Travis Perkins PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Travis Perkins reveals how political shifts, economic cycles, social trends, and environmental regulations converge to shape the builder merchant’s strategy and risk profile; use these findings to anticipate disruptions and identify growth levers. Download the full, ready-to-use report to get granular insights, actionable recommendations, and editable charts for immediate strategic or investment use.

Political factors

UK Government Housing Targets

The Labour government’s target to deliver 1.5 million homes over this parliament (roughly 375,000 homes/year) creates a multi-year demand uplift for building materials, benefiting Travis Perkins whose merchanting revenues reached £3.2bn in FY2024; aligning distribution, inventory and supplier contracts to support large-scale residential projects is essential to capture share of an estimated £60–80bn annual UK construction materials market.

Planning System Reforms

Proposed reforms to the National Planning Policy Framework aim to cut planning times by up to 30%, streamlining approvals for infrastructure and housing projects and targeting faster consents by 2025.

Faster permissions will reduce delays for Travis Perkins’ core trade and contractor customers, lowering project lead-time risk and supporting higher order consistency.

Regulators expect a 12–18% rise in active construction sites by late 2025, which could boost market demand for Travis Perkins’ products and services.

Public Sector Infrastructure Spending

Government investment in schools, hospitals and social housing—UK public capital spending of £134bn planned for 2024/25—remains a key revenue driver for Travis Perkins Commercial, directly fueling demand for heavy building materials.

Autumn Budget shifts to capital expenditure alter procurement cycles; a 3.2% real-terms cut in some departmental budgets in 2024 shortened project pipelines and compressed order lead times for suppliers.

Travis Perkins leverages its 600+ UK branches and national logistics to service geographically dispersed public works, enabling faster fulfilment and supporting an estimated 12% of its merchant revenues tied to public-sector projects.

Post-Brexit Trade Relations

Ongoing post-Brexit trade adjustments affect costs and availability of imported timber and specialist components for Travis Perkins; UK timber imports fell 12% in 2024 versus 2019, raising input-cost pressure amid a 2024 gross margin of 19.8% (Travis Perkins plc reports).

Despite diversified sourcing, shifts in customs protocols or tariffs could trigger inventory-price volatility—import duties or delays added estimated £25–40/tonne to timber landed costs in 2023–24.

Monitoring diplomatic shifts is essential to protect competitive margins across a supply chain where 40% of key fittings remain EU-sourced.

- UK timber imports down 12% (2019–2024)

- 2024 gross margin 19.8%

- Added landed cost £25–40/tonne (2023–24)

- ~40% of key fittings sourced from EU

Devolved Administration Policies

- Localized regs: Scotland, Wales, NI

- Subsidies: energy efficiency & social housing

- Product mix: insulation, low-carbon materials, retrofit services

- 2024 UK revenue context: ~£3.8bn

UK housing push boosts materials demand; Travis Perkins sees £3.8bn UK revenue, margins hit

Housing target 1.5m homes lifts materials demand; Travis Perkins merchant revenues £3.2bn (FY2024) and group UK revenue ~£3.8bn (2024). Public capex £134bn (2024/25) and +12–18% construction sites by late 2025 support commercial volumes. UK timber imports -12% (2019–24) raised landed costs £25–40/tonne; ~40% fittings EU-sourced, impacting margins (gross margin 19.8% 2024).

| Metric | Value |

|---|---|

| Merchant revenues FY2024 | £3.2bn |

| Group UK revenue 2024 | ~£3.8bn |

| Public capex 2024/25 | £134bn |

| Timber imports change 2019–24 | -12% |

| Added timber landed cost | £25–40/tonne |

| Gross margin 2024 | 19.8% |

| Fittings EU-sourced | ~40% |

What is included in the product

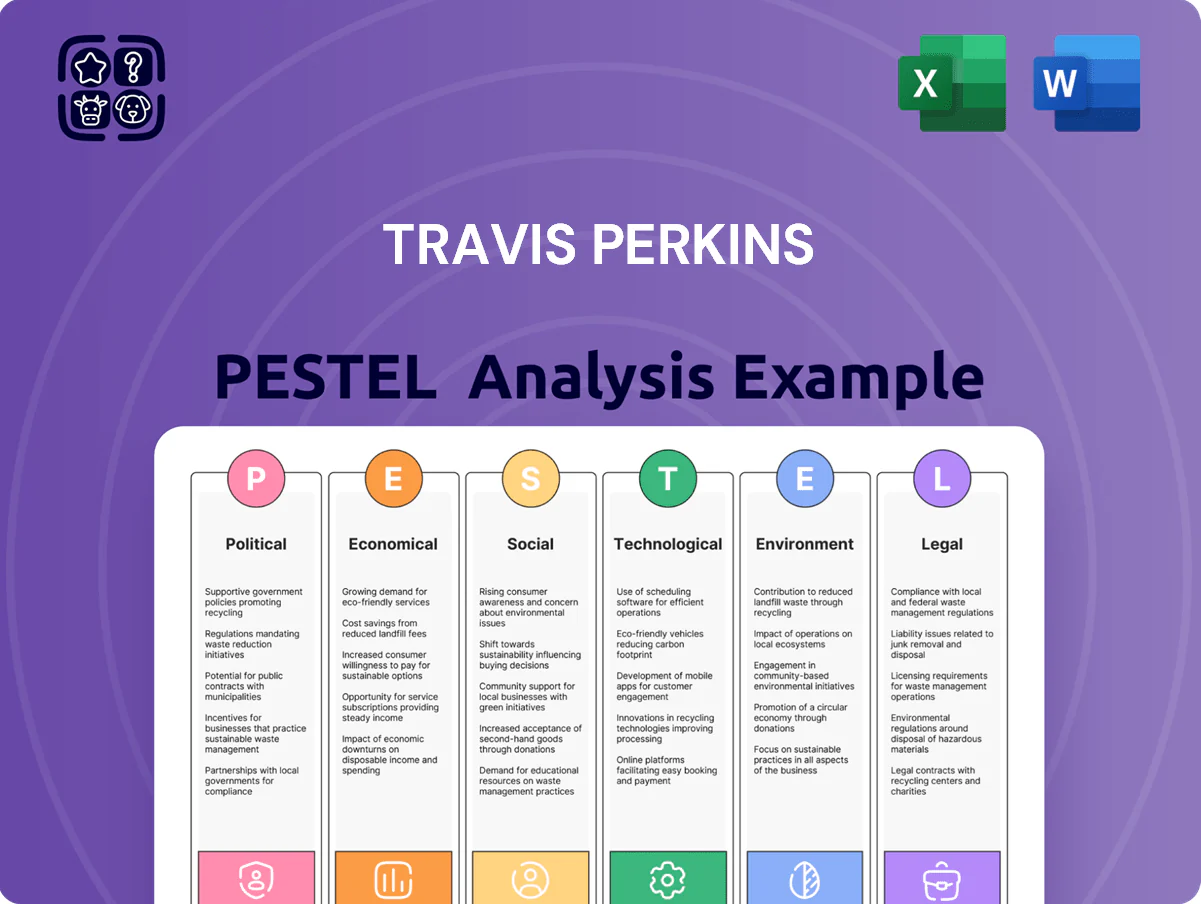

Explores how external macro-environmental factors uniquely affect Travis Perkins across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting tailored for executives, investors, and consultants to identify risks and opportunities within its UK construction-supply market.

Provides a clean, summarized Travis Perkins PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Interest Rate Environment

The Bank of England's policy rate, which peaked at 5.25% in August 2023 and remained around 5% through 2024, directly affects mortgage costs and consumer confidence in the repair, maintenance and improvement market.

Higher rates suppressed DIY and major renovations as average variable mortgage rates rose above 5.5%, reducing disposable income and housing turnover.

Mortgage approvals fell c.20% year-on-year in 2024, hitting housing transaction volumes and Travis Perkins' end market.

As markets priced a gradual easing toward late 2025, forecasts showed a modest rebound in approvals and transactions supporting recovery in demand.

Inflation and Input Costs

Fluctuations in energy prices and raw material costs, notably a 12% year-on-year rise in steel and a 7% increase in cement input costs in 2024, compressed Travis Perkins group gross margins in merchanting segments.

The company deployed dynamic pricing and weekly index-linked adjustments to pass through inflation, contributing to a 1.8ppt gross margin recovery in H2 2024 versus H1.

Sustained wage inflation—UK average construction pay growth of ~6% in 2024—raised branch and delivery fleet overheads, increasing operating costs by an estimated £35–45m annually.

UK GDP Growth and Construction Output

UK GDP grew 0.1% Q4 2025 and 0.6% year‑on‑year to Q4 2025, with construction output down 2.0% year‑on‑year in 2025, curbing new‑build starts and capital expenditure in commercial and residential projects.

Sluggish growth has shifted demand toward repair and maintenance; Travis Perkins reported in 2025 increased sales mix to trade maintenance products and uses GDP and construction PMI data to adjust inventory and capex forecasts.

Consumer Disposable Income

The financial health of UK households directly affects demand for Travis Perkins retail brands; UK real household disposable income fell 0.2% in 2023 and remained 2.5% below pre-COVID levels in 2024, weakening DIY and landscaping spend.

When disposable income is squeezed by high living costs—CPI at 4.0% in 2024—discretionary home-improvement purchases fall, prompting lower basket sizes and volume declines in consumer-facing categories.

Travis Perkins mitigates this through value-focused ranges, promotional pricing and trade credit—trade receivables financing supported c.£1.1bn of customer credit facilities in FY 2024—preserving market share.

- Household disposable income: -0.2% (2023); -2.5% vs pre-COVID (2024)

- UK CPI: ~4.0% (2024) — reduces discretionary spend

- Trade credit facilities: ~£1.1bn supporting trade customers (FY 2024)

Labor Market Shortages

A persistent shortage of skilled tradespeople in the UK construction sector—estimated at around 220,000 workers short in 2024—slows project completion for Travis Perkins customers and caps the addressable market despite high material demand.

Travis Perkins invests in training programs and tool-hire services; in FY2024 it increased training spend and tool-hire revenue accounted for roughly 6–8% of merchanting sales, helping smaller contractors boost productivity.

- UK skilled trades gap ~220,000 (2024)

- Slower project completion reduces TAM despite material demand

- Training investment up in FY2024

- Tool-hire ~6–8% of merchanting sales

Higher rates slam housing demand; input and wage inflation squeeze margins, trade credit cushions

Higher Bank Rate (~5% in 2024) cut housing transactions (mortgage approvals -20% y/y 2024) and DIY spend; input cost inflation (steel +12%, cement +7% 2024) squeezed margins despite price pass-through; wage inflation (~6% construction pay 2024) added ~£35–45m opex; trade credit ~£1.1bn and tool‑hire (6–8% merchant sales) mitigated demand weakness.

| Metric | 2024 |

|---|---|

| Bank Rate | ~5% |

| Mortgage approvals | -20% y/y |

| Steel/cement | +12% / +7% |

| Construction pay | ~6% |

| Trade credit | £1.1bn |

Preview the Actual Deliverable

Travis Perkins PESTLE Analysis

The preview shown here is the exact Travis Perkins PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or reporting.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Travis Perkins reveals how political shifts, economic cycles, social trends, and environmental regulations converge to shape the builder merchant’s strategy and risk profile; use these findings to anticipate disruptions and identify growth levers. Download the full, ready-to-use report to get granular insights, actionable recommendations, and editable charts for immediate strategic or investment use.

Political factors

UK Government Housing Targets

The Labour government’s target to deliver 1.5 million homes over this parliament (roughly 375,000 homes/year) creates a multi-year demand uplift for building materials, benefiting Travis Perkins whose merchanting revenues reached £3.2bn in FY2024; aligning distribution, inventory and supplier contracts to support large-scale residential projects is essential to capture share of an estimated £60–80bn annual UK construction materials market.

Planning System Reforms

Proposed reforms to the National Planning Policy Framework aim to cut planning times by up to 30%, streamlining approvals for infrastructure and housing projects and targeting faster consents by 2025.

Faster permissions will reduce delays for Travis Perkins’ core trade and contractor customers, lowering project lead-time risk and supporting higher order consistency.

Regulators expect a 12–18% rise in active construction sites by late 2025, which could boost market demand for Travis Perkins’ products and services.

Public Sector Infrastructure Spending

Government investment in schools, hospitals and social housing—UK public capital spending of £134bn planned for 2024/25—remains a key revenue driver for Travis Perkins Commercial, directly fueling demand for heavy building materials.

Autumn Budget shifts to capital expenditure alter procurement cycles; a 3.2% real-terms cut in some departmental budgets in 2024 shortened project pipelines and compressed order lead times for suppliers.

Travis Perkins leverages its 600+ UK branches and national logistics to service geographically dispersed public works, enabling faster fulfilment and supporting an estimated 12% of its merchant revenues tied to public-sector projects.

Post-Brexit Trade Relations

Ongoing post-Brexit trade adjustments affect costs and availability of imported timber and specialist components for Travis Perkins; UK timber imports fell 12% in 2024 versus 2019, raising input-cost pressure amid a 2024 gross margin of 19.8% (Travis Perkins plc reports).

Despite diversified sourcing, shifts in customs protocols or tariffs could trigger inventory-price volatility—import duties or delays added estimated £25–40/tonne to timber landed costs in 2023–24.

Monitoring diplomatic shifts is essential to protect competitive margins across a supply chain where 40% of key fittings remain EU-sourced.

- UK timber imports down 12% (2019–2024)

- 2024 gross margin 19.8%

- Added landed cost £25–40/tonne (2023–24)

- ~40% of key fittings sourced from EU

Devolved Administration Policies

- Localized regs: Scotland, Wales, NI

- Subsidies: energy efficiency & social housing

- Product mix: insulation, low-carbon materials, retrofit services

- 2024 UK revenue context: ~£3.8bn

UK housing push boosts materials demand; Travis Perkins sees £3.8bn UK revenue, margins hit

Housing target 1.5m homes lifts materials demand; Travis Perkins merchant revenues £3.2bn (FY2024) and group UK revenue ~£3.8bn (2024). Public capex £134bn (2024/25) and +12–18% construction sites by late 2025 support commercial volumes. UK timber imports -12% (2019–24) raised landed costs £25–40/tonne; ~40% fittings EU-sourced, impacting margins (gross margin 19.8% 2024).

| Metric | Value |

|---|---|

| Merchant revenues FY2024 | £3.2bn |

| Group UK revenue 2024 | ~£3.8bn |

| Public capex 2024/25 | £134bn |

| Timber imports change 2019–24 | -12% |

| Added timber landed cost | £25–40/tonne |

| Gross margin 2024 | 19.8% |

| Fittings EU-sourced | ~40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Travis Perkins across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting tailored for executives, investors, and consultants to identify risks and opportunities within its UK construction-supply market.

Provides a clean, summarized Travis Perkins PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Interest Rate Environment

The Bank of England's policy rate, which peaked at 5.25% in August 2023 and remained around 5% through 2024, directly affects mortgage costs and consumer confidence in the repair, maintenance and improvement market.

Higher rates suppressed DIY and major renovations as average variable mortgage rates rose above 5.5%, reducing disposable income and housing turnover.

Mortgage approvals fell c.20% year-on-year in 2024, hitting housing transaction volumes and Travis Perkins' end market.

As markets priced a gradual easing toward late 2025, forecasts showed a modest rebound in approvals and transactions supporting recovery in demand.

Inflation and Input Costs

Fluctuations in energy prices and raw material costs, notably a 12% year-on-year rise in steel and a 7% increase in cement input costs in 2024, compressed Travis Perkins group gross margins in merchanting segments.

The company deployed dynamic pricing and weekly index-linked adjustments to pass through inflation, contributing to a 1.8ppt gross margin recovery in H2 2024 versus H1.

Sustained wage inflation—UK average construction pay growth of ~6% in 2024—raised branch and delivery fleet overheads, increasing operating costs by an estimated £35–45m annually.

UK GDP Growth and Construction Output

UK GDP grew 0.1% Q4 2025 and 0.6% year‑on‑year to Q4 2025, with construction output down 2.0% year‑on‑year in 2025, curbing new‑build starts and capital expenditure in commercial and residential projects.

Sluggish growth has shifted demand toward repair and maintenance; Travis Perkins reported in 2025 increased sales mix to trade maintenance products and uses GDP and construction PMI data to adjust inventory and capex forecasts.

Consumer Disposable Income

The financial health of UK households directly affects demand for Travis Perkins retail brands; UK real household disposable income fell 0.2% in 2023 and remained 2.5% below pre-COVID levels in 2024, weakening DIY and landscaping spend.

When disposable income is squeezed by high living costs—CPI at 4.0% in 2024—discretionary home-improvement purchases fall, prompting lower basket sizes and volume declines in consumer-facing categories.

Travis Perkins mitigates this through value-focused ranges, promotional pricing and trade credit—trade receivables financing supported c.£1.1bn of customer credit facilities in FY 2024—preserving market share.

- Household disposable income: -0.2% (2023); -2.5% vs pre-COVID (2024)

- UK CPI: ~4.0% (2024) — reduces discretionary spend

- Trade credit facilities: ~£1.1bn supporting trade customers (FY 2024)

Labor Market Shortages

A persistent shortage of skilled tradespeople in the UK construction sector—estimated at around 220,000 workers short in 2024—slows project completion for Travis Perkins customers and caps the addressable market despite high material demand.

Travis Perkins invests in training programs and tool-hire services; in FY2024 it increased training spend and tool-hire revenue accounted for roughly 6–8% of merchanting sales, helping smaller contractors boost productivity.

- UK skilled trades gap ~220,000 (2024)

- Slower project completion reduces TAM despite material demand

- Training investment up in FY2024

- Tool-hire ~6–8% of merchanting sales

Higher rates slam housing demand; input and wage inflation squeeze margins, trade credit cushions

Higher Bank Rate (~5% in 2024) cut housing transactions (mortgage approvals -20% y/y 2024) and DIY spend; input cost inflation (steel +12%, cement +7% 2024) squeezed margins despite price pass-through; wage inflation (~6% construction pay 2024) added ~£35–45m opex; trade credit ~£1.1bn and tool‑hire (6–8% merchant sales) mitigated demand weakness.

| Metric | 2024 |

|---|---|

| Bank Rate | ~5% |

| Mortgage approvals | -20% y/y |

| Steel/cement | +12% / +7% |

| Construction pay | ~6% |

| Trade credit | £1.1bn |

Preview the Actual Deliverable

Travis Perkins PESTLE Analysis

The preview shown here is the exact Travis Perkins PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or reporting.