Trigano Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

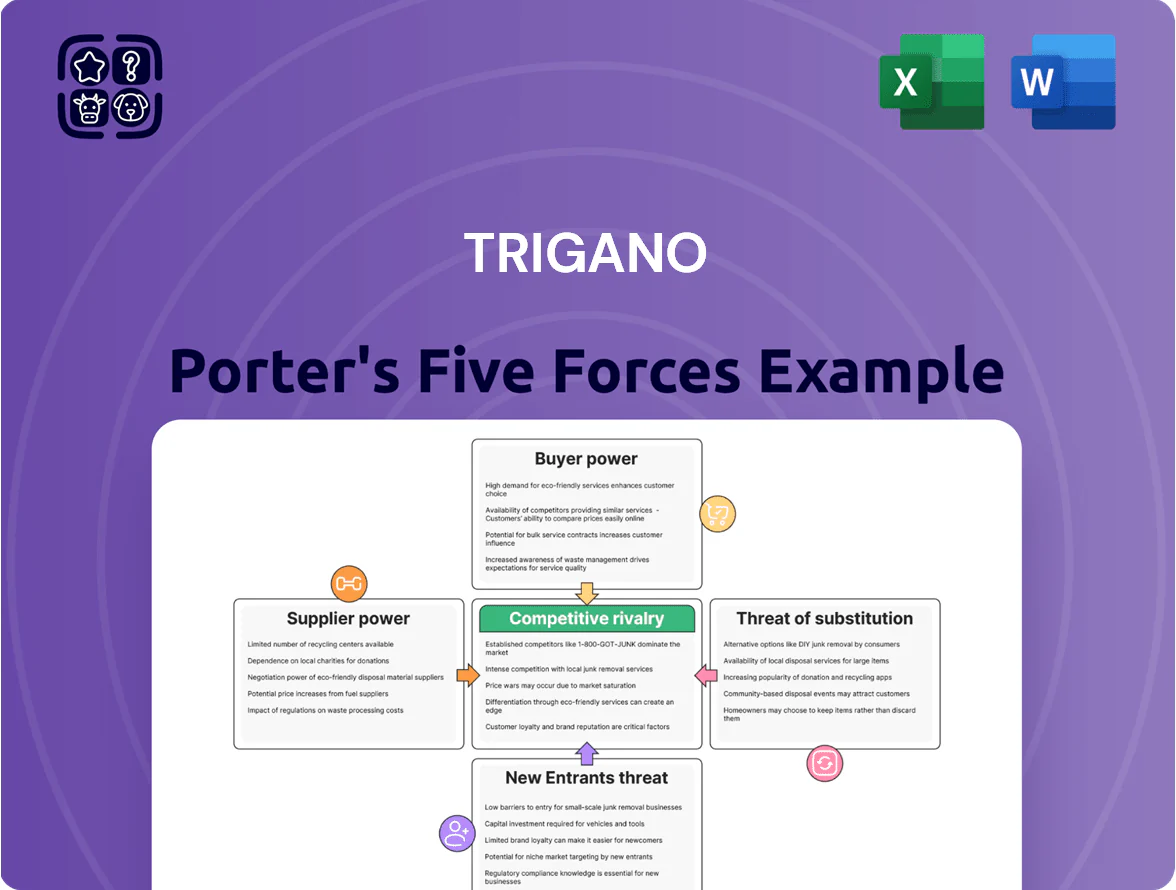

Trigano faces moderate supplier leverage and rising competitive rivalry driven by European leisure trends and consolidation, while buyer power and substitutes pressure margins as electric mobility and rental models evolve; regulatory shifts and distribution complexities further shape entry barriers and industry dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trigano’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of chassis manufacturers

The production of motorhomes depends on few chassis suppliers—Stellantis and Ford supplied roughly 60–70% of European light commercial vehicle (LCV) chassis in 2024—giving them strong leverage on price and lead times when logistics strain capacity. Supply shocks in 2020–22 raised chassis lead times from ~4 to 20+ weeks; similar disruptions would force Trigano to absorb higher input costs or delay production. Trigano therefore needs tight strategic partnerships and multi-year purchase agreements to secure base vehicles for its assembly lines.

Criticality of specialized internal components

Suppliers of key leisure-vehicle parts—heating, fridges, electronics—hold high bargaining power because firms like Dometic (2024 revenue €1.9bn) and Truma dominate niches with proprietary tech; replacing them needs interior redesigns and costs 5–15% of vehicle BOM (bill of materials) on average, so few high-quality alternatives meet reliability expectations, raising supplier leverage on price, lead times, and specs.

Volatility of raw material costs

Technical integration and switching costs

Technical integration of supplier components creates moderate switching costs for Trigano; replacing a primary supplier often needs months of engineering changes, fresh safety certifications, and retraining on assembly techniques, raising one-off costs by an estimated €1–3m per supplier based on typical RV industry data in 2024.

This technical lock-in boosts bargaining power of entrenched suppliers who supply >60% of critical modules, making short-term price pressure limited and contract renegotiation harder.

- Months of reengineering, €1–3m one-off cost

- New safety certs and retraining required

- Suppliers supply >60% of critical modules

Impact of automotive industry transitions

- EV/H2 R&D focus: >60% supplier spend (2024)

- Potential premium: 10–25% per chassis

- Action: co-fund R&D, long-term contracts

Supplier dominance: 60–70% chassis control, input shocks cut EBIT ~3–4ppt; €1–3m switch

Suppliers hold high power: Stellantis/Ford provided ~60–70% LCV chassis in 2024; Dometic/Truma dominate key modules (Dometic revenue €1.9bn 2024). Commodity swings (aluminum +18% y/y 2024) and 10% input shocks can cut EBIT ~3–4ppt. Switching costs ~€1–3m and months for reengineering; EV/H2 R&D shifts can add 10–25% chassis premium.

| Metric | 2024 |

|---|---|

| Chassis share | 60–70% |

| Dometic revenue | €1.9bn |

| Aluminum change | +18% y/y |

| Switch cost | €1–3m |

| Chassis premium | 10–25% |

What is included in the product

Tailored Porter's Five Forces for Trigano, uncovering competitive drivers, buyer/supplier power, threat of entrants and substitutes, and strategic barriers protecting its market position.

Compact Porter's Five Forces for Trigano—instantly highlights supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Consolidation of dealership networks

High price sensitivity of end consumers

Motorhomes and caravans are major discretionary buys, so buyers react strongly to economic shifts; in 2023 European RV sales fell ~5% as rising ECB rates pushed financing costs up, triggering tougher negotiation and delayed purchases.

When consumer confidence drops—Eurozone consumer confidence slid to -18 in Dec 2023—Trigano sees more price pressure, so it keeps entry-level ranges; entry-level models made ~28% of Trigano’s 2024 unit mix to capture budget buyers.

Low switching costs between brands

While Trigano retains brand loyalty, switching costs to rivals like Knaus Tabbert or Hymer are low, since layouts and features overlap widely; a 2024 European RV buyer survey showed 62% consider price and availability the top two purchase drivers. Most leisure vehicles share core specs, so customers shift for a €3,000–€10,000 price gap or faster delivery; this raises buyer leverage. Local dealer service also sways choices, increasing demands for better value.

Information transparency and digital research

Modern consumers use online reviews, price-comparison tools, and forums that expose Trigano product quality and pricing; 72% of RV buyers consult online reviews pre-purchase (Statista 2024), cutting information asymmetry.

This transparency forces buyers to demand clearer value; Trigano reported €2.1bn revenue in 2024, so maintaining visible quality and pricing preserves margin and market share.

- 72% of buyers use online reviews (Statista 2024)

- €2.1bn Trigano 2024 revenue

- Transparency lowers price spread, raises service expectations

Influence of the secondary market

The robust European used leisure-vehicle market—estimated at ~220,000 traded units in 2024 and with average prices ~35% below new retail—caps Trigano’s pricing power by offering a cheaper, late-model alternative.

If Trigano raises new prices beyond a 10–20% premium over comparable late-model pre-owned units, buyers often switch, pressuring margins and sales volumes; Trigano must price new launches near used/finance-adjusted comparisons.

- Used market size: ~220,000 units Europe 2024

- Avg used vs new price gap: ~35% 2024

- Price premium trigger: ~10–20% switch risk

Trigano faces dealer-driven margin pressure: rebates, used market and review-led pricing

| Metric | Value (2024) |

|---|---|

| Dealer channel share | ~60% of €4.2bn |

| Dealer support cost | 4–6% margin |

| Used market size | ~220,000 units |

| Used vs new price gap | ~−35% |

| Buyers using reviews | 72% (Statista) |

Same Document Delivered

Trigano Porter's Five Forces Analysis

This preview shows the exact Trigano Porter’s Five Forces analysis you’ll receive immediately after purchase—no samples or placeholders; the full, professionally formatted document is ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Trigano faces moderate supplier leverage and rising competitive rivalry driven by European leisure trends and consolidation, while buyer power and substitutes pressure margins as electric mobility and rental models evolve; regulatory shifts and distribution complexities further shape entry barriers and industry dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trigano’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of chassis manufacturers

The production of motorhomes depends on few chassis suppliers—Stellantis and Ford supplied roughly 60–70% of European light commercial vehicle (LCV) chassis in 2024—giving them strong leverage on price and lead times when logistics strain capacity. Supply shocks in 2020–22 raised chassis lead times from ~4 to 20+ weeks; similar disruptions would force Trigano to absorb higher input costs or delay production. Trigano therefore needs tight strategic partnerships and multi-year purchase agreements to secure base vehicles for its assembly lines.

Criticality of specialized internal components

Suppliers of key leisure-vehicle parts—heating, fridges, electronics—hold high bargaining power because firms like Dometic (2024 revenue €1.9bn) and Truma dominate niches with proprietary tech; replacing them needs interior redesigns and costs 5–15% of vehicle BOM (bill of materials) on average, so few high-quality alternatives meet reliability expectations, raising supplier leverage on price, lead times, and specs.

Volatility of raw material costs

Technical integration and switching costs

Technical integration of supplier components creates moderate switching costs for Trigano; replacing a primary supplier often needs months of engineering changes, fresh safety certifications, and retraining on assembly techniques, raising one-off costs by an estimated €1–3m per supplier based on typical RV industry data in 2024.

This technical lock-in boosts bargaining power of entrenched suppliers who supply >60% of critical modules, making short-term price pressure limited and contract renegotiation harder.

- Months of reengineering, €1–3m one-off cost

- New safety certs and retraining required

- Suppliers supply >60% of critical modules

Impact of automotive industry transitions

- EV/H2 R&D focus: >60% supplier spend (2024)

- Potential premium: 10–25% per chassis

- Action: co-fund R&D, long-term contracts

Supplier dominance: 60–70% chassis control, input shocks cut EBIT ~3–4ppt; €1–3m switch

Suppliers hold high power: Stellantis/Ford provided ~60–70% LCV chassis in 2024; Dometic/Truma dominate key modules (Dometic revenue €1.9bn 2024). Commodity swings (aluminum +18% y/y 2024) and 10% input shocks can cut EBIT ~3–4ppt. Switching costs ~€1–3m and months for reengineering; EV/H2 R&D shifts can add 10–25% chassis premium.

| Metric | 2024 |

|---|---|

| Chassis share | 60–70% |

| Dometic revenue | €1.9bn |

| Aluminum change | +18% y/y |

| Switch cost | €1–3m |

| Chassis premium | 10–25% |

What is included in the product

Tailored Porter's Five Forces for Trigano, uncovering competitive drivers, buyer/supplier power, threat of entrants and substitutes, and strategic barriers protecting its market position.

Compact Porter's Five Forces for Trigano—instantly highlights supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Consolidation of dealership networks

High price sensitivity of end consumers

Motorhomes and caravans are major discretionary buys, so buyers react strongly to economic shifts; in 2023 European RV sales fell ~5% as rising ECB rates pushed financing costs up, triggering tougher negotiation and delayed purchases.

When consumer confidence drops—Eurozone consumer confidence slid to -18 in Dec 2023—Trigano sees more price pressure, so it keeps entry-level ranges; entry-level models made ~28% of Trigano’s 2024 unit mix to capture budget buyers.

Low switching costs between brands

While Trigano retains brand loyalty, switching costs to rivals like Knaus Tabbert or Hymer are low, since layouts and features overlap widely; a 2024 European RV buyer survey showed 62% consider price and availability the top two purchase drivers. Most leisure vehicles share core specs, so customers shift for a €3,000–€10,000 price gap or faster delivery; this raises buyer leverage. Local dealer service also sways choices, increasing demands for better value.

Information transparency and digital research

Modern consumers use online reviews, price-comparison tools, and forums that expose Trigano product quality and pricing; 72% of RV buyers consult online reviews pre-purchase (Statista 2024), cutting information asymmetry.

This transparency forces buyers to demand clearer value; Trigano reported €2.1bn revenue in 2024, so maintaining visible quality and pricing preserves margin and market share.

- 72% of buyers use online reviews (Statista 2024)

- €2.1bn Trigano 2024 revenue

- Transparency lowers price spread, raises service expectations

Influence of the secondary market

The robust European used leisure-vehicle market—estimated at ~220,000 traded units in 2024 and with average prices ~35% below new retail—caps Trigano’s pricing power by offering a cheaper, late-model alternative.

If Trigano raises new prices beyond a 10–20% premium over comparable late-model pre-owned units, buyers often switch, pressuring margins and sales volumes; Trigano must price new launches near used/finance-adjusted comparisons.

- Used market size: ~220,000 units Europe 2024

- Avg used vs new price gap: ~35% 2024

- Price premium trigger: ~10–20% switch risk

Trigano faces dealer-driven margin pressure: rebates, used market and review-led pricing

| Metric | Value (2024) |

|---|---|

| Dealer channel share | ~60% of €4.2bn |

| Dealer support cost | 4–6% margin |

| Used market size | ~220,000 units |

| Used vs new price gap | ~−35% |

| Buyers using reviews | 72% (Statista) |

Same Document Delivered

Trigano Porter's Five Forces Analysis

This preview shows the exact Trigano Porter’s Five Forces analysis you’ll receive immediately after purchase—no samples or placeholders; the full, professionally formatted document is ready for instant download and use.