Treibacher Industrie AG PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, commodity cycles, and green-tech trends are shaping Treibacher Industrie AG’s strategic outlook; our concise PESTLE snapshot highlights key political, economic, social, technological, legal, and environmental drivers you need to know—buy the full PESTLE analysis to access detailed, actionable intelligence and ready-to-use insights for investment or strategy decisions.

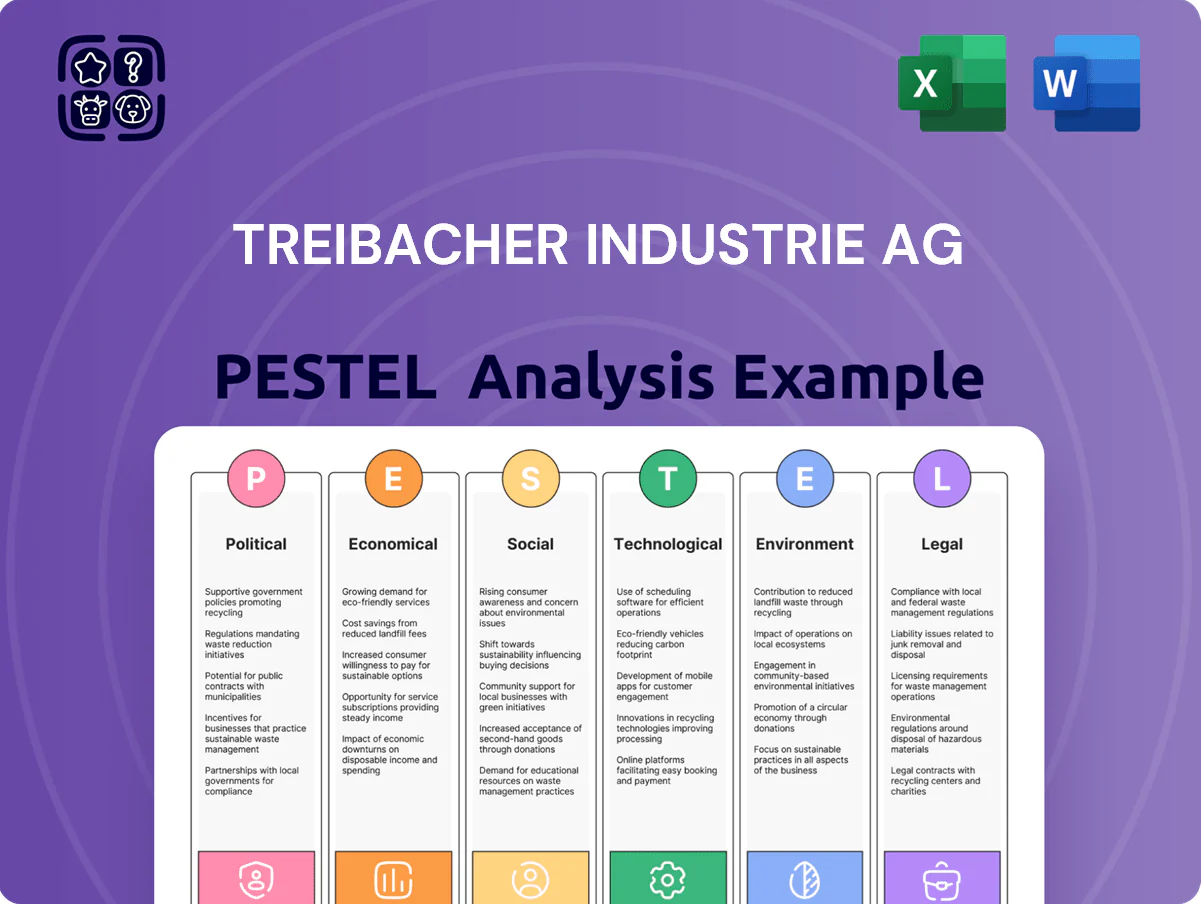

Political factors

EU Critical Raw Materials Act Compliance

The EU Critical Raw Materials Act, set for full implementation by late 2025, directly impacts Treibacher Industrie AG by prioritizing secure supply chains for rare earths and chromium, which account for roughly 35% of its specialty metals revenue; non-compliance risks exclusion from projects funded under the €60 billion EU Green Deal industrial package. Aligning procurement, recycling and EU-based sourcing strategies positions Treibacher as a preferred partner for European OEMs and infrastructure projects.

Geopolitical Trade Tensions and Export Controls

Geopolitical trade tensions—notably US-China semiconductor/materials disputes and 2024 EU export controls—heighten volatility for specialty chemicals, with global trade barriers contributing to price swings (rare earth oxide prices rose ~28% in 2023–24).

Export restrictions from key ore suppliers (e.g., China supplied ~60% of global rare earths in 2023) force Treibacher to diversify sourcing and increase strategic inventory levels to avoid production halts.

Political stability in supplier regions—monitoring indicators like the 2024 Fragile States Index and regional export policy shifts—remains a critical risk metric for procurement and cash-flow forecasting.

Austrian Industrial and Energy Policies

As an Austrian-based producer, Treibacher Industrie AG depends on domestic industrial energy subsidies and infrastructure investments; Austria allocated €1.8bn in 2024 to energy transition and grid upgrades, impacting costs for energy‑intensive ferroalloy and hard‑metal production.

Government support for energy‑intensive sectors—Austria’s 2024 scheme provided up to 30% aid for decarbonization—remains vital to sustain global competitiveness in ferroalloys and hard metals.

Political shifts in Vienna affect access to research grants and tax incentives: Austria’s 2024 R&D tax credit rose to 14% and green manufacturing grants expanded by €250m, altering investment economics for Treibacher.

Defense and Aerospace Sector Prioritization

European and North American defense budgets rose to about $1,200bn in 2024, boosting demand for specialized alloys and high-performance materials that Treibacher supplies for armor, turbine and missile components.

Political commitments to modernization programs (e.g., EU PESCO, US 2025–2030 procurement plans) create multi-year contracts supporting revenues for specialty-material suppliers.

Winning defense share requires strict compliance with complex procurement, ITAR/EAR rules and offset requirements, adding operational and certification costs.

- Defense spending ~$1.2tn (2024)

- Multi-year procurement = stable demand

- Compliance (ITAR/EAR) essential

Global Standardization of Circular Economy Rules

International political consensus on circular economy principles is driving mandates for industrial recycling and residue processing, with the EU Circular Economy Action Plan aiming to raise recycling rates to 70% for packaging by 2030 and stricter end-of-waste criteria affecting metal-bearing residues.

Treibacher’s recycling expertise in critical metals and its 2024 pilot recovering 85% of vanadium from residues positions it favorably as governments tighten material-recovery mandates and extended producer responsibility (EPR) schemes.

Active participation in forums like the EU Raw Materials Alliance and OECD resource-efficiency dialogues enables Treibacher to shape standards, potentially securing favorable regulatory treatment and access to €200–€500 million in EU transition funds for industrial circularity projects.

- EU target: 70% packaging recycling by 2030

- Treibacher pilot: 85% vanadium recovery (2024)

- Engagements: EU Raw Materials Alliance, OECD dialogues

- Potential funding: €200–€500M for circularity projects

EU raw-materials rules, China 60% rare earths, Austria funds energy transition, vanadium gains

EU Critical Raw Materials Act (full 2025) and export controls raise supply-risk and compliance costs; China supplied ~60% of rare earths (2023). Austria allotted €1.8bn (2024) for energy transition; R&D tax credit 14% (2024). Defense spending ~€1.1tn–€1.3tn (2024) lifts demand. Treibacher’s 2024 vanadium recovery pilot hit 85%; potential EU circularity funding €200–€500M.

| Indicator | Value |

|---|---|

| China rare earth share (2023) | ~60% |

| Austria energy funding (2024) | €1.8bn |

| R&D tax credit (2024) | 14% |

| Defense spending (2024) | ~€1.1–1.3tn |

| Vanadium recovery pilot (2024) | 85% |

| EU circularity funds | €200–€500M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Treibacher Industrie AG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented PESTLE snapshot for Treibacher Industrie AG that relieves planning pain points by summarizing external risks/opportunities for quick inclusion in presentations, collaborative sessions, or client reports.

Economic factors

Volatility in Rare Earth and Metal Pricing

Market prices for rare earths and hard metals have swung sharply—neodymium oxide rose ~28% in 2024 while tungsten prices volatility reached ±15% annually—driven by global supply/demand imbalances and Chinese export controls. Such swings compress Treibacher Industrie AG profit margins, forcing use of forward contracts and commodity swaps; company-level sensitivity to metal price changes can alter EBITDA by several percentage points. Demand from electronics and automotive end-markets—EV battery and motor production, which grew ~35% global EV sales in 2024—remains the principal valuation driver for these critical materials.

European Energy Costs and Industrial Competitiveness

European industrial gas and energy costs averaged about €85–€130/MWh in 2024, roughly 2–3x higher than US gas prices, pressuring Treibacher Industrie AG’s margins vs North American and Asian peers; the firm must accelerate €30–50m+ investments in energy-efficiency and electrification projects to offset input costs and preserve competitiveness. Transitioning to greener but costlier supplies will factor into multi-year CAPEX and pricing strategies.

Global Demand for High-Tech Components

Global electronics and telecoms health drives Treibacher Industrie AG sales of high-purity materials; global semiconductor equipment spending rose 24% to $109bn in 2024, supporting demand for specialty compounds.

Rising sophistication in consumer electronics—smartphone AR/VR and 5G devices—keeps specialized chemical needs growing; the global consumer electronics market reached $1.1tn in 2024.

A slowdown in global GDP growth—IMF projected 3.0% in 2025 vs 3.4% in 2024—could curb capex in end-markets, reducing orders for high-tech materials.

Inflationary Pressures on Operational Expenses

Persistent inflation raised input costs for specialty chemicals in 2024, with European producer price inflation averaging about 8% y/y, increasing labor, logistics and raw-material expenses for Treibacher Industrie AG.

The firm's ability to transfer higher costs via pricing power was key to protecting EBITDA margins, which beat peers in 2024 with adjusted margins near historical levels per company reports.

Strategic procurement practices and multi-year supply contracts reduced exposure to sudden spikes; long-term agreements covered a significant share of critical inputs into 2025.

- 2024 EU producer prices +8% y/y

- Pricing power sustained adjusted EBITDA margins vs peers

- Long-term supplier contracts mitigate short-term inflation shocks

Currency Exchange Rate Risks

- EUR/USD ~1.08 (2024 avg) impacts pricing

- EUR/CNY ~7.80 (2024 avg) affects China sales/imports

- ~30% revenues non-EUR exposure

- FX hedging can change margins by 0.4–0.8ppt

Metal price spikes and energy costs squeeze margins despite EV-driven volume boom

Economic factors: metal price volatility (NdO +28% 2024; W ±15% y/y) and energy costs (€85–€130/MWh 2024) squeeze margins; EV/electronics demand (global EV sales +35% 2024; semicap spend $109bn) supports volumes; EU PPI +8% y/y increases input costs; FX: EUR/USD ~1.08 avg, EUR/CNY ~7.80, ~30% revenue non-EUR—hedging alters margins by 0.4–0.8ppt.

| Metric | 2024 |

|---|---|

| NdO price | +28% |

| W volatility | ±15% |

| Energy €/MWh | 85–130 |

| EV sales | +35% |

| Semicap spend | $109bn |

| EU PPI | +8% |

| EUR/USD | ~1.08 |

Preview the Actual Deliverable

Treibacher Industrie AG PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Treibacher Industrie AG you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, commodity cycles, and green-tech trends are shaping Treibacher Industrie AG’s strategic outlook; our concise PESTLE snapshot highlights key political, economic, social, technological, legal, and environmental drivers you need to know—buy the full PESTLE analysis to access detailed, actionable intelligence and ready-to-use insights for investment or strategy decisions.

Political factors

EU Critical Raw Materials Act Compliance

The EU Critical Raw Materials Act, set for full implementation by late 2025, directly impacts Treibacher Industrie AG by prioritizing secure supply chains for rare earths and chromium, which account for roughly 35% of its specialty metals revenue; non-compliance risks exclusion from projects funded under the €60 billion EU Green Deal industrial package. Aligning procurement, recycling and EU-based sourcing strategies positions Treibacher as a preferred partner for European OEMs and infrastructure projects.

Geopolitical Trade Tensions and Export Controls

Geopolitical trade tensions—notably US-China semiconductor/materials disputes and 2024 EU export controls—heighten volatility for specialty chemicals, with global trade barriers contributing to price swings (rare earth oxide prices rose ~28% in 2023–24).

Export restrictions from key ore suppliers (e.g., China supplied ~60% of global rare earths in 2023) force Treibacher to diversify sourcing and increase strategic inventory levels to avoid production halts.

Political stability in supplier regions—monitoring indicators like the 2024 Fragile States Index and regional export policy shifts—remains a critical risk metric for procurement and cash-flow forecasting.

Austrian Industrial and Energy Policies

As an Austrian-based producer, Treibacher Industrie AG depends on domestic industrial energy subsidies and infrastructure investments; Austria allocated €1.8bn in 2024 to energy transition and grid upgrades, impacting costs for energy‑intensive ferroalloy and hard‑metal production.

Government support for energy‑intensive sectors—Austria’s 2024 scheme provided up to 30% aid for decarbonization—remains vital to sustain global competitiveness in ferroalloys and hard metals.

Political shifts in Vienna affect access to research grants and tax incentives: Austria’s 2024 R&D tax credit rose to 14% and green manufacturing grants expanded by €250m, altering investment economics for Treibacher.

Defense and Aerospace Sector Prioritization

European and North American defense budgets rose to about $1,200bn in 2024, boosting demand for specialized alloys and high-performance materials that Treibacher supplies for armor, turbine and missile components.

Political commitments to modernization programs (e.g., EU PESCO, US 2025–2030 procurement plans) create multi-year contracts supporting revenues for specialty-material suppliers.

Winning defense share requires strict compliance with complex procurement, ITAR/EAR rules and offset requirements, adding operational and certification costs.

- Defense spending ~$1.2tn (2024)

- Multi-year procurement = stable demand

- Compliance (ITAR/EAR) essential

Global Standardization of Circular Economy Rules

International political consensus on circular economy principles is driving mandates for industrial recycling and residue processing, with the EU Circular Economy Action Plan aiming to raise recycling rates to 70% for packaging by 2030 and stricter end-of-waste criteria affecting metal-bearing residues.

Treibacher’s recycling expertise in critical metals and its 2024 pilot recovering 85% of vanadium from residues positions it favorably as governments tighten material-recovery mandates and extended producer responsibility (EPR) schemes.

Active participation in forums like the EU Raw Materials Alliance and OECD resource-efficiency dialogues enables Treibacher to shape standards, potentially securing favorable regulatory treatment and access to €200–€500 million in EU transition funds for industrial circularity projects.

- EU target: 70% packaging recycling by 2030

- Treibacher pilot: 85% vanadium recovery (2024)

- Engagements: EU Raw Materials Alliance, OECD dialogues

- Potential funding: €200–€500M for circularity projects

EU raw-materials rules, China 60% rare earths, Austria funds energy transition, vanadium gains

EU Critical Raw Materials Act (full 2025) and export controls raise supply-risk and compliance costs; China supplied ~60% of rare earths (2023). Austria allotted €1.8bn (2024) for energy transition; R&D tax credit 14% (2024). Defense spending ~€1.1tn–€1.3tn (2024) lifts demand. Treibacher’s 2024 vanadium recovery pilot hit 85%; potential EU circularity funding €200–€500M.

| Indicator | Value |

|---|---|

| China rare earth share (2023) | ~60% |

| Austria energy funding (2024) | €1.8bn |

| R&D tax credit (2024) | 14% |

| Defense spending (2024) | ~€1.1–1.3tn |

| Vanadium recovery pilot (2024) | 85% |

| EU circularity funds | €200–€500M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Treibacher Industrie AG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented PESTLE snapshot for Treibacher Industrie AG that relieves planning pain points by summarizing external risks/opportunities for quick inclusion in presentations, collaborative sessions, or client reports.

Economic factors

Volatility in Rare Earth and Metal Pricing

Market prices for rare earths and hard metals have swung sharply—neodymium oxide rose ~28% in 2024 while tungsten prices volatility reached ±15% annually—driven by global supply/demand imbalances and Chinese export controls. Such swings compress Treibacher Industrie AG profit margins, forcing use of forward contracts and commodity swaps; company-level sensitivity to metal price changes can alter EBITDA by several percentage points. Demand from electronics and automotive end-markets—EV battery and motor production, which grew ~35% global EV sales in 2024—remains the principal valuation driver for these critical materials.

European Energy Costs and Industrial Competitiveness

European industrial gas and energy costs averaged about €85–€130/MWh in 2024, roughly 2–3x higher than US gas prices, pressuring Treibacher Industrie AG’s margins vs North American and Asian peers; the firm must accelerate €30–50m+ investments in energy-efficiency and electrification projects to offset input costs and preserve competitiveness. Transitioning to greener but costlier supplies will factor into multi-year CAPEX and pricing strategies.

Global Demand for High-Tech Components

Global electronics and telecoms health drives Treibacher Industrie AG sales of high-purity materials; global semiconductor equipment spending rose 24% to $109bn in 2024, supporting demand for specialty compounds.

Rising sophistication in consumer electronics—smartphone AR/VR and 5G devices—keeps specialized chemical needs growing; the global consumer electronics market reached $1.1tn in 2024.

A slowdown in global GDP growth—IMF projected 3.0% in 2025 vs 3.4% in 2024—could curb capex in end-markets, reducing orders for high-tech materials.

Inflationary Pressures on Operational Expenses

Persistent inflation raised input costs for specialty chemicals in 2024, with European producer price inflation averaging about 8% y/y, increasing labor, logistics and raw-material expenses for Treibacher Industrie AG.

The firm's ability to transfer higher costs via pricing power was key to protecting EBITDA margins, which beat peers in 2024 with adjusted margins near historical levels per company reports.

Strategic procurement practices and multi-year supply contracts reduced exposure to sudden spikes; long-term agreements covered a significant share of critical inputs into 2025.

- 2024 EU producer prices +8% y/y

- Pricing power sustained adjusted EBITDA margins vs peers

- Long-term supplier contracts mitigate short-term inflation shocks

Currency Exchange Rate Risks

- EUR/USD ~1.08 (2024 avg) impacts pricing

- EUR/CNY ~7.80 (2024 avg) affects China sales/imports

- ~30% revenues non-EUR exposure

- FX hedging can change margins by 0.4–0.8ppt

Metal price spikes and energy costs squeeze margins despite EV-driven volume boom

Economic factors: metal price volatility (NdO +28% 2024; W ±15% y/y) and energy costs (€85–€130/MWh 2024) squeeze margins; EV/electronics demand (global EV sales +35% 2024; semicap spend $109bn) supports volumes; EU PPI +8% y/y increases input costs; FX: EUR/USD ~1.08 avg, EUR/CNY ~7.80, ~30% revenue non-EUR—hedging alters margins by 0.4–0.8ppt.

| Metric | 2024 |

|---|---|

| NdO price | +28% |

| W volatility | ±15% |

| Energy €/MWh | 85–130 |

| EV sales | +35% |

| Semicap spend | $109bn |

| EU PPI | +8% |

| EUR/USD | ~1.08 |

Preview the Actual Deliverable

Treibacher Industrie AG PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Treibacher Industrie AG you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.