Transportation Insight PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Transportation Insight—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory. Ideal for investors, consultants, and planners, this ready-to-use report helps you anticipate risks and spot growth opportunities. Purchase the full analysis now for the complete, editable breakdown and actionable recommendations.

Political factors

Trade policy and tariff volatility

Changes in trade agreements and tariff spikes reshape routing and costs: average container shipping rates rose 18% in 2024 after new US-EU and US-ASEAN tariff measures, forcing reroutes that added 6–12% to transit costs for many shippers.

Transportation Insight must adapt pricing models and route optimization to preserve client savings; its clients saw potential savings erosion of up to $200–400 per container without agile adjustments in 2024.

Geopolitical tensions in 2025—including sanctions and Red Sea disruptions—require dynamic playbooks; firms using real-time rerouting reduced delay costs by ~25% in late 2024.

Infrastructure investment initiatives

Government spending on U.S. transportation infrastructure—about $125 billion annual federal and state investment in 2024–2025 including the IIJA allocations—directly shortens transit times and raises operational efficiency on highways, ports, and rail corridors.

Transportation Insight capitalizes on upgraded corridors to optimize carrier routing, cutting average route distances and fuel consumption by an estimated 6–8% versus pre‑IIJA baselines.

Federal funding levels through late 2025, with roughly $110 billion obligated from IIJA programs, are critical inputs for the company’s 5–10 year logistics capacity and fleet planning models.

Labor union influence and regulations

Political support for collective bargaining and recent U.S. federal and state labor reforms have increased unionization efforts, contributing to a 6–8% rise in driver wage costs in 2024 and pressuring margins for Transportation Insight.

Strikes at major ports and carriers—US West Coast port labor disruptions in 2024 reduced throughput by about 12% at peak—require robust contingency plans to avoid service delays and demurrage fees exceeding $1,000+ per container.

Continuous monitoring of labor-rights legislation and union activity is essential to anticipate driver availability shifts and adjust capacity, routing, and contract strategies to contain operational risk and cost volatility.

Governmental focus on supply chain resilience

Following global disruptions, governments worldwide are pushing for domestic manufacturing and supply chain transparency; 78% of OECD countries introduced reshoring incentives by 2024, boosting demand for analytics that guide site selection and risk modeling.

Transportation Insight captures this tailwind by supplying end-to-end visibility and cost-to-serve analytics that support reshoring/nearshoring decisions, with clients reporting average supply-chain cost reductions of 6–12% after deployment.

Policy incentives—$150B+ in US and EU grants/credits by 2025 for supply chain security—drive adoption of real-time tracking, inventory optimization, and compliance reporting solutions.

- 78% of OECD nations with reshoring incentives by 2024

- $150B+ in US/EU supply-chain security incentives through 2025

- Clients see 6–12% average supply-chain cost reduction

- Higher demand for end-to-end visibility and risk analytics

Fuel subsidies and energy policy

Political choices on fuel subsidies and energy independence directly alter transportation operating costs; US federal fuel subsidies and state diesel tax variations contributed to a 4–6% swing in carrier fuel expense in 2024, with diesel averaging about 4.10 USD/gal in 2024 versus 3.65 USD/gal in 2023.

Mandates for renewables and increases in diesel taxes (several states added 1–3¢/gal levies in 2024) shift modal costs and capital plans for carriers managed by Transportation Insight, impacting contract rates and margin forecasts.

Transportation Insight must fold these volatile energy inputs into parcel and freight spend models—fuel surcharges comprised ~8–12% of total freight cost in 2024—updating forecasts and supplier strategies accordingly.

- Fuel price volatility (diesel ~4.10 USD/gal in 2024) alters carrier operating costs

- Renewable mandates and tax changes (1–3¢/gal state levies) affect modal choice and rates

- Fuel surcharges represented ~8–12% of freight spend in 2024; must be modeled

Embed policy-driven tariffs, wages, diesel & infrastructure into pricing to protect margins

Political shifts—tariffs, infrastructure funding (~$125B/yr including IIJA; $110B obligated by late-2025), labor rules (driver wages +6–8% in 2024), and fuel policy (diesel ~$4.10/gal in 2024; fuel surcharges 8–12%)—drive routing, cost and capacity decisions; Transportation Insight must embed these inputs into pricing, routing, and capacity models to protect margins and client savings.

| Factor | 2024–2025 Metric |

|---|---|

| Infrastructure funding | $125B/yr; $110B obligated |

| Tariff impact | container rates +18% (2024) |

| Driver wages | +6–8% (2024) |

| Diesel price | $4.10/gal (2024) |

What is included in the product

Explores how macro-environmental factors affect Transportation Insight across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives and investors.

Provides a clean, visually segmented PESTLE summary for Transportation Insight that’s easily dropped into presentations, editable with notes for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary pressures and interest rates

High global policy rates—US Fed funds at 5.25–5.50% in 2025—raise borrowing costs, constraining capital expenditure decisions for Transportation Insight and its clients and prioritizing leasing over purchases.

Inflation running near 3–4% in 2024–25 increased labor, diesel (US national average diesel ~$4.00/gal in 2024) and equipment costs, amplifying demand for spend-management to protect margins.

Delivering measurable cost-avoidance—typically 5–10% savings in logistics sourcing engagements—remains a core value proposition amid persistent economic uncertainty.

E-commerce growth trajectories

The continued expansion of online retail—global e-commerce sales hit an estimated 5.7 trillion USD in 2023 and are forecasted to reach about 8.1 trillion USD by 2026—drives demand for complex parcel management and last-mile delivery solutions.

Transportation Insight capitalizes by offering specialized analytics that reduced client last-mile costs by up to 18% in 2024 through route optimization and volume consolidation for high-volume e-commerce brands.

Economic shifts in consumer spending—US retail e-commerce grew 7.1% in 2024 while discretionary categories fluctuated—require the company to remain flexible in logistics modeling, adjusting capacity and pricing elasticity analyses in near real time.

Fuel price volatility

Fluctuations in global oil markets—Brent averaged about 86 USD/barrel in 2024, swinging ±15%—remain a primary driver of transportation costs and fuel surcharges.

Transportation Insight uses data-driven auditing and benchmarking to recover typical surcharge overcharges of 3–7% and secure contracted fuel-rate improvements averaging 2–4%.

Energy-price stability or volatility through 2025 will materially shift total cost of ownership for supply chains, with a 10% fuel-price move translating to ~1–3% change in logistics spend for many shippers.

Labor market shortages

A persistent shortage of qualified truck drivers and warehouse personnel has pushed industry wage growth to about 6–8% annually in 2024, raising service costs and capacity volatility for shippers.

Transportation Insight mitigates this by optimizing carrier networks and blending contract, dedicated and spot capacity to secure reliable service despite labor constraints.

Economic competition for talent accelerates adoption of automation and 3PL expertise; US freight automation investment reached an estimated $4.2B in 2024.

- Wage inflation 6–8% (2024)

- TI strategy: carrier network optimization

- Increased automation and 3PL reliance; $4.2B freight automation spend (2024)

Currency exchange rate fluctuations

For clients in international trade, the US dollar's 2024 average trade-weighted index rise of ~3.5% increased imported shipping costs and squeezed margins; Transportation Insight offers visibility to quantify FX impact across lanes and carriers.

Currency volatility—FX moves of up to 6-8% intra-year in 2024—demands sophisticated financial modeling to maintain accurate logistics budgeting and hedge effectiveness.

- Dollar strength raises landed cost and freight expense exposure

- Transportation Insight provides FX-adjusted cost visibility by lane

- 6-8% 2024 intra-year FX swings require scenario modeling and hedging

High rates, rising fuel & wages push automation, 3PLs and lane-level FX visibility

High rates and ~3–4% inflation in 2024–25 raise capex and operating costs; diesel ~$4.00/gal and Brent ~$86/bbl (2024) drive fuel surcharges; e-commerce (USD 5.7T in 2023; ~8.1T by 2026) fuels last-mile demand; wage inflation 6–8% and $4.2B freight automation (2024) shift spend to automation and 3PLs; USD TWI +3.5% (2024) and 6–8% FX swings require lane-level FX visibility.

| Metric | 2024 |

|---|---|

| Diesel | $4.00/gal |

| Brent | $86/bbl |

| Wage inflation | 6–8% |

| Freight automation spend | $4.2B |

| USD TWI change | +3.5% |

Preview the Actual Deliverable

Transportation Insight PESTLE Analysis

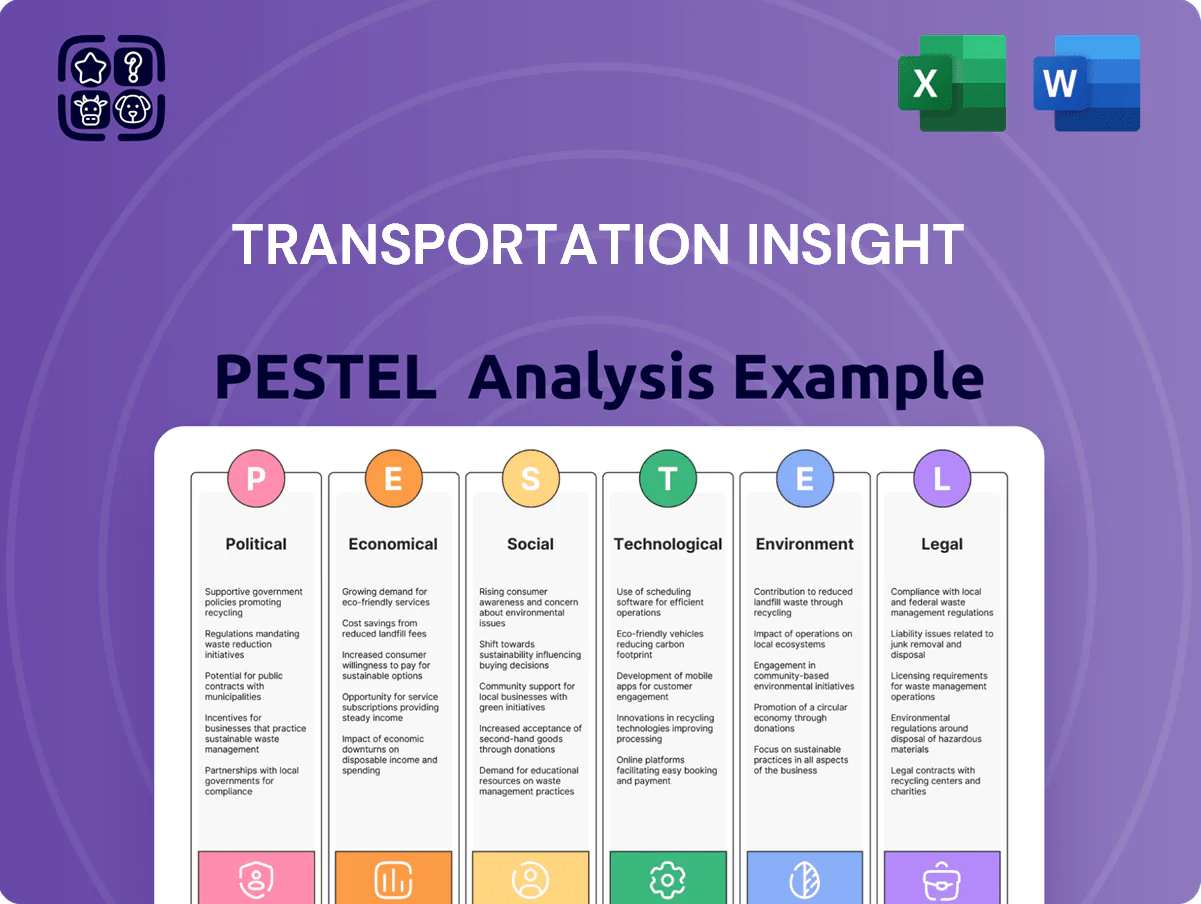

The preview shown here is the exact Transportation Insight PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Transportation Insight—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory. Ideal for investors, consultants, and planners, this ready-to-use report helps you anticipate risks and spot growth opportunities. Purchase the full analysis now for the complete, editable breakdown and actionable recommendations.

Political factors

Trade policy and tariff volatility

Changes in trade agreements and tariff spikes reshape routing and costs: average container shipping rates rose 18% in 2024 after new US-EU and US-ASEAN tariff measures, forcing reroutes that added 6–12% to transit costs for many shippers.

Transportation Insight must adapt pricing models and route optimization to preserve client savings; its clients saw potential savings erosion of up to $200–400 per container without agile adjustments in 2024.

Geopolitical tensions in 2025—including sanctions and Red Sea disruptions—require dynamic playbooks; firms using real-time rerouting reduced delay costs by ~25% in late 2024.

Infrastructure investment initiatives

Government spending on U.S. transportation infrastructure—about $125 billion annual federal and state investment in 2024–2025 including the IIJA allocations—directly shortens transit times and raises operational efficiency on highways, ports, and rail corridors.

Transportation Insight capitalizes on upgraded corridors to optimize carrier routing, cutting average route distances and fuel consumption by an estimated 6–8% versus pre‑IIJA baselines.

Federal funding levels through late 2025, with roughly $110 billion obligated from IIJA programs, are critical inputs for the company’s 5–10 year logistics capacity and fleet planning models.

Labor union influence and regulations

Political support for collective bargaining and recent U.S. federal and state labor reforms have increased unionization efforts, contributing to a 6–8% rise in driver wage costs in 2024 and pressuring margins for Transportation Insight.

Strikes at major ports and carriers—US West Coast port labor disruptions in 2024 reduced throughput by about 12% at peak—require robust contingency plans to avoid service delays and demurrage fees exceeding $1,000+ per container.

Continuous monitoring of labor-rights legislation and union activity is essential to anticipate driver availability shifts and adjust capacity, routing, and contract strategies to contain operational risk and cost volatility.

Governmental focus on supply chain resilience

Following global disruptions, governments worldwide are pushing for domestic manufacturing and supply chain transparency; 78% of OECD countries introduced reshoring incentives by 2024, boosting demand for analytics that guide site selection and risk modeling.

Transportation Insight captures this tailwind by supplying end-to-end visibility and cost-to-serve analytics that support reshoring/nearshoring decisions, with clients reporting average supply-chain cost reductions of 6–12% after deployment.

Policy incentives—$150B+ in US and EU grants/credits by 2025 for supply chain security—drive adoption of real-time tracking, inventory optimization, and compliance reporting solutions.

- 78% of OECD nations with reshoring incentives by 2024

- $150B+ in US/EU supply-chain security incentives through 2025

- Clients see 6–12% average supply-chain cost reduction

- Higher demand for end-to-end visibility and risk analytics

Fuel subsidies and energy policy

Political choices on fuel subsidies and energy independence directly alter transportation operating costs; US federal fuel subsidies and state diesel tax variations contributed to a 4–6% swing in carrier fuel expense in 2024, with diesel averaging about 4.10 USD/gal in 2024 versus 3.65 USD/gal in 2023.

Mandates for renewables and increases in diesel taxes (several states added 1–3¢/gal levies in 2024) shift modal costs and capital plans for carriers managed by Transportation Insight, impacting contract rates and margin forecasts.

Transportation Insight must fold these volatile energy inputs into parcel and freight spend models—fuel surcharges comprised ~8–12% of total freight cost in 2024—updating forecasts and supplier strategies accordingly.

- Fuel price volatility (diesel ~4.10 USD/gal in 2024) alters carrier operating costs

- Renewable mandates and tax changes (1–3¢/gal state levies) affect modal choice and rates

- Fuel surcharges represented ~8–12% of freight spend in 2024; must be modeled

Embed policy-driven tariffs, wages, diesel & infrastructure into pricing to protect margins

Political shifts—tariffs, infrastructure funding (~$125B/yr including IIJA; $110B obligated by late-2025), labor rules (driver wages +6–8% in 2024), and fuel policy (diesel ~$4.10/gal in 2024; fuel surcharges 8–12%)—drive routing, cost and capacity decisions; Transportation Insight must embed these inputs into pricing, routing, and capacity models to protect margins and client savings.

| Factor | 2024–2025 Metric |

|---|---|

| Infrastructure funding | $125B/yr; $110B obligated |

| Tariff impact | container rates +18% (2024) |

| Driver wages | +6–8% (2024) |

| Diesel price | $4.10/gal (2024) |

What is included in the product

Explores how macro-environmental factors affect Transportation Insight across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives and investors.

Provides a clean, visually segmented PESTLE summary for Transportation Insight that’s easily dropped into presentations, editable with notes for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary pressures and interest rates

High global policy rates—US Fed funds at 5.25–5.50% in 2025—raise borrowing costs, constraining capital expenditure decisions for Transportation Insight and its clients and prioritizing leasing over purchases.

Inflation running near 3–4% in 2024–25 increased labor, diesel (US national average diesel ~$4.00/gal in 2024) and equipment costs, amplifying demand for spend-management to protect margins.

Delivering measurable cost-avoidance—typically 5–10% savings in logistics sourcing engagements—remains a core value proposition amid persistent economic uncertainty.

E-commerce growth trajectories

The continued expansion of online retail—global e-commerce sales hit an estimated 5.7 trillion USD in 2023 and are forecasted to reach about 8.1 trillion USD by 2026—drives demand for complex parcel management and last-mile delivery solutions.

Transportation Insight capitalizes by offering specialized analytics that reduced client last-mile costs by up to 18% in 2024 through route optimization and volume consolidation for high-volume e-commerce brands.

Economic shifts in consumer spending—US retail e-commerce grew 7.1% in 2024 while discretionary categories fluctuated—require the company to remain flexible in logistics modeling, adjusting capacity and pricing elasticity analyses in near real time.

Fuel price volatility

Fluctuations in global oil markets—Brent averaged about 86 USD/barrel in 2024, swinging ±15%—remain a primary driver of transportation costs and fuel surcharges.

Transportation Insight uses data-driven auditing and benchmarking to recover typical surcharge overcharges of 3–7% and secure contracted fuel-rate improvements averaging 2–4%.

Energy-price stability or volatility through 2025 will materially shift total cost of ownership for supply chains, with a 10% fuel-price move translating to ~1–3% change in logistics spend for many shippers.

Labor market shortages

A persistent shortage of qualified truck drivers and warehouse personnel has pushed industry wage growth to about 6–8% annually in 2024, raising service costs and capacity volatility for shippers.

Transportation Insight mitigates this by optimizing carrier networks and blending contract, dedicated and spot capacity to secure reliable service despite labor constraints.

Economic competition for talent accelerates adoption of automation and 3PL expertise; US freight automation investment reached an estimated $4.2B in 2024.

- Wage inflation 6–8% (2024)

- TI strategy: carrier network optimization

- Increased automation and 3PL reliance; $4.2B freight automation spend (2024)

Currency exchange rate fluctuations

For clients in international trade, the US dollar's 2024 average trade-weighted index rise of ~3.5% increased imported shipping costs and squeezed margins; Transportation Insight offers visibility to quantify FX impact across lanes and carriers.

Currency volatility—FX moves of up to 6-8% intra-year in 2024—demands sophisticated financial modeling to maintain accurate logistics budgeting and hedge effectiveness.

- Dollar strength raises landed cost and freight expense exposure

- Transportation Insight provides FX-adjusted cost visibility by lane

- 6-8% 2024 intra-year FX swings require scenario modeling and hedging

High rates, rising fuel & wages push automation, 3PLs and lane-level FX visibility

High rates and ~3–4% inflation in 2024–25 raise capex and operating costs; diesel ~$4.00/gal and Brent ~$86/bbl (2024) drive fuel surcharges; e-commerce (USD 5.7T in 2023; ~8.1T by 2026) fuels last-mile demand; wage inflation 6–8% and $4.2B freight automation (2024) shift spend to automation and 3PLs; USD TWI +3.5% (2024) and 6–8% FX swings require lane-level FX visibility.

| Metric | 2024 |

|---|---|

| Diesel | $4.00/gal |

| Brent | $86/bbl |

| Wage inflation | 6–8% |

| Freight automation spend | $4.2B |

| USD TWI change | +3.5% |

Preview the Actual Deliverable

Transportation Insight PESTLE Analysis

The preview shown here is the exact Transportation Insight PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.