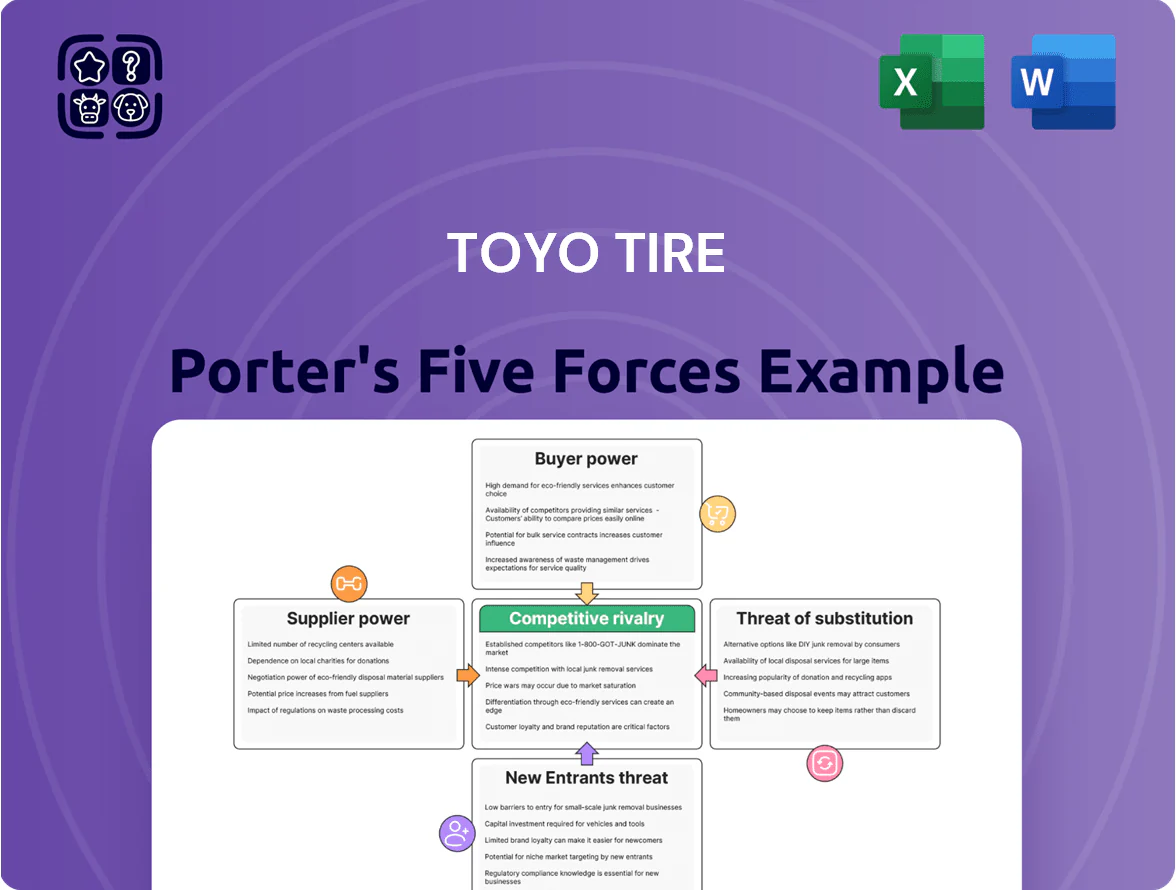

Toyo Tire Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Toyo Tire faces moderate supplier power, intense rivalry in global tyre markets, and evolving substitute threats from mobility tech and retreading; buyer price sensitivity and regulatory shifts add pressure on margins and strategy.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Toyo Tire’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material pricing

Toyo Tire depends on natural rubber, synthetic rubber and carbon black, whose prices swung 18–32% year-on-year in 2024–2025; Southeast Asia weather and crude oil moves drove much of that volatility.

In late 2025 droughts in Thailand and flooding in Indonesia tightened natural rubber supply, lifting spot prices ~28% vs 2023 and giving upstream suppliers bargaining leverage during shortages.

Petrochemical feedstock shifts tied to Brent crude (which ranged $70–95/barrel in 2025) pushed synthetic rubber and carbon black costs up to 20% in some months, squeezing margins if Toyo cannot pass costs to dealers.

To protect profitability Toyo must use hedging, multi-sourcing and long-term contracts; without these, supplier power during shortfalls can materially hit gross margin by several percentage points.

Emphasis on sustainable sourcing requirements

Suppliers of certified sustainable rubber and recycled steel gained leverage as Toyo Tire pushes ESG targets; only about 12 suppliers worldwide met ISO 14001 and EU Green Claims rules by Jan 2025, tightening choice.

Stricter 2025 environmental regs raised compliance costs ~8–12% for suppliers, so specialized green vendors now charge 10–18% premiums and impose longer-term minimums and penalty clauses.

Geopolitical influence on logistics and availability

The concentration of natural rubber production—Thailand and Indonesia account for about 60% of global output in 2024—creates dependence on local political and economic stability, raising supply risk for Toyo Tire.

Political unrest, floods, or export restrictions in those countries can disrupt Toyo’s inventory and force production reschedules, increasing working capital needs.

Suppliers in more stable or diversified regions can charge 5–15% premiums for reliability, giving them bargaining leverage over Toyo’s cost and sourcing choices.

Energy costs and utility dependence

Toyo's tire and component plants are energy‑intensive, so utility pricing directly raises cost of goods sold; in 2024 electricity accounted for roughly 3–6% of manufacturing OPEX in global tyre plants, making suppliers influential.

In regions with limited competition—parts of Japan, Southeast Asia, and Latin America—utility firms exert high bargaining power, squeezing margins; Toyo’s 2023 renewables capex (~¥4.5bn) reduced exposure but grid limits keep reliance on local utilities.

Technological specialization in chemical additives

The development of high-performance tires relies on patented silane coupling agents and specialty polymers held by a handful of chemical firms (e.g., Evonik, LANXESS, and Solvay), giving suppliers strong leverage over Toyo Tire’s SUV/light-truck product lines.

Replacing a supplier triggers 6–18 month re-certification and compound retesting, raising costs and delaying new SKUs, so suppliers extract premium pricing and favorable terms.

In 2024 the global specialty chemicals market was ~$680 billion, concentrating R&D with top 10 firms holding ~55% of sales—this centralization reinforces supplier power for Toyo.

- Patents/specialty grades concentrated among few firms

- 6–18 months switching/testing time

- 2024 specialty chemicals market ~$680B; top 10 ~55%

- Suppliers can demand premiums, affecting margins

Suppliers wield rising power: concentrated rubber, volatile feedstocks, scarce green vendors

Suppliers hold moderate–high power: natural rubber and specialty chemicals are concentrated (Thailand+Indonesia = 60% rubber; 2024 specialty chemicals market ~$680B, top 10 = 55%), 2024–25 raw material swings 18–32%, drought/floods lifted rubber ~28% vs 2023, synthetic feedstock tied to Brent $70–95/barrel in 2025; switching costs 6–18 months; green-certified vendors limited (~12 by Jan 2025), charging 10–18% premiums.

| Metric | Value |

|---|---|

| Rubber share (TH+ID) | 60% |

| Raw price swing 24–25 | 18–32% |

| Rubber spot rise vs 2023 | ~28% |

| Brent 2025 range | $70–95/bbl |

| Specialty chem. market 2024 | $680B (top10=55%) |

| Green suppliers (Jan 2025) | ~12 |

| Switching time | 6–18 months |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to Toyo Tire, highlighting competitive rivalry, buyer and supplier leverage, entry barriers, and substitute threats to illuminate pressures on pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Toyo Tire—quickly highlights supplier, buyer, competitor, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Concentrated buying power of automotive OEMs

Large OEMs exert strong pricing and quality pressure on Toyo Tire, buying millions of units annually—global OEM tire spend exceeds $80 billion in 2024—so Toyo faces tight margin squeeze if it fails cost targets.

OEMs can switch to global leaders like Michelin or Bridgestone; by end-2025 industry consolidation (fewer than 15 global automakers controlling ~70% production) heightens buyers’ leverage.

Low switching costs in the replacement market

Individual consumers in the replacement tire market face very low switching costs when moving from Toyo Tire to rivals; surveys show 62% of U.S. buyers pick on price or availability over brand (2024 NPD data). With over 20 national and import brands at multiple price bands, loyalty is weak, so Toyo spent $145 million on marketing and dealer incentives in 2024 to protect shelf space and preference.

Price transparency through digital platforms

Price transparency via online tire retailers and comparison tools lets customers find lowest prices instantly; 2025 surveys show 72% of US tire shoppers use online comparison before buying, pressuring margins. This transparency weakens Toyo Tire and distributors’ ability to sustain premium pricing without measurable performance leads—Toyo’s 2024 ASP (average selling price) fell 4.1% in North America. With 58% of tire sales researched primarily online by 2025, price competition is more visible and intense than ever.

Influence of large-scale distributors and retailers

- Major chains control 60–70% US replacement sales

- Required margins commonly 20–30%

- Toyo 2024 promo spend ~¥15.2bn

Growing demand for specialized EV tire features

As EV adoption hit ~14% of global new car sales in 2025, buyers now demand tires with lower rolling resistance and less noise, pushing Toyo to invest in EV-specific compounds and tread designs.

That demand helps Toyo differentiate, but well-informed fleet and OEM customers now insist on advanced features at tight price points, increasing their bargaining power and pressuring margins.

Buyers compare specs and life-cycle cost, tilting power to suppliers who can offer the best performance-to-price ratio.

- 2025 EV share ~14%

- Key asks: rolling resistance, NVH (noise) reduction

- OEMs/fleets demand high features, low prices

- Performance-to-price drives buying decisions

Toyo Under Margin Pressure: OEMs, Chains & Price-Driven Shoppers Erode Pricing Power

Large OEMs and big chains wield strong price/quality leverage—global OEM tire spend >$80bn (2024) and US chains control 60–70% replacement sales—so Toyo faces tight margins and must fund ~¥15.2bn (2024) promo + $145m marketing to keep shelf space; online price comparison (72% of shoppers, 2025) and 62% price-driven buyers (2024) further weaken pricing power.

| Metric | Value |

|---|---|

| Global OEM tire spend (2024) | $80bn+ |

| US chain share | 60–70% |

| Toyo promo/marketing (2024) | ¥15.2bn / $145m |

| Online comparison use (2025) | 72% |

| Price-driven US buyers (2024) | 62% |

Same Document Delivered

Toyo Tire Porter's Five Forces Analysis

This preview shows the exact Toyo Tire Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, complete, and ready for use. The document displayed here is the actual deliverable with no placeholders or mockups, so what you see is what you’ll download the moment you buy. You’ll get instant access to this same professionally written file for your analysis and decision-making needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Toyo Tire faces moderate supplier power, intense rivalry in global tyre markets, and evolving substitute threats from mobility tech and retreading; buyer price sensitivity and regulatory shifts add pressure on margins and strategy.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Toyo Tire’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material pricing

Toyo Tire depends on natural rubber, synthetic rubber and carbon black, whose prices swung 18–32% year-on-year in 2024–2025; Southeast Asia weather and crude oil moves drove much of that volatility.

In late 2025 droughts in Thailand and flooding in Indonesia tightened natural rubber supply, lifting spot prices ~28% vs 2023 and giving upstream suppliers bargaining leverage during shortages.

Petrochemical feedstock shifts tied to Brent crude (which ranged $70–95/barrel in 2025) pushed synthetic rubber and carbon black costs up to 20% in some months, squeezing margins if Toyo cannot pass costs to dealers.

To protect profitability Toyo must use hedging, multi-sourcing and long-term contracts; without these, supplier power during shortfalls can materially hit gross margin by several percentage points.

Emphasis on sustainable sourcing requirements

Suppliers of certified sustainable rubber and recycled steel gained leverage as Toyo Tire pushes ESG targets; only about 12 suppliers worldwide met ISO 14001 and EU Green Claims rules by Jan 2025, tightening choice.

Stricter 2025 environmental regs raised compliance costs ~8–12% for suppliers, so specialized green vendors now charge 10–18% premiums and impose longer-term minimums and penalty clauses.

Geopolitical influence on logistics and availability

The concentration of natural rubber production—Thailand and Indonesia account for about 60% of global output in 2024—creates dependence on local political and economic stability, raising supply risk for Toyo Tire.

Political unrest, floods, or export restrictions in those countries can disrupt Toyo’s inventory and force production reschedules, increasing working capital needs.

Suppliers in more stable or diversified regions can charge 5–15% premiums for reliability, giving them bargaining leverage over Toyo’s cost and sourcing choices.

Energy costs and utility dependence

Toyo's tire and component plants are energy‑intensive, so utility pricing directly raises cost of goods sold; in 2024 electricity accounted for roughly 3–6% of manufacturing OPEX in global tyre plants, making suppliers influential.

In regions with limited competition—parts of Japan, Southeast Asia, and Latin America—utility firms exert high bargaining power, squeezing margins; Toyo’s 2023 renewables capex (~¥4.5bn) reduced exposure but grid limits keep reliance on local utilities.

Technological specialization in chemical additives

The development of high-performance tires relies on patented silane coupling agents and specialty polymers held by a handful of chemical firms (e.g., Evonik, LANXESS, and Solvay), giving suppliers strong leverage over Toyo Tire’s SUV/light-truck product lines.

Replacing a supplier triggers 6–18 month re-certification and compound retesting, raising costs and delaying new SKUs, so suppliers extract premium pricing and favorable terms.

In 2024 the global specialty chemicals market was ~$680 billion, concentrating R&D with top 10 firms holding ~55% of sales—this centralization reinforces supplier power for Toyo.

- Patents/specialty grades concentrated among few firms

- 6–18 months switching/testing time

- 2024 specialty chemicals market ~$680B; top 10 ~55%

- Suppliers can demand premiums, affecting margins

Suppliers wield rising power: concentrated rubber, volatile feedstocks, scarce green vendors

Suppliers hold moderate–high power: natural rubber and specialty chemicals are concentrated (Thailand+Indonesia = 60% rubber; 2024 specialty chemicals market ~$680B, top 10 = 55%), 2024–25 raw material swings 18–32%, drought/floods lifted rubber ~28% vs 2023, synthetic feedstock tied to Brent $70–95/barrel in 2025; switching costs 6–18 months; green-certified vendors limited (~12 by Jan 2025), charging 10–18% premiums.

| Metric | Value |

|---|---|

| Rubber share (TH+ID) | 60% |

| Raw price swing 24–25 | 18–32% |

| Rubber spot rise vs 2023 | ~28% |

| Brent 2025 range | $70–95/bbl |

| Specialty chem. market 2024 | $680B (top10=55%) |

| Green suppliers (Jan 2025) | ~12 |

| Switching time | 6–18 months |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to Toyo Tire, highlighting competitive rivalry, buyer and supplier leverage, entry barriers, and substitute threats to illuminate pressures on pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Toyo Tire—quickly highlights supplier, buyer, competitor, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Concentrated buying power of automotive OEMs

Large OEMs exert strong pricing and quality pressure on Toyo Tire, buying millions of units annually—global OEM tire spend exceeds $80 billion in 2024—so Toyo faces tight margin squeeze if it fails cost targets.

OEMs can switch to global leaders like Michelin or Bridgestone; by end-2025 industry consolidation (fewer than 15 global automakers controlling ~70% production) heightens buyers’ leverage.

Low switching costs in the replacement market

Individual consumers in the replacement tire market face very low switching costs when moving from Toyo Tire to rivals; surveys show 62% of U.S. buyers pick on price or availability over brand (2024 NPD data). With over 20 national and import brands at multiple price bands, loyalty is weak, so Toyo spent $145 million on marketing and dealer incentives in 2024 to protect shelf space and preference.

Price transparency through digital platforms

Price transparency via online tire retailers and comparison tools lets customers find lowest prices instantly; 2025 surveys show 72% of US tire shoppers use online comparison before buying, pressuring margins. This transparency weakens Toyo Tire and distributors’ ability to sustain premium pricing without measurable performance leads—Toyo’s 2024 ASP (average selling price) fell 4.1% in North America. With 58% of tire sales researched primarily online by 2025, price competition is more visible and intense than ever.

Influence of large-scale distributors and retailers

- Major chains control 60–70% US replacement sales

- Required margins commonly 20–30%

- Toyo 2024 promo spend ~¥15.2bn

Growing demand for specialized EV tire features

As EV adoption hit ~14% of global new car sales in 2025, buyers now demand tires with lower rolling resistance and less noise, pushing Toyo to invest in EV-specific compounds and tread designs.

That demand helps Toyo differentiate, but well-informed fleet and OEM customers now insist on advanced features at tight price points, increasing their bargaining power and pressuring margins.

Buyers compare specs and life-cycle cost, tilting power to suppliers who can offer the best performance-to-price ratio.

- 2025 EV share ~14%

- Key asks: rolling resistance, NVH (noise) reduction

- OEMs/fleets demand high features, low prices

- Performance-to-price drives buying decisions

Toyo Under Margin Pressure: OEMs, Chains & Price-Driven Shoppers Erode Pricing Power

Large OEMs and big chains wield strong price/quality leverage—global OEM tire spend >$80bn (2024) and US chains control 60–70% replacement sales—so Toyo faces tight margins and must fund ~¥15.2bn (2024) promo + $145m marketing to keep shelf space; online price comparison (72% of shoppers, 2025) and 62% price-driven buyers (2024) further weaken pricing power.

| Metric | Value |

|---|---|

| Global OEM tire spend (2024) | $80bn+ |

| US chain share | 60–70% |

| Toyo promo/marketing (2024) | ¥15.2bn / $145m |

| Online comparison use (2025) | 72% |

| Price-driven US buyers (2024) | 62% |

Same Document Delivered

Toyo Tire Porter's Five Forces Analysis

This preview shows the exact Toyo Tire Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, complete, and ready for use. The document displayed here is the actual deliverable with no placeholders or mockups, so what you see is what you’ll download the moment you buy. You’ll get instant access to this same professionally written file for your analysis and decision-making needs.