Tracsis PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech disruption are reshaping Tracsis—our concise PESTLE snapshot highlights key external risks and opportunities to inform your strategy. Buy the full PESTLE for a detailed, ready-to-use report with actionable insights, editable charts, and sector-specific implications to guide investment or strategic decisions.

Political factors

Government Rail Reform and Great British Railways

The transition to Great British Railways (GBR) centralizes contract bidding and planning, creating demand for unified software; UK government estimates GBR will control ~70% of network functions by 2025-26, accelerating procurements for resource management systems. Tracsis, with FY2024 revenue of £120.8m and growing SaaS bookings, is positioned to capture contracts as operators seek standardized tools. Political stability and the pace of GBR legislation remain key risks that will determine timing of major contract awards.

Public Infrastructure Investment Levels

Government budgetary allocations for transport infrastructure directly affect Tracsis's traffic data and consultancy divisions; the UK 2024 Budget committed 20.7 billion pounds to transport capital investment for 2025/26, underpinning demand for planning-stage analytics.

Political focus on leveling up and regional connectivity—reflected in 2023–25 levelling up fund awards of 2.6 billion pounds—drives need for Tracsis's services during major project appraisals.

Conversely, shifts toward fiscal tightening or austerity risk delays or scope cuts: 2024 fiscal tightening scenarios projected up to 10–15% cuts to local transport capital could reduce short-term consultancy revenues.

International Trade and North American Expansion

As Tracsis expands into North America it faces scrutiny over foreign tech in critical infrastructure; US Committee on Foreign Investment reviews rose 18% in 2024, increasing due diligence and potential delays for UK providers.

UK-US trade ties and USMCA-related frameworks affect cross-border ops and IP; bilateral trade in services was about $338bn in 2024, easing market access but requiring robust IP contracts.

US emphasis on rail safety—Positive Train Control now active on most mainlines after FRA deadlines—creates demand for safety-critical software; US rail safety spending reached $7.5bn in 2023–24, favoring Tracsis offerings.

Subsidies for Green Transport Initiatives

- UK/EU subsidies target rail decarbonisation (eg. £120m+ Network Rail funding)

- Tracsis software can cut fleet energy use ~10–15%

- Subsidy variability from political shifts risks pipeline volatility

Geopolitical Stability and Supply Chain Security

Global political tensions, such as US-China tech frictions, risk disrupting procurement of sensors and semiconductors for Tracsis; global semiconductor lead times averaged 16–24 weeks in 2024, elevating component costs by ~12% year-on-year for industrial IoT suppliers.

Policies securing supply chains (eg UK/NATO resilience programs) may force Tracsis to audit and diversify manufacturers, increasing supplier management spend and CAPEX on certified sources.

Instability in sourcing regions can cause delivery delays and cost inflation—logistics insurance and contingency inventory raised OPEX by an estimated 3–5% for comparable firms in 2024.

- Semiconductor lead times 16–24 weeks (2024)

- Component cost rise ~12% YoY for industrial IoT (2024)

- Contingency OPEX increase 3–5% due to instability

- Supply-chain audits/diversification raise CAPEX/OPEX

Tracsis set to gain from £20.7bn UK capex and 70% GBR centralisation despite supply risks

GBR centralisation (70% network control by 2025–26) and UK transport capital (£20.7bn for 2025/26) boost Tracsis SaaS demand; FY2024 revenue £120.8m. Fiscal tightening risks 10–15% local cuts; US CFI reviews +18% (2024) and semiconductor lead times 16–24 weeks raise entry/ supply risks. Rail safety spending $7.5bn (2023–24) and £120m rail decarbonisation funding favor Tracsis energy-efficiency tools.

| Metric | Value |

|---|---|

| FY2024 revenue | £120.8m |

| UK transport capex 2025/26 | £20.7bn |

| GBR control | ~70% by 2025–26 |

| Semiconductor lead time 2024 | 16–24 wks |

| US rail safety spend | $7.5bn (2023–24) |

What is included in the product

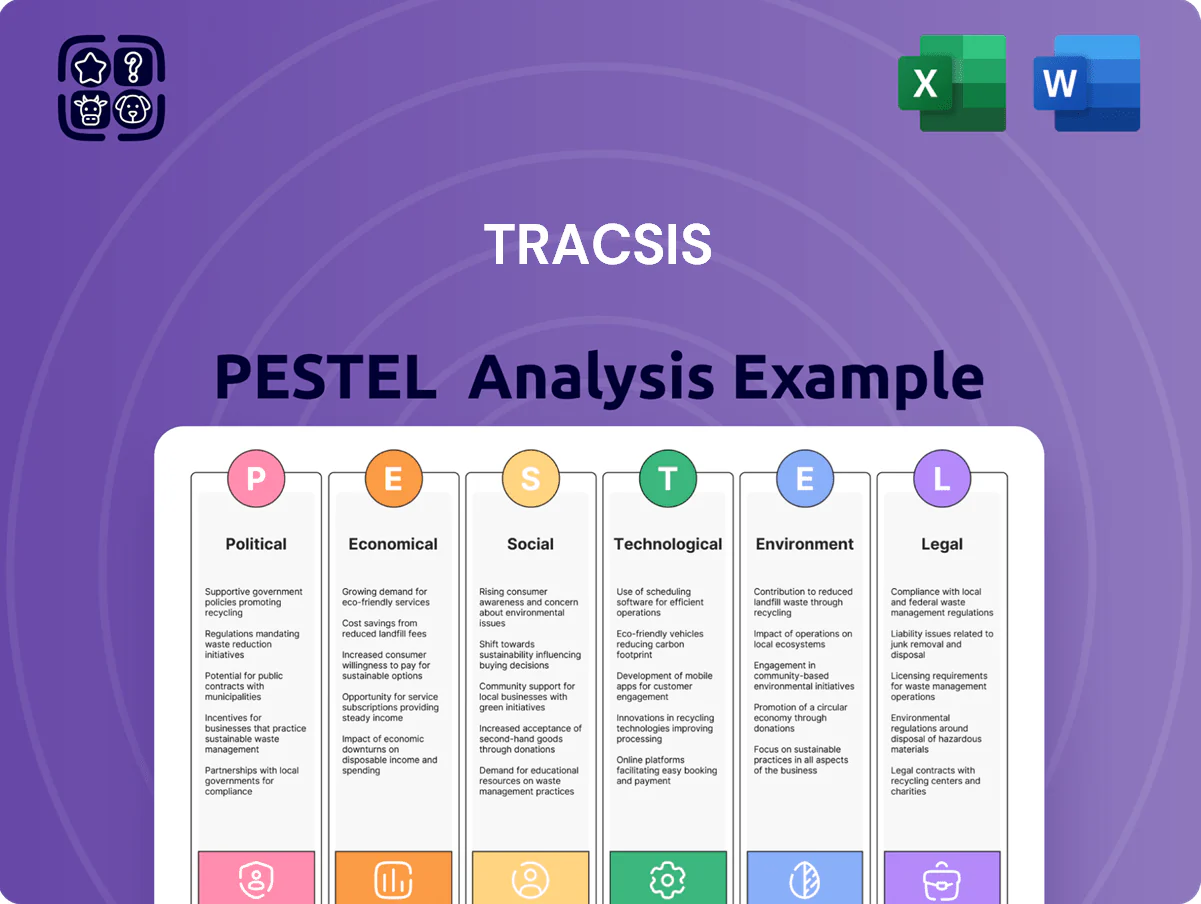

Explores how macro-environmental forces uniquely affect Tracsis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to highlight risks and opportunities.

Condenses Tracsis's PESTLE into a clear, shareable summary organized by category for quick use in meetings, presentations, or strategy packs.

Economic factors

Inflationary Pressures and Operational Costs

High UK CPI inflation at 4.0% in 2024 elevates labor costs for Tracsis, especially for specialized software engineers and data scientists whose average salaries rose ~6–8% year-on-year in 2023–24.

Many long-term contracts include inflation-linked price escalators, but indexation lags can create temporary margin compression between cost spikes and revenue adjustments.

Managing a margin squeeze amid price volatility is critical; Tracsis reported gross margin of ~42% in FY24, underscoring sensitivity to rising operating expenses.

Rail Passenger Volume and Revenue Models

Interest Rates and Acquisition Strategy

Tracsis has used disciplined M&A to scale, completing 10+ acquisitions since 2014 to add niche transport tech capabilities and lift 2024 revenue to c.£99m; rising Bank Rate (UK) to 5.25% in 2024 increases cost of debt and pushes up acquisition hurdle rates. Higher rates make debt-funded deals pricier and may slow deal cadence unless Tracsis uses cash or equity. The group must balance its c.£15–20m cash reserves (2024) against higher borrowing costs to continue consolidating a fragmented market.

Currency Exchange Rate Fluctuations

As Tracsis expands in the US and Europe, GBP/USD and GBP/EUR swings affect reported international revenues and margins; a 10% GBP weakness vs USD in 2024 would have increased translated US revenue impact materially given FY2024 international revenues ~30% of group turnover (£79.1m total revenue in 2024).

Currency moves also influence pricing competitiveness abroad and can compress UK-reported EBITDA if unhedged; Tracsis uses forward contracts and local-currency contracting to reduce volatility in the consolidated balance sheet.

- Exposure: rising US/Europe footprint, ~30% international revenue (FY2024)

- Risk: GBP volatility vs USD/EUR affects translated earnings and pricing

- Mitigation: forward hedges, local-currency contracts to stabilise EBITDA and balance sheet

Labor Market Dynamics in Tech

The competitive market for technical talent in the UK and North America pushes Tracsis to offer higher pay; UK tech median salaries rose ~7% in 2024 and US software engineer median pay grew ~6%, increasing hiring costs.

Shortages—ONS showed 2024 UK vacancy rates for tech roles up ~15% year-on-year—can slow Tracsis scaling by limiting available data analysts and developers.

Tracsis must boost retention and graduate intake; investing in apprenticeships and graduate programs can stabilize the talent pipeline and offset rising recruitment costs.

- Higher compensation: UK tech pay +7% (2024), US +6% (2024)

- Talent shortages: UK tech vacancies +15% y/y (2024)

- Mitigation: retention, apprenticeships, graduate programs

Higher costs, squeezed margins: FY24 revenue £99m, gross margin ~42%, rail recovery lags

High UK CPI 4.0% (2024) and tech pay rises UK +7%/US +6% (2024) pressure margins; FY24 gross margin ~42% with revenue c.£99m and international ~30%. Bank Rate 5.25% raises borrowing costs; cash c.£15–20m. GB rail journeys 1.2bn (2024) vs 1.7bn (2019) affect client spend; TOC IT cuts up to 15% in 2023–24. Hedging/local contracts mitigate FX risk.

| Metric | 2024 |

|---|---|

| UK CPI | 4.0% |

| Gross margin | ~42% |

| Revenue | c.£99m |

| Intl revenue | ~30% |

| Bank Rate | 5.25% |

| Cash | £15–20m |

| GB rail journeys | 1.2bn |

Same Document Delivered

Tracsis PESTLE Analysis

The preview shown here is the exact Tracsis PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech disruption are reshaping Tracsis—our concise PESTLE snapshot highlights key external risks and opportunities to inform your strategy. Buy the full PESTLE for a detailed, ready-to-use report with actionable insights, editable charts, and sector-specific implications to guide investment or strategic decisions.

Political factors

Government Rail Reform and Great British Railways

The transition to Great British Railways (GBR) centralizes contract bidding and planning, creating demand for unified software; UK government estimates GBR will control ~70% of network functions by 2025-26, accelerating procurements for resource management systems. Tracsis, with FY2024 revenue of £120.8m and growing SaaS bookings, is positioned to capture contracts as operators seek standardized tools. Political stability and the pace of GBR legislation remain key risks that will determine timing of major contract awards.

Public Infrastructure Investment Levels

Government budgetary allocations for transport infrastructure directly affect Tracsis's traffic data and consultancy divisions; the UK 2024 Budget committed 20.7 billion pounds to transport capital investment for 2025/26, underpinning demand for planning-stage analytics.

Political focus on leveling up and regional connectivity—reflected in 2023–25 levelling up fund awards of 2.6 billion pounds—drives need for Tracsis's services during major project appraisals.

Conversely, shifts toward fiscal tightening or austerity risk delays or scope cuts: 2024 fiscal tightening scenarios projected up to 10–15% cuts to local transport capital could reduce short-term consultancy revenues.

International Trade and North American Expansion

As Tracsis expands into North America it faces scrutiny over foreign tech in critical infrastructure; US Committee on Foreign Investment reviews rose 18% in 2024, increasing due diligence and potential delays for UK providers.

UK-US trade ties and USMCA-related frameworks affect cross-border ops and IP; bilateral trade in services was about $338bn in 2024, easing market access but requiring robust IP contracts.

US emphasis on rail safety—Positive Train Control now active on most mainlines after FRA deadlines—creates demand for safety-critical software; US rail safety spending reached $7.5bn in 2023–24, favoring Tracsis offerings.

Subsidies for Green Transport Initiatives

- UK/EU subsidies target rail decarbonisation (eg. £120m+ Network Rail funding)

- Tracsis software can cut fleet energy use ~10–15%

- Subsidy variability from political shifts risks pipeline volatility

Geopolitical Stability and Supply Chain Security

Global political tensions, such as US-China tech frictions, risk disrupting procurement of sensors and semiconductors for Tracsis; global semiconductor lead times averaged 16–24 weeks in 2024, elevating component costs by ~12% year-on-year for industrial IoT suppliers.

Policies securing supply chains (eg UK/NATO resilience programs) may force Tracsis to audit and diversify manufacturers, increasing supplier management spend and CAPEX on certified sources.

Instability in sourcing regions can cause delivery delays and cost inflation—logistics insurance and contingency inventory raised OPEX by an estimated 3–5% for comparable firms in 2024.

- Semiconductor lead times 16–24 weeks (2024)

- Component cost rise ~12% YoY for industrial IoT (2024)

- Contingency OPEX increase 3–5% due to instability

- Supply-chain audits/diversification raise CAPEX/OPEX

Tracsis set to gain from £20.7bn UK capex and 70% GBR centralisation despite supply risks

GBR centralisation (70% network control by 2025–26) and UK transport capital (£20.7bn for 2025/26) boost Tracsis SaaS demand; FY2024 revenue £120.8m. Fiscal tightening risks 10–15% local cuts; US CFI reviews +18% (2024) and semiconductor lead times 16–24 weeks raise entry/ supply risks. Rail safety spending $7.5bn (2023–24) and £120m rail decarbonisation funding favor Tracsis energy-efficiency tools.

| Metric | Value |

|---|---|

| FY2024 revenue | £120.8m |

| UK transport capex 2025/26 | £20.7bn |

| GBR control | ~70% by 2025–26 |

| Semiconductor lead time 2024 | 16–24 wks |

| US rail safety spend | $7.5bn (2023–24) |

What is included in the product

Explores how macro-environmental forces uniquely affect Tracsis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to highlight risks and opportunities.

Condenses Tracsis's PESTLE into a clear, shareable summary organized by category for quick use in meetings, presentations, or strategy packs.

Economic factors

Inflationary Pressures and Operational Costs

High UK CPI inflation at 4.0% in 2024 elevates labor costs for Tracsis, especially for specialized software engineers and data scientists whose average salaries rose ~6–8% year-on-year in 2023–24.

Many long-term contracts include inflation-linked price escalators, but indexation lags can create temporary margin compression between cost spikes and revenue adjustments.

Managing a margin squeeze amid price volatility is critical; Tracsis reported gross margin of ~42% in FY24, underscoring sensitivity to rising operating expenses.

Rail Passenger Volume and Revenue Models

Interest Rates and Acquisition Strategy

Tracsis has used disciplined M&A to scale, completing 10+ acquisitions since 2014 to add niche transport tech capabilities and lift 2024 revenue to c.£99m; rising Bank Rate (UK) to 5.25% in 2024 increases cost of debt and pushes up acquisition hurdle rates. Higher rates make debt-funded deals pricier and may slow deal cadence unless Tracsis uses cash or equity. The group must balance its c.£15–20m cash reserves (2024) against higher borrowing costs to continue consolidating a fragmented market.

Currency Exchange Rate Fluctuations

As Tracsis expands in the US and Europe, GBP/USD and GBP/EUR swings affect reported international revenues and margins; a 10% GBP weakness vs USD in 2024 would have increased translated US revenue impact materially given FY2024 international revenues ~30% of group turnover (£79.1m total revenue in 2024).

Currency moves also influence pricing competitiveness abroad and can compress UK-reported EBITDA if unhedged; Tracsis uses forward contracts and local-currency contracting to reduce volatility in the consolidated balance sheet.

- Exposure: rising US/Europe footprint, ~30% international revenue (FY2024)

- Risk: GBP volatility vs USD/EUR affects translated earnings and pricing

- Mitigation: forward hedges, local-currency contracts to stabilise EBITDA and balance sheet

Labor Market Dynamics in Tech

The competitive market for technical talent in the UK and North America pushes Tracsis to offer higher pay; UK tech median salaries rose ~7% in 2024 and US software engineer median pay grew ~6%, increasing hiring costs.

Shortages—ONS showed 2024 UK vacancy rates for tech roles up ~15% year-on-year—can slow Tracsis scaling by limiting available data analysts and developers.

Tracsis must boost retention and graduate intake; investing in apprenticeships and graduate programs can stabilize the talent pipeline and offset rising recruitment costs.

- Higher compensation: UK tech pay +7% (2024), US +6% (2024)

- Talent shortages: UK tech vacancies +15% y/y (2024)

- Mitigation: retention, apprenticeships, graduate programs

Higher costs, squeezed margins: FY24 revenue £99m, gross margin ~42%, rail recovery lags

High UK CPI 4.0% (2024) and tech pay rises UK +7%/US +6% (2024) pressure margins; FY24 gross margin ~42% with revenue c.£99m and international ~30%. Bank Rate 5.25% raises borrowing costs; cash c.£15–20m. GB rail journeys 1.2bn (2024) vs 1.7bn (2019) affect client spend; TOC IT cuts up to 15% in 2023–24. Hedging/local contracts mitigate FX risk.

| Metric | 2024 |

|---|---|

| UK CPI | 4.0% |

| Gross margin | ~42% |

| Revenue | c.£99m |

| Intl revenue | ~30% |

| Bank Rate | 5.25% |

| Cash | £15–20m |

| GB rail journeys | 1.2bn |

Same Document Delivered

Tracsis PESTLE Analysis

The preview shown here is the exact Tracsis PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers.