Trina Solar Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

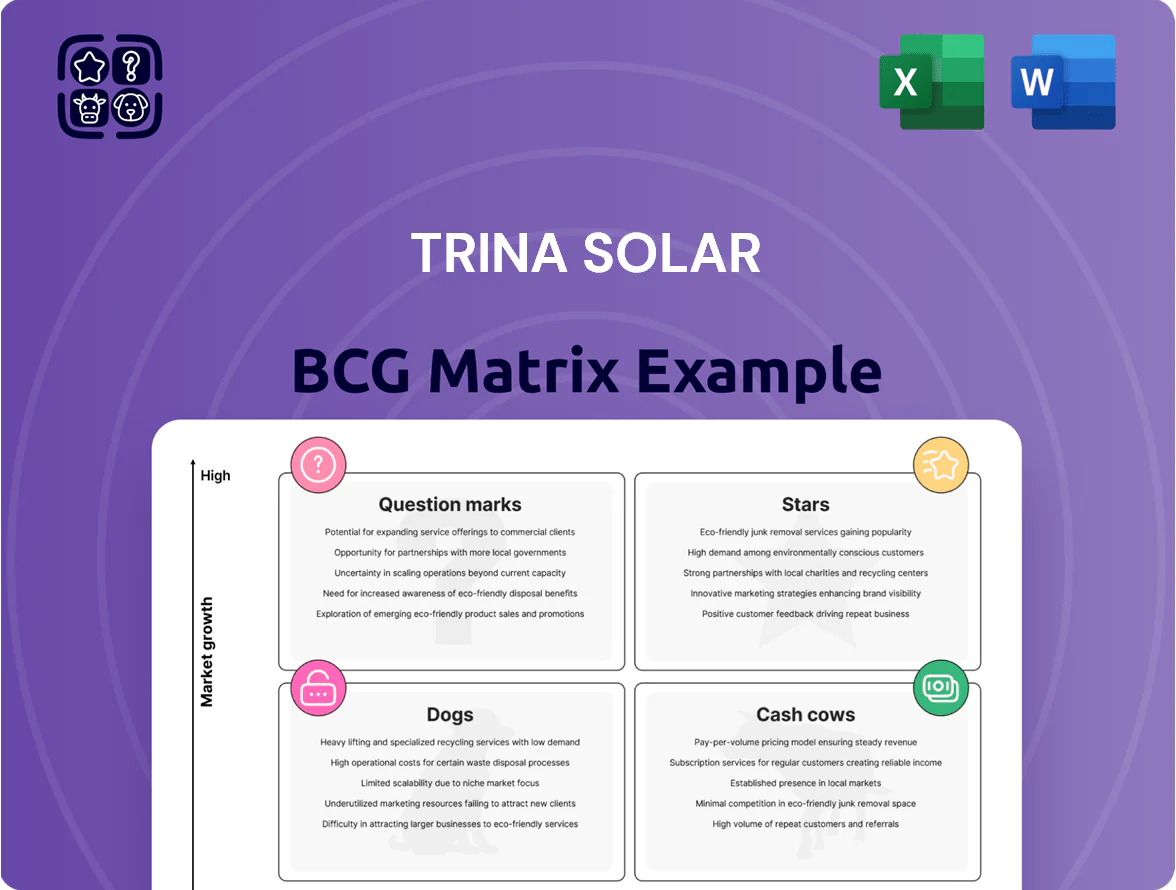

Trina Solar's preliminary BCG Matrix snapshot highlights its high-growth solar module segments occupying Star positions while legacy, commoditized lines trend toward Cash Cow or Dog status—revealing where scale, R&D, or divestment should focus. This preview teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-backed breakdown, actionable recommendations, and downloadable Word and Excel deliverables to guide capital allocation and product strategy.

Stars

N-type TOPCon Vertex Modules

The N-type TOPCon Vertex modules have become Trina Solar’s primary revenue driver by late 2025, accounting for about 42% of product sales and helping deliver a 2025 revenue share gain of 7 percentage points year-over-year.

They hold a leading market share in utility-scale projects—roughly 28% of new global procurement in 2025—driven by 24.4%+ panel efficiency and LID (light-induced degradation) under 0.5% first-year, outperforming P-type alternatives.

Scaling Vertex required roughly $1.2 billion in capex from 2023–2025 to expand N-type TOPCon capacity, but it sustained industry leadership in the high-growth utility segment and improved gross margins by ~220 basis points versus P-type lines.

Trina Storage Utility Solutions

Trina Storage Utility Solutions sits in the BCG Matrix star quadrant: in 2025 Trina captured ~18% of global utility-scale battery shipments, with unit growth ~42% YoY as grids shift to renewables.

Integrated energy storage systems address solar intermittency and in 2024 averaged 200+ MWh project sizes, driving strong demand from developers and 35% gross margins on system sales.

Ongoing investment in LFP (lithium iron phosphate) cell capacity—planned 10 GWh by end-2026—keeps Trina a dominant, high-growth player.

210mm Ultra-High Power Technology

Trina Solar led adoption of 210mm wafers, now the industry standard for high-power modules; by 2025 Trina held ~22% global market share in large-format modules, securing scale advantages and a manufacturing cost edge of ~6-9% vs 166mm lines.

TrinaTracker Smart Tracking Systems

TrinaTracker pairs Trina Solar’s high-efficiency modules with smart bifacial trackers to boost energy yield; field data to Dec 2025 shows bifacial + tracking can raise annual energy by ~15–25% versus fixed-tilt, lifting project IRR by 1.5–3 percentage points.

TrinaTracker sits in a high-growth segment—global tracker shipments grew ~18% in 2024—where Trina holds double-digit share and invests ~USD 60m+ annually in software, digital O&M, and AI pitch/row optimization.

- Complete solution: modules + trackers

- Yield uplift: ~15–25% vs fixed

- IRR impact: +1.5–3 pp

- 2024 tracker market growth: ~18%

- Trina tracker R&D spend: ~USD 60m+/yr

Global Utility-Scale EPC Services

Trina Solar’s Global Utility-Scale EPC Services deliver end-to-end engineering, procurement, and construction for multi-hundred-MW projects across Asia, Latin America, Europe, and Africa, leveraging its 2024 module shipments of ~40 GW to scale deployment.

The segment rides the 2025 wave of national decarbonization and $1.2 trillion global clean-energy infrastructure commitments, boosting demand and pricing power.

Projects tie up significant working capital—typical contract retention cycles of 12–24 months—but cement Trina’s role as an integrated solutions leader in a high-growth market.

- 2024 module shipments ~40 GW

- Global clean-energy commitments ~$1.2 trillion by 2025

- Contract cycles 12–24 months

- Supports market-leading integrated positioning

Trina dominates utility solar: Vertex, storage, trackers drive rapid global growth

Trina’s Stars: N-type TOPCon Vertex modules, Trina Storage, TrinaTracker, and Global EPC lead high-growth utility markets—2025: Vertex = 42% product sales; utility procurement share ~28%; storage shipments ~18% global with 42% YoY unit growth; tracker market +18% in 2024; 2023–25 capex ~$1.2bn; 2024 module shipments ~40 GW; LFP capacity target 10 GWh by end-2026.

| Asset | 2025 metric |

|---|---|

| Vertex modules | 42% sales, 28% utility share |

| Storage | 18% ship., +42% YoY |

| Trackers | +18% mkt growth, +15–25% yield |

What is included in the product

BCG Matrix assessment of Trina Solar’s portfolio with quadrant strategies, investment priorities, risks, and trend context.

One-page Trina Solar BCG Matrix placing PV segments in quadrants for quick strategic clarity.

Cash Cows

Standard Mono PERC Module Portfolio

Standard Mono PERC modules are a mature tech with ~200+ GW cumulative global PERC capacity by end-2024 and Trina holding ~8–10% market share in mainstream PERC volumes, producing steady sales despite slowing market growth for PERC versus rising N-type cells.

With global PERC module ASPs around $0.16–0.20/W in 2024 and low R and D needs, these lines deliver predictable gross margins near 12–16%, generating cash flow Trina uses to fund N-type R&D and expansion.

Trina’s PERC production assets are largely depreciated—capex sunk—so operating cash flow from these modules funds newer n-type investments and capex, effectively milking legacy lines while transitioning technology.

Residential PV Distribution Networks

Trina Solar's mature residential PV distribution in Europe and Australia drives high market share with low incremental investment; 2024 shipments to installers exceeded 1.2 GW, supporting gross margins near 18% in the segment.

Long-term Operations and Maintenance Services

The Long-term Operations and Maintenance (O and M) segment delivers recurring, high-margin revenue from Trina Solar’s 2025 installed base—over 100 GW of modules worldwide—yielding steady service fees and spare-part sales with gross margins often above 30%.

O and M needs far less capital than manufacturing; typical annual capex per MW is under $5,000 versus $60,000+ for new module lines, and multiyear contracts (5–20 years) lock predictable cash flows.

As Trina’s global fleet grows (installed base rose ~12% in 2024), this cash cow smooths earnings and helps absorb module price swings and project-cycle volatility.

Global Brand Equity and Intellectual Property

Trina Solar’s Tier 1 status (BloombergNEF 2025 ranking) lets it charge ~5–8% price premium vs peers, keeping share and cutting promo spend; FY2024 gross margin 20.6% shows scale advantage.

The firm holds 1,200+ global patents in cell/module tech (company filings 2025), earning licensing fees and shielding volumes from fast followers.

Brand and IP act as cash cows: operating cash flow \$1.1B in 2024 funded R&D and downstream expansion, sustaining the corporate ecosystem.

- Tier 1 → 5–8% price premium

- 1,200+ patents (2025)

- Gross margin 20.6% (FY2024)

- Operating cash flow \$1.1B (2024)

Established P-type Cell Manufacturing

Trina Solar’s established P-type cell lines still serve price-sensitive and replacement markets where N-type’s premium isn’t needed, generating steady cashflow; in 2025 these legacy lines contributed an estimated $450–550M in annual gross profit thanks to low overhead and high utilization (~85%).

By keeping P-type capacity, Trina squeezes more ROI from existing fabs in a mature tech segment, lowering blended manufacturing cost per watt while funding N-type R&D and capacity expansion.

- Contributes ~$450–550M gross profit (2025 est.)

- Utilization ~85%, low overhead

- Targets price-sensitive, replacement demand

- Funds N-type R&D and expansion

Trina: $1.1B OCF, 20.6% margin; legacy P-type funds N-type growth amid 100+ GW base

Trina’s mature PERC and P-type lines plus O&M and IP produced operating cash flow $1.1B in 2024, with FY2024 gross margin 20.6%; legacy lines earned an estimated $450–550M gross profit in 2025 at ~85% utilization, funding N-type R&D and expansion while O&M margins exceed 30% on a 100+ GW installed base.

| Metric | Value |

|---|---|

| Op. cash flow (2024) | $1.1B |

| Gross margin (FY2024) | 20.6% |

| P-type gross profit (2025 est.) | $450–550M |

| Utilization (legacy) | ~85% |

| Installed base (2025) | 100+ GW |

| O&M gross margin | >30% |

Preview = Final Product

Trina Solar BCG Matrix

The file you're previewing is the final Trina Solar BCG Matrix you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.

This preview is identical to the downloadable BCG Matrix document you’ll get upon payment; crafted with market-backed insights and precise positioning, it arrives ready for immediate use with no surprises.

Once purchased, the full Trina Solar BCG Matrix is instantly available for editing, printing, or sharing with stakeholders—designed by strategy experts for seamless integration into your planning.

You're viewing the exact report that becomes yours after a one-time purchase: professionally formatted, actionable, and ready to support portfolio decisions, presentations, or client deliverables.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Trina Solar's preliminary BCG Matrix snapshot highlights its high-growth solar module segments occupying Star positions while legacy, commoditized lines trend toward Cash Cow or Dog status—revealing where scale, R&D, or divestment should focus. This preview teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-backed breakdown, actionable recommendations, and downloadable Word and Excel deliverables to guide capital allocation and product strategy.

Stars

N-type TOPCon Vertex Modules

The N-type TOPCon Vertex modules have become Trina Solar’s primary revenue driver by late 2025, accounting for about 42% of product sales and helping deliver a 2025 revenue share gain of 7 percentage points year-over-year.

They hold a leading market share in utility-scale projects—roughly 28% of new global procurement in 2025—driven by 24.4%+ panel efficiency and LID (light-induced degradation) under 0.5% first-year, outperforming P-type alternatives.

Scaling Vertex required roughly $1.2 billion in capex from 2023–2025 to expand N-type TOPCon capacity, but it sustained industry leadership in the high-growth utility segment and improved gross margins by ~220 basis points versus P-type lines.

Trina Storage Utility Solutions

Trina Storage Utility Solutions sits in the BCG Matrix star quadrant: in 2025 Trina captured ~18% of global utility-scale battery shipments, with unit growth ~42% YoY as grids shift to renewables.

Integrated energy storage systems address solar intermittency and in 2024 averaged 200+ MWh project sizes, driving strong demand from developers and 35% gross margins on system sales.

Ongoing investment in LFP (lithium iron phosphate) cell capacity—planned 10 GWh by end-2026—keeps Trina a dominant, high-growth player.

210mm Ultra-High Power Technology

Trina Solar led adoption of 210mm wafers, now the industry standard for high-power modules; by 2025 Trina held ~22% global market share in large-format modules, securing scale advantages and a manufacturing cost edge of ~6-9% vs 166mm lines.

TrinaTracker Smart Tracking Systems

TrinaTracker pairs Trina Solar’s high-efficiency modules with smart bifacial trackers to boost energy yield; field data to Dec 2025 shows bifacial + tracking can raise annual energy by ~15–25% versus fixed-tilt, lifting project IRR by 1.5–3 percentage points.

TrinaTracker sits in a high-growth segment—global tracker shipments grew ~18% in 2024—where Trina holds double-digit share and invests ~USD 60m+ annually in software, digital O&M, and AI pitch/row optimization.

- Complete solution: modules + trackers

- Yield uplift: ~15–25% vs fixed

- IRR impact: +1.5–3 pp

- 2024 tracker market growth: ~18%

- Trina tracker R&D spend: ~USD 60m+/yr

Global Utility-Scale EPC Services

Trina Solar’s Global Utility-Scale EPC Services deliver end-to-end engineering, procurement, and construction for multi-hundred-MW projects across Asia, Latin America, Europe, and Africa, leveraging its 2024 module shipments of ~40 GW to scale deployment.

The segment rides the 2025 wave of national decarbonization and $1.2 trillion global clean-energy infrastructure commitments, boosting demand and pricing power.

Projects tie up significant working capital—typical contract retention cycles of 12–24 months—but cement Trina’s role as an integrated solutions leader in a high-growth market.

- 2024 module shipments ~40 GW

- Global clean-energy commitments ~$1.2 trillion by 2025

- Contract cycles 12–24 months

- Supports market-leading integrated positioning

Trina dominates utility solar: Vertex, storage, trackers drive rapid global growth

Trina’s Stars: N-type TOPCon Vertex modules, Trina Storage, TrinaTracker, and Global EPC lead high-growth utility markets—2025: Vertex = 42% product sales; utility procurement share ~28%; storage shipments ~18% global with 42% YoY unit growth; tracker market +18% in 2024; 2023–25 capex ~$1.2bn; 2024 module shipments ~40 GW; LFP capacity target 10 GWh by end-2026.

| Asset | 2025 metric |

|---|---|

| Vertex modules | 42% sales, 28% utility share |

| Storage | 18% ship., +42% YoY |

| Trackers | +18% mkt growth, +15–25% yield |

What is included in the product

BCG Matrix assessment of Trina Solar’s portfolio with quadrant strategies, investment priorities, risks, and trend context.

One-page Trina Solar BCG Matrix placing PV segments in quadrants for quick strategic clarity.

Cash Cows

Standard Mono PERC Module Portfolio

Standard Mono PERC modules are a mature tech with ~200+ GW cumulative global PERC capacity by end-2024 and Trina holding ~8–10% market share in mainstream PERC volumes, producing steady sales despite slowing market growth for PERC versus rising N-type cells.

With global PERC module ASPs around $0.16–0.20/W in 2024 and low R and D needs, these lines deliver predictable gross margins near 12–16%, generating cash flow Trina uses to fund N-type R&D and expansion.

Trina’s PERC production assets are largely depreciated—capex sunk—so operating cash flow from these modules funds newer n-type investments and capex, effectively milking legacy lines while transitioning technology.

Residential PV Distribution Networks

Trina Solar's mature residential PV distribution in Europe and Australia drives high market share with low incremental investment; 2024 shipments to installers exceeded 1.2 GW, supporting gross margins near 18% in the segment.

Long-term Operations and Maintenance Services

The Long-term Operations and Maintenance (O and M) segment delivers recurring, high-margin revenue from Trina Solar’s 2025 installed base—over 100 GW of modules worldwide—yielding steady service fees and spare-part sales with gross margins often above 30%.

O and M needs far less capital than manufacturing; typical annual capex per MW is under $5,000 versus $60,000+ for new module lines, and multiyear contracts (5–20 years) lock predictable cash flows.

As Trina’s global fleet grows (installed base rose ~12% in 2024), this cash cow smooths earnings and helps absorb module price swings and project-cycle volatility.

Global Brand Equity and Intellectual Property

Trina Solar’s Tier 1 status (BloombergNEF 2025 ranking) lets it charge ~5–8% price premium vs peers, keeping share and cutting promo spend; FY2024 gross margin 20.6% shows scale advantage.

The firm holds 1,200+ global patents in cell/module tech (company filings 2025), earning licensing fees and shielding volumes from fast followers.

Brand and IP act as cash cows: operating cash flow \$1.1B in 2024 funded R&D and downstream expansion, sustaining the corporate ecosystem.

- Tier 1 → 5–8% price premium

- 1,200+ patents (2025)

- Gross margin 20.6% (FY2024)

- Operating cash flow \$1.1B (2024)

Established P-type Cell Manufacturing

Trina Solar’s established P-type cell lines still serve price-sensitive and replacement markets where N-type’s premium isn’t needed, generating steady cashflow; in 2025 these legacy lines contributed an estimated $450–550M in annual gross profit thanks to low overhead and high utilization (~85%).

By keeping P-type capacity, Trina squeezes more ROI from existing fabs in a mature tech segment, lowering blended manufacturing cost per watt while funding N-type R&D and capacity expansion.

- Contributes ~$450–550M gross profit (2025 est.)

- Utilization ~85%, low overhead

- Targets price-sensitive, replacement demand

- Funds N-type R&D and expansion

Trina: $1.1B OCF, 20.6% margin; legacy P-type funds N-type growth amid 100+ GW base

Trina’s mature PERC and P-type lines plus O&M and IP produced operating cash flow $1.1B in 2024, with FY2024 gross margin 20.6%; legacy lines earned an estimated $450–550M gross profit in 2025 at ~85% utilization, funding N-type R&D and expansion while O&M margins exceed 30% on a 100+ GW installed base.

| Metric | Value |

|---|---|

| Op. cash flow (2024) | $1.1B |

| Gross margin (FY2024) | 20.6% |

| P-type gross profit (2025 est.) | $450–550M |

| Utilization (legacy) | ~85% |

| Installed base (2025) | 100+ GW |

| O&M gross margin | >30% |

Preview = Final Product

Trina Solar BCG Matrix

The file you're previewing is the final Trina Solar BCG Matrix you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.

This preview is identical to the downloadable BCG Matrix document you’ll get upon payment; crafted with market-backed insights and precise positioning, it arrives ready for immediate use with no surprises.

Once purchased, the full Trina Solar BCG Matrix is instantly available for editing, printing, or sharing with stakeholders—designed by strategy experts for seamless integration into your planning.

You're viewing the exact report that becomes yours after a one-time purchase: professionally formatted, actionable, and ready to support portfolio decisions, presentations, or client deliverables.