Towne Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

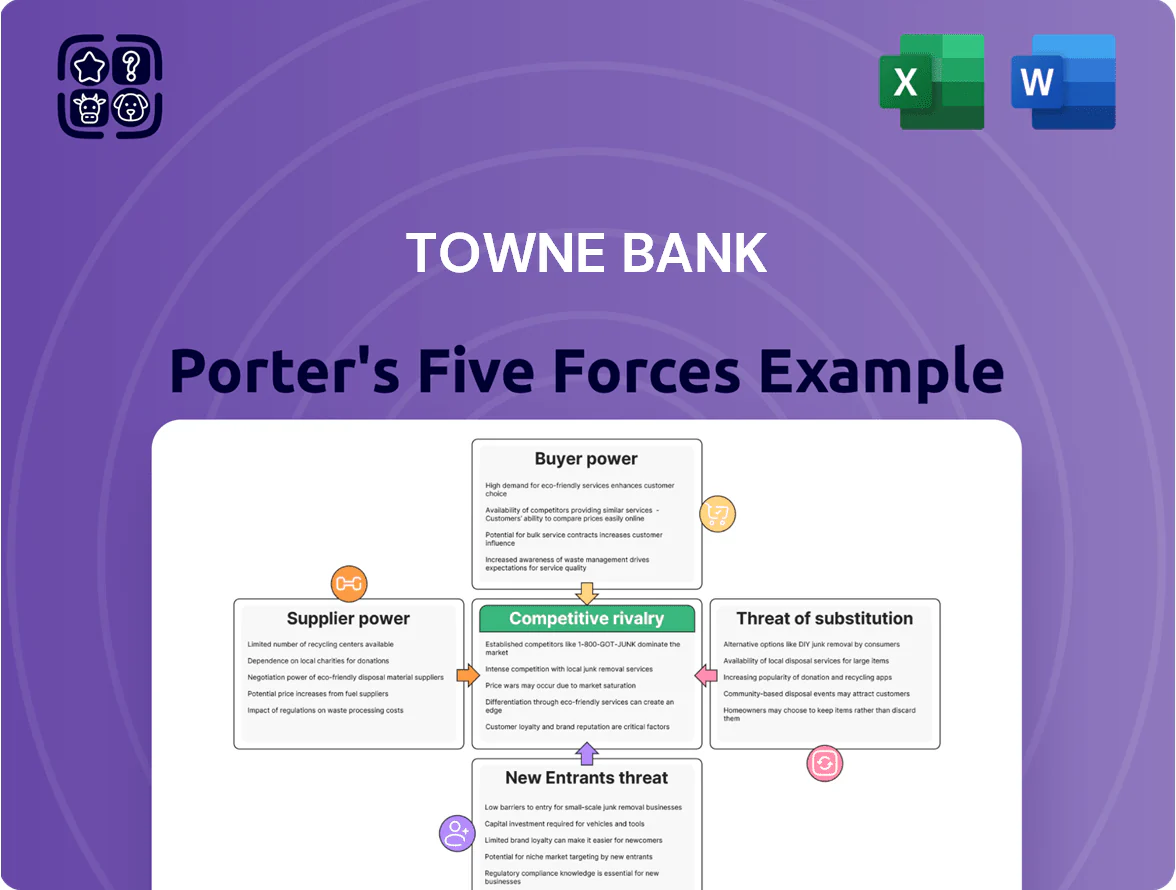

Towne Bank operates in a tightly regulated, relationship-driven regional banking market where competitive rivalry and buyer power shape margins, while digital disruption and potential new entrants pressure long-term growth; this snapshot highlights key tensions in pricing, deposit stability, and local market strength. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic implications for investment or planning decisions.

Suppliers Bargaining Power

Cost of Financial Capital

Technology and Fintech Vendors

TowneBank depends on third-party core-banking, cybersecurity, and digital-platform vendors, giving those firms high supplier power since replacing systems costs tens of millions and can take 6–18 months of integration work. In 2024, 62% of community banks reported vendor concentration as their top tech risk, so vendor leverage is real for TowneBank. Losing access or facing price hikes would hit digital adoption and could raise IT spend above the industry median of 1.8% of assets.

Regulatory and Compliance Costs

Regulatory bodies function as suppliers by controlling licenses and legal frameworks; in 2025 TowneBank spent an estimated $42m on compliance, up 18% year-over-year, for legal, audit, and AML (anti-money laundering) programs. Compliance rules tightened post-2023, raising fixed costs and increasing supplier power because regulators can revoke charters or levy fines—FDIC and OCC penalties topped $1.2bn industry-wide in 2024, so non-compliance risk is existential.

Human Capital and Specialized Talent

The supply of skilled labor in commercial lending, wealth management, and cybersecurity is tight in the Mid-Atlantic, raising TowneBank employees’ bargaining power on pay and benefits; Bureau of Labor Statistics data (2024) shows financial services employment growth of 2.1% in VA/NC regions, tightening markets.

Competition from larger banks and fintechs pushes base salary and bonus offers up—industry surveys in 2024 reported 8–12% higher median pay for experienced relationship managers locally.

High turnover in key relationship roles reduces client retention and fee income; a 2023 industry study links each senior RM departure to a 6–10% average client attrition within 12 months.

- Skilled-labor shortage raises wage costs

- Mid-Atlantic competition drives 8–12% pay premium

- RM turnover → 6–10% client attrition

- Cybersecurity talent scarcity increases hiring time and contract spend

Physical Infrastructure and Real Estate

TowneBank still prioritizes a physical branch network for private and commercial banking despite digital growth, making it exposed to landlords in prime Virginia and North Carolina markets where lease leverage is moderate.

Rising commercial rents in Hampton Roads, Richmond, Raleigh-Durham (average annual rent growth ~5–7% in 2024) heighten cost pressure; TowneBank’s local-presence strategy increases sensitivity to CRE (commercial real estate) inflation and limited prime storefront availability.

- Branch-heavy model raises CRE cost exposure

- Landlords hold moderate lease negotiation power

- 2024 rent growth ~5–7% in key markets

TowneBank under supplier squeeze: costly deposits, funding, compliance and wages

| Metric | 2024–2025 |

|---|---|

| Deposits | $11.8B (9/30/2025) |

| Wholesale funding cost | +175bps vs swaps (2025) |

| Compliance spend | $42M (2025) |

| Pay premium | 8–12% (2024) |

What is included in the product

Provides a Towne Bank–specific Porter’s Five Forces overview that uncovers competitive pressures, customer and supplier influence, entry barriers, substitutes, and emerging threats to inform strategic and investor decisions.

One-sheet Porter's Five Forces for Towne Bank—quickly spot competitive pressures and concentration risks to guide lending, expansion, or MSA strategy.

Customers Bargaining Power

Low Switching Costs for Retail Clients

Individual retail clients face low switching costs for checking and savings; as of 2025 an estimated 40% of US consumers use at least one digital-only bank, and instant ACH and RTP rails make transfers near-instant and free. This trend raises customer churn risk for TowneBank, so the bank must double down on service quality, local-branch relationships, and community branding to retain deposits and fee income.

Price Sensitivity in Mortgage and Loan Products

Borrowers show high price sensitivity: a 0.25% rate gap can shift mortgage demand by ~7% nationally (FHFA 2024), and 62% of borrowers used online rate comparison tools in 2024 (J.D. Power). That visibility compresses margins for mortgage and CRE loans, forcing TowneBank to match or undercut national lenders; in 2024 TowneBank's average 30-year fixed mortgage rate tracked within 10–15 basis points of major banks to retain volume.

Sophistication of Commercial Clients

TowneBank serves middle-market firms and professionals with high financial literacy who commonly hold multiple banking relationships; in 2025 roughly 60% of US middle-market firms used three or more banking partners, increasing negotiation leverage. These clients negotiate lower spreads on credit—often 25–75 basis points below standard pricing—and demand fee waivers on treasury services, pressuring margins. Large accounts can move deposits quickly: top 100 commercial clients often represent 20–35% of regional bank commercial deposits, so TowneBank faces substantial bargaining power.

Access to Information and Transparency

Customers use real-time financial data and peer reviews to compare Towne Bank’s fees and wealth-performance with benchmarks; a 2024 J.D. Power study found 47% of retail investors rely on online reviews when choosing advisors, raising scrutiny on opaque pricing.

Transparent fee tools and performance trackers mean customers can spot hidden charges or lagging returns; Morningstar data shows 66% of investors check benchmark-relative returns before investing, constraining Towne’s pricing and strategy choices.

Demands for Integrated Digital Experiences

Modern Towne Bank customers expect seamless integration across mobile apps, web portals, and branch services; 73% of US bank users (2024) say a poor mobile app would make them switch providers.

If Towne’s digital UX lags fintech features like instant P2P, account aggregation, or API access, churn risk rises—industry attrition linked to poor digital service averaged 12% annually in 2023.

That forces Towne to fund ongoing digital innovation—adding real-time payments, biometrics, and analytics—while keeping retail fees unchanged to meet expectations and remain competitive.

- 73% of users cite app quality for switching (2024)

- 12% average churn tied to weak digital services (2023)

- Need: real-time payments, biometrics, APIs at no extra cost

Customers Hold the Levers: Low Switching Costs, High Transparency Drive Rate Wars

Customers have strong bargaining power: low switching costs (40% use digital-only banks in 2025), high price transparency (62% used rate tools, J.D. Power 2024), and concentrated commercial deposits (top 100 clients = 20–35% of regional deposits), forcing TowneBank to match rates, waive fees, and invest in digital UX to avoid ~12% attrition tied to poor digital service (2023).

| Metric | Value |

|---|---|

| Digital-only usage (2025) | 40% |

| Rate comparison users (2024) | 62% |

| Top-100 deposit share | 20–35% |

| Attrition from poor digital UX (2023) | 12% |

Same Document Delivered

Towne Bank Porter's Five Forces Analysis

This preview displays the exact Towne Bank Porter's Five Forces analysis you will receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Towne Bank operates in a tightly regulated, relationship-driven regional banking market where competitive rivalry and buyer power shape margins, while digital disruption and potential new entrants pressure long-term growth; this snapshot highlights key tensions in pricing, deposit stability, and local market strength. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic implications for investment or planning decisions.

Suppliers Bargaining Power

Cost of Financial Capital

Technology and Fintech Vendors

TowneBank depends on third-party core-banking, cybersecurity, and digital-platform vendors, giving those firms high supplier power since replacing systems costs tens of millions and can take 6–18 months of integration work. In 2024, 62% of community banks reported vendor concentration as their top tech risk, so vendor leverage is real for TowneBank. Losing access or facing price hikes would hit digital adoption and could raise IT spend above the industry median of 1.8% of assets.

Regulatory and Compliance Costs

Regulatory bodies function as suppliers by controlling licenses and legal frameworks; in 2025 TowneBank spent an estimated $42m on compliance, up 18% year-over-year, for legal, audit, and AML (anti-money laundering) programs. Compliance rules tightened post-2023, raising fixed costs and increasing supplier power because regulators can revoke charters or levy fines—FDIC and OCC penalties topped $1.2bn industry-wide in 2024, so non-compliance risk is existential.

Human Capital and Specialized Talent

The supply of skilled labor in commercial lending, wealth management, and cybersecurity is tight in the Mid-Atlantic, raising TowneBank employees’ bargaining power on pay and benefits; Bureau of Labor Statistics data (2024) shows financial services employment growth of 2.1% in VA/NC regions, tightening markets.

Competition from larger banks and fintechs pushes base salary and bonus offers up—industry surveys in 2024 reported 8–12% higher median pay for experienced relationship managers locally.

High turnover in key relationship roles reduces client retention and fee income; a 2023 industry study links each senior RM departure to a 6–10% average client attrition within 12 months.

- Skilled-labor shortage raises wage costs

- Mid-Atlantic competition drives 8–12% pay premium

- RM turnover → 6–10% client attrition

- Cybersecurity talent scarcity increases hiring time and contract spend

Physical Infrastructure and Real Estate

TowneBank still prioritizes a physical branch network for private and commercial banking despite digital growth, making it exposed to landlords in prime Virginia and North Carolina markets where lease leverage is moderate.

Rising commercial rents in Hampton Roads, Richmond, Raleigh-Durham (average annual rent growth ~5–7% in 2024) heighten cost pressure; TowneBank’s local-presence strategy increases sensitivity to CRE (commercial real estate) inflation and limited prime storefront availability.

- Branch-heavy model raises CRE cost exposure

- Landlords hold moderate lease negotiation power

- 2024 rent growth ~5–7% in key markets

TowneBank under supplier squeeze: costly deposits, funding, compliance and wages

| Metric | 2024–2025 |

|---|---|

| Deposits | $11.8B (9/30/2025) |

| Wholesale funding cost | +175bps vs swaps (2025) |

| Compliance spend | $42M (2025) |

| Pay premium | 8–12% (2024) |

What is included in the product

Provides a Towne Bank–specific Porter’s Five Forces overview that uncovers competitive pressures, customer and supplier influence, entry barriers, substitutes, and emerging threats to inform strategic and investor decisions.

One-sheet Porter's Five Forces for Towne Bank—quickly spot competitive pressures and concentration risks to guide lending, expansion, or MSA strategy.

Customers Bargaining Power

Low Switching Costs for Retail Clients

Individual retail clients face low switching costs for checking and savings; as of 2025 an estimated 40% of US consumers use at least one digital-only bank, and instant ACH and RTP rails make transfers near-instant and free. This trend raises customer churn risk for TowneBank, so the bank must double down on service quality, local-branch relationships, and community branding to retain deposits and fee income.

Price Sensitivity in Mortgage and Loan Products

Borrowers show high price sensitivity: a 0.25% rate gap can shift mortgage demand by ~7% nationally (FHFA 2024), and 62% of borrowers used online rate comparison tools in 2024 (J.D. Power). That visibility compresses margins for mortgage and CRE loans, forcing TowneBank to match or undercut national lenders; in 2024 TowneBank's average 30-year fixed mortgage rate tracked within 10–15 basis points of major banks to retain volume.

Sophistication of Commercial Clients

TowneBank serves middle-market firms and professionals with high financial literacy who commonly hold multiple banking relationships; in 2025 roughly 60% of US middle-market firms used three or more banking partners, increasing negotiation leverage. These clients negotiate lower spreads on credit—often 25–75 basis points below standard pricing—and demand fee waivers on treasury services, pressuring margins. Large accounts can move deposits quickly: top 100 commercial clients often represent 20–35% of regional bank commercial deposits, so TowneBank faces substantial bargaining power.

Access to Information and Transparency

Customers use real-time financial data and peer reviews to compare Towne Bank’s fees and wealth-performance with benchmarks; a 2024 J.D. Power study found 47% of retail investors rely on online reviews when choosing advisors, raising scrutiny on opaque pricing.

Transparent fee tools and performance trackers mean customers can spot hidden charges or lagging returns; Morningstar data shows 66% of investors check benchmark-relative returns before investing, constraining Towne’s pricing and strategy choices.

Demands for Integrated Digital Experiences

Modern Towne Bank customers expect seamless integration across mobile apps, web portals, and branch services; 73% of US bank users (2024) say a poor mobile app would make them switch providers.

If Towne’s digital UX lags fintech features like instant P2P, account aggregation, or API access, churn risk rises—industry attrition linked to poor digital service averaged 12% annually in 2023.

That forces Towne to fund ongoing digital innovation—adding real-time payments, biometrics, and analytics—while keeping retail fees unchanged to meet expectations and remain competitive.

- 73% of users cite app quality for switching (2024)

- 12% average churn tied to weak digital services (2023)

- Need: real-time payments, biometrics, APIs at no extra cost

Customers Hold the Levers: Low Switching Costs, High Transparency Drive Rate Wars

Customers have strong bargaining power: low switching costs (40% use digital-only banks in 2025), high price transparency (62% used rate tools, J.D. Power 2024), and concentrated commercial deposits (top 100 clients = 20–35% of regional deposits), forcing TowneBank to match rates, waive fees, and invest in digital UX to avoid ~12% attrition tied to poor digital service (2023).

| Metric | Value |

|---|---|

| Digital-only usage (2025) | 40% |

| Rate comparison users (2024) | 62% |

| Top-100 deposit share | 20–35% |

| Attrition from poor digital UX (2023) | 12% |

Same Document Delivered

Towne Bank Porter's Five Forces Analysis

This preview displays the exact Towne Bank Porter's Five Forces analysis you will receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.