TransAlta Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

TransAlta navigates a complex energy landscape, where the bargaining power of buyers and the threat of substitutes significantly shape its profitability. Understanding these forces is crucial for any stakeholder looking to grasp the company's competitive position.

The complete report reveals the real forces shaping TransAlta’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on specialized equipment providers

TransAlta's reliance on specialized equipment for its diverse energy portfolio, including hydro turbines, wind generators, and solar panels, highlights a key aspect of supplier bargaining power. For instance, the global market for high-efficiency wind turbines is dominated by a few major manufacturers. This concentration means these suppliers can dictate terms, influencing TransAlta's capital expenditures and project timelines.

Fuel supply dynamics (Natural Gas)

As TransAlta continues its portfolio transition, natural gas remains a vital fuel for its thermal power generation. The company's reliance on this commodity means that the pricing and availability of natural gas significantly influence its operational costs.

Suppliers of natural gas wield considerable bargaining power due to market volatility and geopolitical events that can impact supply. For instance, in early 2024, natural gas prices experienced fluctuations influenced by global demand and supply chain disruptions, directly affecting TransAlta's input costs.

This dependence on a fluctuating commodity market creates a direct link between natural gas supplier leverage and TransAlta's profitability. The ability of suppliers to dictate terms or adjust prices can squeeze margins for TransAlta if it cannot pass these increased costs onto consumers.

Access to skilled labor and engineering expertise

The highly technical nature of power generation, from developing and operating diverse energy assets to their ongoing maintenance, demands a very specific and skilled workforce. This means companies like TransAlta rely on a pool of qualified engineers, specialized technicians, and experienced project managers.

A shortage in this specialized labor, which has been a persistent concern across many industrial sectors, can significantly drive up labor costs for TransAlta. Furthermore, such scarcity can cause unwelcome delays in crucial projects, impacting operational efficiency and expansion plans.

This specialized talent pool, therefore, functions much like a powerful supplier. Their unique skills and the limited availability of such expertise grant them considerable bargaining power, influencing wages and project timelines for TransAlta and its peers in the energy sector.

Financing and capital providers

The energy sector, including companies like TransAlta, is inherently capital-intensive. This means significant financial resources are needed for everything from building new power plants to upgrading existing infrastructure and adopting cleaner technologies. For instance, a new renewable energy project can easily cost hundreds of millions, if not billions, of dollars.

TransAlta’s ability to fund its operations and growth hinges on its access to capital from various sources. These include traditional banks, large institutional investors like pension funds and asset managers, and other financial institutions. These entities provide the crucial debt and equity financing that allows TransAlta to undertake major projects and maintain its asset base.

The bargaining power of these financing and capital providers is substantial. They can influence the terms and conditions of loans and investments based on factors like prevailing interest rates, TransAlta's financial health, and overall investor sentiment towards the energy industry. For 2024, interest rates have remained a key consideration, potentially increasing the cost of borrowing for capital-intensive projects.

- Capital Intensity: The energy sector demands high upfront investment for infrastructure and technology.

- Financing Sources: TransAlta relies on banks, institutional investors, and other capital markets.

- Influence of Providers: Terms of financing, including interest rates and covenants, are set by capital providers.

- Impact on Strategy: Favorable or unfavorable financing terms directly affect TransAlta's growth and investment decisions.

Technology and software vendors

Technology and software vendors hold significant bargaining power over companies like TransAlta, especially those managing complex, diversified power portfolios. The need for sophisticated systems to optimize generation, energy trading, and grid integration means specialized software is critical. Vendors with proprietary or highly integrated platforms can therefore dictate terms and pricing, as finding comparable alternatives can be challenging and costly.

For instance, the global market for grid management software was projected to reach approximately $15.7 billion in 2024, indicating a substantial and growing demand for these specialized solutions. This reliance on advanced technology, coupled with the substantial switching costs involved in migrating to new software systems, further solidifies the suppliers' leverage. TransAlta's investment in digital transformation, as highlighted in its 2023 annual report, underscores its dependence on these technology partners.

- High Switching Costs: Migrating complex power management software can involve significant data migration, retraining personnel, and potential operational disruptions, making it expensive and time-consuming for TransAlta to change vendors.

- Proprietary Systems: Vendors offering unique, integrated platforms that are essential for optimizing TransAlta's diverse generation assets (e.g., wind, solar, hydro, natural gas) can command premium pricing due to the lack of direct substitutes.

- Specialized Expertise: The deep technical knowledge and industry-specific understanding required to develop and maintain these critical software solutions mean a limited pool of highly capable vendors, increasing their bargaining power.

Supplier Power: Shaping Energy Project Costs and Timelines

TransAlta's reliance on specialized equipment for its diverse energy portfolio, including hydro turbines, wind generators, and solar panels, highlights a key aspect of supplier bargaining power. For instance, the global market for high-efficiency wind turbines is dominated by a few major manufacturers. This concentration means these suppliers can dictate terms, influencing TransAlta's capital expenditures and project timelines.

What is included in the product

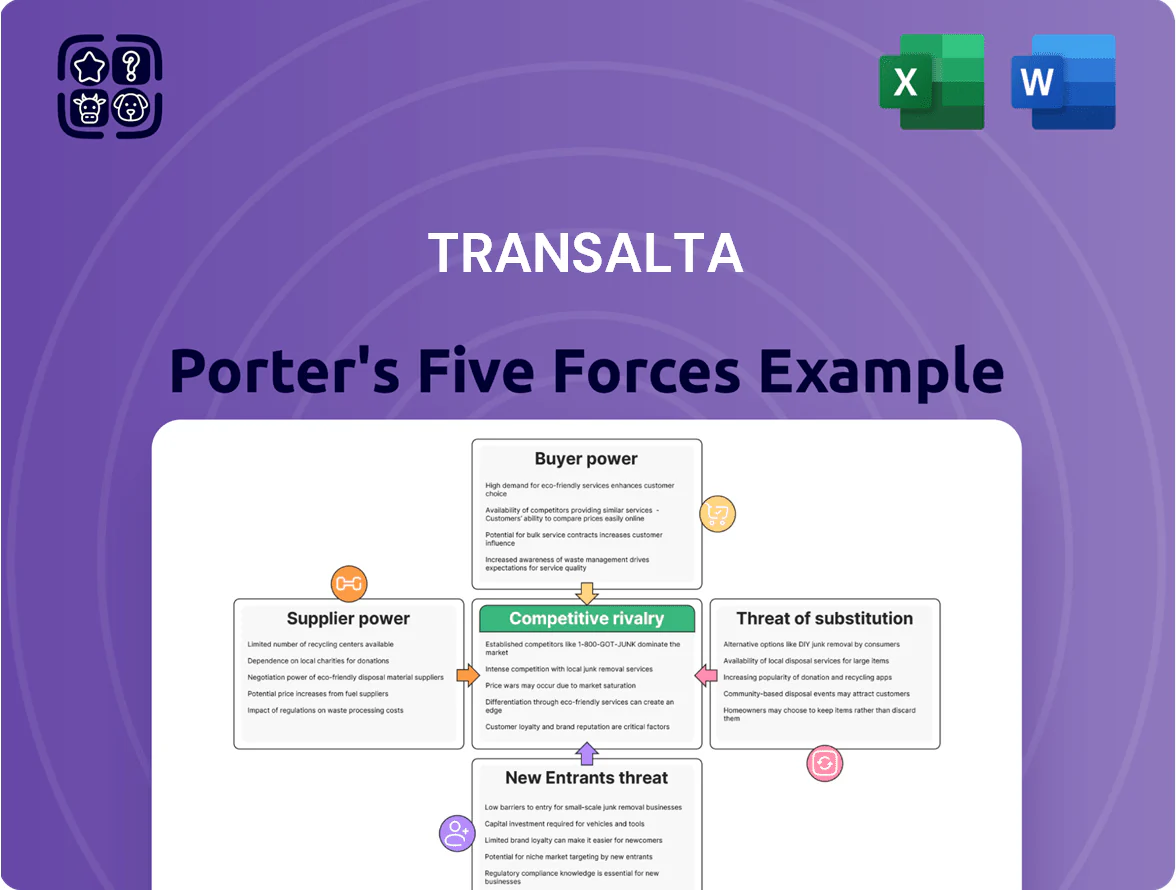

This analysis of TransAlta's competitive environment examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the energy sector.

Instantly understand strategic pressure with a powerful spider/radar chart visualizing TransAlta's competitive landscape.

Swap in your own data, labels, and notes to reflect current business conditions and alleviate uncertainty.

Customers Bargaining Power

Influence of large industrial and commercial customers

TransAlta's large industrial and commercial customers hold significant bargaining power. These clients, representing substantial electricity demand, can leverage their volume to negotiate better pricing and service terms. For instance, a major manufacturing plant consuming a significant portion of a regional grid's output has the ability to influence TransAlta's pricing strategies.

Wholesale market dynamics and price sensitivity

In Alberta's wholesale electricity market, TransAlta faces customers who are acutely sensitive to price. This is largely because electricity has become a commodity, meaning buyers can readily switch providers based on cost. This price sensitivity is a significant factor in their bargaining power.

The market conditions in Alberta highlight this dynamic. With new renewable energy projects and additional gas facilities coming online, the supply of electricity has increased, leading to a softening of power prices. This oversupply environment naturally empowers customers to negotiate for more competitive rates, as they have more options available.

Availability of alternative power sources for customers

Customers, particularly large industrial users, are increasingly exploring and adopting alternative power sources. This includes significant investments in self-generation, such as rooftop solar installations, and direct purchasing agreements with independent renewable energy developers. For instance, by 2024, corporate renewable energy Power Purchase Agreements (PPAs) in North America saw substantial growth, with companies securing gigawatts of clean energy, directly reducing their reliance on traditional utility providers.

The growing viability and accessibility of these alternatives directly diminish customer dependence on established utility-scale generators like TransAlta. As more customers gain the ability to generate their own power or source it from diverse, often cheaper, options, their leverage in negotiations with incumbent suppliers naturally increases.

This diversified access to energy significantly bolsters customer bargaining power. When customers have readily available and cost-effective alternatives, they are less compelled to accept terms dictated by a single provider, forcing suppliers to compete more aggressively on price and service.

Low customer switching costs in competitive markets

In deregulated electricity markets, customers often face low switching costs, allowing them to easily move to a new provider. This ease of transition empowers them by providing significant leverage to seek better pricing or service terms from their current or potential electricity suppliers.

This low switching cost environment directly enhances the bargaining power of customers in the energy sector. For instance, in many North American deregulated markets, the process to switch electricity providers can be completed within a few weeks with minimal administrative hassle for the consumer.

- Low Switching Costs: Customers can switch electricity providers with minimal effort and expense.

- Competitive Pressure: This forces providers to compete on price and service to retain or attract customers.

- Customer Leverage: Consumers can readily demand better terms, impacting provider profitability.

Regulatory frameworks favoring consumer choice

Regulatory frameworks increasingly favor consumer choice in the electricity sector, directly impacting TransAlta's customer bargaining power. For instance, by 2024, many jurisdictions have seen the unbundling of energy services, allowing consumers to select their electricity providers. This shift, driven by government policies aimed at fostering competition, gives customers more leverage to negotiate prices or switch suppliers if they find better deals.

These evolving regulations empower customers by increasing transparency in pricing structures and offering a wider array of service options. For example, in Alberta, a key market for TransAlta, the retail electricity market has been open for years, allowing consumers to choose from various energy retailers. This competitive environment means customers can compare offers, driving down prices and enhancing their ability to bargain.

- Increased Competition: Regulatory frameworks promoting consumer choice lead to more electricity retailers entering the market.

- Price Transparency: Policies mandate clearer pricing information, enabling customers to easily compare offers.

- Supplier Switching: Consumers have greater freedom to switch providers, forcing generators to offer competitive rates.

- Alberta's Retail Market: By 2024, Alberta's deregulated market exemplifies how regulatory structures can amplify customer bargaining power.

Customer Power: Negotiating Electricity in a Competitive Market

TransAlta's customers, especially large industrial and commercial entities, wield considerable bargaining power due to their substantial electricity consumption. This allows them to negotiate favorable pricing and service conditions, a trend amplified by Alberta's competitive wholesale market where electricity is a commodity. The increasing availability of alternative energy sources and the ease of switching providers further bolster customer leverage.

| Factor | Impact on TransAlta | Supporting Data (2024) |

|---|---|---|

| Customer Volume | High bargaining power for large consumers | Major industrial clients represent significant load, enabling price negotiations. |

| Price Sensitivity | Customers readily switch for lower costs | Commoditized nature of electricity in Alberta drives price-driven decisions. |

| Alternative Sources | Reduced reliance on TransAlta | Growth in corporate PPAs for renewables, securing gigawatts of clean energy. |

| Switching Costs | Ease of changing providers | Minimal administrative hassle for switching in deregulated North American markets. |

Preview Before You Purchase

TransAlta Porter's Five Forces Analysis

This preview displays the complete TransAlta Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. You're looking at the actual document; once your purchase is complete, you'll gain instant access to this exact, professionally formatted file. This means you'll receive the full, ready-to-use analysis without any alterations or missing sections.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

TransAlta navigates a complex energy landscape, where the bargaining power of buyers and the threat of substitutes significantly shape its profitability. Understanding these forces is crucial for any stakeholder looking to grasp the company's competitive position.

The complete report reveals the real forces shaping TransAlta’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on specialized equipment providers

TransAlta's reliance on specialized equipment for its diverse energy portfolio, including hydro turbines, wind generators, and solar panels, highlights a key aspect of supplier bargaining power. For instance, the global market for high-efficiency wind turbines is dominated by a few major manufacturers. This concentration means these suppliers can dictate terms, influencing TransAlta's capital expenditures and project timelines.

Fuel supply dynamics (Natural Gas)

As TransAlta continues its portfolio transition, natural gas remains a vital fuel for its thermal power generation. The company's reliance on this commodity means that the pricing and availability of natural gas significantly influence its operational costs.

Suppliers of natural gas wield considerable bargaining power due to market volatility and geopolitical events that can impact supply. For instance, in early 2024, natural gas prices experienced fluctuations influenced by global demand and supply chain disruptions, directly affecting TransAlta's input costs.

This dependence on a fluctuating commodity market creates a direct link between natural gas supplier leverage and TransAlta's profitability. The ability of suppliers to dictate terms or adjust prices can squeeze margins for TransAlta if it cannot pass these increased costs onto consumers.

Access to skilled labor and engineering expertise

The highly technical nature of power generation, from developing and operating diverse energy assets to their ongoing maintenance, demands a very specific and skilled workforce. This means companies like TransAlta rely on a pool of qualified engineers, specialized technicians, and experienced project managers.

A shortage in this specialized labor, which has been a persistent concern across many industrial sectors, can significantly drive up labor costs for TransAlta. Furthermore, such scarcity can cause unwelcome delays in crucial projects, impacting operational efficiency and expansion plans.

This specialized talent pool, therefore, functions much like a powerful supplier. Their unique skills and the limited availability of such expertise grant them considerable bargaining power, influencing wages and project timelines for TransAlta and its peers in the energy sector.

Financing and capital providers

The energy sector, including companies like TransAlta, is inherently capital-intensive. This means significant financial resources are needed for everything from building new power plants to upgrading existing infrastructure and adopting cleaner technologies. For instance, a new renewable energy project can easily cost hundreds of millions, if not billions, of dollars.

TransAlta’s ability to fund its operations and growth hinges on its access to capital from various sources. These include traditional banks, large institutional investors like pension funds and asset managers, and other financial institutions. These entities provide the crucial debt and equity financing that allows TransAlta to undertake major projects and maintain its asset base.

The bargaining power of these financing and capital providers is substantial. They can influence the terms and conditions of loans and investments based on factors like prevailing interest rates, TransAlta's financial health, and overall investor sentiment towards the energy industry. For 2024, interest rates have remained a key consideration, potentially increasing the cost of borrowing for capital-intensive projects.

- Capital Intensity: The energy sector demands high upfront investment for infrastructure and technology.

- Financing Sources: TransAlta relies on banks, institutional investors, and other capital markets.

- Influence of Providers: Terms of financing, including interest rates and covenants, are set by capital providers.

- Impact on Strategy: Favorable or unfavorable financing terms directly affect TransAlta's growth and investment decisions.

Technology and software vendors

Technology and software vendors hold significant bargaining power over companies like TransAlta, especially those managing complex, diversified power portfolios. The need for sophisticated systems to optimize generation, energy trading, and grid integration means specialized software is critical. Vendors with proprietary or highly integrated platforms can therefore dictate terms and pricing, as finding comparable alternatives can be challenging and costly.

For instance, the global market for grid management software was projected to reach approximately $15.7 billion in 2024, indicating a substantial and growing demand for these specialized solutions. This reliance on advanced technology, coupled with the substantial switching costs involved in migrating to new software systems, further solidifies the suppliers' leverage. TransAlta's investment in digital transformation, as highlighted in its 2023 annual report, underscores its dependence on these technology partners.

- High Switching Costs: Migrating complex power management software can involve significant data migration, retraining personnel, and potential operational disruptions, making it expensive and time-consuming for TransAlta to change vendors.

- Proprietary Systems: Vendors offering unique, integrated platforms that are essential for optimizing TransAlta's diverse generation assets (e.g., wind, solar, hydro, natural gas) can command premium pricing due to the lack of direct substitutes.

- Specialized Expertise: The deep technical knowledge and industry-specific understanding required to develop and maintain these critical software solutions mean a limited pool of highly capable vendors, increasing their bargaining power.

Supplier Power: Shaping Energy Project Costs and Timelines

TransAlta's reliance on specialized equipment for its diverse energy portfolio, including hydro turbines, wind generators, and solar panels, highlights a key aspect of supplier bargaining power. For instance, the global market for high-efficiency wind turbines is dominated by a few major manufacturers. This concentration means these suppliers can dictate terms, influencing TransAlta's capital expenditures and project timelines.

What is included in the product

This analysis of TransAlta's competitive environment examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the energy sector.

Instantly understand strategic pressure with a powerful spider/radar chart visualizing TransAlta's competitive landscape.

Swap in your own data, labels, and notes to reflect current business conditions and alleviate uncertainty.

Customers Bargaining Power

Influence of large industrial and commercial customers

TransAlta's large industrial and commercial customers hold significant bargaining power. These clients, representing substantial electricity demand, can leverage their volume to negotiate better pricing and service terms. For instance, a major manufacturing plant consuming a significant portion of a regional grid's output has the ability to influence TransAlta's pricing strategies.

Wholesale market dynamics and price sensitivity

In Alberta's wholesale electricity market, TransAlta faces customers who are acutely sensitive to price. This is largely because electricity has become a commodity, meaning buyers can readily switch providers based on cost. This price sensitivity is a significant factor in their bargaining power.

The market conditions in Alberta highlight this dynamic. With new renewable energy projects and additional gas facilities coming online, the supply of electricity has increased, leading to a softening of power prices. This oversupply environment naturally empowers customers to negotiate for more competitive rates, as they have more options available.

Availability of alternative power sources for customers

Customers, particularly large industrial users, are increasingly exploring and adopting alternative power sources. This includes significant investments in self-generation, such as rooftop solar installations, and direct purchasing agreements with independent renewable energy developers. For instance, by 2024, corporate renewable energy Power Purchase Agreements (PPAs) in North America saw substantial growth, with companies securing gigawatts of clean energy, directly reducing their reliance on traditional utility providers.

The growing viability and accessibility of these alternatives directly diminish customer dependence on established utility-scale generators like TransAlta. As more customers gain the ability to generate their own power or source it from diverse, often cheaper, options, their leverage in negotiations with incumbent suppliers naturally increases.

This diversified access to energy significantly bolsters customer bargaining power. When customers have readily available and cost-effective alternatives, they are less compelled to accept terms dictated by a single provider, forcing suppliers to compete more aggressively on price and service.

Low customer switching costs in competitive markets

In deregulated electricity markets, customers often face low switching costs, allowing them to easily move to a new provider. This ease of transition empowers them by providing significant leverage to seek better pricing or service terms from their current or potential electricity suppliers.

This low switching cost environment directly enhances the bargaining power of customers in the energy sector. For instance, in many North American deregulated markets, the process to switch electricity providers can be completed within a few weeks with minimal administrative hassle for the consumer.

- Low Switching Costs: Customers can switch electricity providers with minimal effort and expense.

- Competitive Pressure: This forces providers to compete on price and service to retain or attract customers.

- Customer Leverage: Consumers can readily demand better terms, impacting provider profitability.

Regulatory frameworks favoring consumer choice

Regulatory frameworks increasingly favor consumer choice in the electricity sector, directly impacting TransAlta's customer bargaining power. For instance, by 2024, many jurisdictions have seen the unbundling of energy services, allowing consumers to select their electricity providers. This shift, driven by government policies aimed at fostering competition, gives customers more leverage to negotiate prices or switch suppliers if they find better deals.

These evolving regulations empower customers by increasing transparency in pricing structures and offering a wider array of service options. For example, in Alberta, a key market for TransAlta, the retail electricity market has been open for years, allowing consumers to choose from various energy retailers. This competitive environment means customers can compare offers, driving down prices and enhancing their ability to bargain.

- Increased Competition: Regulatory frameworks promoting consumer choice lead to more electricity retailers entering the market.

- Price Transparency: Policies mandate clearer pricing information, enabling customers to easily compare offers.

- Supplier Switching: Consumers have greater freedom to switch providers, forcing generators to offer competitive rates.

- Alberta's Retail Market: By 2024, Alberta's deregulated market exemplifies how regulatory structures can amplify customer bargaining power.

Customer Power: Negotiating Electricity in a Competitive Market

TransAlta's customers, especially large industrial and commercial entities, wield considerable bargaining power due to their substantial electricity consumption. This allows them to negotiate favorable pricing and service conditions, a trend amplified by Alberta's competitive wholesale market where electricity is a commodity. The increasing availability of alternative energy sources and the ease of switching providers further bolster customer leverage.

| Factor | Impact on TransAlta | Supporting Data (2024) |

|---|---|---|

| Customer Volume | High bargaining power for large consumers | Major industrial clients represent significant load, enabling price negotiations. |

| Price Sensitivity | Customers readily switch for lower costs | Commoditized nature of electricity in Alberta drives price-driven decisions. |

| Alternative Sources | Reduced reliance on TransAlta | Growth in corporate PPAs for renewables, securing gigawatts of clean energy. |

| Switching Costs | Ease of changing providers | Minimal administrative hassle for switching in deregulated North American markets. |

Preview Before You Purchase

TransAlta Porter's Five Forces Analysis

This preview displays the complete TransAlta Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. You're looking at the actual document; once your purchase is complete, you'll gain instant access to this exact, professionally formatted file. This means you'll receive the full, ready-to-use analysis without any alterations or missing sections.