Trivago Porter's Five Forces Analysis

From Overview to Strategy Blueprint

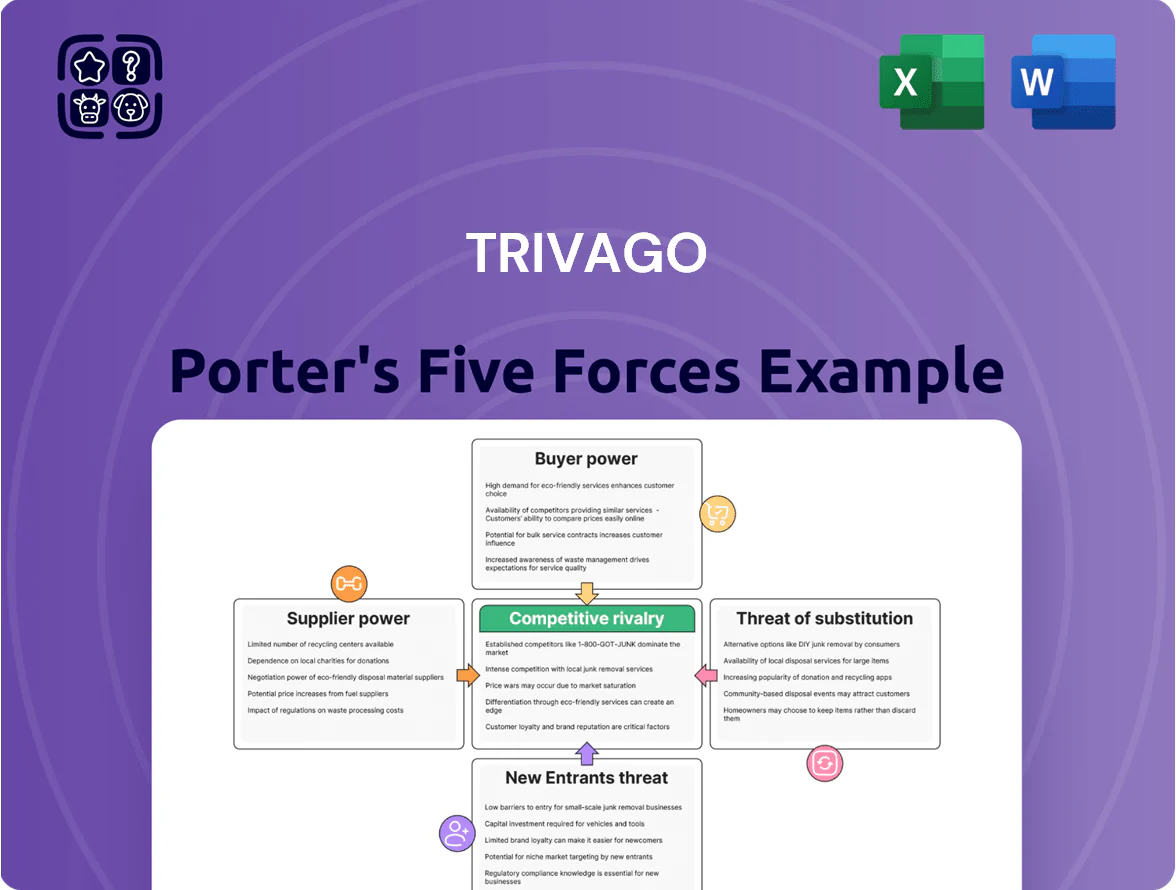

Trivago faces intense buyer power, strong rivalry among online travel platforms, and moderate supplier influence from hotels and OTAs, while threat of new entrants and substitutes hinge on tech differentiation and brand reach; this snapshot highlights key tensions shaping its margins and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trivago’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major OTA Groups

Trivago depends on a few dominant OTAs—Expedia Group and Booking Holdings—which accounted for roughly 45–55% of referral revenue in 2024, creating a concentrated supplier base. These groups operate multiple brands and can demand lower CPCs or shift bidding, squeezing Trivago’s margins and ad yields. That concentration gives suppliers price-setting power and limits Trivago’s negotiation leverage and strategic options.

Direct Hotel Integration Trends

Control Over Data and Inventory

Suppliers control room-availability, real-time pricing, and property metadata that Trivago needs; in 2024 OTAs and hotels provided over 70% of metasearch feed data, so any throttling or higher-latency feeds cut conversion rates and ad yield. If suppliers delay updates by minutes versus seconds, Trivago’s click-to-book accuracy and revenue per click fall; in 2023 Trivago reported a 9% QoQ sensitivity in partner booking yield to feed freshness. This technical dependency gives suppliers indirect leverage over Trivago’s operational efficiency.

Bidding Competition for Ad Placement

Trivago’s CPC/CPA auction lets suppliers bid for visibility; in 2024 Google-listed metasearch spend showed Expedia Group and Booking Holdings each spent over $2.5B on global marketing, letting large suppliers dominate top slots and reduce smaller hotels’ share.

This forces Trivago to balance revenue from high-paying chains—which drive ~60% of clicks—with user need for variety, or risk poorer user experience and higher churn.

- Revenue model: CPC/CPA auction

- Big suppliers: >$2.5B marketing spend (2024)

- Clicks concentration: ~60% from large chains

- Risk: reduced variety, higher churn

Platform Switching Costs for Suppliers

Suppliers can list across metasearch engines, but integrating and managing booking feeds costs engineering time and ad spend; large OTAs report engineering costs ~0.5–1.5% of revenue for integrations (2024 data).

For a major OTA, leaving Trivago reduces reach but typically cuts <1% of their bookings, while Trivago earned €497m revenue in 2023—so lost large-OTA listings hurt Trivago disproportionately.

This asymmetry—higher switching pain for Trivago than for suppliers—gives suppliers bargaining power in pricing and placement terms.

- Integration cost: ~0.5–1.5% revenue

- Trivago revenue 2023: €497m

- Large OTA booking share vs Trivago impact: supplier advantage

Trivago squeezed: OTAs control referrals, hotel direct bookings and ad wars cut margins

Suppliers—mainly Expedia Group and Booking Holdings—accounted for ~45–55% of Trivago referrals in 2024, giving concentrated price-setting power; large hotel chains pushed direct bookings (Marriott 54% direct in 2024), reducing intermediary leverage. Technical feed control and massive OTA marketing (> $2.5B each in 2024) raise switching costs for Trivago and squeeze CPC/CPA yields.

| Metric | 2023–24 |

|---|---|

| Trivago revenue | €497m (2023) |

| Referral share | 45–55% from top OTAs (2024) |

| OTA marketing spend | >$2.5B each (2024) |

| Marriott direct | 54% bookings (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Trivago that uncovers competitive intensity, buyer/supplier power, threat of substitutes and entrants, and identifies disruptive forces and strategic levers impacting its pricing, market share, and profitability.

A concise Trivago Porter’s Five Forces snapshot—visualize competitive intensity and categorize threats quickly for strategic decisions.

Customers Bargaining Power

Low Switching Costs for Travelers

Users face zero financial cost switching from Trivago to Google Hotels or Skyscanner, so price wins over loyalty; 2024 surveys show 68% of online bookers choose the cheapest option per date.

Trivago’s no-subscription model means brand stickiness is low, and price-sensitive travel demand (global OTA bookings ≈ $360B in 2024) amplifies churn.

This ease of movement forces Trivago to spend: marketing plus R&D were 42% of 2024 revenue, driving continual UI and ad investment to retain traffic.

High Price Sensitivity and Transparency

Trivago’s core value is price transparency, attracting highly price-sensitive users who primarily seek the cheapest bookings; in 2024 meta-search travel sites accounted for about 45% of OTA (online travel agency) referral traffic, underscoring this sensitivity. Customers switch platforms when a better deal appears, so loyalty is low and retention hinges on price alone. That dynamic forces Trivago to keep aggregation coverage broad—by 2025 it indexed over 5 million properties—to avoid losing clicks to rivals. Constant price-driven churn compresses CPC yields and raises acquisition costs.

Availability of Information Alternatives

Travelers now consult social media, blogs, and review sites like Google Reviews and TripAdvisor—over 80% of US leisure travelers used peer reviews in 2024, per Phocuswright—so users can cross-check Trivago listings fast.

This abundance cuts intermediaries’ exclusive influence: price discrepancies on OTA listings are verified in minutes, lowering Trivago’s leverage over consumers.

Impact of User Reviews and Ratings

- 94% of leisure travelers used reviews in 2024

- Perceived trust gap can shift ~15% bookings

- User ratings determine platform authority

Expectation of Seamless Mobile Experience

As over 70% of global travel searches now begin on mobile (2024 Google data), users demand snappy apps and sub‑2s load times; even slight friction versus competitors drives immediate abandonment and lost referral revenue for Trivago.

That user sensitivity hands customers bargaining power, forcing Trivago to invest continuously in mobile UX, CDN costs, and faster APIs to retain click-through rates and ad yield.

- 70%+ travel searches on mobile (2024)

- Target load time: <2 seconds

- Small UX lag → immediate abandonment

- Requires ongoing tech spend to protect revenue

Trivago under pressure: price-driven travelers, mobile/meta dominance, 42% rev spent

Customers hold strong bargaining power: zero switching cost to rivals, 68% pick the cheapest option (2024), meta-searches drove ~45% OTA referrals (2024), reviews used by 94% of leisure travelers (2024), mobile >70% searches (2024) — forcing Trivago to spend 42% of 2024 revenue on marketing+R&D to protect click yields.

| Metric | 2024 value |

|---|---|

| Cheap-choice rate | 68% |

| Meta-search OTA referrals | 45% |

| Leisure travelers using reviews | 94% |

| Mobile searches | 70%+ |

| Marketing+R&D spend | 42% rev |

What You See Is What You Get

Trivago Porter's Five Forces Analysis

This preview shows the exact Trivago Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Trivago faces intense buyer power, strong rivalry among online travel platforms, and moderate supplier influence from hotels and OTAs, while threat of new entrants and substitutes hinge on tech differentiation and brand reach; this snapshot highlights key tensions shaping its margins and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Trivago’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major OTA Groups

Trivago depends on a few dominant OTAs—Expedia Group and Booking Holdings—which accounted for roughly 45–55% of referral revenue in 2024, creating a concentrated supplier base. These groups operate multiple brands and can demand lower CPCs or shift bidding, squeezing Trivago’s margins and ad yields. That concentration gives suppliers price-setting power and limits Trivago’s negotiation leverage and strategic options.

Direct Hotel Integration Trends

Control Over Data and Inventory

Suppliers control room-availability, real-time pricing, and property metadata that Trivago needs; in 2024 OTAs and hotels provided over 70% of metasearch feed data, so any throttling or higher-latency feeds cut conversion rates and ad yield. If suppliers delay updates by minutes versus seconds, Trivago’s click-to-book accuracy and revenue per click fall; in 2023 Trivago reported a 9% QoQ sensitivity in partner booking yield to feed freshness. This technical dependency gives suppliers indirect leverage over Trivago’s operational efficiency.

Bidding Competition for Ad Placement

Trivago’s CPC/CPA auction lets suppliers bid for visibility; in 2024 Google-listed metasearch spend showed Expedia Group and Booking Holdings each spent over $2.5B on global marketing, letting large suppliers dominate top slots and reduce smaller hotels’ share.

This forces Trivago to balance revenue from high-paying chains—which drive ~60% of clicks—with user need for variety, or risk poorer user experience and higher churn.

- Revenue model: CPC/CPA auction

- Big suppliers: >$2.5B marketing spend (2024)

- Clicks concentration: ~60% from large chains

- Risk: reduced variety, higher churn

Platform Switching Costs for Suppliers

Suppliers can list across metasearch engines, but integrating and managing booking feeds costs engineering time and ad spend; large OTAs report engineering costs ~0.5–1.5% of revenue for integrations (2024 data).

For a major OTA, leaving Trivago reduces reach but typically cuts <1% of their bookings, while Trivago earned €497m revenue in 2023—so lost large-OTA listings hurt Trivago disproportionately.

This asymmetry—higher switching pain for Trivago than for suppliers—gives suppliers bargaining power in pricing and placement terms.

- Integration cost: ~0.5–1.5% revenue

- Trivago revenue 2023: €497m

- Large OTA booking share vs Trivago impact: supplier advantage

Trivago squeezed: OTAs control referrals, hotel direct bookings and ad wars cut margins

Suppliers—mainly Expedia Group and Booking Holdings—accounted for ~45–55% of Trivago referrals in 2024, giving concentrated price-setting power; large hotel chains pushed direct bookings (Marriott 54% direct in 2024), reducing intermediary leverage. Technical feed control and massive OTA marketing (> $2.5B each in 2024) raise switching costs for Trivago and squeeze CPC/CPA yields.

| Metric | 2023–24 |

|---|---|

| Trivago revenue | €497m (2023) |

| Referral share | 45–55% from top OTAs (2024) |

| OTA marketing spend | >$2.5B each (2024) |

| Marriott direct | 54% bookings (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Trivago that uncovers competitive intensity, buyer/supplier power, threat of substitutes and entrants, and identifies disruptive forces and strategic levers impacting its pricing, market share, and profitability.

A concise Trivago Porter’s Five Forces snapshot—visualize competitive intensity and categorize threats quickly for strategic decisions.

Customers Bargaining Power

Low Switching Costs for Travelers

Users face zero financial cost switching from Trivago to Google Hotels or Skyscanner, so price wins over loyalty; 2024 surveys show 68% of online bookers choose the cheapest option per date.

Trivago’s no-subscription model means brand stickiness is low, and price-sensitive travel demand (global OTA bookings ≈ $360B in 2024) amplifies churn.

This ease of movement forces Trivago to spend: marketing plus R&D were 42% of 2024 revenue, driving continual UI and ad investment to retain traffic.

High Price Sensitivity and Transparency

Trivago’s core value is price transparency, attracting highly price-sensitive users who primarily seek the cheapest bookings; in 2024 meta-search travel sites accounted for about 45% of OTA (online travel agency) referral traffic, underscoring this sensitivity. Customers switch platforms when a better deal appears, so loyalty is low and retention hinges on price alone. That dynamic forces Trivago to keep aggregation coverage broad—by 2025 it indexed over 5 million properties—to avoid losing clicks to rivals. Constant price-driven churn compresses CPC yields and raises acquisition costs.

Availability of Information Alternatives

Travelers now consult social media, blogs, and review sites like Google Reviews and TripAdvisor—over 80% of US leisure travelers used peer reviews in 2024, per Phocuswright—so users can cross-check Trivago listings fast.

This abundance cuts intermediaries’ exclusive influence: price discrepancies on OTA listings are verified in minutes, lowering Trivago’s leverage over consumers.

Impact of User Reviews and Ratings

- 94% of leisure travelers used reviews in 2024

- Perceived trust gap can shift ~15% bookings

- User ratings determine platform authority

Expectation of Seamless Mobile Experience

As over 70% of global travel searches now begin on mobile (2024 Google data), users demand snappy apps and sub‑2s load times; even slight friction versus competitors drives immediate abandonment and lost referral revenue for Trivago.

That user sensitivity hands customers bargaining power, forcing Trivago to invest continuously in mobile UX, CDN costs, and faster APIs to retain click-through rates and ad yield.

- 70%+ travel searches on mobile (2024)

- Target load time: <2 seconds

- Small UX lag → immediate abandonment

- Requires ongoing tech spend to protect revenue

Trivago under pressure: price-driven travelers, mobile/meta dominance, 42% rev spent

Customers hold strong bargaining power: zero switching cost to rivals, 68% pick the cheapest option (2024), meta-searches drove ~45% OTA referrals (2024), reviews used by 94% of leisure travelers (2024), mobile >70% searches (2024) — forcing Trivago to spend 42% of 2024 revenue on marketing+R&D to protect click yields.

| Metric | 2024 value |

|---|---|

| Cheap-choice rate | 68% |

| Meta-search OTA referrals | 45% |

| Leisure travelers using reviews | 94% |

| Mobile searches | 70%+ |

| Marketing+R&D spend | 42% rev |

What You See Is What You Get

Trivago Porter's Five Forces Analysis

This preview shows the exact Trivago Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.