Trisura Group Boston Consulting Group Matrix

Download Your Competitive Advantage

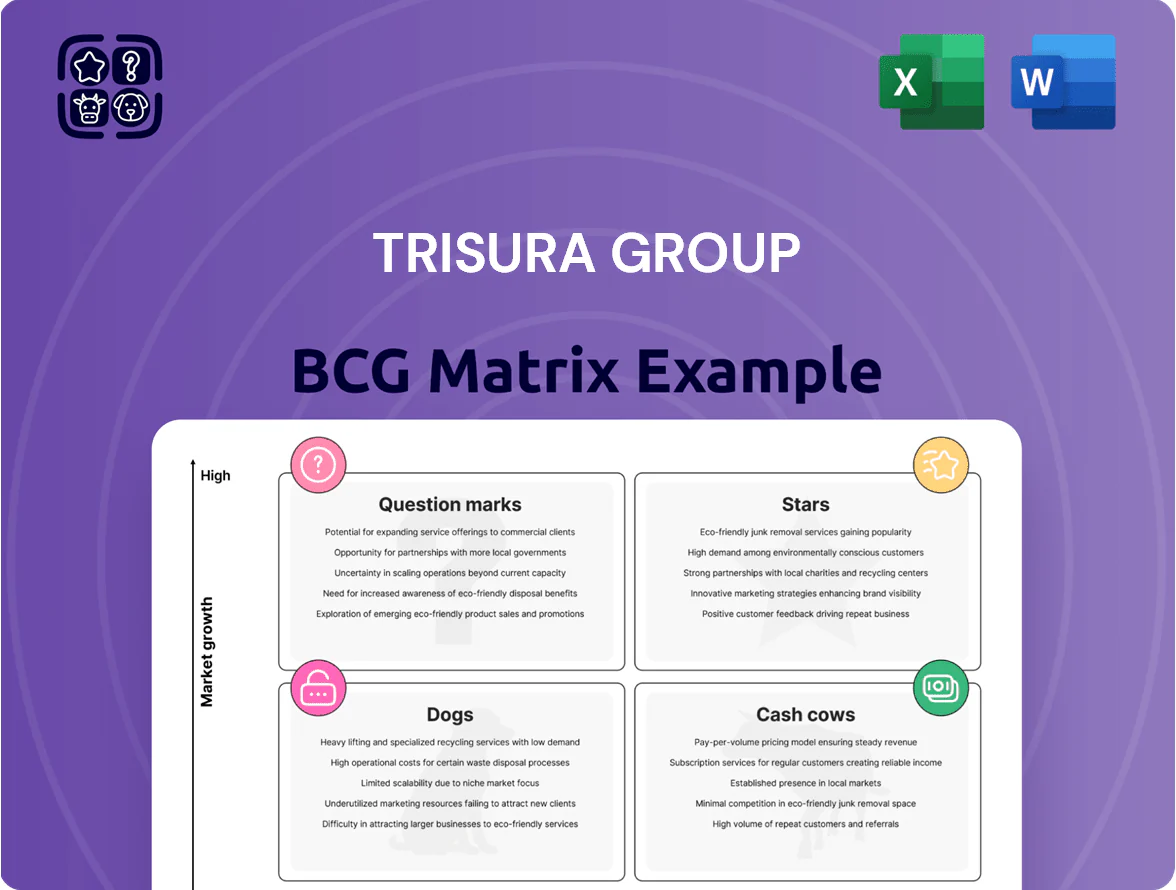

Trisura Group’s preliminary BCG Matrix snapshot highlights promising growth segments alongside slower, capital-intensive lines—helping you quickly spot potential Stars and Cash Cows versus Dogs and Question Marks. This concise preview teases actionable positioning and risk signals, but the full BCG Matrix delivers quadrant-level data, tailored strategic moves, and ready-to-use Word and Excel files to inform investment and portfolio decisions. Purchase the complete report for a comprehensive, data-driven roadmap to optimize capital allocation and competitive strategy.

Stars

U.S. Surety Operations

U.S. Surety Operations is a star: premiums rose 36% in 2025 and the unit entered the top 30 U.S. surety writers by Q3, driven by a newly capitalized balance sheet and multi-state licensing that target the $70+ billion U.S. specialty surety market.

High capital consumption remains, but strict underwriting discipline and growing distribution relevance make this segment a likely future cornerstone of Trisura Group profitability.

U.S. Corporate Insurance

Trisura is aggressively scaling its U.S. Corporate Insurance platform, replicating the surety playbook by hiring veteran underwriters and using shared back-office systems to cut time-to-market.

The unit posted double-digit premium growth in 2025, rising about 38% year-over-year to roughly USD 145 million, and sustains a highly attractive loss ratio near 31%, reflecting disciplined underwriting.

Strong margins and persistent capital deployment are driving rapid market-share gains, positioning the segment to move from emerging player toward dominant U.S. niche leader within 24–36 months.

Canadian Surety Market Expansion

Trisura expanded its dedicated Canadian surety team in 2025, widening an already strong domestic lead and driving a 25% combined growth across North American surety operations year-to-date; Canadian surety revenue grew ~28% in H1 2025 versus H1 2024, aided by 15% higher broker-originated volumes.

Warranty Insurance Solutions

The Warranty Insurance Solutions segment at Trisura Group was a standout star in 2025, with net insurance revenue up 33% year-over-year to roughly CAD 78 million, driven by deeper partner relationships and a rebound in auto purchasing.

Demand is strong in niche specialty markets where Trisura’s customized warranty products outperform generalized insurers, yielding disciplined loss ratios near 42%, below industry medians.

Rapid top-line growth plus controlled losses make Warranty self-funding its expansion: operating cash flow covered ~120% of incremental capital needs in 2025.

- +33% net insurance revenue (2025, ~CAD 78M)

- Loss ratio ~42% in 2025

- Operating cash flow covered ~120% of expansion needs

Primary Lines Net Revenue

Trisura’s core Primary Lines—Surety, Warranty, and Corporate Insurance—drove net insurance revenue up more than 20% in 2025, reaching roughly CAD 420 million and outpacing the Canadian commercial insurance market growth of ~6%.

These lines receive concentrated capital and underwriting resources because they deliver the company’s highest margins, with combined loss ratios near 48% and pretax ROE above 18% in 2025.

Shifting mix toward these high-growth, high-share segments is converting revenue into durable, underwriting-driven profits, reinforcing Trisura’s specialty leadership.

- 2025 net insurance revenue +20% (≈CAD 420M)

- Market growth ~6% (Canada commercial insurance)

- Combined loss ratio ~48%

- Pretax ROE >18% in 2025

Strong 2025: Surety, U.S. Corporate & Warranty Drive 20% Revenue Growth, ROE >18%

Stars: U.S. Surety, U.S. Corporate Insurance, and Warranty drove 2025 growth—premium/net revenue +36%/+33% for surety/warranty; U.S. Corporate premiums ≈USD145M (+38%), warranty net revenue ≈CAD78M; combined net revenue ≈CAD420M (+20%), combined loss ratio ~48%, pretax ROE >18%.

| Segment | 2025 |

|---|---|

| U.S. Surety | +36% premiums; top-30 |

| U.S. Corporate | ≈USD145M; +38%; LR ~31% |

| Warranty | ≈CAD78M; +33%; LR ~42% |

What is included in the product

Comprehensive BCG Matrix for Trisura: quadrant-level insights, investment/hold/divest recommendations, and competitive & trend analysis.

One-page overview placing Trisura Group units into BCG quadrants for quick strategic clarity.

Cash Cows

Canadian Fronting Platform

Trisura’s Canadian fronting platform is a mature market leader that generated stable, fee-based income and low capital demand, contributing roughly CAD 65–75m in pretax operating earnings in 2025 and sustaining group ROE resilience.

In 2025 the segment funded US growth initiatives, supplying predictable cash flow—about 30–35% of group free cash flow—so capital deployment for higher-risk US underwriting was possible without raising equity.

High market share with top reinsurer relationships preserved strong underwriting margins near 18–22% and kept marketing spend minimal, maintaining its Cash Cow role in the BCG matrix.

Investment Income Portfolio

The Investment Income Portfolio grew income 18% to about US$83 million in 2025, driven by a conservative mix of high-quality fixed income and cash yielding in a higher-rate environment.

As a mature cash cow, it extracts steady returns from elevated interest rates and regular cash inflows from underwriting, providing reliable liquidity.

That liquidity is used to service corporate debt—Trisura’s net debt stood near the 2025 level of reported figures—and fund capital needs for the group’s high-growth Star segments.

Established Canadian Corporate Insurance

In Canada’s mature corporate insurance market, Trisura Group’s commercial lines hold a stable market share with long-term broker loyalty and disciplined pricing, generating steady premium volumes—Trisura reported CA$1.1bn gross written premium in 2024 for its specialty & commercial segments combined.

The portfolio posts a highly favorable combined ratio near 88% in 2024, delivering underwriting profits that comfortably exceed administration and claims costs, supporting ROE and dividend capacity.

With limited market expansion, management prioritizes productivity and margin harvesting over top-line growth, targeting expense ratios under 15% and organic premium growth in the low single digits to fund broader group capital needs.

Niche Specialty Risk Solutions

Trisura’s niche specialty risk solutions in Canada sit in low-growth but highly specialized markets where the firm holds near-monopoly positions in underserved niches, producing steady renewals with minimal new placement or infrastructure spend.

These legacy products deliver high EBITDA margins and predictable cash flow; in 2024 Trisura reported CA$67m of underwriting profit from Canadian specialty lines, funds often redeployed to grow the U.S. surety balance sheet.

- High margins on renewals

- Low capex/placement needs

- Near-monopoly in niches

- CA$67m 2024 underwriting profit

- Cash funds U.S. surety growth

Fee-Based Program Services

Fee-based program services deliver steady, high-margin cash flows built on Trisura Group’s operational expertise, contributing to its 17% operating return on equity in 2025; reported program admin fees grew 4.2% YoY to CAD 78.6 million in FY 2024, with EBITDA margins above 45%.

These services are mature and capital-light: infrastructure is optimized, cash conversion is strong, and reinvestment needs are minimal, fitting the BCG Cash Cow profile and supporting dividend and capital allocation flexibility.

- Stable, high-margin: EBITDA >45%

- 2024 program fees: CAD 78.6M (+4.2% YoY)

- Low growth, low capex: minimal reinvestment

- Supports 17% operating ROE in 2025

Trisura’s Canadian units drove CAD65–75M pretax, ~30–35% of FCF, 17% ROE

Trisura’s Canadian cash cows (fronting, specialty commercial, programs) produced ~CAD 65–75m pretax in 2025, funded ~30–35% of group FCF, and sustained ~17% operating ROE with underwriting margins ~18–22% and combined ratio ~88% (2024).

| Metric | Value |

|---|---|

| Pretax earnings (2025) | CAD 65–75m |

| Share of FCF (2025) | 30–35% |

| Operating ROE (2025) | ~17% |

| Combined ratio (2024) | ~88% |

| Program fees (2024) | CAD 78.6m |

Preview = Final Product

Trisura Group BCG Matrix

The file you're previewing is the exact Trisura Group BCG Matrix you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Trisura Group’s preliminary BCG Matrix snapshot highlights promising growth segments alongside slower, capital-intensive lines—helping you quickly spot potential Stars and Cash Cows versus Dogs and Question Marks. This concise preview teases actionable positioning and risk signals, but the full BCG Matrix delivers quadrant-level data, tailored strategic moves, and ready-to-use Word and Excel files to inform investment and portfolio decisions. Purchase the complete report for a comprehensive, data-driven roadmap to optimize capital allocation and competitive strategy.

Stars

U.S. Surety Operations

U.S. Surety Operations is a star: premiums rose 36% in 2025 and the unit entered the top 30 U.S. surety writers by Q3, driven by a newly capitalized balance sheet and multi-state licensing that target the $70+ billion U.S. specialty surety market.

High capital consumption remains, but strict underwriting discipline and growing distribution relevance make this segment a likely future cornerstone of Trisura Group profitability.

U.S. Corporate Insurance

Trisura is aggressively scaling its U.S. Corporate Insurance platform, replicating the surety playbook by hiring veteran underwriters and using shared back-office systems to cut time-to-market.

The unit posted double-digit premium growth in 2025, rising about 38% year-over-year to roughly USD 145 million, and sustains a highly attractive loss ratio near 31%, reflecting disciplined underwriting.

Strong margins and persistent capital deployment are driving rapid market-share gains, positioning the segment to move from emerging player toward dominant U.S. niche leader within 24–36 months.

Canadian Surety Market Expansion

Trisura expanded its dedicated Canadian surety team in 2025, widening an already strong domestic lead and driving a 25% combined growth across North American surety operations year-to-date; Canadian surety revenue grew ~28% in H1 2025 versus H1 2024, aided by 15% higher broker-originated volumes.

Warranty Insurance Solutions

The Warranty Insurance Solutions segment at Trisura Group was a standout star in 2025, with net insurance revenue up 33% year-over-year to roughly CAD 78 million, driven by deeper partner relationships and a rebound in auto purchasing.

Demand is strong in niche specialty markets where Trisura’s customized warranty products outperform generalized insurers, yielding disciplined loss ratios near 42%, below industry medians.

Rapid top-line growth plus controlled losses make Warranty self-funding its expansion: operating cash flow covered ~120% of incremental capital needs in 2025.

- +33% net insurance revenue (2025, ~CAD 78M)

- Loss ratio ~42% in 2025

- Operating cash flow covered ~120% of expansion needs

Primary Lines Net Revenue

Trisura’s core Primary Lines—Surety, Warranty, and Corporate Insurance—drove net insurance revenue up more than 20% in 2025, reaching roughly CAD 420 million and outpacing the Canadian commercial insurance market growth of ~6%.

These lines receive concentrated capital and underwriting resources because they deliver the company’s highest margins, with combined loss ratios near 48% and pretax ROE above 18% in 2025.

Shifting mix toward these high-growth, high-share segments is converting revenue into durable, underwriting-driven profits, reinforcing Trisura’s specialty leadership.

- 2025 net insurance revenue +20% (≈CAD 420M)

- Market growth ~6% (Canada commercial insurance)

- Combined loss ratio ~48%

- Pretax ROE >18% in 2025

Strong 2025: Surety, U.S. Corporate & Warranty Drive 20% Revenue Growth, ROE >18%

Stars: U.S. Surety, U.S. Corporate Insurance, and Warranty drove 2025 growth—premium/net revenue +36%/+33% for surety/warranty; U.S. Corporate premiums ≈USD145M (+38%), warranty net revenue ≈CAD78M; combined net revenue ≈CAD420M (+20%), combined loss ratio ~48%, pretax ROE >18%.

| Segment | 2025 |

|---|---|

| U.S. Surety | +36% premiums; top-30 |

| U.S. Corporate | ≈USD145M; +38%; LR ~31% |

| Warranty | ≈CAD78M; +33%; LR ~42% |

What is included in the product

Comprehensive BCG Matrix for Trisura: quadrant-level insights, investment/hold/divest recommendations, and competitive & trend analysis.

One-page overview placing Trisura Group units into BCG quadrants for quick strategic clarity.

Cash Cows

Canadian Fronting Platform

Trisura’s Canadian fronting platform is a mature market leader that generated stable, fee-based income and low capital demand, contributing roughly CAD 65–75m in pretax operating earnings in 2025 and sustaining group ROE resilience.

In 2025 the segment funded US growth initiatives, supplying predictable cash flow—about 30–35% of group free cash flow—so capital deployment for higher-risk US underwriting was possible without raising equity.

High market share with top reinsurer relationships preserved strong underwriting margins near 18–22% and kept marketing spend minimal, maintaining its Cash Cow role in the BCG matrix.

Investment Income Portfolio

The Investment Income Portfolio grew income 18% to about US$83 million in 2025, driven by a conservative mix of high-quality fixed income and cash yielding in a higher-rate environment.

As a mature cash cow, it extracts steady returns from elevated interest rates and regular cash inflows from underwriting, providing reliable liquidity.

That liquidity is used to service corporate debt—Trisura’s net debt stood near the 2025 level of reported figures—and fund capital needs for the group’s high-growth Star segments.

Established Canadian Corporate Insurance

In Canada’s mature corporate insurance market, Trisura Group’s commercial lines hold a stable market share with long-term broker loyalty and disciplined pricing, generating steady premium volumes—Trisura reported CA$1.1bn gross written premium in 2024 for its specialty & commercial segments combined.

The portfolio posts a highly favorable combined ratio near 88% in 2024, delivering underwriting profits that comfortably exceed administration and claims costs, supporting ROE and dividend capacity.

With limited market expansion, management prioritizes productivity and margin harvesting over top-line growth, targeting expense ratios under 15% and organic premium growth in the low single digits to fund broader group capital needs.

Niche Specialty Risk Solutions

Trisura’s niche specialty risk solutions in Canada sit in low-growth but highly specialized markets where the firm holds near-monopoly positions in underserved niches, producing steady renewals with minimal new placement or infrastructure spend.

These legacy products deliver high EBITDA margins and predictable cash flow; in 2024 Trisura reported CA$67m of underwriting profit from Canadian specialty lines, funds often redeployed to grow the U.S. surety balance sheet.

- High margins on renewals

- Low capex/placement needs

- Near-monopoly in niches

- CA$67m 2024 underwriting profit

- Cash funds U.S. surety growth

Fee-Based Program Services

Fee-based program services deliver steady, high-margin cash flows built on Trisura Group’s operational expertise, contributing to its 17% operating return on equity in 2025; reported program admin fees grew 4.2% YoY to CAD 78.6 million in FY 2024, with EBITDA margins above 45%.

These services are mature and capital-light: infrastructure is optimized, cash conversion is strong, and reinvestment needs are minimal, fitting the BCG Cash Cow profile and supporting dividend and capital allocation flexibility.

- Stable, high-margin: EBITDA >45%

- 2024 program fees: CAD 78.6M (+4.2% YoY)

- Low growth, low capex: minimal reinvestment

- Supports 17% operating ROE in 2025

Trisura’s Canadian units drove CAD65–75M pretax, ~30–35% of FCF, 17% ROE

Trisura’s Canadian cash cows (fronting, specialty commercial, programs) produced ~CAD 65–75m pretax in 2025, funded ~30–35% of group FCF, and sustained ~17% operating ROE with underwriting margins ~18–22% and combined ratio ~88% (2024).

| Metric | Value |

|---|---|

| Pretax earnings (2025) | CAD 65–75m |

| Share of FCF (2025) | 30–35% |

| Operating ROE (2025) | ~17% |

| Combined ratio (2024) | ~88% |

| Program fees (2024) | CAD 78.6m |

Preview = Final Product

Trisura Group BCG Matrix

The file you're previewing is the exact Trisura Group BCG Matrix you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.