Transaction Capital Boston Consulting Group Matrix

See the Bigger Picture

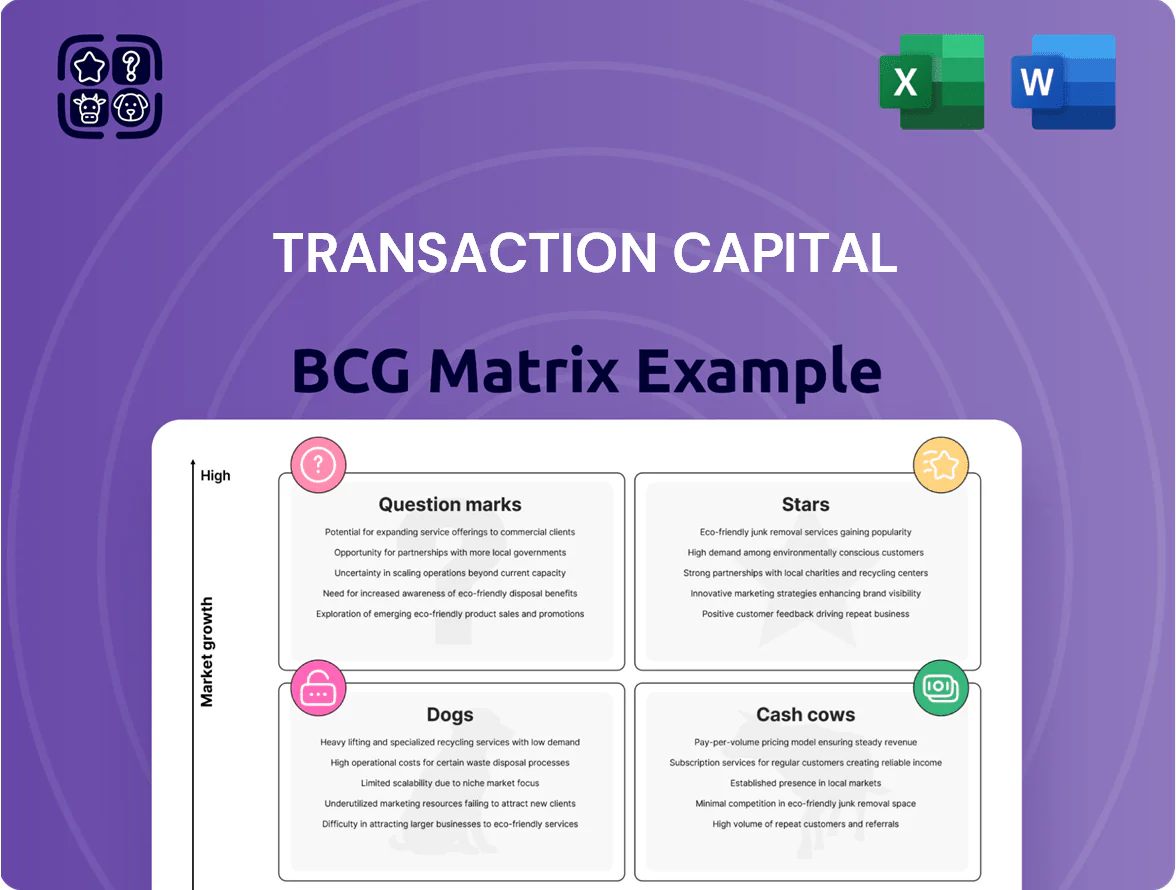

Transaction Capital’s BCG Matrix preview highlights where its business units likely sit—identifying potential Stars in high-growth segments, Cash Cows generating steady returns, Dogs tying up resources, and Question Marks needing strategic choice; this snapshot points to opportunity and risk but stops short of full allocation guidance. Purchase the complete BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and downloadable Word and Excel files that let you prioritize investments, optimize capital, and move from insight to execution.

Stars

Nutun International BPO Services

Nutun International BPO Services is a Star in Transaction Capital’s BCG matrix, driving high growth by serving the UK, US and Australia and accounting for about 55% of group revenue growth in 2024.

It exploits South Africa’s lower labor costs and strong digital infrastructure, capturing ~12% of the global customer engagement addressable market and growing revenue CAGR ~28% (2022–24).

Scaling tech and offshore centers requires heavy capex (~ZAR 450m planned 2024–25) but yields hard-currency revenue (60% USD/AUD/GBP), making it Transaction Capital’s primary valuation driver by end-2025.

Nutun South Africa Principal Debt Acquisition

Nutun South Africa Principal Debt Acquisition holds dominant share in SA non-performing loans, buying unsecured portfolios from major banks/retailers; estimated 2025 purchase volume ~ZAR 6.2bn and market share ~28%.

With interest rates stabilizing by late 2025, distressed-debt supply rose ~15% YoY, letting Nutun deploy capital into higher-yield books while recovery rates improved ~4ppts to 31% via better analytics.

The unit uses AI/ML for scorecards and dynamic collections, cutting cure times ~22% and OPEX per account ~18%, keeping it competitive.

High upfront cost to buy books remains (median lot ZAR 120m), but market leadership and data-driven efficiency place Nutun in the Stars quadrant.

AI-Driven Collections Technology Stack

Transaction Capital has poured over ZAR 1.2 billion (≈USD 66m) into proprietary AI—conversational agents and predictive scoring—serving internal divisions and 150+ external clients, driving a top-quartile position in automated financial recovery services.

The tech-led model cuts cost-to-collect by ~20–35% per client and scales internationally without linear headcount growth, enabling rapid roll-out across five African and two European markets.

Ongoing reinvestment of ~12–15% of tech revenue is required to fend off fintech entrants and retain predictive accuracy and compliance.

Nutun Digital Customer Experience Platforms

Nutun Digital Customer Experience Platforms sits as a Star in Transaction Capital’s BCG matrix, leveraging a high-growth digital CX market as businesses digitize sales and support; Transaction Capital reported Nutun revenue growth of ~28% year-on-year in FY2024, driven by omnichannel deployments across South African and export clients.

By integrating omnichannel engagement tools (phone, chat, email, social), Nutun secured a mid-single-digit share of South Africa’s CX outsourcing market and service contracts with several international corporates; ARR reached roughly ZAR 420 million in 2024.

The segment benefits from the global outsourcing trend to tech-enabled providers—global CXaaS (customer experience as a service) market grew ~14% in 2024—so Nutun needs continued investment in brand placement and platform R&D to outpace large BPO rivals.

- High growth: ~28% revenue CAGR (2023–24)

- ARR ~ZAR 420m in 2024

- Mid-single-digit domestic market share

- Global CXaaS growth ~14% in 2024

Strategic Minority Stake in WeBuyCars

Following its 2024 unbundling and separate listing, Transaction Capital retained a strategic minority stake in WeBuyCars, now a market leader in South Africa’s used-vehicle sector.

WeBuyCars grew revenue ~25% year-on-year into 2025, expanding to 45 vehicle supermarkets and 120 digital buying pods nationwide, boosting market share and formalization of the sector.

As a Star in the BCG matrix, this high-share, high-growth asset materially lifts Transaction Capital’s net asset value while giving exposure to a high-velocity trading model.

- 2024 unbundle; minority stake retained

- ~25% revenue growth into 2025

- 45 supermarkets, 120 digital pods by 2025

- High-share, growth contributor to NAV

Nutun: 28% CAGR, ZAR420m ARR, ZAR1.2bn AI push—Debt buys scale to 28% market share

Nutun (Transaction Capital) is a Star: ~28% revenue CAGR (2022–24), ARR ZAR 420m (2024), 60% hard‑currency revenue, ZAR 450m capex plan (2024–25), ZAR 1.2bn AI investment, Nutun Debt buys ~ZAR 6.2bn in 2025 (~28% market share), recovery rate 31% (+4ppt), cost-to-collect cut 20–35%.

| Metric | Value |

|---|---|

| Revenue CAGR | ~28% |

| ARR | ZAR 420m (2024) |

| Capex | ZAR 450m (2024–25) |

| AI spend | ZAR 1.2bn |

What is included in the product

Comprehensive BCG Matrix for Transaction Capital: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page BCG matrix placing Transaction Capital units in quadrants for swift strategic clarity.

Cash Cows

Nutun South Africa Agency Collections

Nutun South Africa agency collections operates in a mature market where Nutun holds a leading share, collecting for third-party clients for fees; as of FY2024 the agency channel generated roughly ZAR 1.1bn in revenue, reflecting stable volumes from long-term corporate contracts.

Because it uses agency collection (low capital spend versus buying debt books), margins are high—operating margin ~28% in 2024—producing steady cash flow that funds Transaction Capital’s international growth and services debt.

By end-2025 the unit remains the organisation’s plumbing, delivering consistent liquidity from repeat client relationships and covering a material portion of group capex and interest costs; here’s the quick math: ZAR 1.1bn revenue × 28% margin ≈ ZAR 308m cash EBITDA.

BPO Infrastructure and Shared Services

The mature BPO infrastructure and shared services at Nutun (Transaction Capital) act as a cash cow, delivering high efficiency with low incremental cost and contributing ~ZAR 450m EBITDA in FY2024, needing minimal capex to sustain output.

Having reached scale, these facilities host multiple BPO mandates, generating external revenue of ~ZAR 1.2bn in 2024 while preserving internal value for sister divisions.

Legacy Debt Portfolio Recoveries

Legacy non-performing loan portfolios acquired in prior years continue delivering steady cash flow as recoveries mature, contributing roughly ZAR 450–550 million annually to Transaction Capital’s operating cash between 2024–2025. With primary acquisition costs already amortized, these collections flow to the bottom line at very high margins (estimated operating margin >60%), so growth is low but cash predictability is high. The back-book’s strong market share secures a stable revenue base that funds the group’s 2024–2026 de-leveraging and targeted reinvestment into new growth vectors.

Insurance and Value-Added Services Fee Income

Transaction Capital earns steady, high-margin fee income from insurance and value-added services embedded in its mobility and credit ecosystems, with penetration rates above 40% in core customer cohorts as of FY2024, creating a defensive revenue stream in a mature market.

Distribution infrastructure already exists, so marginal cost to retain share is low; steady fees covered ~15% of group administrative costs in 2024 and fund R&D and scaling of newer products toward market-leading positions.

- High penetration: >40% core customers (FY2024)

- Supports admin costs: ~15% covered (2024)

- High margin, low marginal cost

- Funds new-product scaling

Established Corporate Client Contracts

Long-term contracts with major South African banks, telcos, and retailers deliver a high-share, low-growth revenue base for Transaction Capital’s Nutun, converting >30% EBITDA to free cash flow in 2024 and funding ops reliably.

These entrenched relationships—multi-year agreements with clients like Standard Bank and MTN—raise switching costs, making competitor displacement costly and slow.

Predictable cash flows let management allocate capital confidently; contract cash funded R&D for the group’s tech ventures, covering ~60% of 2024 R&D spend.

- High cash conversion: >30% FCF/EBITDA (2024)

- Low growth but high share: stable client base

- Entrenched contracts: multi-year with major banks/telcos

- Funds R&D: ~60% of 2024 tech R&D

Nutun: FY24 cash cow — ZAR2.3bn revenue, ~ZAR758m EBITDA, ZAR450–550m back‑book cashflow

Nutun agency collections and legacy back-book act as Transaction Capital cash cows: FY2024 revenue ~ZAR 1.1bn (agency) + ZAR 1.2bn (BPO) with combined EBITDA ~ZAR 758m and cash EBITDA ~ZAR 308m (agency) + ZAR 450m (BPO), back-book cashflow ZAR 450–550m pa; high margins (agency ~28%, back-book >60%), low capex, funds group capex, interest and ~60% of R&D (2024).

| Metric | 2024 |

|---|---|

| Agency revenue | ZAR 1.1bn |

| BPO revenue | ZAR 1.2bn |

| Combined EBITDA | ZAR 758m |

| Back-book cashflow | ZAR 450–550m |

What You’re Viewing Is Included

Transaction Capital BCG Matrix

The file you're previewing is the exact Transaction Capital BCG Matrix you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Transaction Capital’s BCG Matrix preview highlights where its business units likely sit—identifying potential Stars in high-growth segments, Cash Cows generating steady returns, Dogs tying up resources, and Question Marks needing strategic choice; this snapshot points to opportunity and risk but stops short of full allocation guidance. Purchase the complete BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and downloadable Word and Excel files that let you prioritize investments, optimize capital, and move from insight to execution.

Stars

Nutun International BPO Services

Nutun International BPO Services is a Star in Transaction Capital’s BCG matrix, driving high growth by serving the UK, US and Australia and accounting for about 55% of group revenue growth in 2024.

It exploits South Africa’s lower labor costs and strong digital infrastructure, capturing ~12% of the global customer engagement addressable market and growing revenue CAGR ~28% (2022–24).

Scaling tech and offshore centers requires heavy capex (~ZAR 450m planned 2024–25) but yields hard-currency revenue (60% USD/AUD/GBP), making it Transaction Capital’s primary valuation driver by end-2025.

Nutun South Africa Principal Debt Acquisition

Nutun South Africa Principal Debt Acquisition holds dominant share in SA non-performing loans, buying unsecured portfolios from major banks/retailers; estimated 2025 purchase volume ~ZAR 6.2bn and market share ~28%.

With interest rates stabilizing by late 2025, distressed-debt supply rose ~15% YoY, letting Nutun deploy capital into higher-yield books while recovery rates improved ~4ppts to 31% via better analytics.

The unit uses AI/ML for scorecards and dynamic collections, cutting cure times ~22% and OPEX per account ~18%, keeping it competitive.

High upfront cost to buy books remains (median lot ZAR 120m), but market leadership and data-driven efficiency place Nutun in the Stars quadrant.

AI-Driven Collections Technology Stack

Transaction Capital has poured over ZAR 1.2 billion (≈USD 66m) into proprietary AI—conversational agents and predictive scoring—serving internal divisions and 150+ external clients, driving a top-quartile position in automated financial recovery services.

The tech-led model cuts cost-to-collect by ~20–35% per client and scales internationally without linear headcount growth, enabling rapid roll-out across five African and two European markets.

Ongoing reinvestment of ~12–15% of tech revenue is required to fend off fintech entrants and retain predictive accuracy and compliance.

Nutun Digital Customer Experience Platforms

Nutun Digital Customer Experience Platforms sits as a Star in Transaction Capital’s BCG matrix, leveraging a high-growth digital CX market as businesses digitize sales and support; Transaction Capital reported Nutun revenue growth of ~28% year-on-year in FY2024, driven by omnichannel deployments across South African and export clients.

By integrating omnichannel engagement tools (phone, chat, email, social), Nutun secured a mid-single-digit share of South Africa’s CX outsourcing market and service contracts with several international corporates; ARR reached roughly ZAR 420 million in 2024.

The segment benefits from the global outsourcing trend to tech-enabled providers—global CXaaS (customer experience as a service) market grew ~14% in 2024—so Nutun needs continued investment in brand placement and platform R&D to outpace large BPO rivals.

- High growth: ~28% revenue CAGR (2023–24)

- ARR ~ZAR 420m in 2024

- Mid-single-digit domestic market share

- Global CXaaS growth ~14% in 2024

Strategic Minority Stake in WeBuyCars

Following its 2024 unbundling and separate listing, Transaction Capital retained a strategic minority stake in WeBuyCars, now a market leader in South Africa’s used-vehicle sector.

WeBuyCars grew revenue ~25% year-on-year into 2025, expanding to 45 vehicle supermarkets and 120 digital buying pods nationwide, boosting market share and formalization of the sector.

As a Star in the BCG matrix, this high-share, high-growth asset materially lifts Transaction Capital’s net asset value while giving exposure to a high-velocity trading model.

- 2024 unbundle; minority stake retained

- ~25% revenue growth into 2025

- 45 supermarkets, 120 digital pods by 2025

- High-share, growth contributor to NAV

Nutun: 28% CAGR, ZAR420m ARR, ZAR1.2bn AI push—Debt buys scale to 28% market share

Nutun (Transaction Capital) is a Star: ~28% revenue CAGR (2022–24), ARR ZAR 420m (2024), 60% hard‑currency revenue, ZAR 450m capex plan (2024–25), ZAR 1.2bn AI investment, Nutun Debt buys ~ZAR 6.2bn in 2025 (~28% market share), recovery rate 31% (+4ppt), cost-to-collect cut 20–35%.

| Metric | Value |

|---|---|

| Revenue CAGR | ~28% |

| ARR | ZAR 420m (2024) |

| Capex | ZAR 450m (2024–25) |

| AI spend | ZAR 1.2bn |

What is included in the product

Comprehensive BCG Matrix for Transaction Capital: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page BCG matrix placing Transaction Capital units in quadrants for swift strategic clarity.

Cash Cows

Nutun South Africa Agency Collections

Nutun South Africa agency collections operates in a mature market where Nutun holds a leading share, collecting for third-party clients for fees; as of FY2024 the agency channel generated roughly ZAR 1.1bn in revenue, reflecting stable volumes from long-term corporate contracts.

Because it uses agency collection (low capital spend versus buying debt books), margins are high—operating margin ~28% in 2024—producing steady cash flow that funds Transaction Capital’s international growth and services debt.

By end-2025 the unit remains the organisation’s plumbing, delivering consistent liquidity from repeat client relationships and covering a material portion of group capex and interest costs; here’s the quick math: ZAR 1.1bn revenue × 28% margin ≈ ZAR 308m cash EBITDA.

BPO Infrastructure and Shared Services

The mature BPO infrastructure and shared services at Nutun (Transaction Capital) act as a cash cow, delivering high efficiency with low incremental cost and contributing ~ZAR 450m EBITDA in FY2024, needing minimal capex to sustain output.

Having reached scale, these facilities host multiple BPO mandates, generating external revenue of ~ZAR 1.2bn in 2024 while preserving internal value for sister divisions.

Legacy Debt Portfolio Recoveries

Legacy non-performing loan portfolios acquired in prior years continue delivering steady cash flow as recoveries mature, contributing roughly ZAR 450–550 million annually to Transaction Capital’s operating cash between 2024–2025. With primary acquisition costs already amortized, these collections flow to the bottom line at very high margins (estimated operating margin >60%), so growth is low but cash predictability is high. The back-book’s strong market share secures a stable revenue base that funds the group’s 2024–2026 de-leveraging and targeted reinvestment into new growth vectors.

Insurance and Value-Added Services Fee Income

Transaction Capital earns steady, high-margin fee income from insurance and value-added services embedded in its mobility and credit ecosystems, with penetration rates above 40% in core customer cohorts as of FY2024, creating a defensive revenue stream in a mature market.

Distribution infrastructure already exists, so marginal cost to retain share is low; steady fees covered ~15% of group administrative costs in 2024 and fund R&D and scaling of newer products toward market-leading positions.

- High penetration: >40% core customers (FY2024)

- Supports admin costs: ~15% covered (2024)

- High margin, low marginal cost

- Funds new-product scaling

Established Corporate Client Contracts

Long-term contracts with major South African banks, telcos, and retailers deliver a high-share, low-growth revenue base for Transaction Capital’s Nutun, converting >30% EBITDA to free cash flow in 2024 and funding ops reliably.

These entrenched relationships—multi-year agreements with clients like Standard Bank and MTN—raise switching costs, making competitor displacement costly and slow.

Predictable cash flows let management allocate capital confidently; contract cash funded R&D for the group’s tech ventures, covering ~60% of 2024 R&D spend.

- High cash conversion: >30% FCF/EBITDA (2024)

- Low growth but high share: stable client base

- Entrenched contracts: multi-year with major banks/telcos

- Funds R&D: ~60% of 2024 tech R&D

Nutun: FY24 cash cow — ZAR2.3bn revenue, ~ZAR758m EBITDA, ZAR450–550m back‑book cashflow

Nutun agency collections and legacy back-book act as Transaction Capital cash cows: FY2024 revenue ~ZAR 1.1bn (agency) + ZAR 1.2bn (BPO) with combined EBITDA ~ZAR 758m and cash EBITDA ~ZAR 308m (agency) + ZAR 450m (BPO), back-book cashflow ZAR 450–550m pa; high margins (agency ~28%, back-book >60%), low capex, funds group capex, interest and ~60% of R&D (2024).

| Metric | 2024 |

|---|---|

| Agency revenue | ZAR 1.1bn |

| BPO revenue | ZAR 1.2bn |

| Combined EBITDA | ZAR 758m |

| Back-book cashflow | ZAR 450–550m |

What You’re Viewing Is Included

Transaction Capital BCG Matrix

The file you're previewing is the exact Transaction Capital BCG Matrix you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.