Transportation Insight Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

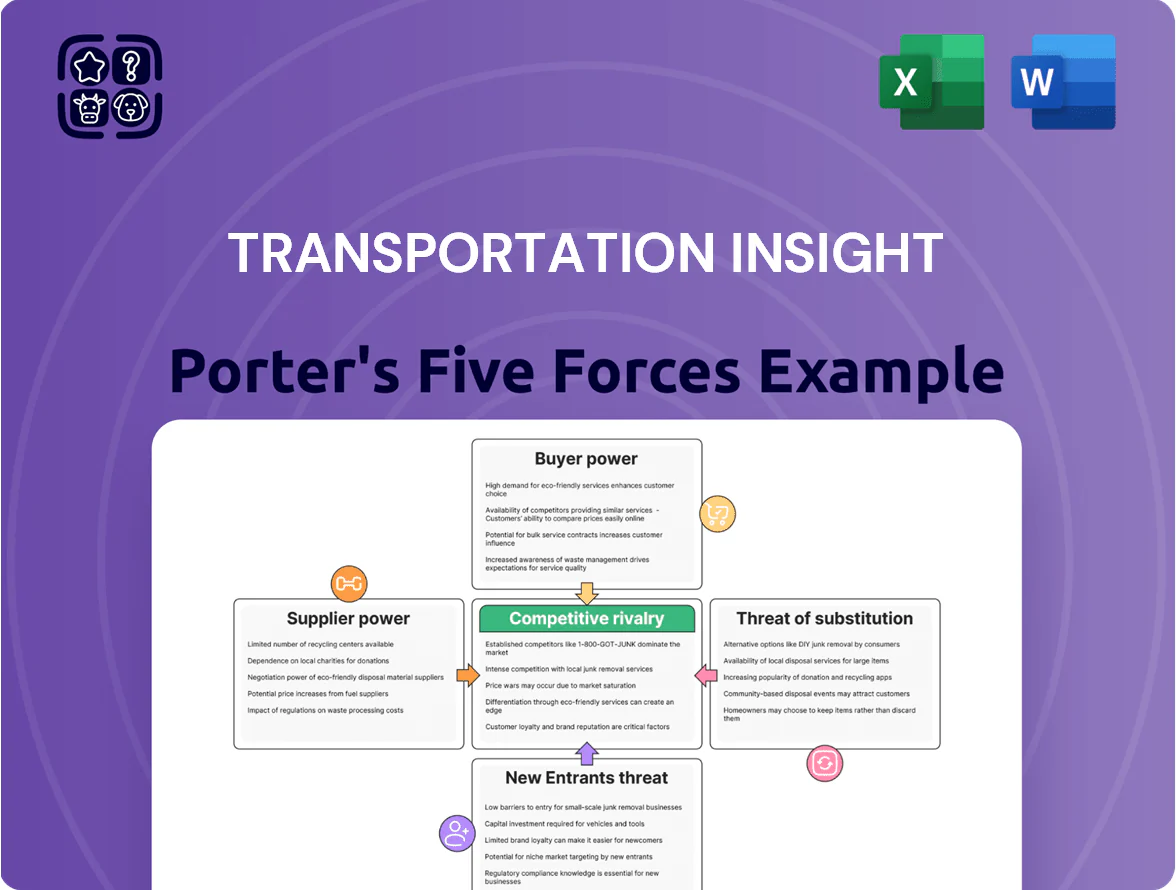

Transportation Insight operates in a competitive logistics landscape where supplier leverage, buyer demands, and threat of entrants shape margins and growth—this snapshot highlights key pressures but omits force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Carrier Capacity Fragmentation

The primary suppliers for Transportation Insight are thousands of US trucking firms; as of 2024 the top 10 carriers held under 25% of domestic truckload market share, so carrier fragmentation remains high.

No single small-to-mid carrier can exert major leverage, letting Transportation Insight negotiate rates by pooling volume—the company managed over $1.2 billion in freight spend in 2024, driving pricing power.

Consistent weekly loads and optimized routing reduce carrier empty miles (industry avg empty-mile rate ~21% in 2023), improving carrier yield and supporting lower contracted rates.

Technology and Cloud Infrastructure Providers

Transportation Insight depends on third-party cloud and SaaS vendors for its analytics; in 2025 leading providers like AWS, Microsoft Azure, and Google Cloud held ~64% of global market share, giving suppliers moderate bargaining power.

Their standardized pricing and essential uptime mean limited price competition, while multi-cloud discounts and reserved instances cap cost exposure.

Switching costs are high: migrating petabytes of supply-chain data can exceed $1–3M plus weeks of downtime risk, so Transportation Insight faces real operational lock-in.

Dominance of Major Parcel Carriers

The parcel spend management market is concentrated: UPS and FedEx together handled about 64% of US small-package volume in 2024 (US BLS/Carrier filings), giving them strong supplier power over pricing and capacity.

Regional postal services and last-mile partners fill gaps, but offer limited substitutes for national/international lanes, so Transportation Insight must keep strategic carrier ties.

With average parcel rates up roughly 3.5% year-over-year in 2024, the firm needs negotiated discounts, zone optimization, and service-mix shifts to cut client costs within rigid carrier tariffs.

Specialized Logistics Labor Market

- 2024–25 demand +28% for logistics data roles

- Median comp ≈ $155,000 (2025)

- Contractor rates +10–20%

- Service delays: weeks to insight

Real-Time Data and Telematics Providers

Access to real-time traffic, weather, and GPS data is essential for supply chain visibility and predictive analytics; telematics firms like HERE Technologies and Trimble processed billions of events in 2024, enabling ETA accuracy improvements of 10–25%.

Firms that aggregate this data occupy a gatekeeper role and can pressure logistics players via subscription pricing, tiered APIs, and contract terms—HERE reported $1.1B revenue in 2024 from location services, showing pricing power.

As logistics optimization relies on data, limited access or higher fees raise operating costs and raise barriers to entry for smaller carriers, shifting bargaining power toward these providers.

- Real-time data = core input for visibility and ETA gains (10–25%)

- Major providers (HERE, Trimble) showed strong 2024 revenues (~$1B range)

- Subscription/API limits used as leverage over logistics firms

- Smaller carriers face higher costs and entry barriers

Parcel and cloud giants tighten supplier leverage as talent costs surge; pooled spend offsets

Suppliers exert mixed power: fragmented truck carriers limit leverage, while parcel giants (UPS+FedEx ~64% share in 2024) and cloud/telematics providers (AWS/Azure/GCP ~64% cloud share; HERE ~$1.1B revenue 2024) hold strong negotiating positions; talent shortages pushed logistics data-scientist pay to ~$155,000 in 2025, raising costs. Transportation Insight offsets this via $1.2B pooled spend and routing efficiency.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Top US carriers | Top 10 market share | <25% |

| Parcel (UPS+FedEx) | US small-package share | ~64% |

| Cloud providers | Global market share | ~64% |

| Telematics (HERE) | Revenue | ~$1.1B |

| Logistics data scientists | Median comp | ~$155,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Transportation Insight that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats—delivering strategic commentary and editable insights for investor materials, strategy decks, or academic use.

Condenses Transportation Insight’s Porter’s Five Forces into a single, actionable sheet—ideal for quick strategy checks and boardroom-ready slides.

Customers Bargaining Power

Low Switching Costs for Standard Services

Customers view basic freight brokerage as commoditized, so switching for a 3–7% rate improvement is common; 2024 DAT freight index showed spot rates down 6% year-over-year, easing switching. Deep consulting and TI’s integrated TMS (transportation management system) create some stickiness—clients with tech integrations report 12–18% lower churn—but execution layers still move with low friction, forcing TI to prove savings and tech ROI continually.

High Price Sensitivity in Competitive Industries

Many shippers Transportation Insight serves are in low-margin sectors—US retail gross margins averaged 24.6% in 2024 and manufacturing net margins 6.8%—so cents-per-mile matter; clients push for fee cuts or higher shared-savings splits. Customers commonly demand 10–25% fee reductions or raise shared-savings claims, forcing providers to trim margins; in late 2025, with logistics cost-efficiency a priority, upward pricing pressure on carriers and 3PLs is acute.

Demand for End-to-End Visibility

Buyers now demand real-time visibility and predictive shipment insights across the full lifecycle, giving them leverage to insist advanced telematics, AI ETA, and blockchain tracking as baseline features; 72% of shippers cited visibility as a top selection factor in 2024 surveys.

Volume-Based Negotiation Leverage

- 25–40% revenue concentration per large shipper

- Net-60+ payment terms common

- Dedicated account teams required

- Single-client loss → revenue drop 10–30%

Availability of Alternative Digital Platforms

The rise of self-service digital freight marketplaces lets shippers bypass managed services for parts of their supply chain; platforms like Uber Freight and FLEXPORT reported combined spot volume growth of ~28% in 2024, making direct rate comparisons common.

Buyers can quickly compare spot rates to Transportation Insight’s contract rates, increasing pressure to justify fees when spot is 10–25% cheaper in volatile lanes.

That transparency raises customer bargaining power when cost-to-benefit of managed services isn’t clearly quantified.

- Spot vs contract: 10–25% gap in volatile lanes (2024)

- Self-serve spot volume +28% (2024)

- Buyers can benchmark rates instantly

Customers Hold Leverage: Spot Surge, Contract Gaps & TI ROI Required (12–18%)

Customers hold strong bargaining power: spot rates fell 6% YoY (DAT 2024) and spot volume rose ~28% (2024), enabling 10–25% spot vs contract gaps; large shippers (25–40% revenue concentration) demand net-60+ terms and custom services, risking 10–30% revenue loss if churned; clients with TI integrations show 12–18% lower churn, so TI must continually prove 12–18% ROI to defend margins.

| Metric | Value |

|---|---|

| DAT spot rate YoY (2024) | -6% |

| Spot volume growth (2024) | ~28% |

| Spot vs contract gap | 10–25% |

| Large shipper revenue share | 25–40% |

| Revenue loss if churned | 10–30% |

| Churn reduction with TI integrations | 12–18% |

Same Document Delivered

Transportation Insight Porter's Five Forces Analysis

This preview shows the exact Transportation Insight Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders or samples, fully formatted and ready for use. The document displayed is the final, professionally written deliverable covering industry rivalry, buyer and supplier power, threat of substitutes, and barriers to entry. Purchase grants immediate access to this identical file for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Transportation Insight operates in a competitive logistics landscape where supplier leverage, buyer demands, and threat of entrants shape margins and growth—this snapshot highlights key pressures but omits force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Carrier Capacity Fragmentation

The primary suppliers for Transportation Insight are thousands of US trucking firms; as of 2024 the top 10 carriers held under 25% of domestic truckload market share, so carrier fragmentation remains high.

No single small-to-mid carrier can exert major leverage, letting Transportation Insight negotiate rates by pooling volume—the company managed over $1.2 billion in freight spend in 2024, driving pricing power.

Consistent weekly loads and optimized routing reduce carrier empty miles (industry avg empty-mile rate ~21% in 2023), improving carrier yield and supporting lower contracted rates.

Technology and Cloud Infrastructure Providers

Transportation Insight depends on third-party cloud and SaaS vendors for its analytics; in 2025 leading providers like AWS, Microsoft Azure, and Google Cloud held ~64% of global market share, giving suppliers moderate bargaining power.

Their standardized pricing and essential uptime mean limited price competition, while multi-cloud discounts and reserved instances cap cost exposure.

Switching costs are high: migrating petabytes of supply-chain data can exceed $1–3M plus weeks of downtime risk, so Transportation Insight faces real operational lock-in.

Dominance of Major Parcel Carriers

The parcel spend management market is concentrated: UPS and FedEx together handled about 64% of US small-package volume in 2024 (US BLS/Carrier filings), giving them strong supplier power over pricing and capacity.

Regional postal services and last-mile partners fill gaps, but offer limited substitutes for national/international lanes, so Transportation Insight must keep strategic carrier ties.

With average parcel rates up roughly 3.5% year-over-year in 2024, the firm needs negotiated discounts, zone optimization, and service-mix shifts to cut client costs within rigid carrier tariffs.

Specialized Logistics Labor Market

- 2024–25 demand +28% for logistics data roles

- Median comp ≈ $155,000 (2025)

- Contractor rates +10–20%

- Service delays: weeks to insight

Real-Time Data and Telematics Providers

Access to real-time traffic, weather, and GPS data is essential for supply chain visibility and predictive analytics; telematics firms like HERE Technologies and Trimble processed billions of events in 2024, enabling ETA accuracy improvements of 10–25%.

Firms that aggregate this data occupy a gatekeeper role and can pressure logistics players via subscription pricing, tiered APIs, and contract terms—HERE reported $1.1B revenue in 2024 from location services, showing pricing power.

As logistics optimization relies on data, limited access or higher fees raise operating costs and raise barriers to entry for smaller carriers, shifting bargaining power toward these providers.

- Real-time data = core input for visibility and ETA gains (10–25%)

- Major providers (HERE, Trimble) showed strong 2024 revenues (~$1B range)

- Subscription/API limits used as leverage over logistics firms

- Smaller carriers face higher costs and entry barriers

Parcel and cloud giants tighten supplier leverage as talent costs surge; pooled spend offsets

Suppliers exert mixed power: fragmented truck carriers limit leverage, while parcel giants (UPS+FedEx ~64% share in 2024) and cloud/telematics providers (AWS/Azure/GCP ~64% cloud share; HERE ~$1.1B revenue 2024) hold strong negotiating positions; talent shortages pushed logistics data-scientist pay to ~$155,000 in 2025, raising costs. Transportation Insight offsets this via $1.2B pooled spend and routing efficiency.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Top US carriers | Top 10 market share | <25% |

| Parcel (UPS+FedEx) | US small-package share | ~64% |

| Cloud providers | Global market share | ~64% |

| Telematics (HERE) | Revenue | ~$1.1B |

| Logistics data scientists | Median comp | ~$155,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Transportation Insight that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats—delivering strategic commentary and editable insights for investor materials, strategy decks, or academic use.

Condenses Transportation Insight’s Porter’s Five Forces into a single, actionable sheet—ideal for quick strategy checks and boardroom-ready slides.

Customers Bargaining Power

Low Switching Costs for Standard Services

Customers view basic freight brokerage as commoditized, so switching for a 3–7% rate improvement is common; 2024 DAT freight index showed spot rates down 6% year-over-year, easing switching. Deep consulting and TI’s integrated TMS (transportation management system) create some stickiness—clients with tech integrations report 12–18% lower churn—but execution layers still move with low friction, forcing TI to prove savings and tech ROI continually.

High Price Sensitivity in Competitive Industries

Many shippers Transportation Insight serves are in low-margin sectors—US retail gross margins averaged 24.6% in 2024 and manufacturing net margins 6.8%—so cents-per-mile matter; clients push for fee cuts or higher shared-savings splits. Customers commonly demand 10–25% fee reductions or raise shared-savings claims, forcing providers to trim margins; in late 2025, with logistics cost-efficiency a priority, upward pricing pressure on carriers and 3PLs is acute.

Demand for End-to-End Visibility

Buyers now demand real-time visibility and predictive shipment insights across the full lifecycle, giving them leverage to insist advanced telematics, AI ETA, and blockchain tracking as baseline features; 72% of shippers cited visibility as a top selection factor in 2024 surveys.

Volume-Based Negotiation Leverage

- 25–40% revenue concentration per large shipper

- Net-60+ payment terms common

- Dedicated account teams required

- Single-client loss → revenue drop 10–30%

Availability of Alternative Digital Platforms

The rise of self-service digital freight marketplaces lets shippers bypass managed services for parts of their supply chain; platforms like Uber Freight and FLEXPORT reported combined spot volume growth of ~28% in 2024, making direct rate comparisons common.

Buyers can quickly compare spot rates to Transportation Insight’s contract rates, increasing pressure to justify fees when spot is 10–25% cheaper in volatile lanes.

That transparency raises customer bargaining power when cost-to-benefit of managed services isn’t clearly quantified.

- Spot vs contract: 10–25% gap in volatile lanes (2024)

- Self-serve spot volume +28% (2024)

- Buyers can benchmark rates instantly

Customers Hold Leverage: Spot Surge, Contract Gaps & TI ROI Required (12–18%)

Customers hold strong bargaining power: spot rates fell 6% YoY (DAT 2024) and spot volume rose ~28% (2024), enabling 10–25% spot vs contract gaps; large shippers (25–40% revenue concentration) demand net-60+ terms and custom services, risking 10–30% revenue loss if churned; clients with TI integrations show 12–18% lower churn, so TI must continually prove 12–18% ROI to defend margins.

| Metric | Value |

|---|---|

| DAT spot rate YoY (2024) | -6% |

| Spot volume growth (2024) | ~28% |

| Spot vs contract gap | 10–25% |

| Large shipper revenue share | 25–40% |

| Revenue loss if churned | 10–30% |

| Churn reduction with TI integrations | 12–18% |

Same Document Delivered

Transportation Insight Porter's Five Forces Analysis

This preview shows the exact Transportation Insight Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders or samples, fully formatted and ready for use. The document displayed is the final, professionally written deliverable covering industry rivalry, buyer and supplier power, threat of substitutes, and barriers to entry. Purchase grants immediate access to this identical file for download and application.