Towne Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Towne Bank faces shifting regulatory scrutiny, regional economic cycles, and accelerating fintech competition—our PESTLE snapshot highlights the strategic risks and opportunities these forces create for growth and resilience. Purchase the full PESTLE analysis to access detailed, actionable insights and editable charts that will sharpen your investment thesis or strategic plan.

Political factors

Federal Regulatory Oversight Transitions

The 2024–25 federal administration transitions and new CFPB and FDIC leadership have prompted tightened focus on capital adequacy and fee transparency; FDIC’s 2024 insured deposits rose 3.6% year-over-year while CFPB enforcement actions totaled $2.1B in 2024, forcing regional banks to recalibrate.

Regional Infrastructure Policy Influence

Political initiatives boosting Mid-Atlantic infrastructure create sizeable commercial lending opportunities for Towne Bank; Virginia and North Carolina committed over $7.8 billion combined in 2024–2025 for transportation and energy hub projects, driving demand for industrial and construction financing. Towne leverages local political relationships to secure roles in public-private partnerships, targeting a 10–15% growth in project loan originations in these states.

Tax Policy and Corporate Strategy

Legislative debates over corporate tax rates and enhanced small business credits shape investment choices for TowneBank’s commercial clients, with 2024 SBA data showing small businesses received $74.8B in federal assistance influencing lending demand.

By late 2025 proposed capital gains reforms—projected to affect 10–15% of high-net-worth portfolios—have spiked wealth management inquiries by ~22% year-over-year.

TowneBank’s private banking arm expanded advisory teams 18% in 2024 to support clients navigating shifting fiscal policy and tax planning.

Defense Spending and Local Economy

The bank’s heavy presence in Hampton Roads ties loan demand and credit quality to federal defense spending; the region hosts ~90% of Navy shipbuilding jobs in Virginia and Portsmouth-area naval contracts totaled about $12.3bn in 2024, directly supporting household incomes and small-business revenues.

Political shifts in congressional defense appropriations and Navy shipbuilding plans (e.g., FY2025 shipbuilding request of ~$28bn) materially affect regional employment and commercial real estate performance, so monitoring defense committees informs provisioning and risk pricing.

- Hampton Roads exposure: ~90% regional Navy shipbuilding jobs

- Portsmouth-area defense contracts: ~$12.3bn (2024)

- FY2025 Navy shipbuilding request: ~$28bn — impacts loan demand

State Level Banking Legislation

Legislative activity in the 2024–25 Virginia and North Carolina sessions tightened rules on predatory lending and clarified bank-fintech partnership oversight, affecting market entry; Virginia passed a 2024 bill expanding consumer protections, while NC proposed similar limits increasing compliance costs by an estimated 5–8% for small banks.

TowneBank lobbies through state banking associations to defend relationship-banking, citing $8.7B in 2024 assets and concern that stricter fintech rules shift competitive balance toward regulated incumbents.

- 2024–25 state bills tighten predatory lending rules

- Estimated 5–8% compliance cost rise for small banks

- TowneBank: $8.7B assets (2024) and active advocacy

Regulatory Costs Rise While Defense, Infrastructure and Private Banking Fuel Loan Growth

Federal regulatory tightening (CFPB $2.1B enforcement in 2024; FDIC insured deposits +3.6% YoY) and 2024–25 state laws raising compliance costs (~5–8%) increase operational burdens; regional defense spending (Portsmouth $12.3B contracts; FY2025 shipbuilding ~$28B) sustains loan demand; VA/NC infrastructure commitments ~$7.8B drive commercial lending; TowneBank assets $8.7B (2024), private banking growth +18% (2024).

| Indicator | Value |

|---|---|

| CFPB 2024 enforcement | $2.1B |

| FDIC insured deposits YoY | +3.6% |

| Portsmouth defense contracts (2024) | $12.3B |

| FY2025 Navy shipbuilding request | $28B |

| VA/NC infrastructure (2024–25) | $7.8B |

| TowneBank assets (2024) | $8.7B |

| Private banking headcount growth (2024) | +18% |

What is included in the product

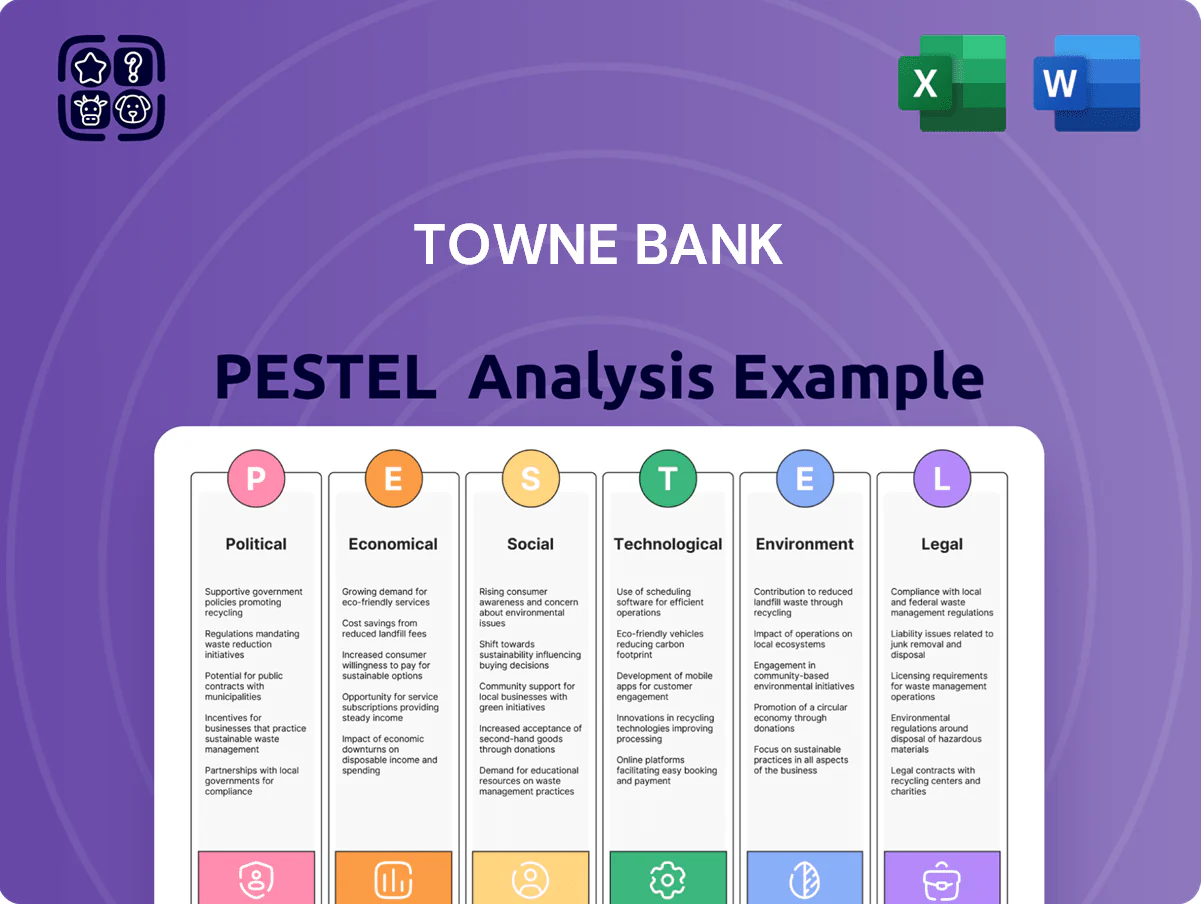

Explores how external macro-environmental factors uniquely affect Towne Bank across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current regional data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise Towne Bank PESTLE summary that’s visually segmented for quick meetings, easily dropped into slides, and editable for regional or business-line notes to streamline external risk discussions and team alignment.

Economic factors

Interest Rate Stabilization and Margin Management

Following Fed stabilization of the policy rate in 2025, Towne Bank benefits from clearer net interest margin planning as the 10-year Treasury hovered near 4.3% in Q1 2025; the bank is actively repricing loans while offsetting deposit cost rises—insured deposit beta rose to ~45% in 2024—aiming to preserve historical NIM around 3.2% through disciplined balance-sheet management and capital allocation to protect long-term shareholder value.

Real Estate Market Resilience

Mid-Atlantic real estate remains a regional economic pillar despite high valuations and sub-4% vacancy in core markets; TowneBank’s loan book exposure to commercial and residential property necessitates rigorous stress testing as cycles mature toward late 2025, with CRE concentration limits reviewed against estimated regional cap rates shifting ~50–150bps in 2024–25; sustained demand for multi-family and industrial space (rent growth ~3–6% in 2024) cushions office sector weakness.

Inflationary Impacts on Operational Costs

Persistent inflationary pressures raised Towne Bank’s non-interest expenses in 2025, with wage growth near 5.2% and technology/service costs up about 7.8% year-over-year, contributing to a higher operating expense base.

To offset this, the bank launched efficiency initiatives and automation pilots targeting a 10–15% reduction in back-office FTE hours and expects $12–18 million in annualized savings if fully scaled.

Maintaining a favorable efficiency ratio—recently reported around 58%—is critical for Towne to compete with national banks whose median efficiency ratios are closer to 50% due to larger scale.

Labor Market Dynamics in Service Areas

The bank tracks local unemployment and wage growth as leading indicators; 2024 wage growth of 4.1% regionally correlated with 2.8% consumer loan growth and 1.6% deposit growth in its markets.

- Unemployment: VA 3.3%, NC 3.6% (Dec 2025)

- Regional wage growth 2024: ~4.1%

- Tech wage increase 2024: ~6.2% y/y

- Observed: consumer loans +2.8%, deposits +1.6%

Small Business Economic Sentiment

The economic health of small and medium enterprises (SMEs) remains a primary driver of TowneBank’s commercial lending, with 2024 SBA-backed lending up ~12% year-over-year and regional small business loan demand rising 9% through Q3 2025.

Entrepreneurial activity in the Mid-Atlantic is robust—small business formation grew 6% in 2024—yet concerns about global supply-chain disruptions and a 2024–25 average U.S. industrial energy price increase of ~8% temper sentiment.

TowneBank augments lending with consultative cash-flow services and working-capital solutions; client advisory engagements increased 18% in 2024 as firms sought guidance navigating 2025’s rate and cost pressures.

- SME lending growth: +12% (2024 SBA-backed)

- Regional loan demand: +9% (through Q3 2025)

- New business formation: +6% (Mid-Atlantic, 2024)

- Industrial energy costs: +8% avg (2024–25)

- Advisory engagements: +18% (2024)

Towne Bank eyes ~3.2% NIM as Fed pause, 4.3% 10y and 45% deposit beta pressure margins

Towne Bank’s NIM guidance stabilizes as Fed pauses in 2025 and 10y Treasury ~4.3% (Q1 2025); deposit beta ~45% (2024) pressures margins while repricing and cost savings target preserving ~3.2% NIM. Regional CRE and multi-family demand (rent growth 3–6% in 2024) mitigate office weakness; SME lending +12% (2024 SBA), advisory engagements +18% (2024) support fee income.

| Metric | Value |

|---|---|

| 10y Treasury (Q1 2025) | 4.3% |

| Deposit beta (2024) | ~45% |

| Target NIM | ~3.2% |

| Regional rent growth (2024) | 3–6% |

| SME lending (2024) | +12% |

| Advisory engagements (2024) | +18% |

Preview Before You Purchase

Towne Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the Towne Bank PESTLE Analysis includes comprehensive political, economic, social, technological, legal, and environmental insights presented in the same structure and detail as the sample.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Towne Bank faces shifting regulatory scrutiny, regional economic cycles, and accelerating fintech competition—our PESTLE snapshot highlights the strategic risks and opportunities these forces create for growth and resilience. Purchase the full PESTLE analysis to access detailed, actionable insights and editable charts that will sharpen your investment thesis or strategic plan.

Political factors

Federal Regulatory Oversight Transitions

The 2024–25 federal administration transitions and new CFPB and FDIC leadership have prompted tightened focus on capital adequacy and fee transparency; FDIC’s 2024 insured deposits rose 3.6% year-over-year while CFPB enforcement actions totaled $2.1B in 2024, forcing regional banks to recalibrate.

Regional Infrastructure Policy Influence

Political initiatives boosting Mid-Atlantic infrastructure create sizeable commercial lending opportunities for Towne Bank; Virginia and North Carolina committed over $7.8 billion combined in 2024–2025 for transportation and energy hub projects, driving demand for industrial and construction financing. Towne leverages local political relationships to secure roles in public-private partnerships, targeting a 10–15% growth in project loan originations in these states.

Tax Policy and Corporate Strategy

Legislative debates over corporate tax rates and enhanced small business credits shape investment choices for TowneBank’s commercial clients, with 2024 SBA data showing small businesses received $74.8B in federal assistance influencing lending demand.

By late 2025 proposed capital gains reforms—projected to affect 10–15% of high-net-worth portfolios—have spiked wealth management inquiries by ~22% year-over-year.

TowneBank’s private banking arm expanded advisory teams 18% in 2024 to support clients navigating shifting fiscal policy and tax planning.

Defense Spending and Local Economy

The bank’s heavy presence in Hampton Roads ties loan demand and credit quality to federal defense spending; the region hosts ~90% of Navy shipbuilding jobs in Virginia and Portsmouth-area naval contracts totaled about $12.3bn in 2024, directly supporting household incomes and small-business revenues.

Political shifts in congressional defense appropriations and Navy shipbuilding plans (e.g., FY2025 shipbuilding request of ~$28bn) materially affect regional employment and commercial real estate performance, so monitoring defense committees informs provisioning and risk pricing.

- Hampton Roads exposure: ~90% regional Navy shipbuilding jobs

- Portsmouth-area defense contracts: ~$12.3bn (2024)

- FY2025 Navy shipbuilding request: ~$28bn — impacts loan demand

State Level Banking Legislation

Legislative activity in the 2024–25 Virginia and North Carolina sessions tightened rules on predatory lending and clarified bank-fintech partnership oversight, affecting market entry; Virginia passed a 2024 bill expanding consumer protections, while NC proposed similar limits increasing compliance costs by an estimated 5–8% for small banks.

TowneBank lobbies through state banking associations to defend relationship-banking, citing $8.7B in 2024 assets and concern that stricter fintech rules shift competitive balance toward regulated incumbents.

- 2024–25 state bills tighten predatory lending rules

- Estimated 5–8% compliance cost rise for small banks

- TowneBank: $8.7B assets (2024) and active advocacy

Regulatory Costs Rise While Defense, Infrastructure and Private Banking Fuel Loan Growth

Federal regulatory tightening (CFPB $2.1B enforcement in 2024; FDIC insured deposits +3.6% YoY) and 2024–25 state laws raising compliance costs (~5–8%) increase operational burdens; regional defense spending (Portsmouth $12.3B contracts; FY2025 shipbuilding ~$28B) sustains loan demand; VA/NC infrastructure commitments ~$7.8B drive commercial lending; TowneBank assets $8.7B (2024), private banking growth +18% (2024).

| Indicator | Value |

|---|---|

| CFPB 2024 enforcement | $2.1B |

| FDIC insured deposits YoY | +3.6% |

| Portsmouth defense contracts (2024) | $12.3B |

| FY2025 Navy shipbuilding request | $28B |

| VA/NC infrastructure (2024–25) | $7.8B |

| TowneBank assets (2024) | $8.7B |

| Private banking headcount growth (2024) | +18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Towne Bank across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current regional data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise Towne Bank PESTLE summary that’s visually segmented for quick meetings, easily dropped into slides, and editable for regional or business-line notes to streamline external risk discussions and team alignment.

Economic factors

Interest Rate Stabilization and Margin Management

Following Fed stabilization of the policy rate in 2025, Towne Bank benefits from clearer net interest margin planning as the 10-year Treasury hovered near 4.3% in Q1 2025; the bank is actively repricing loans while offsetting deposit cost rises—insured deposit beta rose to ~45% in 2024—aiming to preserve historical NIM around 3.2% through disciplined balance-sheet management and capital allocation to protect long-term shareholder value.

Real Estate Market Resilience

Mid-Atlantic real estate remains a regional economic pillar despite high valuations and sub-4% vacancy in core markets; TowneBank’s loan book exposure to commercial and residential property necessitates rigorous stress testing as cycles mature toward late 2025, with CRE concentration limits reviewed against estimated regional cap rates shifting ~50–150bps in 2024–25; sustained demand for multi-family and industrial space (rent growth ~3–6% in 2024) cushions office sector weakness.

Inflationary Impacts on Operational Costs

Persistent inflationary pressures raised Towne Bank’s non-interest expenses in 2025, with wage growth near 5.2% and technology/service costs up about 7.8% year-over-year, contributing to a higher operating expense base.

To offset this, the bank launched efficiency initiatives and automation pilots targeting a 10–15% reduction in back-office FTE hours and expects $12–18 million in annualized savings if fully scaled.

Maintaining a favorable efficiency ratio—recently reported around 58%—is critical for Towne to compete with national banks whose median efficiency ratios are closer to 50% due to larger scale.

Labor Market Dynamics in Service Areas

The bank tracks local unemployment and wage growth as leading indicators; 2024 wage growth of 4.1% regionally correlated with 2.8% consumer loan growth and 1.6% deposit growth in its markets.

- Unemployment: VA 3.3%, NC 3.6% (Dec 2025)

- Regional wage growth 2024: ~4.1%

- Tech wage increase 2024: ~6.2% y/y

- Observed: consumer loans +2.8%, deposits +1.6%

Small Business Economic Sentiment

The economic health of small and medium enterprises (SMEs) remains a primary driver of TowneBank’s commercial lending, with 2024 SBA-backed lending up ~12% year-over-year and regional small business loan demand rising 9% through Q3 2025.

Entrepreneurial activity in the Mid-Atlantic is robust—small business formation grew 6% in 2024—yet concerns about global supply-chain disruptions and a 2024–25 average U.S. industrial energy price increase of ~8% temper sentiment.

TowneBank augments lending with consultative cash-flow services and working-capital solutions; client advisory engagements increased 18% in 2024 as firms sought guidance navigating 2025’s rate and cost pressures.

- SME lending growth: +12% (2024 SBA-backed)

- Regional loan demand: +9% (through Q3 2025)

- New business formation: +6% (Mid-Atlantic, 2024)

- Industrial energy costs: +8% avg (2024–25)

- Advisory engagements: +18% (2024)

Towne Bank eyes ~3.2% NIM as Fed pause, 4.3% 10y and 45% deposit beta pressure margins

Towne Bank’s NIM guidance stabilizes as Fed pauses in 2025 and 10y Treasury ~4.3% (Q1 2025); deposit beta ~45% (2024) pressures margins while repricing and cost savings target preserving ~3.2% NIM. Regional CRE and multi-family demand (rent growth 3–6% in 2024) mitigate office weakness; SME lending +12% (2024 SBA), advisory engagements +18% (2024) support fee income.

| Metric | Value |

|---|---|

| 10y Treasury (Q1 2025) | 4.3% |

| Deposit beta (2024) | ~45% |

| Target NIM | ~3.2% |

| Regional rent growth (2024) | 3–6% |

| SME lending (2024) | +12% |

| Advisory engagements (2024) | +18% |

Preview Before You Purchase

Towne Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the Towne Bank PESTLE Analysis includes comprehensive political, economic, social, technological, legal, and environmental insights presented in the same structure and detail as the sample.