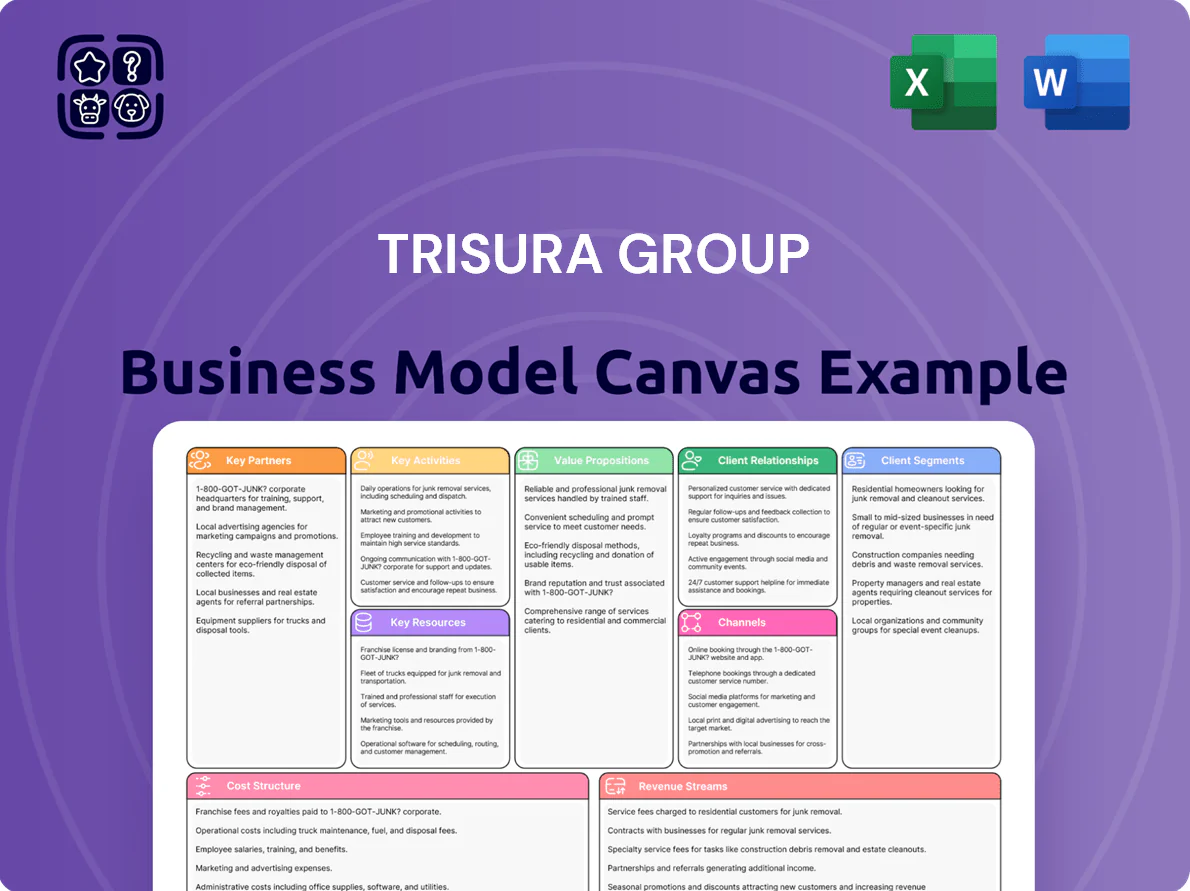

Trisura Group Business Model Canvas

Trisura Group BMC: How specialty underwriting, broker ties & monetization drive growth

Unlock the full strategic blueprint behind Trisura Group’s business model—this concise Business Model Canvas exposes how the firm underwrites risk, builds broker partnerships, and monetizes specialty insurance lines to sustain growth and margin expansion.

Partnerships

Global Reinsurance Partners

Trisura maintains deep relationships with a broad panel of A- to A++ rated global reinsurers, supplying over C$1.2 billion of capital capacity in 2025 to support its fronting and specialty lines and enable writing large-scale risks while capping balance-sheet exposure.

Managing General Agents and MGUs

Trisura partners with Managing General Agents and MGUs that supply niche-market underwriting and programs, acting as an extension of Trisura’s underwriting arm; in 2024 MGAs produced roughly 28% of specialty premium flows industry-wide, helping Trisura scale specialty lines without adding large sales teams.

Independent Broker Networks

Trisura relies on a vast network of independent retail and wholesale brokers as the primary gateway to commercial clients, with brokers accounting for roughly 85% of new specialty premiums in 2024 (C$420m of C$495m). Trisura reinforces these ties via dedicated portal access and SLAs, keeping high-touch service across Canadian and US operations so brokers keep Trisura as the preferred carrier for specialty risks.

Technology and Data Vendors

Strategic alliances with insurtech firms and data providers boost Trisura Group’s underwriting precision and cut processing time; partners supply advanced analytics, third-party data validation, and cloud infrastructure that reduced quote-to-bind time by ~22% in 2024.

As of 2025, these tech partnerships are essential to retain competitiveness in the US fronting market, supporting ~15% annual growth in fronting premium volume.

- Advanced analytics: better risk pricing

- Data validation: lower loss leakage

- Cloud infra: faster deployment

- 2024 impact: 22% faster binds

- 2025: supports 15% premium growth

Regulatory and Industry Bodies

Trisura actively engages Canadian insurers regulators and US state regulators to maintain licences and compliance, supporting its FY2024 gross written premium of CAD 1.1 billion and Solvency ratios above regulatory minima.

Memberships like the Surety Association of Canada give Trisura influence on standards and legislation, underpinning trust and legal standing in tightly regulated markets.

- Regulatory engagement: ongoing licence reviews in Canada + multiple US states

- Industry membership: Surety Association of Canada — advocacy seat

- Financial backing: FY2024 GWP CAD 1.1B; maintained required capital ratios

Trisura ramps C$1.2B reinsurance, tech-driven distribution cuts bind 22%—GWP C$1.1B

Trisura secures C$1.2B reinsurance capacity (2025) and partners with MGAs (≈28% specialty channel, 2024) plus brokers (≈85% new specialty premiums, 2024) and insurtechs that cut quote-to-bind by 22% (2024) and support ~15% fronting premium growth (2025); active regulatory engagement underpinned FY2024 GWP C$1.1B and compliant capital ratios.

| Metric | Value |

|---|---|

| Reinsurance capacity | C$1.2B (2025) |

| MGAs share | 28% (2024) |

| Brokers share | 85% new specialty (2024) |

| Quote-to-bind | -22% (2024) |

| Fronting growth | ~15% (2025) |

| GWP | C$1.1B (FY2024) |

What is included in the product

A concise Business Model Canvas for Trisura Group detailing customer segments, value propositions, channels, revenue streams, key activities, partners, resources, cost structure and risk management, reflecting its specialty in surety, trade credit and risk solutions for commercial and broker clients.

High-level view of Trisura Group’s insurance and surety model with editable cells, condensing underwriting, distribution, and risk management into a one-page snapshot for fast strategic review.

Activities

Specialized Risk Underwriting

Specialized risk underwriting at Trisura Group centers on meticulous assessment and pricing of complex surety, corporate and specialty risks, using historical loss data plus forward-looking analytics; in 2024 Trisura reported a combined ratio of ~72% in surety and specialty lines, reflecting disciplined underwriting. Underwriters target niche markets with tailored policies where standard products fail, keeping gross written premiums growing — 2024 GWP rose 18% to CAD 493M — to meet profitability targets.

Reinsurance Placement and Management

Trisura actively places and manages reinsurance, negotiating terms and monitoring counterparty credit to support its hybrid fronting model; as of FY2024 it ceded ~45% of insured exposure, helping keep statutory capital adequacy above target and producing fee income that was C$78m in 2024.

Claims Management and Advocacy

Trisura runs a claims operation focused on fairness, speed and technical expertise, with internal claims teams working with legal counsel and adjusters to cut loss costs—claims expense ratio was 24.6% in FY2024, helping keep combined ratio near 93%.

High-quality claims handling drives retention—Trisura reported a 2024 policy renewal rate above 82%, showing claims advocacy reinforces contract value for clients and reinsurers.

Program Development and Onboarding

Trisura partners with MGAs to identify and launch specialty insurance programs, performing strict due diligence, drafting policy wording, and building underwriting and claims infrastructure to support scale.

By 2025 Trisura cut average onboarding time to under 90 days, enabling ~15% faster speed-to-market for niche products and supporting a 12% year-over-year increase in new program premiums.

- Due diligence on partners and risks

- Policy wording and product design

- Operational setup: underwriting, claims, IT

- Onboarding <90 days by 2025

- ~15% faster speed-to-market

Capital Allocation and Investment

Management actively monitors capital to meet OSFI and provincial solvency rules while maximizing shareholder returns, targeting a regulatory capital adequacy ratio around 160% and preserving the A- rating from A.M. Best (2025) to enable growth.

The firm invests premium reserves into a diversified portfolio—~70% high-quality fixed income, ~25% equities, ~5% alternatives—yielding a blended return near 4.0% in 2024, giving flexibility for geographic expansion.

- Regulatory target: ~160% capital adequacy

- Rating: A- (A.M. Best, 2025)

- Portfolio mix: 70/25/5 (fixed/eq/alt)

- Blended yield: ~4.0% (2024)

Specialty Surety Leader: CAD493M GWP, ~72% Combined, A- Target & 160% CAR

Underwrite niche surety and specialty risks (2024 GWP CAD 493M, combined ratio ~72% in lines), place/retrieve reinsurance (ceded ~45%, fee income CAD 78M), manage claims (claims ratio 24.6%, renewal >82%), partner with MGAs (onboarding <90 days by 2025, ~15% faster), and steward capital (target CAR ~160%, A- A.M. Best 2025; investment yield ~4.0% in 2024).

| Metric | 2024/2025 |

|---|---|

| GWP | CAD 493M |

| Combined ratio (lines) | ~72% |

| Ceded exposure | ~45% |

| Fee income | CAD 78M |

| Claims ratio | 24.6% |

| Renewal rate | >82% |

| Onboarding | <90 days (2025) |

| Capital target | ~160% CAR |

| Rating | A- (A.M. Best, 2025) |

| Investment yield | ~4.0% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Trisura Group Business Model Canvas—not a mockup—and it matches the exact file you'll receive after purchase; upon payment you'll get the full, editable document in the same professional format ready for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Trisura Group BMC: How specialty underwriting, broker ties & monetization drive growth

Unlock the full strategic blueprint behind Trisura Group’s business model—this concise Business Model Canvas exposes how the firm underwrites risk, builds broker partnerships, and monetizes specialty insurance lines to sustain growth and margin expansion.

Partnerships

Global Reinsurance Partners

Trisura maintains deep relationships with a broad panel of A- to A++ rated global reinsurers, supplying over C$1.2 billion of capital capacity in 2025 to support its fronting and specialty lines and enable writing large-scale risks while capping balance-sheet exposure.

Managing General Agents and MGUs

Trisura partners with Managing General Agents and MGUs that supply niche-market underwriting and programs, acting as an extension of Trisura’s underwriting arm; in 2024 MGAs produced roughly 28% of specialty premium flows industry-wide, helping Trisura scale specialty lines without adding large sales teams.

Independent Broker Networks

Trisura relies on a vast network of independent retail and wholesale brokers as the primary gateway to commercial clients, with brokers accounting for roughly 85% of new specialty premiums in 2024 (C$420m of C$495m). Trisura reinforces these ties via dedicated portal access and SLAs, keeping high-touch service across Canadian and US operations so brokers keep Trisura as the preferred carrier for specialty risks.

Technology and Data Vendors

Strategic alliances with insurtech firms and data providers boost Trisura Group’s underwriting precision and cut processing time; partners supply advanced analytics, third-party data validation, and cloud infrastructure that reduced quote-to-bind time by ~22% in 2024.

As of 2025, these tech partnerships are essential to retain competitiveness in the US fronting market, supporting ~15% annual growth in fronting premium volume.

- Advanced analytics: better risk pricing

- Data validation: lower loss leakage

- Cloud infra: faster deployment

- 2024 impact: 22% faster binds

- 2025: supports 15% premium growth

Regulatory and Industry Bodies

Trisura actively engages Canadian insurers regulators and US state regulators to maintain licences and compliance, supporting its FY2024 gross written premium of CAD 1.1 billion and Solvency ratios above regulatory minima.

Memberships like the Surety Association of Canada give Trisura influence on standards and legislation, underpinning trust and legal standing in tightly regulated markets.

- Regulatory engagement: ongoing licence reviews in Canada + multiple US states

- Industry membership: Surety Association of Canada — advocacy seat

- Financial backing: FY2024 GWP CAD 1.1B; maintained required capital ratios

Trisura ramps C$1.2B reinsurance, tech-driven distribution cuts bind 22%—GWP C$1.1B

Trisura secures C$1.2B reinsurance capacity (2025) and partners with MGAs (≈28% specialty channel, 2024) plus brokers (≈85% new specialty premiums, 2024) and insurtechs that cut quote-to-bind by 22% (2024) and support ~15% fronting premium growth (2025); active regulatory engagement underpinned FY2024 GWP C$1.1B and compliant capital ratios.

| Metric | Value |

|---|---|

| Reinsurance capacity | C$1.2B (2025) |

| MGAs share | 28% (2024) |

| Brokers share | 85% new specialty (2024) |

| Quote-to-bind | -22% (2024) |

| Fronting growth | ~15% (2025) |

| GWP | C$1.1B (FY2024) |

What is included in the product

A concise Business Model Canvas for Trisura Group detailing customer segments, value propositions, channels, revenue streams, key activities, partners, resources, cost structure and risk management, reflecting its specialty in surety, trade credit and risk solutions for commercial and broker clients.

High-level view of Trisura Group’s insurance and surety model with editable cells, condensing underwriting, distribution, and risk management into a one-page snapshot for fast strategic review.

Activities

Specialized Risk Underwriting

Specialized risk underwriting at Trisura Group centers on meticulous assessment and pricing of complex surety, corporate and specialty risks, using historical loss data plus forward-looking analytics; in 2024 Trisura reported a combined ratio of ~72% in surety and specialty lines, reflecting disciplined underwriting. Underwriters target niche markets with tailored policies where standard products fail, keeping gross written premiums growing — 2024 GWP rose 18% to CAD 493M — to meet profitability targets.

Reinsurance Placement and Management

Trisura actively places and manages reinsurance, negotiating terms and monitoring counterparty credit to support its hybrid fronting model; as of FY2024 it ceded ~45% of insured exposure, helping keep statutory capital adequacy above target and producing fee income that was C$78m in 2024.

Claims Management and Advocacy

Trisura runs a claims operation focused on fairness, speed and technical expertise, with internal claims teams working with legal counsel and adjusters to cut loss costs—claims expense ratio was 24.6% in FY2024, helping keep combined ratio near 93%.

High-quality claims handling drives retention—Trisura reported a 2024 policy renewal rate above 82%, showing claims advocacy reinforces contract value for clients and reinsurers.

Program Development and Onboarding

Trisura partners with MGAs to identify and launch specialty insurance programs, performing strict due diligence, drafting policy wording, and building underwriting and claims infrastructure to support scale.

By 2025 Trisura cut average onboarding time to under 90 days, enabling ~15% faster speed-to-market for niche products and supporting a 12% year-over-year increase in new program premiums.

- Due diligence on partners and risks

- Policy wording and product design

- Operational setup: underwriting, claims, IT

- Onboarding <90 days by 2025

- ~15% faster speed-to-market

Capital Allocation and Investment

Management actively monitors capital to meet OSFI and provincial solvency rules while maximizing shareholder returns, targeting a regulatory capital adequacy ratio around 160% and preserving the A- rating from A.M. Best (2025) to enable growth.

The firm invests premium reserves into a diversified portfolio—~70% high-quality fixed income, ~25% equities, ~5% alternatives—yielding a blended return near 4.0% in 2024, giving flexibility for geographic expansion.

- Regulatory target: ~160% capital adequacy

- Rating: A- (A.M. Best, 2025)

- Portfolio mix: 70/25/5 (fixed/eq/alt)

- Blended yield: ~4.0% (2024)

Specialty Surety Leader: CAD493M GWP, ~72% Combined, A- Target & 160% CAR

Underwrite niche surety and specialty risks (2024 GWP CAD 493M, combined ratio ~72% in lines), place/retrieve reinsurance (ceded ~45%, fee income CAD 78M), manage claims (claims ratio 24.6%, renewal >82%), partner with MGAs (onboarding <90 days by 2025, ~15% faster), and steward capital (target CAR ~160%, A- A.M. Best 2025; investment yield ~4.0% in 2024).

| Metric | 2024/2025 |

|---|---|

| GWP | CAD 493M |

| Combined ratio (lines) | ~72% |

| Ceded exposure | ~45% |

| Fee income | CAD 78M |

| Claims ratio | 24.6% |

| Renewal rate | >82% |

| Onboarding | <90 days (2025) |

| Capital target | ~160% CAR |

| Rating | A- (A.M. Best, 2025) |

| Investment yield | ~4.0% |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Trisura Group Business Model Canvas—not a mockup—and it matches the exact file you'll receive after purchase; upon payment you'll get the full, editable document in the same professional format ready for presentation or analysis.