Transcat PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political, economic, and technological forces are reshaping Transcat’s prospects with our concise PESTLE snapshot—designed to inform investors, strategists, and analysts. Buy the full PESTLE to unlock detailed risk assessments, market implications, and actionable recommendations you can use in boardrooms or investment memos. Download now for immediate, editable insights.

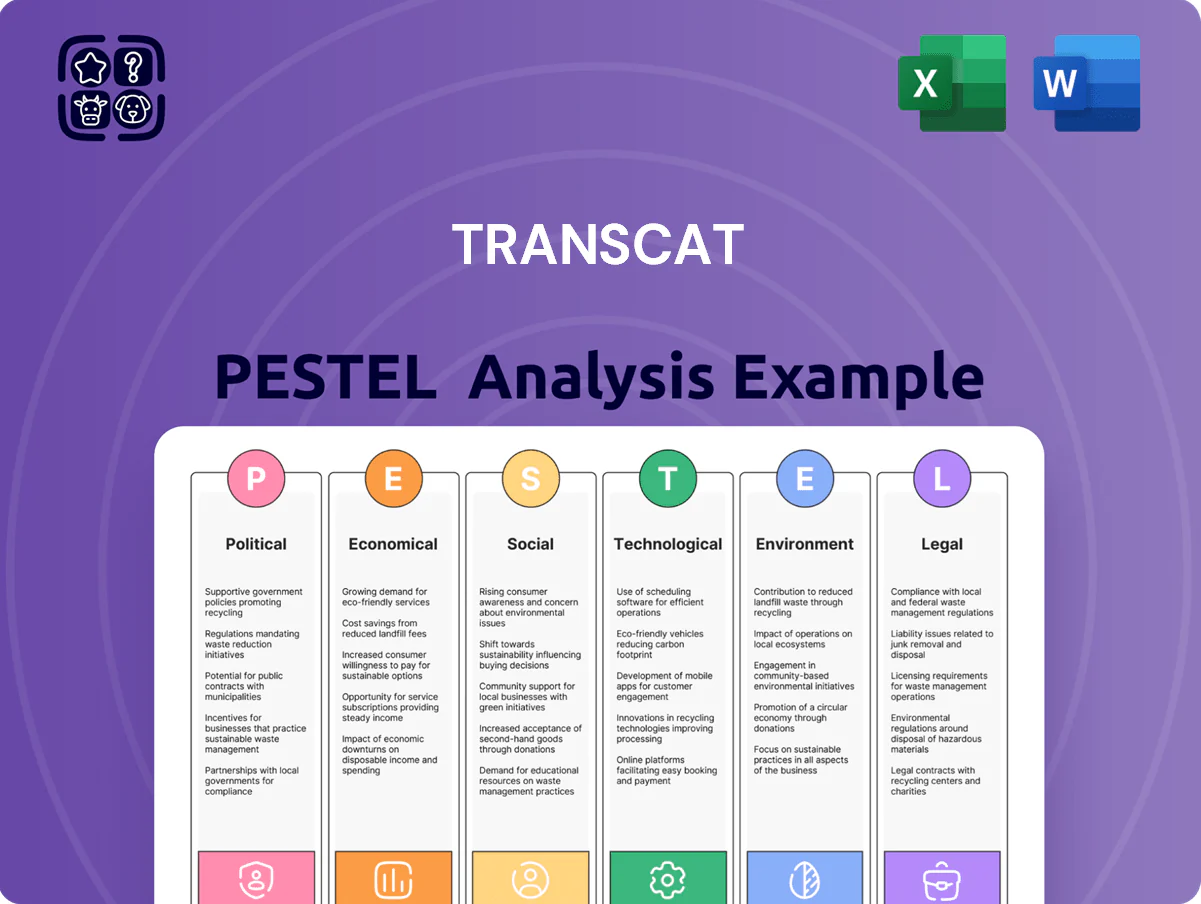

Political factors

Impact of US Trade and Tariff Policies

Shifts in US trade policies through late 2025—including 10–25% tariffs on select electronics imports and $50B in domestic production incentives—have raised Transcat Distribution's imported instrument costs by an estimated 6–9%, pressuring gross margins reported at ~32% in FY2024.

Government Spending in Aerospace and Defense

Transcat’s significant footprint in aerospace and defense ties revenue exposure to US federal budgets, where FY2025 Department of Defense discretionary funding was about $842 billion and NASA enacted budget was $27.2 billion, driving demand for calibration and specialized instrumentation. Legislative choices on defense modernization and space initiatives—like continued investment in hypersonics and Artemis—directly increase procurement of precision services. Sudden shifts in contracts or geopolitical priorities can cause quarterly service-volume volatility in these regulated sectors.

Regulatory Oversight and FDA Funding

The political climate around healthcare regulation drives Transcat's Life Sciences segment; in FY2024 FDA received about $6.6B in appropriations, up ~9% from FY2021, which can increase inspection frequency and demand for accredited calibration and validation services.

Focus on Industrial Reshoring and Infrastructure

Political momentum for reshoring surged through 2025, with US incentives allocating over $200 billion to semiconductor and battery supply chains, driving demand for Transcat’s precision instruments and calibration services as new plants open domestically.

Domestic manufacturing growth—US semiconductor fab capacity up ~30% YoY in 2024–25—supports recurring calibration cycles and equipment sales, positioning Transcat to capture higher lifetime service revenue.

- Federal incentives >$200B for chips/batteries

- Semiconductor fab capacity +30% YoY (2024–25)

- Increased domestic facilities → more equipment + recurring calibration

Corporate Tax Policy and Investment Incentives

- R&D credit boosts capex propensity 10–15%

- Depreciation incentives drove 8–12% sales/rental gains (2024)

- Restrictive tax settings shift spend from Distribution to Service (2025 observations)

Tariffs Pressure Margins; Defense, FDA, Reshoring Fuel Calibration Revenue Boom

Political shifts (tariffs 10–25% on electronics, $50B domestic incentives) raised Transcat’s import costs ~6–9%, pressuring FY2024 gross margin (~32%); defense/NASA budgets ($842B DoD, $27.2B NASA FY2025) and FDA funding ($6.6B FY2024) drive service demand; >$200B reshoring incentives and +30% semiconductor fab capacity (2024–25) boost recurring calibration revenue.

| Metric | Value |

|---|---|

| Import cost impact | +6–9% |

| Gross margin FY2024 | ~32% |

| DoD budget FY2025 | $842B |

| NASA FY2025 | $27.2B |

| FDA FY2024 | $6.6B |

| Reshoring incentives | >$200B |

| Semiconductor fab capacity | +30% (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely affect Transcat across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and multiple sub-points tailored to the company's industry and region to inform strategy, funding, and scenario planning.

Provides a concise, visually segmented PESTLE summary for Transcat that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and align on strategic decisions.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, a higher-rate backdrop—US fed funds around 5.25–5.50% in 2024–25—raises Transcat’s cost of debt, squeezing margins on acquisitions of smaller calibration labs and potentially slowing its aggressive M&A cadence versus prior years.

Elevated borrowing costs increase acquisition financing expense and could reduce deal volume; Transcat’s capital-intensive Distribution sales mix also faces demand shifts as customers defer purchases and favor rental/leasing options, pressuring equipment sales growth.

Industrial Production and GDP Growth

Transcat's performance tracks industrial output and GDP growth; US industrial production fell 0.1% year-over-year in 2025 while real GDP expanded 2.1% in 2024, constraining capital spending in some sectors.

Demand from biotechnology, energy, and advanced manufacturing—where US biotech funding rose 8% in 2024 and clean energy investment hit $300 billion globally in 2024—supports instrument utilization and calibration frequency.

A sustained slowdown in industrial production, which saw global manufacturing PMI average 49.8 in 2025 H1, would likely lower calibration cycles and postpone purchases across Transcat's equipment portfolio.

Labor Market Dynamics and Wage Inflation

The market for highly skilled calibration technicians remained tight at the close of 2025, with U.S. vacancy rates for skilled trades near 4.2% and average wage growth in technical services about 4.8% year-over-year, putting upward pressure on Transcat’s labor costs.

Transcat must balance competitive compensation—market data suggest premium pay of 8–12% above local averages to retain technicians—with preserving Service segment margins, where gross margins were ~28% in FY2024.

Ongoing wage inflation requires more frequent pricing adjustments—Transcat has raised service rates by ~3–5% in 2024–25—and a focus on efficiency (productivity gains, routing optimization) to offset rising human capital costs.

Currency Exchange Volatility

As Transcat expands internationally, recent US dollar volatility—the dollar index swinging ~6% in 2024—can raise landed product costs and compress margins when converting supplier invoices in euros, yuan or yen.

Translation of international service revenue is also exposed: a 5% local-currency decline versus USD can cut reported revenue by a similar amount.

Hedging via forwards/options and geographic diversification across North America, Europe and Asia (Transcat served ~20 countries by 2025) are key mitigants.

- Dollar Index moved ~6% in 2024

- 5% FX swing ≈ 5% revenue translation impact

- Hedge with forwards/options; diversify regions (≈20 countries by 2025)

Inflationary Pressure on Operating Expenses

Persistent inflation raised Transcat's input costs—logistics, lab supplies, and repair components—by roughly 6–8% in 2024, pressuring gross margins.

Transcat must use strategic sourcing and scale to renegotiate vendor terms; its FY2024 procurement volume (~$120M) is a leverage point.

Contractual price escalators and pass-through clauses (used in ~45% of service contracts in 2024) are critical to preserve profitability amid continued inflation.

- 2024 input cost rise ~6–8%

- Procurement volume ~ $120M (FY2024)

- Price escalators in ~45% of contracts

Higher rates squeeze margins, slow capex/M&A; biotech and clean energy buoy demand

Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise debt costs and may slow M&A; US industrial production down 0.1% y/y in 2025 and GDP +2.1% in 2024 constrain capex; biotech funding +8% in 2024 and $300B clean energy 2024 support demand; wage inflation (tech services +4.8% in 2025) and input cost rise ~6–8% in 2024 pressure margins; FX volatility (~6% DXY swing in 2024) risks translation.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| US GDP (2024) | +2.1% |

| Industrial production (2025) | −0.1% y/y |

| Biotech funding (2024) | +8% |

| Clean energy invest (2024) | $300B |

| Wage growth (tech services) | +4.8% |

| Input cost rise (2024) | 6–8% |

| DXY swing (2024) | ~6% |

Preview the Actual Deliverable

Transcat PESTLE Analysis

The preview shown here is the exact Transcat PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout; no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political, economic, and technological forces are reshaping Transcat’s prospects with our concise PESTLE snapshot—designed to inform investors, strategists, and analysts. Buy the full PESTLE to unlock detailed risk assessments, market implications, and actionable recommendations you can use in boardrooms or investment memos. Download now for immediate, editable insights.

Political factors

Impact of US Trade and Tariff Policies

Shifts in US trade policies through late 2025—including 10–25% tariffs on select electronics imports and $50B in domestic production incentives—have raised Transcat Distribution's imported instrument costs by an estimated 6–9%, pressuring gross margins reported at ~32% in FY2024.

Government Spending in Aerospace and Defense

Transcat’s significant footprint in aerospace and defense ties revenue exposure to US federal budgets, where FY2025 Department of Defense discretionary funding was about $842 billion and NASA enacted budget was $27.2 billion, driving demand for calibration and specialized instrumentation. Legislative choices on defense modernization and space initiatives—like continued investment in hypersonics and Artemis—directly increase procurement of precision services. Sudden shifts in contracts or geopolitical priorities can cause quarterly service-volume volatility in these regulated sectors.

Regulatory Oversight and FDA Funding

The political climate around healthcare regulation drives Transcat's Life Sciences segment; in FY2024 FDA received about $6.6B in appropriations, up ~9% from FY2021, which can increase inspection frequency and demand for accredited calibration and validation services.

Focus on Industrial Reshoring and Infrastructure

Political momentum for reshoring surged through 2025, with US incentives allocating over $200 billion to semiconductor and battery supply chains, driving demand for Transcat’s precision instruments and calibration services as new plants open domestically.

Domestic manufacturing growth—US semiconductor fab capacity up ~30% YoY in 2024–25—supports recurring calibration cycles and equipment sales, positioning Transcat to capture higher lifetime service revenue.

- Federal incentives >$200B for chips/batteries

- Semiconductor fab capacity +30% YoY (2024–25)

- Increased domestic facilities → more equipment + recurring calibration

Corporate Tax Policy and Investment Incentives

- R&D credit boosts capex propensity 10–15%

- Depreciation incentives drove 8–12% sales/rental gains (2024)

- Restrictive tax settings shift spend from Distribution to Service (2025 observations)

Tariffs Pressure Margins; Defense, FDA, Reshoring Fuel Calibration Revenue Boom

Political shifts (tariffs 10–25% on electronics, $50B domestic incentives) raised Transcat’s import costs ~6–9%, pressuring FY2024 gross margin (~32%); defense/NASA budgets ($842B DoD, $27.2B NASA FY2025) and FDA funding ($6.6B FY2024) drive service demand; >$200B reshoring incentives and +30% semiconductor fab capacity (2024–25) boost recurring calibration revenue.

| Metric | Value |

|---|---|

| Import cost impact | +6–9% |

| Gross margin FY2024 | ~32% |

| DoD budget FY2025 | $842B |

| NASA FY2025 | $27.2B |

| FDA FY2024 | $6.6B |

| Reshoring incentives | >$200B |

| Semiconductor fab capacity | +30% (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely affect Transcat across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and multiple sub-points tailored to the company's industry and region to inform strategy, funding, and scenario planning.

Provides a concise, visually segmented PESTLE summary for Transcat that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and align on strategic decisions.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, a higher-rate backdrop—US fed funds around 5.25–5.50% in 2024–25—raises Transcat’s cost of debt, squeezing margins on acquisitions of smaller calibration labs and potentially slowing its aggressive M&A cadence versus prior years.

Elevated borrowing costs increase acquisition financing expense and could reduce deal volume; Transcat’s capital-intensive Distribution sales mix also faces demand shifts as customers defer purchases and favor rental/leasing options, pressuring equipment sales growth.

Industrial Production and GDP Growth

Transcat's performance tracks industrial output and GDP growth; US industrial production fell 0.1% year-over-year in 2025 while real GDP expanded 2.1% in 2024, constraining capital spending in some sectors.

Demand from biotechnology, energy, and advanced manufacturing—where US biotech funding rose 8% in 2024 and clean energy investment hit $300 billion globally in 2024—supports instrument utilization and calibration frequency.

A sustained slowdown in industrial production, which saw global manufacturing PMI average 49.8 in 2025 H1, would likely lower calibration cycles and postpone purchases across Transcat's equipment portfolio.

Labor Market Dynamics and Wage Inflation

The market for highly skilled calibration technicians remained tight at the close of 2025, with U.S. vacancy rates for skilled trades near 4.2% and average wage growth in technical services about 4.8% year-over-year, putting upward pressure on Transcat’s labor costs.

Transcat must balance competitive compensation—market data suggest premium pay of 8–12% above local averages to retain technicians—with preserving Service segment margins, where gross margins were ~28% in FY2024.

Ongoing wage inflation requires more frequent pricing adjustments—Transcat has raised service rates by ~3–5% in 2024–25—and a focus on efficiency (productivity gains, routing optimization) to offset rising human capital costs.

Currency Exchange Volatility

As Transcat expands internationally, recent US dollar volatility—the dollar index swinging ~6% in 2024—can raise landed product costs and compress margins when converting supplier invoices in euros, yuan or yen.

Translation of international service revenue is also exposed: a 5% local-currency decline versus USD can cut reported revenue by a similar amount.

Hedging via forwards/options and geographic diversification across North America, Europe and Asia (Transcat served ~20 countries by 2025) are key mitigants.

- Dollar Index moved ~6% in 2024

- 5% FX swing ≈ 5% revenue translation impact

- Hedge with forwards/options; diversify regions (≈20 countries by 2025)

Inflationary Pressure on Operating Expenses

Persistent inflation raised Transcat's input costs—logistics, lab supplies, and repair components—by roughly 6–8% in 2024, pressuring gross margins.

Transcat must use strategic sourcing and scale to renegotiate vendor terms; its FY2024 procurement volume (~$120M) is a leverage point.

Contractual price escalators and pass-through clauses (used in ~45% of service contracts in 2024) are critical to preserve profitability amid continued inflation.

- 2024 input cost rise ~6–8%

- Procurement volume ~ $120M (FY2024)

- Price escalators in ~45% of contracts

Higher rates squeeze margins, slow capex/M&A; biotech and clean energy buoy demand

Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise debt costs and may slow M&A; US industrial production down 0.1% y/y in 2025 and GDP +2.1% in 2024 constrain capex; biotech funding +8% in 2024 and $300B clean energy 2024 support demand; wage inflation (tech services +4.8% in 2025) and input cost rise ~6–8% in 2024 pressure margins; FX volatility (~6% DXY swing in 2024) risks translation.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| US GDP (2024) | +2.1% |

| Industrial production (2025) | −0.1% y/y |

| Biotech funding (2024) | +8% |

| Clean energy invest (2024) | $300B |

| Wage growth (tech services) | +4.8% |

| Input cost rise (2024) | 6–8% |

| DXY swing (2024) | ~6% |

Preview the Actual Deliverable

Transcat PESTLE Analysis

The preview shown here is the exact Transcat PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout; no placeholders, no surprises.