Hong Kong and China Gas Boston Consulting Group Matrix

Unlock Strategic Clarity

Hong Kong and China Gas sits at an inflection point: traditional piped gas and urban services remain reliable cash generators, while new energy ventures and mainland expansion are potential Stars or Question Marks depending on execution and regulatory shifts. Our preview maps core segments but the full BCG Matrix provides quadrant-by-quadrant placement, revenue drivers, and risk-adjusted recommendations. Purchase the complete report for a ready-to-use Word analysis and Excel summary that tells you exactly where to invest, divest, or double down next.

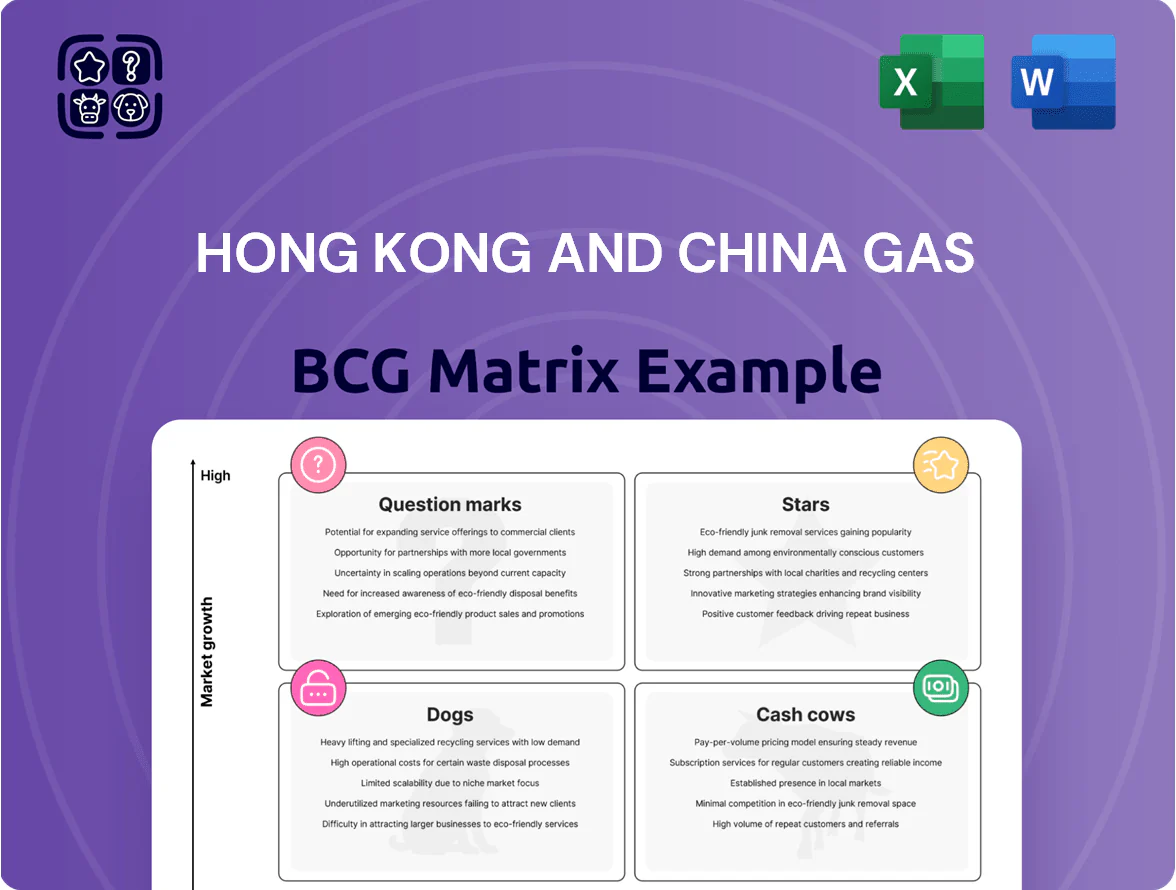

Stars

Mainland China Renewable Energy Projects

As of late 2025 Towngas Smart Energy is a Star in Mainland China, operating 1,000+ renewable projects across 24 provinces and reporting 2.6 GW grid‑connected PV capacity by mid‑2025, driven by China’s dual‑carbon targets (2030 CO2 peak, 2060 neutrality).

These assets delivered double‑digit revenue and EBITDA growth in 2024–25 (company reports show ~15–20% CAGR), but demand ongoing heavy capex—estimated hundreds of millions CNY annually—for grids, storage, and smart‑park integration.

Green Methanol and Sustainable Aviation Fuel (SAF)

This Star segment is fueled by urgent decarbonization in shipping and aviation; SAF demand hit ~3.5 Mt in 2025 global supply and IMO/CORSIA targets push rapid growth. Towngas opened its Malaysia SAF plant in late 2025 and co-founded VENEX to pursue 1.0 Mt green methanol capacity, aiming for commercial volumes by 2028. High market interest and potential share coexist with heavy cash burn: CapEx + R&D likely >USD 700–900M through 2028 to keep first-mover edge.

Mainland City-Gas Smart Metering and Digital Platforms

Mainland City-Gas Smart Metering and Digital Platforms are Stars: rapid urban network modernization in China drives high growth for smart meters and customer platforms, supporting Towngas’s 322 city-gas projects and 42.1 million customers (2025 internal ops data).

These systems lock in usage data and cut O&M costs—pilots show up to 18% efficiency gains and 12% lower non-revenue gas; still, nationwide rollouts need heavy capex (estimated HKD 3.6–4.2 billion through 2027) to fend off tech-first rivals.

Hydrogen Energy Applications in Hong Kong

With SENTX landfill starting green hydrogen in 2025, Towngas’ Hydrogen Energy business moves into the Star quadrant—first-year output targets 2.5 tonnes/day and aims for 900 tonnes/year by 2026, supporting industrial and mobility demand.

Towngas leverages its 3,700-km pipeline to supply construction sites and refuelling stations, securing local market dominance but facing upfront capex: ~HKD 400–600 million for conversion and electrolysers, keeping cash burn high.

- 2025 green H2 start at SENTX

- Output target 2.5 t/day, 900 t/yr by 2026

- 3,700-km pipeline reuse

- Capex ~HKD 400–600m, high cash consumption

- Star: high growth, strong position, heavy investment

Distributed Energy and Storage Solutions

Integrating photovoltaic, energy storage and electricity sales now drives growth in mainland China industrial parks; by mid-2025 Towngas secured 775 MWh of ESS contracts, showing strong demand for reliable low-carbon power.

As a zero-carbon smart industrial park leader, Towngas should keep investing in ESS to protect market share and enable higher-margin power sales and grid services amid expanding subsidy-free PV and frequency regulation markets.

- 775 MWh ESS contracts by mid-2025

- Core model: PV + ESS + retail electricity

- Targets: industrial-park decarbonisation, grid services revenue

Towngas: Rapid 2.6GW PV, 775MWh ESS, H2 buildout—major capex ahead

Towngas Stars: rapid renewables, hydrogen, smart meters; 2.6 GW PV (mid‑2025), 775 MWh ESS, 322 city‑gas projects/42.1M customers, SENTX H2 2.5 t/day (900 t/yr 2026); capex needs high — CNY hundreds‑M pa PV/storage, HKD 3.6–4.2B metering, HKD 400–600M H2.

| Metric | Value |

|---|---|

| PV | 2.6 GW |

| ESS | 775 MWh |

| H2 | 2.5 t/day |

What is included in the product

BCG Matrix review of Hong Kong & China Gas: quadrant-by-quadrant strategic guidance—invest in Stars, milk Cash Cows, selectively grow Question Marks, divest Dogs.

One-page overview placing each Hong Kong and China Gas business unit in a BCG quadrant for instant strategic clarity.

Cash Cows

Hong Kong Piped Gas Utility

Towngas remains Hong Kong’s sole piped gas supplier, serving over 2.1 million customers (≈90% household penetration) and holding a near-monopoly market share.

The mature utility yields stable cash flow and high EBIT margins around 18% (FY2024 reported EBIT margin 17.8%), driven by low capex needs and a dense distribution network.

Cash from this segment funded ~HKD 2.3 billion of the Group’s new-energy investments in 2024, and is the primary source backing Stars and Question Marks.

Established Mainland City-Gas Concessions

The Group's mature city-gas projects across Tier 1–2 mainland cities act as Cash Cows, delivering steady cashflows from long-term concessions and high market share in saturated urban grids.

Stable urbanization and cost-pass-through lifted dollar margins to RMB 0.54/m3 by Dec 2025, supporting predictable EBITDA; China Gas reported mainland gas sales volumes of ~22.3 billion m3 in 2025.

With low market growth, management focuses on milking cash via tariff optimization, O&M efficiency and capex discipline to sustain returns and free cash flow.

Water and Waste Management Services

Operating across multiple mainland provinces, Hong Kong and China Gas’s water and waste management arm delivered 8% profit growth in 2025, reflecting low-growth but steady returns; revenue visibility is high due to long-term concession contracts averaging 20–30 years.

These essential utilities require minimal marketing, generate predictable cash flow—water projects contributed roughly HK$1.8 billion operating cash in 2025—and supply stable capital for Group reinvestment while lowering overall portfolio risk.

Appliances and Extended B2C Services

Leveraging a 44 million household customer base, Towngas sells Mia Cucina appliances and Bauhinia home insurance, driving high-margin, low-capex revenue in mature HK and established China regions.

The segment supplies steady daily revenue per household—small-service fees and appliance sales—boosting 2024 operating margins above the Group average and contributing materially to net profit without large infrastructure spend.

- 44 million households reach

- Mature markets: HK and established mainland cities

- High margins, low capex

- Steady daily revenue per household

- Supports Group net profit in 2024

Mainland Regulated Gas Transmission

Mainland Regulated Gas Transmission acts as a Cash Cow for Hong Kong and China Gas by delivering steady, regulated returns from midstream assets and transmission pipelines essential to gas flow; these assets reported c. RMB 2.4 billion EBITDA in FY2024 and face high barriers to entry due to network scale and permits.

They need only maintenance-level capex—estimated RMB 300–400 million annually—so Towngas can redeploy excess cash into its green energy transition and low-carbon projects.

- FY2024 EBITDA ~RMB 2.4 billion

- Annual maintenance capex ~RMB 300–400 million

- High regulatory barriers and long-term contracts

- Cash reallocated to green energy investments

Towngas: Near‑monopoly cash cow—stable margins, 2.1m HK customers, RMB2.4bn midstream EBITDA

Towngas and mainland city-gas projects are Cash Cows: near‑monopoly HK supply (2.1m customers) plus Tier‑1/2 city concessions yield stable EBITDA (FY2024 EBIT 17.8%; mainland sales ~22.3bn m3 in 2025) and fund ~HKD2.3bn new‑energy spend in 2024; midstream EBITDA ~RMB2.4bn (FY2024) with maintenance capex ~RMB300–400m.

| Metric | Value |

|---|---|

| HK customers | 2.1m |

| FY2024 EBIT margin | 17.8% |

| Mainland sales (2025) | 22.3bn m3 |

| Midstream EBITDA (FY2024) | RMB2.4bn |

| Annual maint. capex | RMB300–400m |

Delivered as Shown

Hong Kong and China Gas BCG Matrix

The file you're previewing is the final Hong Kong and China Gas BCG Matrix you'll receive after purchase—no watermarks, no demo content; just a fully formatted, presentation-ready strategic analysis tailored for market clarity and decision-making.

This preview matches the exact document delivered post-purchase, crafted with market-backed inputs and clear quadrant placement so you can immediately use it for portfolio review, investor briefings, or internal strategy sessions.

What you see is the live BCG Matrix file available for instant download after one-time payment, editable and printable for seamless inclusion in reports, decks, or stakeholder presentations.

Prepared by strategy professionals, the report is analysis-ready and designed for direct application in business planning and competitive assessment—no further edits required unless you choose to customize.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Hong Kong and China Gas sits at an inflection point: traditional piped gas and urban services remain reliable cash generators, while new energy ventures and mainland expansion are potential Stars or Question Marks depending on execution and regulatory shifts. Our preview maps core segments but the full BCG Matrix provides quadrant-by-quadrant placement, revenue drivers, and risk-adjusted recommendations. Purchase the complete report for a ready-to-use Word analysis and Excel summary that tells you exactly where to invest, divest, or double down next.

Stars

Mainland China Renewable Energy Projects

As of late 2025 Towngas Smart Energy is a Star in Mainland China, operating 1,000+ renewable projects across 24 provinces and reporting 2.6 GW grid‑connected PV capacity by mid‑2025, driven by China’s dual‑carbon targets (2030 CO2 peak, 2060 neutrality).

These assets delivered double‑digit revenue and EBITDA growth in 2024–25 (company reports show ~15–20% CAGR), but demand ongoing heavy capex—estimated hundreds of millions CNY annually—for grids, storage, and smart‑park integration.

Green Methanol and Sustainable Aviation Fuel (SAF)

This Star segment is fueled by urgent decarbonization in shipping and aviation; SAF demand hit ~3.5 Mt in 2025 global supply and IMO/CORSIA targets push rapid growth. Towngas opened its Malaysia SAF plant in late 2025 and co-founded VENEX to pursue 1.0 Mt green methanol capacity, aiming for commercial volumes by 2028. High market interest and potential share coexist with heavy cash burn: CapEx + R&D likely >USD 700–900M through 2028 to keep first-mover edge.

Mainland City-Gas Smart Metering and Digital Platforms

Mainland City-Gas Smart Metering and Digital Platforms are Stars: rapid urban network modernization in China drives high growth for smart meters and customer platforms, supporting Towngas’s 322 city-gas projects and 42.1 million customers (2025 internal ops data).

These systems lock in usage data and cut O&M costs—pilots show up to 18% efficiency gains and 12% lower non-revenue gas; still, nationwide rollouts need heavy capex (estimated HKD 3.6–4.2 billion through 2027) to fend off tech-first rivals.

Hydrogen Energy Applications in Hong Kong

With SENTX landfill starting green hydrogen in 2025, Towngas’ Hydrogen Energy business moves into the Star quadrant—first-year output targets 2.5 tonnes/day and aims for 900 tonnes/year by 2026, supporting industrial and mobility demand.

Towngas leverages its 3,700-km pipeline to supply construction sites and refuelling stations, securing local market dominance but facing upfront capex: ~HKD 400–600 million for conversion and electrolysers, keeping cash burn high.

- 2025 green H2 start at SENTX

- Output target 2.5 t/day, 900 t/yr by 2026

- 3,700-km pipeline reuse

- Capex ~HKD 400–600m, high cash consumption

- Star: high growth, strong position, heavy investment

Distributed Energy and Storage Solutions

Integrating photovoltaic, energy storage and electricity sales now drives growth in mainland China industrial parks; by mid-2025 Towngas secured 775 MWh of ESS contracts, showing strong demand for reliable low-carbon power.

As a zero-carbon smart industrial park leader, Towngas should keep investing in ESS to protect market share and enable higher-margin power sales and grid services amid expanding subsidy-free PV and frequency regulation markets.

- 775 MWh ESS contracts by mid-2025

- Core model: PV + ESS + retail electricity

- Targets: industrial-park decarbonisation, grid services revenue

Towngas: Rapid 2.6GW PV, 775MWh ESS, H2 buildout—major capex ahead

Towngas Stars: rapid renewables, hydrogen, smart meters; 2.6 GW PV (mid‑2025), 775 MWh ESS, 322 city‑gas projects/42.1M customers, SENTX H2 2.5 t/day (900 t/yr 2026); capex needs high — CNY hundreds‑M pa PV/storage, HKD 3.6–4.2B metering, HKD 400–600M H2.

| Metric | Value |

|---|---|

| PV | 2.6 GW |

| ESS | 775 MWh |

| H2 | 2.5 t/day |

What is included in the product

BCG Matrix review of Hong Kong & China Gas: quadrant-by-quadrant strategic guidance—invest in Stars, milk Cash Cows, selectively grow Question Marks, divest Dogs.

One-page overview placing each Hong Kong and China Gas business unit in a BCG quadrant for instant strategic clarity.

Cash Cows

Hong Kong Piped Gas Utility

Towngas remains Hong Kong’s sole piped gas supplier, serving over 2.1 million customers (≈90% household penetration) and holding a near-monopoly market share.

The mature utility yields stable cash flow and high EBIT margins around 18% (FY2024 reported EBIT margin 17.8%), driven by low capex needs and a dense distribution network.

Cash from this segment funded ~HKD 2.3 billion of the Group’s new-energy investments in 2024, and is the primary source backing Stars and Question Marks.

Established Mainland City-Gas Concessions

The Group's mature city-gas projects across Tier 1–2 mainland cities act as Cash Cows, delivering steady cashflows from long-term concessions and high market share in saturated urban grids.

Stable urbanization and cost-pass-through lifted dollar margins to RMB 0.54/m3 by Dec 2025, supporting predictable EBITDA; China Gas reported mainland gas sales volumes of ~22.3 billion m3 in 2025.

With low market growth, management focuses on milking cash via tariff optimization, O&M efficiency and capex discipline to sustain returns and free cash flow.

Water and Waste Management Services

Operating across multiple mainland provinces, Hong Kong and China Gas’s water and waste management arm delivered 8% profit growth in 2025, reflecting low-growth but steady returns; revenue visibility is high due to long-term concession contracts averaging 20–30 years.

These essential utilities require minimal marketing, generate predictable cash flow—water projects contributed roughly HK$1.8 billion operating cash in 2025—and supply stable capital for Group reinvestment while lowering overall portfolio risk.

Appliances and Extended B2C Services

Leveraging a 44 million household customer base, Towngas sells Mia Cucina appliances and Bauhinia home insurance, driving high-margin, low-capex revenue in mature HK and established China regions.

The segment supplies steady daily revenue per household—small-service fees and appliance sales—boosting 2024 operating margins above the Group average and contributing materially to net profit without large infrastructure spend.

- 44 million households reach

- Mature markets: HK and established mainland cities

- High margins, low capex

- Steady daily revenue per household

- Supports Group net profit in 2024

Mainland Regulated Gas Transmission

Mainland Regulated Gas Transmission acts as a Cash Cow for Hong Kong and China Gas by delivering steady, regulated returns from midstream assets and transmission pipelines essential to gas flow; these assets reported c. RMB 2.4 billion EBITDA in FY2024 and face high barriers to entry due to network scale and permits.

They need only maintenance-level capex—estimated RMB 300–400 million annually—so Towngas can redeploy excess cash into its green energy transition and low-carbon projects.

- FY2024 EBITDA ~RMB 2.4 billion

- Annual maintenance capex ~RMB 300–400 million

- High regulatory barriers and long-term contracts

- Cash reallocated to green energy investments

Towngas: Near‑monopoly cash cow—stable margins, 2.1m HK customers, RMB2.4bn midstream EBITDA

Towngas and mainland city-gas projects are Cash Cows: near‑monopoly HK supply (2.1m customers) plus Tier‑1/2 city concessions yield stable EBITDA (FY2024 EBIT 17.8%; mainland sales ~22.3bn m3 in 2025) and fund ~HKD2.3bn new‑energy spend in 2024; midstream EBITDA ~RMB2.4bn (FY2024) with maintenance capex ~RMB300–400m.

| Metric | Value |

|---|---|

| HK customers | 2.1m |

| FY2024 EBIT margin | 17.8% |

| Mainland sales (2025) | 22.3bn m3 |

| Midstream EBITDA (FY2024) | RMB2.4bn |

| Annual maint. capex | RMB300–400m |

Delivered as Shown

Hong Kong and China Gas BCG Matrix

The file you're previewing is the final Hong Kong and China Gas BCG Matrix you'll receive after purchase—no watermarks, no demo content; just a fully formatted, presentation-ready strategic analysis tailored for market clarity and decision-making.

This preview matches the exact document delivered post-purchase, crafted with market-backed inputs and clear quadrant placement so you can immediately use it for portfolio review, investor briefings, or internal strategy sessions.

What you see is the live BCG Matrix file available for instant download after one-time payment, editable and printable for seamless inclusion in reports, decks, or stakeholder presentations.

Prepared by strategy professionals, the report is analysis-ready and designed for direct application in business planning and competitive assessment—no further edits required unless you choose to customize.