Travelers Companies Boston Consulting Group Matrix

See the Bigger Picture

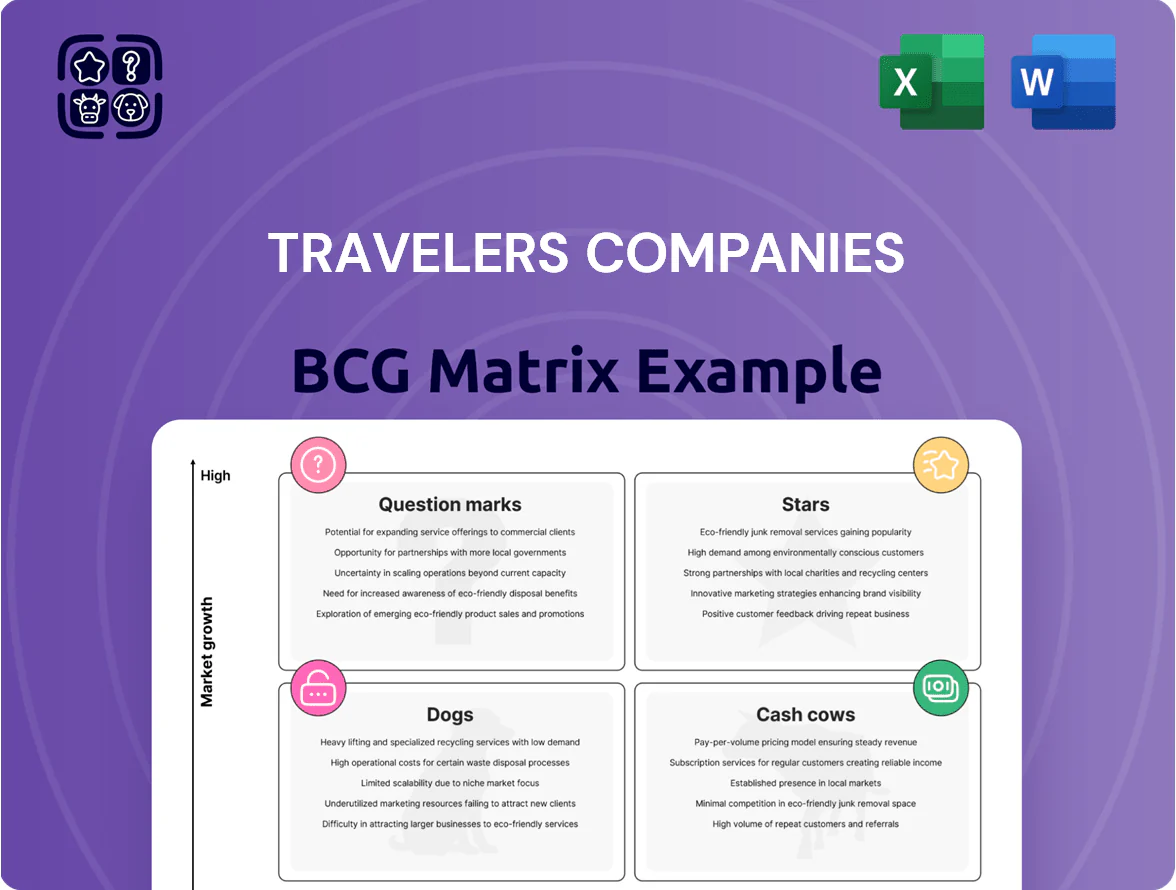

Travelers Companies’ BCG Matrix preview highlights its dominant commercial insurance lines as likely Cash Cows, emerging specialty units as potential Stars, and legacy low-growth segments edging toward Dogs—offering a snapshot of capital allocation priorities and growth levers. This concise view teases quadrant placements and strategic implications; buy the full BCG Matrix to access a quadrant-by-quadrant breakdown, data-driven recommendations, and downloadable Word and Excel files to guide investment and portfolio decisions.

Stars

Cyber Insurance Solutions

By late 2025 Travelers Companies has emerged as a leader in cyber insurance, with the global cyber insurance market projected at $30.9B in 2025 and Travelers holding an estimated 8–10% share in the US commercial segment.

The unit leverages proprietary underwriting data from ~30m commercial policies to offer comprehensive coverage in high demand across SMEs to Fortune 500s.

Heavy ongoing spend on cybersecurity R&D and real-time threat monitoring compresses near-term margins, but high market share makes it a primary growth driver.

Analysts expect this Stars unit to become a cash cow as the cyber market matures toward ~2030, with premium growth slowing and loss ratios stabilizing.

Technology Sector Business Insurance

Travelers holds a leading spot in the tech & life-sciences insurance niche, capturing an estimated 12–15% share of the US specialty tech market by 2024 and writing roughly $1.1B in related premiums in 2024; products cover software, hardware, and renewable-energy firms that need tailored liability and cyber protections. The sector’s ~8–10% CAGR keeps new premium inflows robust, but Travelers must keep investing in specialist claims teams and tech-driven underwriting to fend off nimble fintech entrants.

Excess and Surplus Lines

Through Northfield and specialty units, Travelers captured notable share in the hard market of 2024–2025, growing excess & surplus (E&S) written premiums by about 28% year-over-year to roughly $3.2 billion in 2025, per company segment disclosures.

As standard carriers withdrew from volatile sectors, E&S supplied coverage for unique/high-capacity risks, driving a combined ratio advantage near 92 in 2025 while requiring elevated statutory capital—about 15% of Travelers’ allocated commercial capital—to back volatility.

The segment’s high growth and pricing power made it a Stars quadrant fit in the BCG matrix: strong market growth and high relative share, generating substantial premium income but needing continued capital intensity and active risk selection.

Management and Professional Liability

Management and Professional Liability has surged in the mid-2020s as corporate governance and employment-practice claims rose; Travelers holds a leading share in Directors & Officers (D&O) and Employment Practices Liability Insurance (EPLI), with 2024 segment premiums around $1.1B, up ~8% year-over-year.

The complexity lets Travelers charge premium pricing while global market growth continues; maintaining this position requires ongoing investment in legal teams and actuarial modeling to track regulatory changes and loss trends.

- 2024 segment premiums ~$1.1B, +8% YoY

- Leading share in D&O and EPLI markets

- Premium pricing enabled by complex risk profiles

- Ongoing legal and actuarial investment required

Middle Market International Expansion

Travelers has grown middle-market commercial share in Canada, the UK and Ireland, lifting international commercial premiums to about $1.8B in 2024, with mid‑single-digit CAGR since 2019, driven by package-based products where Travelers leads.

Infrastructure costs are high—estimated incremental SG&A of ~$120–150M to scale—but revenue growth in these markets outpaced US mature segments in 2023–24, reducing US concentration risk for long‑term revenue.

- International commercial premiums ≈ $1.8B (2024)

- Mid‑single‑digit CAGR since 2019

- Incremental SG&A ~$120–150M to scale

- Package products driving share gains in Canada/UK/Ireland

Travelers' Specialty Units Drive High Growth: Leading Shares in Cyber, Tech, E&S

Travelers’ Stars units (cyber, tech/life‑sciences, E&S, D&O/EPLI) show high growth and leading share: cyber ~$30.9B market (2025) with Travelers 8–10% US share; tech specialty ~$1.1B premiums (2024); E&S ~$3.2B premiums (2025); D&O/EPLI ~$1.1B (2024); international commercial ~$1.8B (2024).

| Unit | Key metric |

|---|---|

| Cyber | $30.9B market (2025); 8–10% US share |

| Tech | $1.1B premiums (2024) |

| E&S | $3.2B premiums (2025) |

| D&O/EPLI | $1.1B premiums (2024) |

| Intl Commercial | $1.8B premiums (2024) |

What is included in the product

BCG Matrix of Travelers: strategic placement of insurance lines as Stars, Cash Cows, Question Marks, and Dogs with investment and divestment guidance.

One-page BCG Matrix placing Travelers' business units into clear quadrants for executive decision-making and portfolio optimization.

Cash Cows

Workers Compensation

Travelers is the US market leader in workers compensation, leveraging decades of proprietary claims data to price risk; in 2024 the segment generated roughly $4.2 billion in net premiums written, delivering steady underwriting gains. This mature line produces predictable cash flow that funds dividends and share buybacks—Travelers returned $3.1 billion to shareholders in 2024. Minimal promotional spend keeps expense ratios low, so the focus is on operational efficiency and medical cost containment to protect margins.

Surety and Fidelity Bonds

As one of the largest surety writers globally, Travelers (TRV) holds ~12–15% market share in US surety as of 2024, giving it a dominant position in a high-barrier sector tied to licensing, capital and relationships.

The mature surety market tracks infrastructure and construction cycles, delivering steady premiums and historically low loss ratios (~20–30% combined ratio on surety lines in 2023), so returns are reliable.

Surety needs little new capital, freeing cash—Travelers redirected roughly $400–600M annually (2022–2024) to higher-growth units—while its AA financial strength rating makes it preferred for large government and private contracts.

Commercial Multi-Peril Insurance

Commercial Multi-Peril insurance at Travelers Companies (TRV) covers property and liability for small and mid-sized firms, delivering high retention (≈85% renewal rate in 2024) and a leading U.S. market share estimated near 10% of commercial P&C premium pools. It’s a portfolio cornerstone producing strong underwriting profit — Travelers reported combined ratio ~92.5% in 2024 for commercial lines — and steady cash flow tied to GDP-linked premium growth (~2–3% CAGR). Generated cash funds digital transformation across the group, supporting a $500+ million tech investment plan announced for 2024–2026.

Commercial Automobile Insurance

Despite social inflation and higher repair costs, Travelers (Ticker: TRV) retains a massive, stable commercial auto franchise—2019–2024 combined ratio improved to ~96% after pricing and underwriting tightenings.

By 2025 pricing stabilization restored margins, making commercial auto a reliable liquidity source: roughly $1.3–1.6 billion annual underwriting profit contribution to Business Insurance.

Market maturity and Travelers’ scale let it manage frequency/severity better than regional peers and drive cross-sell into GL, workers’ comp, and risk services.

- Scale: national fleet data, large broker relationships

- Margins: combined ratio ~96% (post-2023 rate actions)

- Liquidity: ~$1.3–1.6B underwriting profit (annual)

- Role: foundational Business Insurance product; strong cross-sell

Standard Homeowners Insurance

Standard Homeowners Insurance: Travelers holds a leading, stable share in the high-value U.S. home market—personal property is a mature segment with ~12% market share in 2024 for high-net-worth policies—yielding steady margins despite weather losses by using geographic segmentation and risk-based pricing to protect profitability.

Investment is focused on agent distribution upkeep, not expansion; consistent renewals (≈85% retention in 2024) supply cash flow that funds trials of personal-lines tech like AI underwriting and digital claims triage.

- ~12% share in high-value homes (2024)

- ~85% policy renewal rate (2024)

- Pricing/geographic segmentation preserves margins vs climate risk

- Capex shifted to agent network and tech pilots

Travelers’ core lines drive steady cash: $4.2B comp, strong profits & 85% retention

Travelers’ cash cows—workers’ comp, surety, commercial multi-peril, commercial auto, and standard homeowners—generated predictable cash: ~ $4.2B workers’ comp NPW (2024), surety 12–15% US share, commercial combined ratio ~92.5% (2024), commercial auto underwriting profit ~$1.3–1.6B annually, homeowners ~85% retention (2024).

| Line | Key 2024–25 Metric |

|---|---|

| Workers’ comp | $4.2B NPW |

| Surety | 12–15% US share |

| Commercial MP | Combined ratio 92.5% |

| Commercial auto | $1.3–1.6B profit |

| Homeowners | 85% retention |

Delivered as Shown

Travelers Companies BCG Matrix

The file you're previewing is the exact Travelers Companies BCG Matrix report you'll receive after purchase—no watermarks or draft content—fully formatted for immediate use in presentations, investor meetings, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Travelers Companies’ BCG Matrix preview highlights its dominant commercial insurance lines as likely Cash Cows, emerging specialty units as potential Stars, and legacy low-growth segments edging toward Dogs—offering a snapshot of capital allocation priorities and growth levers. This concise view teases quadrant placements and strategic implications; buy the full BCG Matrix to access a quadrant-by-quadrant breakdown, data-driven recommendations, and downloadable Word and Excel files to guide investment and portfolio decisions.

Stars

Cyber Insurance Solutions

By late 2025 Travelers Companies has emerged as a leader in cyber insurance, with the global cyber insurance market projected at $30.9B in 2025 and Travelers holding an estimated 8–10% share in the US commercial segment.

The unit leverages proprietary underwriting data from ~30m commercial policies to offer comprehensive coverage in high demand across SMEs to Fortune 500s.

Heavy ongoing spend on cybersecurity R&D and real-time threat monitoring compresses near-term margins, but high market share makes it a primary growth driver.

Analysts expect this Stars unit to become a cash cow as the cyber market matures toward ~2030, with premium growth slowing and loss ratios stabilizing.

Technology Sector Business Insurance

Travelers holds a leading spot in the tech & life-sciences insurance niche, capturing an estimated 12–15% share of the US specialty tech market by 2024 and writing roughly $1.1B in related premiums in 2024; products cover software, hardware, and renewable-energy firms that need tailored liability and cyber protections. The sector’s ~8–10% CAGR keeps new premium inflows robust, but Travelers must keep investing in specialist claims teams and tech-driven underwriting to fend off nimble fintech entrants.

Excess and Surplus Lines

Through Northfield and specialty units, Travelers captured notable share in the hard market of 2024–2025, growing excess & surplus (E&S) written premiums by about 28% year-over-year to roughly $3.2 billion in 2025, per company segment disclosures.

As standard carriers withdrew from volatile sectors, E&S supplied coverage for unique/high-capacity risks, driving a combined ratio advantage near 92 in 2025 while requiring elevated statutory capital—about 15% of Travelers’ allocated commercial capital—to back volatility.

The segment’s high growth and pricing power made it a Stars quadrant fit in the BCG matrix: strong market growth and high relative share, generating substantial premium income but needing continued capital intensity and active risk selection.

Management and Professional Liability

Management and Professional Liability has surged in the mid-2020s as corporate governance and employment-practice claims rose; Travelers holds a leading share in Directors & Officers (D&O) and Employment Practices Liability Insurance (EPLI), with 2024 segment premiums around $1.1B, up ~8% year-over-year.

The complexity lets Travelers charge premium pricing while global market growth continues; maintaining this position requires ongoing investment in legal teams and actuarial modeling to track regulatory changes and loss trends.

- 2024 segment premiums ~$1.1B, +8% YoY

- Leading share in D&O and EPLI markets

- Premium pricing enabled by complex risk profiles

- Ongoing legal and actuarial investment required

Middle Market International Expansion

Travelers has grown middle-market commercial share in Canada, the UK and Ireland, lifting international commercial premiums to about $1.8B in 2024, with mid‑single-digit CAGR since 2019, driven by package-based products where Travelers leads.

Infrastructure costs are high—estimated incremental SG&A of ~$120–150M to scale—but revenue growth in these markets outpaced US mature segments in 2023–24, reducing US concentration risk for long‑term revenue.

- International commercial premiums ≈ $1.8B (2024)

- Mid‑single‑digit CAGR since 2019

- Incremental SG&A ~$120–150M to scale

- Package products driving share gains in Canada/UK/Ireland

Travelers' Specialty Units Drive High Growth: Leading Shares in Cyber, Tech, E&S

Travelers’ Stars units (cyber, tech/life‑sciences, E&S, D&O/EPLI) show high growth and leading share: cyber ~$30.9B market (2025) with Travelers 8–10% US share; tech specialty ~$1.1B premiums (2024); E&S ~$3.2B premiums (2025); D&O/EPLI ~$1.1B (2024); international commercial ~$1.8B (2024).

| Unit | Key metric |

|---|---|

| Cyber | $30.9B market (2025); 8–10% US share |

| Tech | $1.1B premiums (2024) |

| E&S | $3.2B premiums (2025) |

| D&O/EPLI | $1.1B premiums (2024) |

| Intl Commercial | $1.8B premiums (2024) |

What is included in the product

BCG Matrix of Travelers: strategic placement of insurance lines as Stars, Cash Cows, Question Marks, and Dogs with investment and divestment guidance.

One-page BCG Matrix placing Travelers' business units into clear quadrants for executive decision-making and portfolio optimization.

Cash Cows

Workers Compensation

Travelers is the US market leader in workers compensation, leveraging decades of proprietary claims data to price risk; in 2024 the segment generated roughly $4.2 billion in net premiums written, delivering steady underwriting gains. This mature line produces predictable cash flow that funds dividends and share buybacks—Travelers returned $3.1 billion to shareholders in 2024. Minimal promotional spend keeps expense ratios low, so the focus is on operational efficiency and medical cost containment to protect margins.

Surety and Fidelity Bonds

As one of the largest surety writers globally, Travelers (TRV) holds ~12–15% market share in US surety as of 2024, giving it a dominant position in a high-barrier sector tied to licensing, capital and relationships.

The mature surety market tracks infrastructure and construction cycles, delivering steady premiums and historically low loss ratios (~20–30% combined ratio on surety lines in 2023), so returns are reliable.

Surety needs little new capital, freeing cash—Travelers redirected roughly $400–600M annually (2022–2024) to higher-growth units—while its AA financial strength rating makes it preferred for large government and private contracts.

Commercial Multi-Peril Insurance

Commercial Multi-Peril insurance at Travelers Companies (TRV) covers property and liability for small and mid-sized firms, delivering high retention (≈85% renewal rate in 2024) and a leading U.S. market share estimated near 10% of commercial P&C premium pools. It’s a portfolio cornerstone producing strong underwriting profit — Travelers reported combined ratio ~92.5% in 2024 for commercial lines — and steady cash flow tied to GDP-linked premium growth (~2–3% CAGR). Generated cash funds digital transformation across the group, supporting a $500+ million tech investment plan announced for 2024–2026.

Commercial Automobile Insurance

Despite social inflation and higher repair costs, Travelers (Ticker: TRV) retains a massive, stable commercial auto franchise—2019–2024 combined ratio improved to ~96% after pricing and underwriting tightenings.

By 2025 pricing stabilization restored margins, making commercial auto a reliable liquidity source: roughly $1.3–1.6 billion annual underwriting profit contribution to Business Insurance.

Market maturity and Travelers’ scale let it manage frequency/severity better than regional peers and drive cross-sell into GL, workers’ comp, and risk services.

- Scale: national fleet data, large broker relationships

- Margins: combined ratio ~96% (post-2023 rate actions)

- Liquidity: ~$1.3–1.6B underwriting profit (annual)

- Role: foundational Business Insurance product; strong cross-sell

Standard Homeowners Insurance

Standard Homeowners Insurance: Travelers holds a leading, stable share in the high-value U.S. home market—personal property is a mature segment with ~12% market share in 2024 for high-net-worth policies—yielding steady margins despite weather losses by using geographic segmentation and risk-based pricing to protect profitability.

Investment is focused on agent distribution upkeep, not expansion; consistent renewals (≈85% retention in 2024) supply cash flow that funds trials of personal-lines tech like AI underwriting and digital claims triage.

- ~12% share in high-value homes (2024)

- ~85% policy renewal rate (2024)

- Pricing/geographic segmentation preserves margins vs climate risk

- Capex shifted to agent network and tech pilots

Travelers’ core lines drive steady cash: $4.2B comp, strong profits & 85% retention

Travelers’ cash cows—workers’ comp, surety, commercial multi-peril, commercial auto, and standard homeowners—generated predictable cash: ~ $4.2B workers’ comp NPW (2024), surety 12–15% US share, commercial combined ratio ~92.5% (2024), commercial auto underwriting profit ~$1.3–1.6B annually, homeowners ~85% retention (2024).

| Line | Key 2024–25 Metric |

|---|---|

| Workers’ comp | $4.2B NPW |

| Surety | 12–15% US share |

| Commercial MP | Combined ratio 92.5% |

| Commercial auto | $1.3–1.6B profit |

| Homeowners | 85% retention |

Delivered as Shown

Travelers Companies BCG Matrix

The file you're previewing is the exact Travelers Companies BCG Matrix report you'll receive after purchase—no watermarks or draft content—fully formatted for immediate use in presentations, investor meetings, or strategic planning.