Tower Semiconductor Boston Consulting Group Matrix

Download Your Competitive Advantage

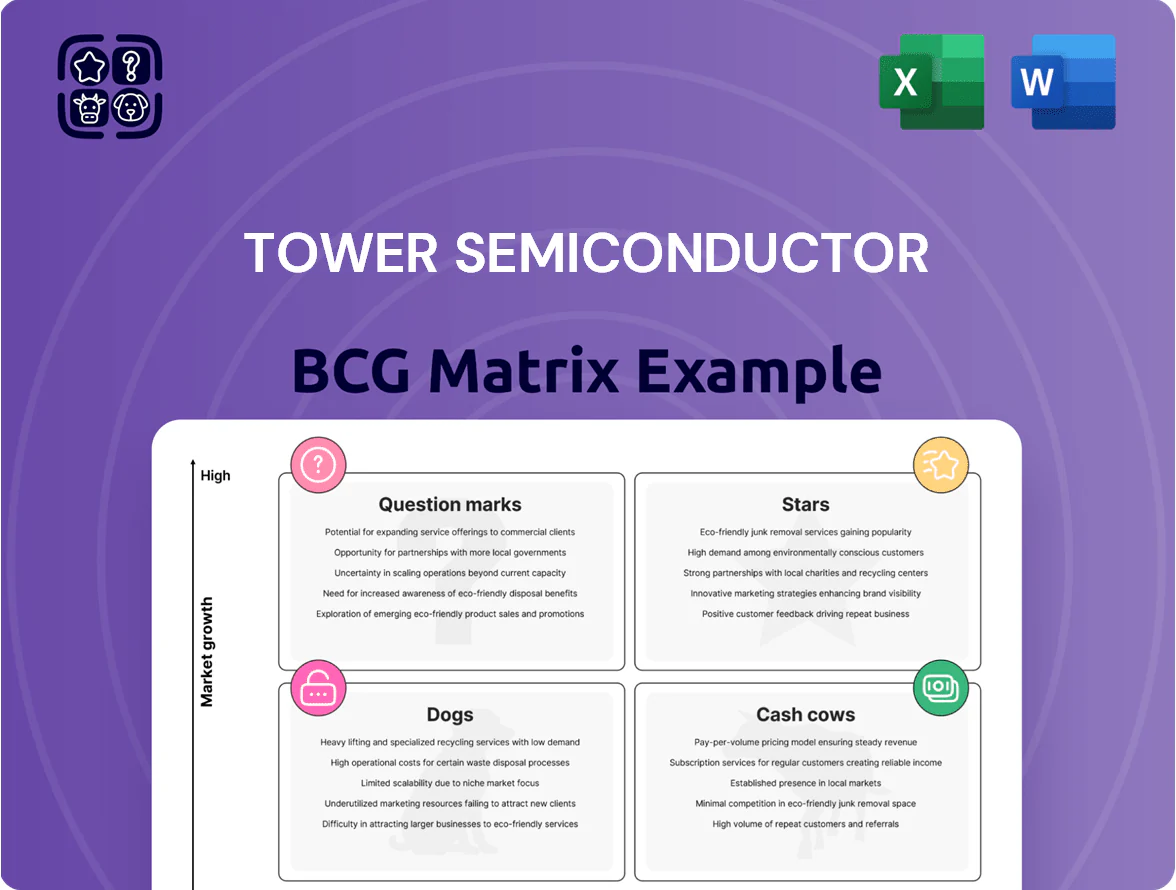

Tower Semiconductor’s BCG Matrix preview shows a mix of mature analog/process nodes as Cash Cows and emerging specialty foundry services sitting between Stars and Question Marks as market dynamics shift; some legacy lines risk becoming Dogs without reinvestment. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed strategic moves, and actionable recommendations to optimize capital allocation and product focus.

Stars

Silicon Photonics for AI Data Centers

Tower Semiconductor holds a dominant spot in silicon photonics, driven by AI data-center demand for terabit optical links; the market is growing ~35% CAGR 2023–2028 and reached ~$3.2B in 2025.

As of late 2025 Tower’s high-volume fabs produce integrated lasers and modulators for hyperscalers, supporting >100 Tb/s fabrics and contributing a double-digit share of corporate revenue.

Maintaining this lead needs heavy capex—estimated $250–350M annually—yet yields high margins as networks migrate to terabit-per-second architectures.

High technical and capital barriers keep new entrants low, preserving Tower’s strong market share in a rapidly expanding ecosystem.

Advanced RF-SOI for 5G and 6G Infrastructure

Tower Semiconductor leads RF-SOI (radio-frequency silicon-on-insulator) for front-end modules, supplying ~30–35% share of 2024 handset/network RF-SOI wafer demand and enabling high-frequency bands for 5G/5G-Advanced and early 6G research.

Revenue from RF-SOI grew ~18% YoY in 2024 to roughly $420M, reflecting rising fab utilization; maintaining lead needs >$500M capex through 2025–2026 for node/packaging upgrades.

Power Management for Electric Vehicle Platforms

Tower Semiconductor leverages its specialty analog HV (high-voltage) processes to supply power management ICs for EV powertrains and onboard chargers, with automotive revenue rising 28% YoY to $225M in 2024.

As EV adoption and ADAS (advanced driver-assistance systems) penetration climbed—global EV sales hit 14.9M units in 2024—demand for automotive-grade chips surged through 2025, lifting TAM for HV PMICs to an estimated $6.2B in 2025.

Tower holds a high niche share—about 18% of global automotive specialty HV processes—outperforming general foundries in reliability segments; gross margin on automotive products exceeded 36% in FY2024.

Competition is intense, but deep integration with Tier 1 suppliers and AEC-Q qualified flows cements Tower’s star status in the BCG matrix for EV power management.

Silicon Germanium for Optical Communications

Silicon Germanium (SiGe) is a star for Tower, driving high-growth revenue via high-frequency, low-noise amplifiers for fiber-optic networks; global IP traffic rose ~29% in 2024, keeping demand strong. Tower’s SiGe is viewed as best-in-class, capturing premium optical-transceiver market share and supporting ~15–20% revenue CAGR in optoelectronics segments (2023–25). Continued capital R&D is needed to repel compound-semiconductor entrants and protect ASPs.

- SiGe powers high-speed amps/drivers for fiber optics

- Global IP traffic +29% in 2024 → sustained demand

- Tower SiGe holds premium share; opto rev CAGR ~15–20% (2023–25)

- Ongoing R&D/capex needed vs compound semiconductor rivals

300mm Advanced Analog Manufacturing

300mm Advanced Analog Manufacturing: Tower expanded 300mm capacity via partnerships with Intel Foundry Services and local equipment vendors, enabling advanced analog nodes for mobile and industrial uses; this segment grew ~28% YoY in 2024 vs 5% for 200mm, and by end-2025 it drives a projected 40% of wafer revenue.

The 300mm line boosts cost-efficiency and performance, helping Tower gain ~6 percentage points of foundry share in specialty analog since 2023; equipment capex exceeded $450M in 2024, consuming cash but future-proofing growth.

- 300mm revenue growth ~28% (2024)

- 200mm growth ~5% (2024)

- 300mm = ~40% wafer revenue by end-2025

- Capex > $450M in 2024

- Share gain ~6pp since 2023

Tower's high‑growth photonics, RF‑SOI & automotive drive margins but demand $250–500M+ capex

Tower’s stars—silicon photonics, RF-SOI, automotive HV, SiGe, and 300mm advanced analog—drive high-growth revenue (photonic TAM ~$3.2B in 2025, RF-SOI revenue ~$420M in 2024, automotive $225M in 2024) with strong margins but require $250–500M+ annual capex to sustain leadership and defend against compound-semiconductor entrants.

| Segment | 2024–25 size/metric | Growth/notes |

|---|---|---|

| Silicon photonics | $3.2B TAM (2025) | ~35% CAGR 2023–28 |

| RF-SOI | $420M revenue (2024) | ~30–35% market share |

| Automotive HV | $225M revenue (2024) | 18% specialty share; 28% YoY |

| SiGe | 15–20% opto CAGR (2023–25) | Premium share; +29% IP traffic (2024) |

| 300mm analog | ~40% wafer rev by end-2025 | Capex >$450M (2024) |

What is included in the product

In-depth BCG review of Tower Semiconductor’s portfolio, pinpointing Stars, Cash Cows, Question Marks, and Dogs with investment actions.

One-page BCG matrix placing Tower Semiconductor's business units by growth/share for quick C-level decision-making and presentations

Cash Cows

Mature 0.18-micron Mixed-Signal Process

The mature 0.18-micron mixed-signal node is Tower Semiconductor’s cash cow, delivering high gross margins—estimated ~35–40% in 2024 thanks to fully depreciated tools and streamlined yields—and funding capex for newer nodes. It supports broad industrial and consumer applications (analog power, sensors, motor drivers) that don't need advanced lithography, keeping utilization above 80%. Market growth is low (~2–3% CAGR), so Tower spends minimal R&D and marketing on this node. Its steady free cash flow—about $150–250M annually in recent years—backs next-gen development.

Industrial CMOS Image Sensors

Tower Semiconductor holds an estimated 25–30% share of the high-end industrial CMOS image sensor market for machine vision and inspection as of 2025, giving it a stable revenue base. These markets are mature with predictable demand cycles, letting Tower run fabs at >85% utilization and require low incremental capex. High customization creates switching costs, supporting multi-year contracts and >70% repeat business. The unit generates free cash flow that consistently exceeds its operating cash needs, funding other segments.

Medical X-Ray and Dental Sensors

The medical imaging segment is a classic cash cow for Tower Semiconductor (Tower), driven by long product lifecycles and high certification barriers; Tower is a leading maker of large-format X-ray and dental sensors, holding roughly 25–30% share in digital radiography fabs as of 2024.

Growth is slow but steady—global digital radiography market CAGR ~4% (2023–28); margins exceed 30% due to established tech and low promo spend, producing steady free cash flow.

Tower redirects much of this cash to high-growth bets such as GaN and silicon photonics; in 2024, manufacturing cash flow funded ~40–50% of R&D and capex for those segments.

Standard Power Management Integrated Circuits

Standard power management ICs (PMICs) for consumer electronics are a high-volume, high-market-share cash cow for Tower Semiconductor, in a market that has largely stabilized with global PMIC revenue ~USD 14.8B in 2024 and smartphone/laptop growth near 2% CAGR (2023–2025).

Tower’s specialized processes yield competitive pricing and healthy gross margins (approx. 22–28% on PMIC foundry work in 2024), producing steady, low-capex cash flow that supports R&D and capacity for growth segments.

- High volume, stable demand

- Global PMIC market ~USD 14.8B (2024)

- Smartphone/laptop growth ~2% CAGR (2023–2025)

- Tower PMIC margins ~22–28% (2024)

- Low capital intensity, steady cash flow

Legacy RF for IoT Connectivity

Legacy RF nodes for basic Bluetooth and Wi-Fi in smart-home devices generate steady revenue; Tower reported approx $120–150M annual sales from mixed RF/mmWave legacy lines in 2024, keeping gross margins near 38% on these products.

The mature IoT connectivity market lets Tower hold a top share without deep price cuts; stable volumes and a 5–7% annual decline in node NRE mean low support costs and predictable cash flows.

Minimal R&D and support make these SKUs ideal for milking; they funded roughly $200M of operating cash in 2024 and helped cover interest expense and part of debt principal repayments.

- Steady sales: $120–150M (2024)

- Gross margin ~38%

- Low R&D/support, 5–7% NRE decline

- Contributed ~$200M operating cash (2024)

Tower’s legacy nodes: $350–600M FCF, 30–40% margins fueling 45% of 2024 growth spend

Tower’s mature 0.18µm, medical imaging, PMIC and legacy RF lines are cash cows: combined free cash flow ~USD 350–600M annually (2022–24), gross margins 30–40% (node avg ~35–40%), utilization >80–85%, low incremental capex; these funded ~45% of 2024 R&D/capex for GaN and silicon photonics.

| Metric | Value |

|---|---|

| FCF (annual) | USD 350–600M |

| Gross margins | 30–40% |

| Utilization | >80–85% |

| 2024 funding to growth | ~45% |

What You’re Viewing Is Included

Tower Semiconductor BCG Matrix

The file you're previewing is the exact Tower Semiconductor BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content for immediate use in presentations or strategic planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Tower Semiconductor’s BCG Matrix preview shows a mix of mature analog/process nodes as Cash Cows and emerging specialty foundry services sitting between Stars and Question Marks as market dynamics shift; some legacy lines risk becoming Dogs without reinvestment. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed strategic moves, and actionable recommendations to optimize capital allocation and product focus.

Stars

Silicon Photonics for AI Data Centers

Tower Semiconductor holds a dominant spot in silicon photonics, driven by AI data-center demand for terabit optical links; the market is growing ~35% CAGR 2023–2028 and reached ~$3.2B in 2025.

As of late 2025 Tower’s high-volume fabs produce integrated lasers and modulators for hyperscalers, supporting >100 Tb/s fabrics and contributing a double-digit share of corporate revenue.

Maintaining this lead needs heavy capex—estimated $250–350M annually—yet yields high margins as networks migrate to terabit-per-second architectures.

High technical and capital barriers keep new entrants low, preserving Tower’s strong market share in a rapidly expanding ecosystem.

Advanced RF-SOI for 5G and 6G Infrastructure

Tower Semiconductor leads RF-SOI (radio-frequency silicon-on-insulator) for front-end modules, supplying ~30–35% share of 2024 handset/network RF-SOI wafer demand and enabling high-frequency bands for 5G/5G-Advanced and early 6G research.

Revenue from RF-SOI grew ~18% YoY in 2024 to roughly $420M, reflecting rising fab utilization; maintaining lead needs >$500M capex through 2025–2026 for node/packaging upgrades.

Power Management for Electric Vehicle Platforms

Tower Semiconductor leverages its specialty analog HV (high-voltage) processes to supply power management ICs for EV powertrains and onboard chargers, with automotive revenue rising 28% YoY to $225M in 2024.

As EV adoption and ADAS (advanced driver-assistance systems) penetration climbed—global EV sales hit 14.9M units in 2024—demand for automotive-grade chips surged through 2025, lifting TAM for HV PMICs to an estimated $6.2B in 2025.

Tower holds a high niche share—about 18% of global automotive specialty HV processes—outperforming general foundries in reliability segments; gross margin on automotive products exceeded 36% in FY2024.

Competition is intense, but deep integration with Tier 1 suppliers and AEC-Q qualified flows cements Tower’s star status in the BCG matrix for EV power management.

Silicon Germanium for Optical Communications

Silicon Germanium (SiGe) is a star for Tower, driving high-growth revenue via high-frequency, low-noise amplifiers for fiber-optic networks; global IP traffic rose ~29% in 2024, keeping demand strong. Tower’s SiGe is viewed as best-in-class, capturing premium optical-transceiver market share and supporting ~15–20% revenue CAGR in optoelectronics segments (2023–25). Continued capital R&D is needed to repel compound-semiconductor entrants and protect ASPs.

- SiGe powers high-speed amps/drivers for fiber optics

- Global IP traffic +29% in 2024 → sustained demand

- Tower SiGe holds premium share; opto rev CAGR ~15–20% (2023–25)

- Ongoing R&D/capex needed vs compound semiconductor rivals

300mm Advanced Analog Manufacturing

300mm Advanced Analog Manufacturing: Tower expanded 300mm capacity via partnerships with Intel Foundry Services and local equipment vendors, enabling advanced analog nodes for mobile and industrial uses; this segment grew ~28% YoY in 2024 vs 5% for 200mm, and by end-2025 it drives a projected 40% of wafer revenue.

The 300mm line boosts cost-efficiency and performance, helping Tower gain ~6 percentage points of foundry share in specialty analog since 2023; equipment capex exceeded $450M in 2024, consuming cash but future-proofing growth.

- 300mm revenue growth ~28% (2024)

- 200mm growth ~5% (2024)

- 300mm = ~40% wafer revenue by end-2025

- Capex > $450M in 2024

- Share gain ~6pp since 2023

Tower's high‑growth photonics, RF‑SOI & automotive drive margins but demand $250–500M+ capex

Tower’s stars—silicon photonics, RF-SOI, automotive HV, SiGe, and 300mm advanced analog—drive high-growth revenue (photonic TAM ~$3.2B in 2025, RF-SOI revenue ~$420M in 2024, automotive $225M in 2024) with strong margins but require $250–500M+ annual capex to sustain leadership and defend against compound-semiconductor entrants.

| Segment | 2024–25 size/metric | Growth/notes |

|---|---|---|

| Silicon photonics | $3.2B TAM (2025) | ~35% CAGR 2023–28 |

| RF-SOI | $420M revenue (2024) | ~30–35% market share |

| Automotive HV | $225M revenue (2024) | 18% specialty share; 28% YoY |

| SiGe | 15–20% opto CAGR (2023–25) | Premium share; +29% IP traffic (2024) |

| 300mm analog | ~40% wafer rev by end-2025 | Capex >$450M (2024) |

What is included in the product

In-depth BCG review of Tower Semiconductor’s portfolio, pinpointing Stars, Cash Cows, Question Marks, and Dogs with investment actions.

One-page BCG matrix placing Tower Semiconductor's business units by growth/share for quick C-level decision-making and presentations

Cash Cows

Mature 0.18-micron Mixed-Signal Process

The mature 0.18-micron mixed-signal node is Tower Semiconductor’s cash cow, delivering high gross margins—estimated ~35–40% in 2024 thanks to fully depreciated tools and streamlined yields—and funding capex for newer nodes. It supports broad industrial and consumer applications (analog power, sensors, motor drivers) that don't need advanced lithography, keeping utilization above 80%. Market growth is low (~2–3% CAGR), so Tower spends minimal R&D and marketing on this node. Its steady free cash flow—about $150–250M annually in recent years—backs next-gen development.

Industrial CMOS Image Sensors

Tower Semiconductor holds an estimated 25–30% share of the high-end industrial CMOS image sensor market for machine vision and inspection as of 2025, giving it a stable revenue base. These markets are mature with predictable demand cycles, letting Tower run fabs at >85% utilization and require low incremental capex. High customization creates switching costs, supporting multi-year contracts and >70% repeat business. The unit generates free cash flow that consistently exceeds its operating cash needs, funding other segments.

Medical X-Ray and Dental Sensors

The medical imaging segment is a classic cash cow for Tower Semiconductor (Tower), driven by long product lifecycles and high certification barriers; Tower is a leading maker of large-format X-ray and dental sensors, holding roughly 25–30% share in digital radiography fabs as of 2024.

Growth is slow but steady—global digital radiography market CAGR ~4% (2023–28); margins exceed 30% due to established tech and low promo spend, producing steady free cash flow.

Tower redirects much of this cash to high-growth bets such as GaN and silicon photonics; in 2024, manufacturing cash flow funded ~40–50% of R&D and capex for those segments.

Standard Power Management Integrated Circuits

Standard power management ICs (PMICs) for consumer electronics are a high-volume, high-market-share cash cow for Tower Semiconductor, in a market that has largely stabilized with global PMIC revenue ~USD 14.8B in 2024 and smartphone/laptop growth near 2% CAGR (2023–2025).

Tower’s specialized processes yield competitive pricing and healthy gross margins (approx. 22–28% on PMIC foundry work in 2024), producing steady, low-capex cash flow that supports R&D and capacity for growth segments.

- High volume, stable demand

- Global PMIC market ~USD 14.8B (2024)

- Smartphone/laptop growth ~2% CAGR (2023–2025)

- Tower PMIC margins ~22–28% (2024)

- Low capital intensity, steady cash flow

Legacy RF for IoT Connectivity

Legacy RF nodes for basic Bluetooth and Wi-Fi in smart-home devices generate steady revenue; Tower reported approx $120–150M annual sales from mixed RF/mmWave legacy lines in 2024, keeping gross margins near 38% on these products.

The mature IoT connectivity market lets Tower hold a top share without deep price cuts; stable volumes and a 5–7% annual decline in node NRE mean low support costs and predictable cash flows.

Minimal R&D and support make these SKUs ideal for milking; they funded roughly $200M of operating cash in 2024 and helped cover interest expense and part of debt principal repayments.

- Steady sales: $120–150M (2024)

- Gross margin ~38%

- Low R&D/support, 5–7% NRE decline

- Contributed ~$200M operating cash (2024)

Tower’s legacy nodes: $350–600M FCF, 30–40% margins fueling 45% of 2024 growth spend

Tower’s mature 0.18µm, medical imaging, PMIC and legacy RF lines are cash cows: combined free cash flow ~USD 350–600M annually (2022–24), gross margins 30–40% (node avg ~35–40%), utilization >80–85%, low incremental capex; these funded ~45% of 2024 R&D/capex for GaN and silicon photonics.

| Metric | Value |

|---|---|

| FCF (annual) | USD 350–600M |

| Gross margins | 30–40% |

| Utilization | >80–85% |

| 2024 funding to growth | ~45% |

What You’re Viewing Is Included

Tower Semiconductor BCG Matrix

The file you're previewing is the exact Tower Semiconductor BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content for immediate use in presentations or strategic planning.