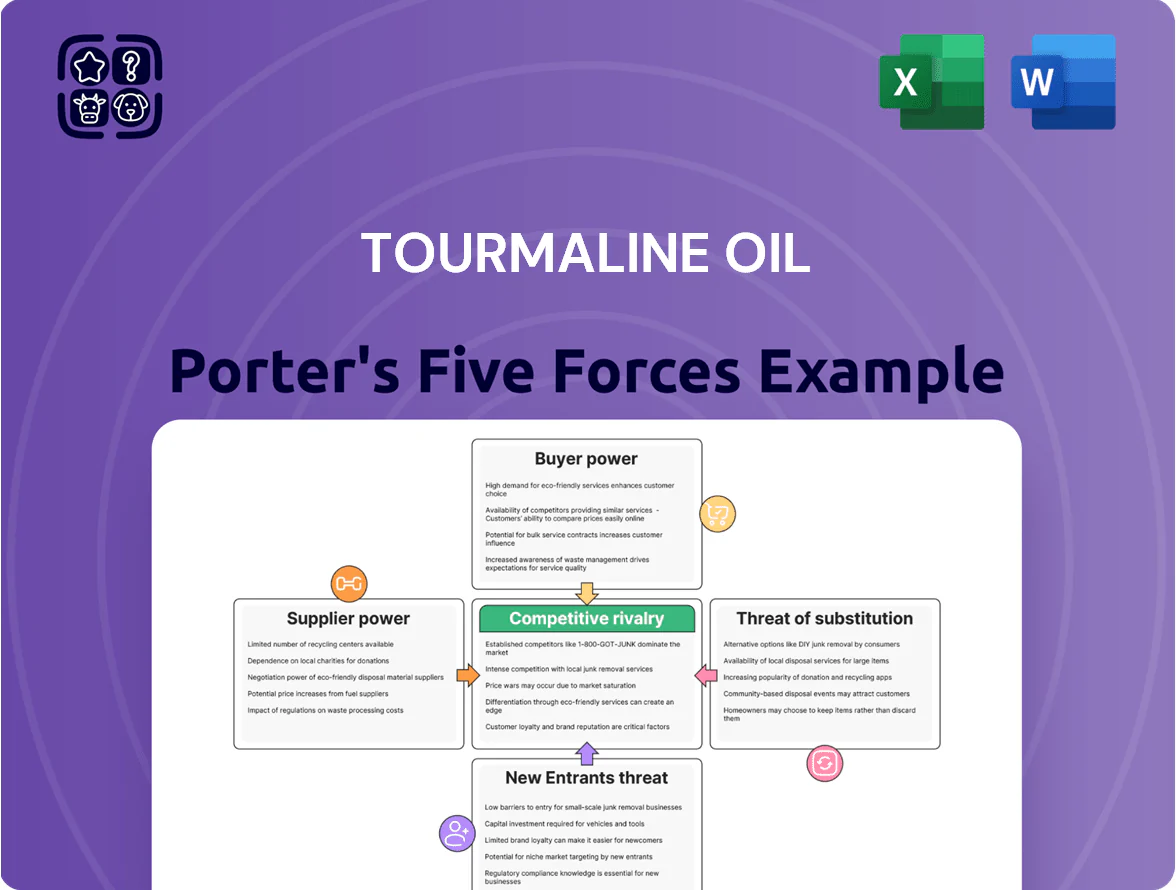

Tourmaline Oil Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Tourmaline Oil operates in a capital-intensive, low-margin upstream oil & gas sector where supplier leverage, regulatory shifts, and commodity-price volatility tightly shape profitability—our snapshot highlights key pressures and competitive levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tourmaline Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Oilfield Service Provider Concentration

The market for specialized drilling and hydraulic fracturing services in the Western Canadian Sedimentary Basin is concentrated among a few large firms (e.g., Precision Drilling, Ensign, Trican), giving suppliers moderate bargaining power because their rigs and completion crews are essential for Tourmaline’s output.

By late 2025, fleet tightness saw utilization above 85% and dayrates for high-spec rigs rose ~22% YoY, letting suppliers push higher rates or multi-year contracts that increase Tourmaline’s operating cost risk.

Specialized Labor Availability

The Canadian energy sector faces a tightening market for skilled technical labor—petroleum engineers and field operators—driving vacancy rates above 7% in Alberta in 2024 and wage growth near 6–8% year-over-year. This scarcity gives suppliers of labor strong bargaining leverage, forcing firms to raise wages, sign-on bonuses, and benefits; industry median total cash compensation rose to about CAD 140,000 for senior engineers in 2024. Tourmaline must absorb or offset these rising operational costs to keep its reported 2024 operating cost per boe near CAD 6.50 and preserve its low-cost producer status.

Midstream and Transportation Constraints

Suppliers of pipeline capacity and midstream processing wield strong leverage over Tourmaline because the company ships ~85% of its 2024 Canadian gas volumes via third-party pipelines; toll increases hit margins directly.

In Western Canada takeaway constraints—capacity utilization spiked to ~95% in 2023—let pipeline owners set allocations and tolls, forcing production curtailments or flare risks.

Higher tolls and limited midstream slots can raise per-Mcf transport costs by C$0.20–0.50, squeezing EBITDA per boe.

Regulatory and Emissions Technology Providers

- Fewer certified vendors → higher supplier leverage

- Mandatory 2026 methane targets → urgent purchases

- 2024 CCUS market ~$4.7B; ~12% CAGR → rising costs

- Compliance capex risk for Tourmaline: supplier-driven

Capital Equipment Lead Times

Tourmaline faces supplier leverage on long-lead capital items—turbines, compressors, steel tubulars—where 2024 industry data showed turbine lead times at 12–18 months and tubulars backorders up 20% vs 2022, letting suppliers set prices and schedules and raising capex per well by an estimated 8–12%.

Delays in critical machinery have paused projects and can compress Tourmaline’s growth runway, increasing financing needs and risking missed production targets.

- Typical turbine lead time: 12–18 months (2024)

- Steel tubular backorders: +20% vs 2022

- Estimated capex increase per well: 8–12%

- Project delay impact: higher financing, deferred production

Supply squeeze lifts costs: rigs +22%, vacancies >7%, capex per well +8–12%

Suppliers hold moderate-to-strong power: rig/completion firms pushed dayrates +22% YoY (late 2025, utilization >85%), skilled labor shortages lifted Alberta vacancy >7% (2024) and senior engineer cash comp ~CAD140,000, pipelines carried ~85% of 2024 volumes with takeaway at ~95% utilization (2023), and turbine lead times 12–18 months (2024) raising capex per well ~8–12%.

| Metric | Value |

|---|---|

| Rig dayrates change | +22% YoY (late 2025) |

| Fleet utilization | >85% (late 2025) |

| Alberta vacancy (tech) | >7% (2024) |

| Senior engineer cash | CAD140,000 (2024) |

| Pipeline share | ~85% of gas volumes (2024) |

| Takeaway utilization | ~95% (2023) |

| Turbine lead time | 12–18 months (2024) |

| Capex impact per well | +8–12% |

What is included in the product

Tailored Porter's Five Forces for Tourmaline Oil revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to defend market share and pricing power.

A concise Porter's Five Forces snapshot for Tourmaline Oil—clear ratings and driver notes to speed strategic decisions and investor briefings.

Customers Bargaining Power

Commodity Price Taker Status

Tourmaline mainly sells natural gas and crude oil, priced by benchmarks like AECO and NYMEX; in 2024 Canadian gas averaged ~C$2.25/GJ at AECO and Henry Hub averaged US$3.50/MMBtu, so Tourmaline is a commodity price taker.

Products are undifferentiated, so buyers switch on price alone, raising customer bargaining power and pressuring margins.

That dynamic forces Tourmaline to cut costs and boost efficiency; in 2024 its operating cost per BOE was roughly US$9–12 to stay profitable through price swings.

Concentration of Industrial End-Users

A large share of Tourmaline Oil’s 2024 natural gas sales flow to a handful of utilities and industrial buyers buying millions of MMBtu annually; in 2024 Tourmaline produced ~1.7 Bcf/day, so losing one large buyer (5–10% of volumes) would cut local revenue materially.

Access to Global LNG Markets

With Canadian LNG export capacity set to reach about 16–20 mtpa by late 2025, international buyers—mostly sovereign buyers and majors like Shell and TotalEnergies—wield strong bargaining power due to volume needs and credit strength.

Availability of Alternative Energy Sources

Customers in power generation can increasingly switch from natural gas to renewables plus batteries; global battery storage capacity grew 220% in 2024 to ~32 GW (BloombergNEF 2025), raising substitution risk for gas-fired demand.

Utilities gain leverage in long-term gas contracts as storage reduces intermittency; in 2024 US utility RFPs for renewables rose 18% vs 2023, pressuring gas price premia.

The energy transition caps fossil-fuel pricing: carbon-free procurement targets (over 60% of US utilities by 2030) and falling LCOE for solar (down 15% in 2024) limit Tourmaline’s pricing power.

- Battery storage: ~32 GW global (2024)

- US utility renewables RFPs +18% (2024)

- Solar LCOE -15% (2024)

- 60%+ US utilities with 2030 clean targets

Midstream Marketing and Trading Intermediaries

High buyer leverage: Tourmaline a price-taker amid low gas prices, LNG growth & storage gains

Customers hold high bargaining power: commodity pricing (AECO C$2.25/GJ, Henry Hub US$3.50/MMBtu in 2024) makes Tourmaline a price taker; buyers switch on price, utilities and majors buy large volumes (losing a 5–10% buyer hurts revenue); LNG export growth (16–20 mtpa by 2025) and 2024 storage/renewables gains (battery 32 GW) increase buyer leverage and substitution risk.

| Metric | 2024/2025 |

|---|---|

| AECO | C$2.25/GJ (2024) |

| Henry Hub | US$3.50/MMBtu (2024) |

| Tourmaline prod | ~2.4 Bcf/d (2024) |

| Battery storage | 32 GW (2024) |

| Canada LNG cap | 16–20 mtpa by late 2025 |

Preview Before You Purchase

Tourmaline Oil Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tourmaline Oil you’ll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file—ready for download and use the moment you buy.

What you see is the deliverable: the same comprehensive analysis content and structure available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Tourmaline Oil operates in a capital-intensive, low-margin upstream oil & gas sector where supplier leverage, regulatory shifts, and commodity-price volatility tightly shape profitability—our snapshot highlights key pressures and competitive levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tourmaline Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Oilfield Service Provider Concentration

The market for specialized drilling and hydraulic fracturing services in the Western Canadian Sedimentary Basin is concentrated among a few large firms (e.g., Precision Drilling, Ensign, Trican), giving suppliers moderate bargaining power because their rigs and completion crews are essential for Tourmaline’s output.

By late 2025, fleet tightness saw utilization above 85% and dayrates for high-spec rigs rose ~22% YoY, letting suppliers push higher rates or multi-year contracts that increase Tourmaline’s operating cost risk.

Specialized Labor Availability

The Canadian energy sector faces a tightening market for skilled technical labor—petroleum engineers and field operators—driving vacancy rates above 7% in Alberta in 2024 and wage growth near 6–8% year-over-year. This scarcity gives suppliers of labor strong bargaining leverage, forcing firms to raise wages, sign-on bonuses, and benefits; industry median total cash compensation rose to about CAD 140,000 for senior engineers in 2024. Tourmaline must absorb or offset these rising operational costs to keep its reported 2024 operating cost per boe near CAD 6.50 and preserve its low-cost producer status.

Midstream and Transportation Constraints

Suppliers of pipeline capacity and midstream processing wield strong leverage over Tourmaline because the company ships ~85% of its 2024 Canadian gas volumes via third-party pipelines; toll increases hit margins directly.

In Western Canada takeaway constraints—capacity utilization spiked to ~95% in 2023—let pipeline owners set allocations and tolls, forcing production curtailments or flare risks.

Higher tolls and limited midstream slots can raise per-Mcf transport costs by C$0.20–0.50, squeezing EBITDA per boe.

Regulatory and Emissions Technology Providers

- Fewer certified vendors → higher supplier leverage

- Mandatory 2026 methane targets → urgent purchases

- 2024 CCUS market ~$4.7B; ~12% CAGR → rising costs

- Compliance capex risk for Tourmaline: supplier-driven

Capital Equipment Lead Times

Tourmaline faces supplier leverage on long-lead capital items—turbines, compressors, steel tubulars—where 2024 industry data showed turbine lead times at 12–18 months and tubulars backorders up 20% vs 2022, letting suppliers set prices and schedules and raising capex per well by an estimated 8–12%.

Delays in critical machinery have paused projects and can compress Tourmaline’s growth runway, increasing financing needs and risking missed production targets.

- Typical turbine lead time: 12–18 months (2024)

- Steel tubular backorders: +20% vs 2022

- Estimated capex increase per well: 8–12%

- Project delay impact: higher financing, deferred production

Supply squeeze lifts costs: rigs +22%, vacancies >7%, capex per well +8–12%

Suppliers hold moderate-to-strong power: rig/completion firms pushed dayrates +22% YoY (late 2025, utilization >85%), skilled labor shortages lifted Alberta vacancy >7% (2024) and senior engineer cash comp ~CAD140,000, pipelines carried ~85% of 2024 volumes with takeaway at ~95% utilization (2023), and turbine lead times 12–18 months (2024) raising capex per well ~8–12%.

| Metric | Value |

|---|---|

| Rig dayrates change | +22% YoY (late 2025) |

| Fleet utilization | >85% (late 2025) |

| Alberta vacancy (tech) | >7% (2024) |

| Senior engineer cash | CAD140,000 (2024) |

| Pipeline share | ~85% of gas volumes (2024) |

| Takeaway utilization | ~95% (2023) |

| Turbine lead time | 12–18 months (2024) |

| Capex impact per well | +8–12% |

What is included in the product

Tailored Porter's Five Forces for Tourmaline Oil revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to defend market share and pricing power.

A concise Porter's Five Forces snapshot for Tourmaline Oil—clear ratings and driver notes to speed strategic decisions and investor briefings.

Customers Bargaining Power

Commodity Price Taker Status

Tourmaline mainly sells natural gas and crude oil, priced by benchmarks like AECO and NYMEX; in 2024 Canadian gas averaged ~C$2.25/GJ at AECO and Henry Hub averaged US$3.50/MMBtu, so Tourmaline is a commodity price taker.

Products are undifferentiated, so buyers switch on price alone, raising customer bargaining power and pressuring margins.

That dynamic forces Tourmaline to cut costs and boost efficiency; in 2024 its operating cost per BOE was roughly US$9–12 to stay profitable through price swings.

Concentration of Industrial End-Users

A large share of Tourmaline Oil’s 2024 natural gas sales flow to a handful of utilities and industrial buyers buying millions of MMBtu annually; in 2024 Tourmaline produced ~1.7 Bcf/day, so losing one large buyer (5–10% of volumes) would cut local revenue materially.

Access to Global LNG Markets

With Canadian LNG export capacity set to reach about 16–20 mtpa by late 2025, international buyers—mostly sovereign buyers and majors like Shell and TotalEnergies—wield strong bargaining power due to volume needs and credit strength.

Availability of Alternative Energy Sources

Customers in power generation can increasingly switch from natural gas to renewables plus batteries; global battery storage capacity grew 220% in 2024 to ~32 GW (BloombergNEF 2025), raising substitution risk for gas-fired demand.

Utilities gain leverage in long-term gas contracts as storage reduces intermittency; in 2024 US utility RFPs for renewables rose 18% vs 2023, pressuring gas price premia.

The energy transition caps fossil-fuel pricing: carbon-free procurement targets (over 60% of US utilities by 2030) and falling LCOE for solar (down 15% in 2024) limit Tourmaline’s pricing power.

- Battery storage: ~32 GW global (2024)

- US utility renewables RFPs +18% (2024)

- Solar LCOE -15% (2024)

- 60%+ US utilities with 2030 clean targets

Midstream Marketing and Trading Intermediaries

High buyer leverage: Tourmaline a price-taker amid low gas prices, LNG growth & storage gains

Customers hold high bargaining power: commodity pricing (AECO C$2.25/GJ, Henry Hub US$3.50/MMBtu in 2024) makes Tourmaline a price taker; buyers switch on price, utilities and majors buy large volumes (losing a 5–10% buyer hurts revenue); LNG export growth (16–20 mtpa by 2025) and 2024 storage/renewables gains (battery 32 GW) increase buyer leverage and substitution risk.

| Metric | 2024/2025 |

|---|---|

| AECO | C$2.25/GJ (2024) |

| Henry Hub | US$3.50/MMBtu (2024) |

| Tourmaline prod | ~2.4 Bcf/d (2024) |

| Battery storage | 32 GW (2024) |

| Canada LNG cap | 16–20 mtpa by late 2025 |

Preview Before You Purchase

Tourmaline Oil Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tourmaline Oil you’ll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file—ready for download and use the moment you buy.

What you see is the deliverable: the same comprehensive analysis content and structure available to you instantly after payment.