Trigano PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech trends are reshaping Trigano’s market position with our concise PESTLE snapshot—designed to spark strategic action and investment insight; buy the full analysis for a detailed, editable report you can use immediately.

Political factors

European Trade Policy Stability

Trigano’s pan-European operations rely on the Single Market; intra-EU trade accounted for over 80% of EU goods flows in 2024, so any friction raises logistics costs and lead times across its network.

Seamless cross-border movement affects production cadence for caravans and components; EU transport bottlenecks raised average delivery times by 7% in 2024, impacting working capital needs.

As of late 2025, proposed EU customs rule tweaks and localized regulatory divergence could increase import costs versus non-EU rivals, eroding Trigano’s margin advantage in key markets.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions in Eastern Europe and the Black Sea region risk disrupting supply of steel and electronics, with 2024 EU imports of steel from Ukraine/Russia down ~35% YoY, potentially affecting Trigano’s motorhome chassis sourcing.

Trigano must secure long-term contracts for chassis and ECU modules; in 2025 OEM component lead times averaged 22–30 weeks, raising working capital needs.

Political instability in transit corridors has pushed firms to localize: shifting 20–30% of procurement to EU suppliers can reduce delay risk but may raise input costs by ~8–12%.

National Tourism Support Programs

Many European governments rolled out subsidies and infrastructure investments for domestic tourism, with EU member states allocating over €12.5bn to rural tourism and campsite upgrades in 2024–25, boosting motorhome-friendly sites and service stations across France, Germany and Spain.

These political initiatives expanded campsite capacity by an estimated 8–10% year-on-year in 2024, directly lowering barriers to entry for new leisure vehicle users and shortening payback periods for first-time buyers.

Trigano, which reported 2024 leisure vehicle revenues of €3.1bn, benefits as increased site availability raises sales volumes and aftermarket service demand, supporting margin resilience amid cyclical volatility.

Post-Brexit Regulatory Alignment

The UK remains a key market for Trigano, accounting for roughly 6-8% of European caravan and motorhome sales in 2024, so regulatory divergence post-Brexit needs constant monitoring to avoid market access disruption.

Shifts in safety standards, technical specs or import duties—UK tariff adjustments or differing UNECE rules—can raise export admin costs; similar firms reported a 4-7% rise in compliance expenses after 2021.

Management should stay engaged with trade bodies (e.g., CCIA, ECF) and government channels to hedge against political shifts between London and Brussels and preserve supply-chain fluidity.

- UK ≈ 6-8% of regional sales (2024)

- Compliance costs rose ~4-7% post-Brexit for comparable firms

- Active engagement with CCIA/ECF advised

Public Infrastructure Investment

Government plans to invest in transport — the EU pledged 300+ billion euros for TEN-T and EV charging through 2024–27 — directly affect Trigano by improving road quality and expanding charging networks critical for motorhome touring as fleets electrify.

Political commitment to modernize infrastructure, including national stimulus packages (e.g., France invested ~€14bn in 2024 transport upgrades), supports long-term demand for leisure vehicles transitioning to new energy sources.

Trigano depends on public investment to keep long-distance travel practical; greater EV charging density and road upgrades reduce range anxiety and preserve resale values for electric and hybrid motorhomes.

- EU TEN-T/EV funds ~€300bn (2024–27)

- France transport spend ~€14bn (2024)

- Higher charging density reduces range anxiety, supports resale value

Trigano weathers EU trade shocks as TEN‑T funds and campsite boom drive €3.1bn leisure sales

EU trade friction, customs tweaks and regional instability (steel imports -35% YoY 2024) raise input costs and lead times; TEN-T/EV funds (~€300bn 2024–27) and €12.5bn tourism subsidies boost campsite capacity (+8–10% 2024) supporting Trigano’s €3.1bn leisure revenue (2024); UK ≈6–8% sales—post-Brexit compliance +4–7%.

| Metric | Value |

|---|---|

| Leisure revenue (2024) | €3.1bn |

| Campsite capacity Δ (2024) | +8–10% |

| EU TEN-T/EV funds | ~€300bn (2024–27) |

| Steel imports change (2024) | -35% YoY |

| UK sales share (2024) | 6–8% |

What is included in the product

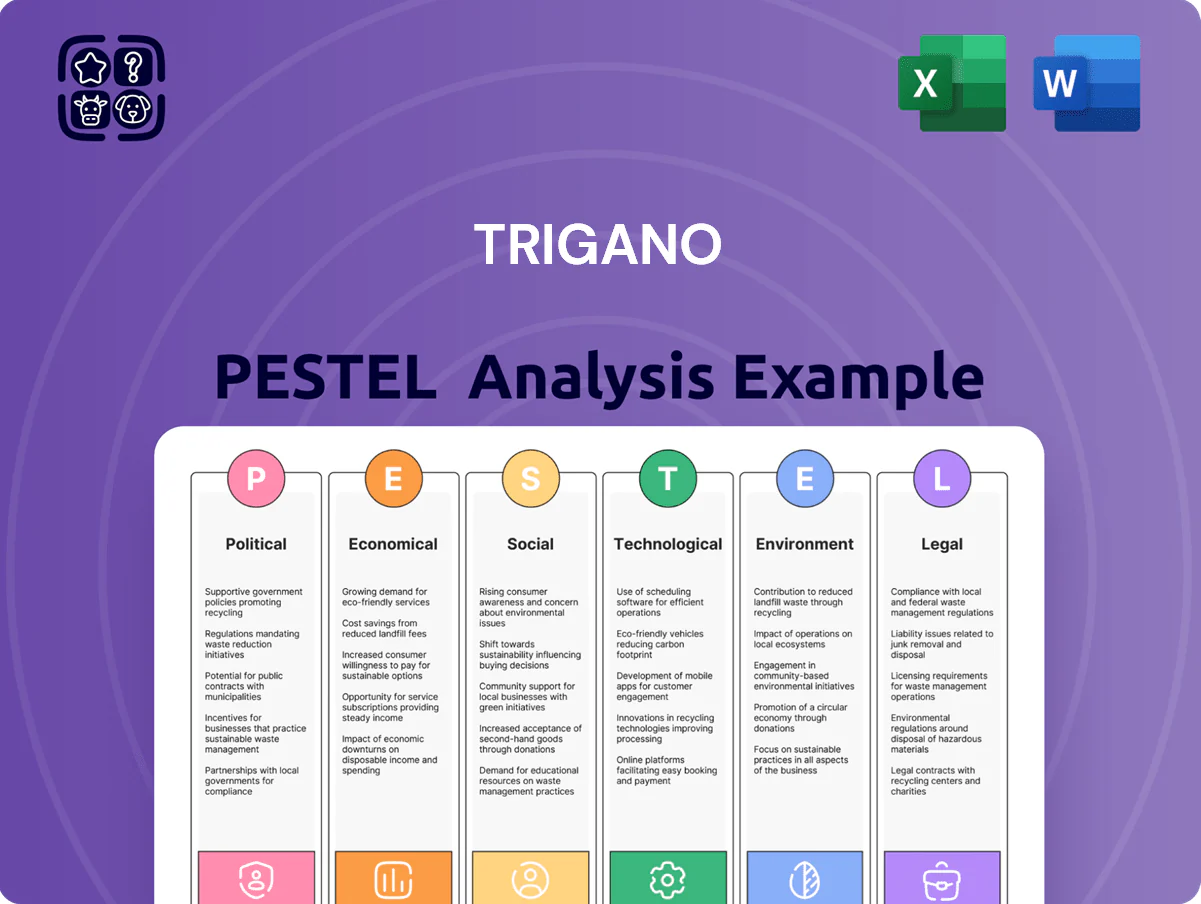

Explores how macro-environmental forces uniquely affect Trigano across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

Provides a clean, summarized Trigano PESTLE that’s visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Interest Rate Environment

The cost of borrowing is key for Trigano since about 60% of European motorhome purchases were financed in 2024; elevated ECB rates (deposit rate 4.00% by Dec 2025 expectations) and average motorhome loan rates rising to ~6–8% in 2025 have pushed up monthly payments and cooled demand. Trigano must track ECB policy and 2025 dealer financing spreads to forecast consumer affordability and inventory funding costs.

Raw Material Price Volatility

The manufacturing of leisure vehicles is highly sensitive to aluminum, steel and petroleum-based plastics prices; aluminum rose ~18% and steel ~12% globally in 2024, increasing input costs for Trigano and peers. Economic swings in commodity markets can compress margins if costs cannot be passed to consumers—Trigano reported 2024 adjusted operating margin of ~8.6%, reflecting input pressure. Trigano mitigates risk via strategic hedging and long-term supplier contracts, covering a significant portion of 2024 procurement and smoothing cost volatility.

Consumer Purchasing Power

As a maker of discretionary luxury goods, Trigano is sensitive to European disposable income trends; Eurostat reported real household disposable income in the EU fell 0.4% in 2023 while inflation averaged 6.6% in 2023 and 3.4% in 2024, prompting consumers to delay big purchases like caravans. Inflation on essentials squeezes budgets, and Trigano has shifted toward entry-level motorhome ranges—lower-priced models grew share in 2024—to preserve volumes.

Currency Exchange Fluctuations

Trigano faces currency risk as 2024 saw EUR/GBP move roughly 5% and EUR/USD about 6% year-on-year, which can erode margins in the UK and US if retail prices and component costs are set in non-euro currencies.

Significant swings hurt price competitiveness and raise imported parts costs; finance must use hedging (forwards, options)—Trigano reported FX losses impact on consolidated EBITDA in prior years, underscoring need for active FX management.

- EUR/GBP ~5% Y/Y (2024)

- EUR/USD ~6% Y/Y (2024)

- Hedging via forwards/options recommended

- FX volatility can compress margins and raise import costs

Labor Market Dynamics

The availability of skilled labor in France, Italy and Spain shapes Trigano’s manufacturing capacity and wage bill; France and Italy account for over 60% of EU RV production and recent tightness pushed manufacturing vacancy rates to 2.3% in 2024, raising hourly labor costs by ~4–6% year-on-year and increasing production unit costs.

Economic growth in these hubs tightened labor markets in 2023–2024, pressuring salaries and total cost of production; Trigano recorded a 5% rise in personnel expenses in 2024 versus 2023, prompting investments in automation and process efficiency to contain margins.

To offset rising labor costs Trigano expanded vocational training and retention programs and increased CAPEX in production optimization (CAPEX up ~8% in 2024), improving labor productivity and lowering turnover in key plants.

- Manufacturing vacancy rate: 2.3% (2024)

- Personnel expenses +5% YoY (2024)

- CAPEX on production +8% (2024)

- Hourly labor costs +4–6% YoY (2024)

Rising rates, commodity inflation and tight labor squeeze margins—hedging essential

Higher borrowing costs (motorhome loan rates ~6–8% in 2025) and ECB policy (deposit rate ~4.00% by Dec 2025 expectations) have cooled demand; commodity inflation (aluminum +18%, steel +12% in 2024) raised input costs, compressing margins (adj. op. margin ~8.6% in 2024). FX volatility (EUR/GBP ~5% Y/Y, EUR/USD ~6% Y/Y in 2024) and tight labor (vacancy 2.3%, personnel expenses +5% YoY, CAPEX +8% in 2024) increase costs; hedging and financing strategies are critical.

| Metric | 2024/2025 |

|---|---|

| Adj. op. margin | ~8.6% (2024) |

| Aluminum/Steel | +18% / +12% (2024) |

| Loan rates | ~6–8% (2025 est.) |

| ECB deposit rate | ~4.00% (Dec 2025 est.) |

| EUR/GBP, EUR/USD | ~5%, ~6% Y/Y (2024) |

| Vacancy / personnel costs | 2.3% / +5% YoY (2024) |

Preview Before You Purchase

Trigano PESTLE Analysis

The preview shown here is the exact Trigano PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech trends are reshaping Trigano’s market position with our concise PESTLE snapshot—designed to spark strategic action and investment insight; buy the full analysis for a detailed, editable report you can use immediately.

Political factors

European Trade Policy Stability

Trigano’s pan-European operations rely on the Single Market; intra-EU trade accounted for over 80% of EU goods flows in 2024, so any friction raises logistics costs and lead times across its network.

Seamless cross-border movement affects production cadence for caravans and components; EU transport bottlenecks raised average delivery times by 7% in 2024, impacting working capital needs.

As of late 2025, proposed EU customs rule tweaks and localized regulatory divergence could increase import costs versus non-EU rivals, eroding Trigano’s margin advantage in key markets.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions in Eastern Europe and the Black Sea region risk disrupting supply of steel and electronics, with 2024 EU imports of steel from Ukraine/Russia down ~35% YoY, potentially affecting Trigano’s motorhome chassis sourcing.

Trigano must secure long-term contracts for chassis and ECU modules; in 2025 OEM component lead times averaged 22–30 weeks, raising working capital needs.

Political instability in transit corridors has pushed firms to localize: shifting 20–30% of procurement to EU suppliers can reduce delay risk but may raise input costs by ~8–12%.

National Tourism Support Programs

Many European governments rolled out subsidies and infrastructure investments for domestic tourism, with EU member states allocating over €12.5bn to rural tourism and campsite upgrades in 2024–25, boosting motorhome-friendly sites and service stations across France, Germany and Spain.

These political initiatives expanded campsite capacity by an estimated 8–10% year-on-year in 2024, directly lowering barriers to entry for new leisure vehicle users and shortening payback periods for first-time buyers.

Trigano, which reported 2024 leisure vehicle revenues of €3.1bn, benefits as increased site availability raises sales volumes and aftermarket service demand, supporting margin resilience amid cyclical volatility.

Post-Brexit Regulatory Alignment

The UK remains a key market for Trigano, accounting for roughly 6-8% of European caravan and motorhome sales in 2024, so regulatory divergence post-Brexit needs constant monitoring to avoid market access disruption.

Shifts in safety standards, technical specs or import duties—UK tariff adjustments or differing UNECE rules—can raise export admin costs; similar firms reported a 4-7% rise in compliance expenses after 2021.

Management should stay engaged with trade bodies (e.g., CCIA, ECF) and government channels to hedge against political shifts between London and Brussels and preserve supply-chain fluidity.

- UK ≈ 6-8% of regional sales (2024)

- Compliance costs rose ~4-7% post-Brexit for comparable firms

- Active engagement with CCIA/ECF advised

Public Infrastructure Investment

Government plans to invest in transport — the EU pledged 300+ billion euros for TEN-T and EV charging through 2024–27 — directly affect Trigano by improving road quality and expanding charging networks critical for motorhome touring as fleets electrify.

Political commitment to modernize infrastructure, including national stimulus packages (e.g., France invested ~€14bn in 2024 transport upgrades), supports long-term demand for leisure vehicles transitioning to new energy sources.

Trigano depends on public investment to keep long-distance travel practical; greater EV charging density and road upgrades reduce range anxiety and preserve resale values for electric and hybrid motorhomes.

- EU TEN-T/EV funds ~€300bn (2024–27)

- France transport spend ~€14bn (2024)

- Higher charging density reduces range anxiety, supports resale value

Trigano weathers EU trade shocks as TEN‑T funds and campsite boom drive €3.1bn leisure sales

EU trade friction, customs tweaks and regional instability (steel imports -35% YoY 2024) raise input costs and lead times; TEN-T/EV funds (~€300bn 2024–27) and €12.5bn tourism subsidies boost campsite capacity (+8–10% 2024) supporting Trigano’s €3.1bn leisure revenue (2024); UK ≈6–8% sales—post-Brexit compliance +4–7%.

| Metric | Value |

|---|---|

| Leisure revenue (2024) | €3.1bn |

| Campsite capacity Δ (2024) | +8–10% |

| EU TEN-T/EV funds | ~€300bn (2024–27) |

| Steel imports change (2024) | -35% YoY |

| UK sales share (2024) | 6–8% |

What is included in the product

Explores how macro-environmental forces uniquely affect Trigano across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

Provides a clean, summarized Trigano PESTLE that’s visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Interest Rate Environment

The cost of borrowing is key for Trigano since about 60% of European motorhome purchases were financed in 2024; elevated ECB rates (deposit rate 4.00% by Dec 2025 expectations) and average motorhome loan rates rising to ~6–8% in 2025 have pushed up monthly payments and cooled demand. Trigano must track ECB policy and 2025 dealer financing spreads to forecast consumer affordability and inventory funding costs.

Raw Material Price Volatility

The manufacturing of leisure vehicles is highly sensitive to aluminum, steel and petroleum-based plastics prices; aluminum rose ~18% and steel ~12% globally in 2024, increasing input costs for Trigano and peers. Economic swings in commodity markets can compress margins if costs cannot be passed to consumers—Trigano reported 2024 adjusted operating margin of ~8.6%, reflecting input pressure. Trigano mitigates risk via strategic hedging and long-term supplier contracts, covering a significant portion of 2024 procurement and smoothing cost volatility.

Consumer Purchasing Power

As a maker of discretionary luxury goods, Trigano is sensitive to European disposable income trends; Eurostat reported real household disposable income in the EU fell 0.4% in 2023 while inflation averaged 6.6% in 2023 and 3.4% in 2024, prompting consumers to delay big purchases like caravans. Inflation on essentials squeezes budgets, and Trigano has shifted toward entry-level motorhome ranges—lower-priced models grew share in 2024—to preserve volumes.

Currency Exchange Fluctuations

Trigano faces currency risk as 2024 saw EUR/GBP move roughly 5% and EUR/USD about 6% year-on-year, which can erode margins in the UK and US if retail prices and component costs are set in non-euro currencies.

Significant swings hurt price competitiveness and raise imported parts costs; finance must use hedging (forwards, options)—Trigano reported FX losses impact on consolidated EBITDA in prior years, underscoring need for active FX management.

- EUR/GBP ~5% Y/Y (2024)

- EUR/USD ~6% Y/Y (2024)

- Hedging via forwards/options recommended

- FX volatility can compress margins and raise import costs

Labor Market Dynamics

The availability of skilled labor in France, Italy and Spain shapes Trigano’s manufacturing capacity and wage bill; France and Italy account for over 60% of EU RV production and recent tightness pushed manufacturing vacancy rates to 2.3% in 2024, raising hourly labor costs by ~4–6% year-on-year and increasing production unit costs.

Economic growth in these hubs tightened labor markets in 2023–2024, pressuring salaries and total cost of production; Trigano recorded a 5% rise in personnel expenses in 2024 versus 2023, prompting investments in automation and process efficiency to contain margins.

To offset rising labor costs Trigano expanded vocational training and retention programs and increased CAPEX in production optimization (CAPEX up ~8% in 2024), improving labor productivity and lowering turnover in key plants.

- Manufacturing vacancy rate: 2.3% (2024)

- Personnel expenses +5% YoY (2024)

- CAPEX on production +8% (2024)

- Hourly labor costs +4–6% YoY (2024)

Rising rates, commodity inflation and tight labor squeeze margins—hedging essential

Higher borrowing costs (motorhome loan rates ~6–8% in 2025) and ECB policy (deposit rate ~4.00% by Dec 2025 expectations) have cooled demand; commodity inflation (aluminum +18%, steel +12% in 2024) raised input costs, compressing margins (adj. op. margin ~8.6% in 2024). FX volatility (EUR/GBP ~5% Y/Y, EUR/USD ~6% Y/Y in 2024) and tight labor (vacancy 2.3%, personnel expenses +5% YoY, CAPEX +8% in 2024) increase costs; hedging and financing strategies are critical.

| Metric | 2024/2025 |

|---|---|

| Adj. op. margin | ~8.6% (2024) |

| Aluminum/Steel | +18% / +12% (2024) |

| Loan rates | ~6–8% (2025 est.) |

| ECB deposit rate | ~4.00% (Dec 2025 est.) |

| EUR/GBP, EUR/USD | ~5%, ~6% Y/Y (2024) |

| Vacancy / personnel costs | 2.3% / +5% YoY (2024) |

Preview Before You Purchase

Trigano PESTLE Analysis

The preview shown here is the exact Trigano PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.