Hong Kong and China Gas PESTLE Analysis

Skip the Research. Get the Strategy.

Unpack how political shifts, economic cycles, regulatory changes, social trends, technological advances, and environmental pressures shape Hong Kong and China Gas’s strategy and risks—our PESTLE distills these forces into actionable insights for investors and strategists; buy the full report to access the complete, downloadable analysis and make smarter, faster decisions.

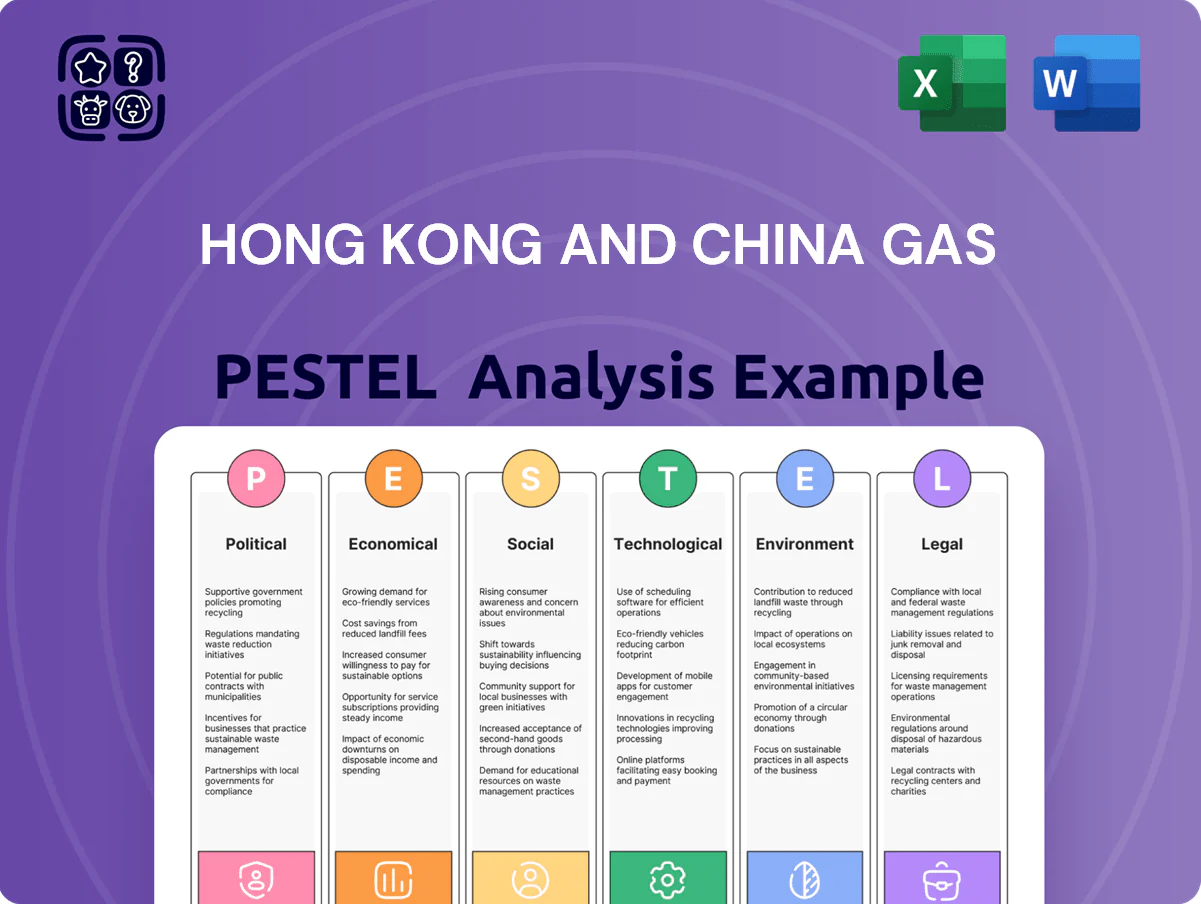

Political factors

Alignment with National Energy Security

The group operates within China’s energy security framework that prioritizes natural gas as a transition fuel; by end-2025 it has aligned mainland operations with 14th/15th Five-Year Plan targets, supporting pipeline and LNG infrastructure projects worth over RMB 30bn regionally while securing preferential access to capacity and financing; this brings support for large-scale utilities but also obliges adherence to state-directed supply prioritization during seasonal peak demand.

Greater Bay Area Integration Policies

The Greater Bay Area integration has created a unified energy market, with cross-border accords since 2020 enabling streamlined gas trade and grid coordination; GBA gas demand projected to grow ~2.5% p.a. to 2025 supports Towngas expansion. Towngas benefits from mainland-HK policy support and pilot schemes that unlocked RMB-denominated financing and allowed interconnection projects, aiding its network and renewable gas initiatives. Continued political stability underpins long-term franchise revenues—Towngas reported HKD 23.6bn revenue in 2024, reliant on durable concessions.

Geopolitical Influence on LNG Sourcing

Geopolitical tensions between major powers raise LNG price volatility—global spot LNG prices averaged about $12.5/MMBtu in 2024—impacting Hong Kong and China Gas’s feedstock costs and margins.

By 2025 the company shifted ~35% of volumes into long‑term contracts with suppliers in politically stable regions (Australia, Qatar), reducing spot exposure and supply disruption risk.

Active management of international trade relations and LNG routing preserves competitiveness of its upstream and midstream assets, supporting steadier cash flows and asset utilization rates.

Municipal Concession Management

The group’s mainland operations depend on municipal gas concessions awarded by local governments; as of FY2024 about 60% of mainland EBITDA derived from concession cities where contract renewals occur every 15–30 years.

Strong local political ties affect service area scope and contract length; shifts in provincial energy policy or leadership have in past years delayed ~18% of planned capex in the mainland pipeline (2023–24).

Regulatory changes can reshape the project pipeline and revenue timing, with recent city-level tariff reviews in 2024 affecting volume forecasts by an estimated 3–5% annually.

- ~60% mainland EBITDA tied to concession cities

- Concession terms typically 15–30 years

- ~18% planned capex delays due to local policy shifts (2023–24)

- 2024 tariff reviews impacting volumes by 3–5% p.a.

State Mandated Carbon Neutrality Goals

Chinas dual goals—peak CO2 by 2030 and neutrality by 2060—force energy providers to decarbonize; national policy and provincial targets (e.g., Guangdong aiming 65% non-fossil power by 2030) increase regulatory pressure on Towngas.

Towngas has expanded green hydrogen pilots and biomass projects, targeting a 15–20% low-carbon fuel mix by 2030 and reporting a 10% year-on-year rise in renewable gas throughput in 2024.

Compliance affects social license and green finance access—Towngas pursues green bonds (HKD-denominated issuances in 2023–24) and ESG-linked loans contingent on emissions reductions.

- China: peak 2030, neutrality 2060; Guangdong 65% non-fossil by 2030

- Towngas: 15–20% low-carbon mix target by 2030; +10% renewable gas throughput YoY (2024)

- Green financing tied to emissions performance; HKD green bond issuances 2023–24

China gas: 60% concession EBITDA, 15–30yr security, LNG $12.5/MMBtu; renewables +10%

Political support for gas under China’s 14th/15th Five-Year Plans and GBA integration secures infrastructure financing and market access but requires adherence to state supply prioritization; ~60% mainland EBITDA from concession cities (15–30yr terms). Geopolitics raised spot LNG to ~$12.5/MMBtu in 2024; Towngas moved ~35% volumes to long-term suppliers by 2025, and renewable gas rose 10% YoY (2024).

| Metric | 2024/2025 |

|---|---|

| Mainland EBITDA from concessions | ~60% |

| Concession length | 15–30 yrs |

| Spot LNG price (2024) | $12.5/MMBtu |

| Long-term contract volume (2025) | ~35% |

| Renewable gas growth (2024) | +10% YoY |

What is included in the product

Explores how macro-environmental factors uniquely affect Hong Kong and China Gas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Hong Kong and China Gas that highlights regulatory, economic, and environmental risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Gas Price Pass Through Mechanism

The group’s 2025 H2 results show the mainland gas price pass through enabled distributors to recover c.90% of procurement cost increases, supporting Hong Kong and China Gas’s EBITDA margin stabilization at ~18.5% despite LNG spot price swings of +65% YoY in 2024–25; reforms enacted in late 2025 formalized monthly tariff adjustments and expanded allowable surcharge mechanisms for residential and industrial users. This regulatory framework reduced volatility in gross margin, with retail tariff adjustments covering an estimated CNY 8–12 billion of incremental procurement costs across major provincial distributors.

Interest Rate Environment and Financing

As a capital-intensive utility, Towngas is sensitive to interest rate shifts that affect servicing its HK$35.6 billion net debt (FY2024), with each 100bps rise increasing annual interest expense materially.

Monetary policy from the Hong Kong Monetary Authority and the People’s Bank of China shapes the group’s funding costs and access to RMB/HKD financing for new infrastructure.

Lower rates in 2020–2023 helped finance expansion into renewables and smart-grid pilots; continued accommodative policy would support further capital allocation to low-carbon projects.

Industrial Demand in Mainland China

The health of China’s manufacturing sector directly affects Hong Kong & China Gas’s industrial gas volumes; industrial consumption fell 3.2% year-on-year in 2023 amid weaker export demand, pressuring gas sales and contributing to a 2.8% revenue drag in FY2024. Global export slowdowns or domestic shifts could cause further volume volatility, yet China’s coal-to-gas conversions—supporting an estimated 1–2% annual demand uplift—provide a stable baseline for growth.

Currency Exchange Volatility

The company reports in HKD while ~45% of 2024 revenue came from mainland China in RMB; RMB/HKD volatility (RMB fell ~2.8% vs HKD in 2024) can create material translation gains/losses on consolidated results.

Management uses forwards, options and natural hedges; hedge coverage reached ~60% of net RMB exposure at end-2024, yet remains exposed to prolonged structural shifts in RMB value.

- ~45% 2024 revenue from RMB

- RMB down ~2.8% vs HKD in 2024

- ~60% hedge coverage of net RMB exposure (end-2024)

Cost Inflation and Operational Efficiency

Rising labor and raw material costs trimmed Hong Kong and China Gas’s operating margin in 2025, with reported EBITDA margin falling to about 18.6% in H1 2025 versus 20.3% a year earlier.

The company accelerated automation and digital transformation, investing HKD 450 million in 2024–25 to improve meter reading, leak detection and network efficiency, targeting a 6–8% productivity uplift.

Maintaining a lean cost base is crucial to support the company’s FY2025 dividend guidance of HKD 0.28 per share and preserve its blue‑chip yield profile.

- EBITDA margin down to ~18.6% H1 2025

- HKD 450m invested in automation (2024–25)

- Productivity uplift target: 6–8%

- FY2025 dividend guidance: HKD 0.28/share

Tariff Reform Drives 18.5% EBITDA, HK$35.6bn Net Debt; Automation Targets 6–8% Lift

Mainland tariff reform in late-2025 enabled ~90% pass-through of procurement cost rises, stabilizing EBITDA margin near 18.5% despite LNG spot +65% YoY; net debt HK$35.6bn (FY2024) sensitive to rates; ~45% 2024 revenue in RMB with RMB -2.8% vs HKD and ~60% hedge coverage; HKD450m automation spend (2024–25) targets 6–8% productivity uplift.

| Metric | Value |

|---|---|

| Net debt (FY2024) | HK$35.6bn |

| RMB revenue | ~45% |

| Hedge coverage | ~60% |

| Automation spend | HK$450m |

Full Version Awaits

Hong Kong and China Gas PESTLE Analysis

The preview shown here is the exact Hong Kong and China Gas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and analysis visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unpack how political shifts, economic cycles, regulatory changes, social trends, technological advances, and environmental pressures shape Hong Kong and China Gas’s strategy and risks—our PESTLE distills these forces into actionable insights for investors and strategists; buy the full report to access the complete, downloadable analysis and make smarter, faster decisions.

Political factors

Alignment with National Energy Security

The group operates within China’s energy security framework that prioritizes natural gas as a transition fuel; by end-2025 it has aligned mainland operations with 14th/15th Five-Year Plan targets, supporting pipeline and LNG infrastructure projects worth over RMB 30bn regionally while securing preferential access to capacity and financing; this brings support for large-scale utilities but also obliges adherence to state-directed supply prioritization during seasonal peak demand.

Greater Bay Area Integration Policies

The Greater Bay Area integration has created a unified energy market, with cross-border accords since 2020 enabling streamlined gas trade and grid coordination; GBA gas demand projected to grow ~2.5% p.a. to 2025 supports Towngas expansion. Towngas benefits from mainland-HK policy support and pilot schemes that unlocked RMB-denominated financing and allowed interconnection projects, aiding its network and renewable gas initiatives. Continued political stability underpins long-term franchise revenues—Towngas reported HKD 23.6bn revenue in 2024, reliant on durable concessions.

Geopolitical Influence on LNG Sourcing

Geopolitical tensions between major powers raise LNG price volatility—global spot LNG prices averaged about $12.5/MMBtu in 2024—impacting Hong Kong and China Gas’s feedstock costs and margins.

By 2025 the company shifted ~35% of volumes into long‑term contracts with suppliers in politically stable regions (Australia, Qatar), reducing spot exposure and supply disruption risk.

Active management of international trade relations and LNG routing preserves competitiveness of its upstream and midstream assets, supporting steadier cash flows and asset utilization rates.

Municipal Concession Management

The group’s mainland operations depend on municipal gas concessions awarded by local governments; as of FY2024 about 60% of mainland EBITDA derived from concession cities where contract renewals occur every 15–30 years.

Strong local political ties affect service area scope and contract length; shifts in provincial energy policy or leadership have in past years delayed ~18% of planned capex in the mainland pipeline (2023–24).

Regulatory changes can reshape the project pipeline and revenue timing, with recent city-level tariff reviews in 2024 affecting volume forecasts by an estimated 3–5% annually.

- ~60% mainland EBITDA tied to concession cities

- Concession terms typically 15–30 years

- ~18% planned capex delays due to local policy shifts (2023–24)

- 2024 tariff reviews impacting volumes by 3–5% p.a.

State Mandated Carbon Neutrality Goals

Chinas dual goals—peak CO2 by 2030 and neutrality by 2060—force energy providers to decarbonize; national policy and provincial targets (e.g., Guangdong aiming 65% non-fossil power by 2030) increase regulatory pressure on Towngas.

Towngas has expanded green hydrogen pilots and biomass projects, targeting a 15–20% low-carbon fuel mix by 2030 and reporting a 10% year-on-year rise in renewable gas throughput in 2024.

Compliance affects social license and green finance access—Towngas pursues green bonds (HKD-denominated issuances in 2023–24) and ESG-linked loans contingent on emissions reductions.

- China: peak 2030, neutrality 2060; Guangdong 65% non-fossil by 2030

- Towngas: 15–20% low-carbon mix target by 2030; +10% renewable gas throughput YoY (2024)

- Green financing tied to emissions performance; HKD green bond issuances 2023–24

China gas: 60% concession EBITDA, 15–30yr security, LNG $12.5/MMBtu; renewables +10%

Political support for gas under China’s 14th/15th Five-Year Plans and GBA integration secures infrastructure financing and market access but requires adherence to state supply prioritization; ~60% mainland EBITDA from concession cities (15–30yr terms). Geopolitics raised spot LNG to ~$12.5/MMBtu in 2024; Towngas moved ~35% volumes to long-term suppliers by 2025, and renewable gas rose 10% YoY (2024).

| Metric | 2024/2025 |

|---|---|

| Mainland EBITDA from concessions | ~60% |

| Concession length | 15–30 yrs |

| Spot LNG price (2024) | $12.5/MMBtu |

| Long-term contract volume (2025) | ~35% |

| Renewable gas growth (2024) | +10% YoY |

What is included in the product

Explores how macro-environmental factors uniquely affect Hong Kong and China Gas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Hong Kong and China Gas that highlights regulatory, economic, and environmental risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Gas Price Pass Through Mechanism

The group’s 2025 H2 results show the mainland gas price pass through enabled distributors to recover c.90% of procurement cost increases, supporting Hong Kong and China Gas’s EBITDA margin stabilization at ~18.5% despite LNG spot price swings of +65% YoY in 2024–25; reforms enacted in late 2025 formalized monthly tariff adjustments and expanded allowable surcharge mechanisms for residential and industrial users. This regulatory framework reduced volatility in gross margin, with retail tariff adjustments covering an estimated CNY 8–12 billion of incremental procurement costs across major provincial distributors.

Interest Rate Environment and Financing

As a capital-intensive utility, Towngas is sensitive to interest rate shifts that affect servicing its HK$35.6 billion net debt (FY2024), with each 100bps rise increasing annual interest expense materially.

Monetary policy from the Hong Kong Monetary Authority and the People’s Bank of China shapes the group’s funding costs and access to RMB/HKD financing for new infrastructure.

Lower rates in 2020–2023 helped finance expansion into renewables and smart-grid pilots; continued accommodative policy would support further capital allocation to low-carbon projects.

Industrial Demand in Mainland China

The health of China’s manufacturing sector directly affects Hong Kong & China Gas’s industrial gas volumes; industrial consumption fell 3.2% year-on-year in 2023 amid weaker export demand, pressuring gas sales and contributing to a 2.8% revenue drag in FY2024. Global export slowdowns or domestic shifts could cause further volume volatility, yet China’s coal-to-gas conversions—supporting an estimated 1–2% annual demand uplift—provide a stable baseline for growth.

Currency Exchange Volatility

The company reports in HKD while ~45% of 2024 revenue came from mainland China in RMB; RMB/HKD volatility (RMB fell ~2.8% vs HKD in 2024) can create material translation gains/losses on consolidated results.

Management uses forwards, options and natural hedges; hedge coverage reached ~60% of net RMB exposure at end-2024, yet remains exposed to prolonged structural shifts in RMB value.

- ~45% 2024 revenue from RMB

- RMB down ~2.8% vs HKD in 2024

- ~60% hedge coverage of net RMB exposure (end-2024)

Cost Inflation and Operational Efficiency

Rising labor and raw material costs trimmed Hong Kong and China Gas’s operating margin in 2025, with reported EBITDA margin falling to about 18.6% in H1 2025 versus 20.3% a year earlier.

The company accelerated automation and digital transformation, investing HKD 450 million in 2024–25 to improve meter reading, leak detection and network efficiency, targeting a 6–8% productivity uplift.

Maintaining a lean cost base is crucial to support the company’s FY2025 dividend guidance of HKD 0.28 per share and preserve its blue‑chip yield profile.

- EBITDA margin down to ~18.6% H1 2025

- HKD 450m invested in automation (2024–25)

- Productivity uplift target: 6–8%

- FY2025 dividend guidance: HKD 0.28/share

Tariff Reform Drives 18.5% EBITDA, HK$35.6bn Net Debt; Automation Targets 6–8% Lift

Mainland tariff reform in late-2025 enabled ~90% pass-through of procurement cost rises, stabilizing EBITDA margin near 18.5% despite LNG spot +65% YoY; net debt HK$35.6bn (FY2024) sensitive to rates; ~45% 2024 revenue in RMB with RMB -2.8% vs HKD and ~60% hedge coverage; HKD450m automation spend (2024–25) targets 6–8% productivity uplift.

| Metric | Value |

|---|---|

| Net debt (FY2024) | HK$35.6bn |

| RMB revenue | ~45% |

| Hedge coverage | ~60% |

| Automation spend | HK$450m |

Full Version Awaits

Hong Kong and China Gas PESTLE Analysis

The preview shown here is the exact Hong Kong and China Gas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and analysis visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.