Truist Financial Boston Consulting Group Matrix

Download Your Competitive Advantage

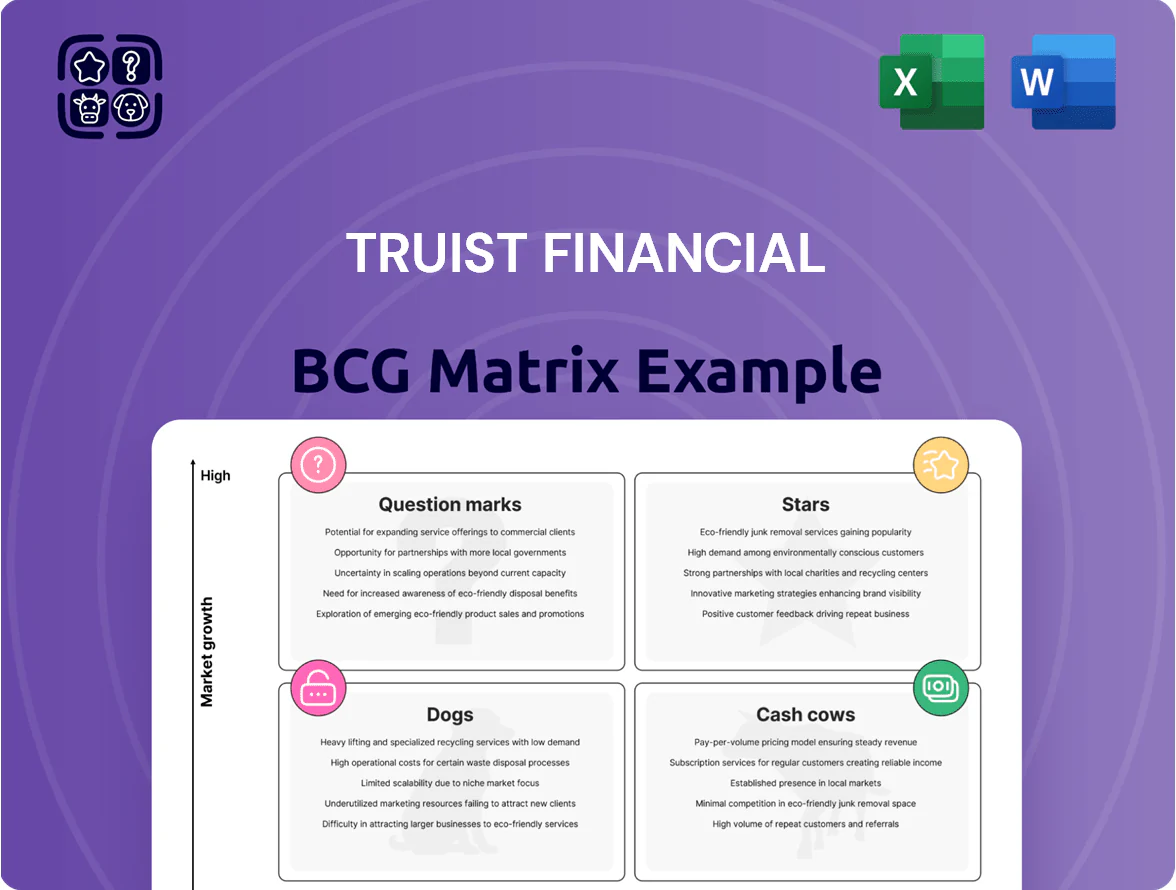

Truist Financial’s BCG Matrix preview highlights where its core segments—consumer banking, commercial lending, wealth management, and insurance—likely fall among Stars, Cash Cows, Dogs, or Question Marks given recent market share and growth trends; this snapshot identifies key opportunities and pressure points for capital allocation. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel files to guide confident investment and strategic decisions.

Stars

Digital Banking and Mobile Platforms

Truist has modernized its digital ecosystem to capture mobile-first consumers, migrating about 68% of active customers to integrated retail and commercial platforms by Q4 2025, up from 42% in 2022.

These platforms need ongoing reinvestment—Truist budgeted $1.1B for technology and cybersecurity in 2025—but they deliver strong market share among Sunbelt tech-savvy demographics, driving ~22% deposit growth in those states year-over-year.

Sunbelt Commercial Real Estate Lending

Sunbelt Commercial Real Estate Lending operates in high-growth Southeastern markets, letting Truist capture large CRE development volume; Florida, Texas, and North Carolina accounted for roughly 45% of regional CRE loan originations in 2024, per Truist filings.

Rapid population influx—Florida +1.2M, Texas +1.0M, North Carolina +400k (2020–2024 census estimates)—drives steady demand for infrastructure and housing projects.

Truist holds a leading regional market share, leveraging deep local relationships and sector expertise to underwrite complex developments; average CRE loan size exceeded $18M in 2024.

The unit is capital-intensive, funding large-scale projects, yet delivered higher returns with portfolio yield ~210 basis points above national CRE averages in 2024 as Sunbelt growth outpaced the U.S.

Wealth Management and Private Banking

Wealth Management and Private Banking sits in the BCG Matrix high-growth, strong-share quadrant after Truist grew AUM to $370 billion by FY2024, leveraging a 2,800-branch retail footprint to upsell HNW services and capture share in core Southeast markets.

Integrating advisory with deposit and lending products raised client retention and fees, pushing fee revenue for wealth to 28% of segment revenue in 2024, while demand for personalized planning and estate services keeps growth elevated.

To defend this star position against national firms, Truist plans continued advisor recruitment (targeting 500 hires 2025) and upgraded digital portfolio tools, requiring ongoing investment to sustain market-leading growth.

Sustainable Finance and ESG Advisory

Truist ranks this segment as a Star: it led $8.2bn in renewable and sustainability-linked loans in 2024, tapping a US market growing ~12% CAGR to 2030 driven by corporate net-zero commitments and tighter regulation.

The bank offers project finance and ESG advisory for wind, solar, grid and green bonds, winning large corporates and hauling fee income and deposit growth while requiring specialist teams and marketing to hold share.

- 2024 originations $8.2bn

- US sustainable finance market ≈12% CAGR to 2030

- High advisory fees, specialist headcount needed

- Strong corporate client partnerships, fast growth

Payments and Treasury Management

The shift to real-time payments and integrated treasury solutions is a high-growth area where Truist holds a strong position, serving corporate clients with real-time ACH and RTP rails and growing treasury revenues ~8–10% annually in 2024.

Truist’s cash-management tools help businesses optimize liquidity amid volatile rates; commercial deposit balances rose 6% YoY to $120B in 2024, boosting fee income and float management.

Digital transformation demands ongoing tech investment to counter fintechs; Truist increased tech spend to $2.1B in 2024, focusing on APIs, ERP integrations, and fraud controls.

High market share in the Mid-Atlantic and Southeast—top-3 deposit share in North Carolina and Florida—keeps Truist a primary partner for regional enterprises.

- Real-time payments growth: +8–10% revenue (2024)

- Commercial deposits: $120B (2024), +6% YoY

- Tech spend: $2.1B (2024)

- Strong regional market share: top-3 in NC and FL

Truist: 68% Digital Adoption, $1.1B Tech Spend, $370B AUM — CRE, Wealth & Sustainable Growth

Truist’s Stars: digital migration 68% of actives (Q4 2025), tech spend $1.1B (2025); CRE/Wealth/sustainable finance AUM $370B (2024), CRE avg loan $18M (2024), sustainable originations $8.2B (2024); commercial deposits $120B (2024), treasury rev growth 8–10% (2024).

| Metric | Value |

|---|---|

| Digital adoption | 68% (Q4 2025) |

| Tech spend | $1.1B (2025) |

| AUM Wealth | $370B (2024) |

| CRE avg loan | $18M (2024) |

| Sustainable originations | $8.2B (2024) |

| Commercial deposits | $120B (2024) |

What is included in the product

BCG Matrix mapping Truist's businesses into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Truist BCG matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Southeastern Retail Deposit Base

Truist’s Southeastern branch network—about 1,700 branches as of 2025—generates a deep, low-cost deposit base (~$450B retail deposits in 2024), yielding stable, cheap funding to support lending and dividends.

Growth upside is limited in this mature market, but high share ensures steady liquidity; upkeep costs are low versus digital-acquisition spend, making these legacy accounts classic BCG cash cows.

Commercial and Industrial Lending

The Commercial and Industrial loan portfolio is a cornerstone of Truist Financial’s profitability, generating stable net interest income—about $6.2 billion of C&I-related NII in 2024 (Truist 2024 10-K)—and serving established firms with recurring credit needs.

This mature segment tracks GDP; Truist saw ~3–4% annual loan growth in C&I from 2022–2024, reflecting steady but low growth versus higher-yielding lines.

Truist’s multidecade client ties and regional footprint create a defensive moat, limiting new-entrant disruption and keeping C&I net charge-offs low (0.25% in 2024).

Cash from C&I interest and fees underwrote ~$1.1 billion in strategic investments and loss provisions in 2024, funding the bank’s more speculative ventures.

Residential Mortgage Servicing

Truist’s residential mortgage servicing handles roughly $400 billion in unpaid principal balance (2025 estimate), producing steady servicing fees that convert to predictable cash flow even as originations drop with rising rates.

Servicing is low-growth but high-margin: existing infrastructure keeps ROE elevated and capital needs minimal, so the unit acts as a cash cow and a reliable hedge during slow GDP growth.

Consumer Credit Card Operations

The Consumer Credit Card Operations generate steady interest and fee income from Truist’s ~10 million retail customers, delivering mid- to high-single-digit ROAA and covering ~15–20% of Truist’s annual net income (2024 est), despite a saturated US card market with low organic growth.

Marketing centers on retention and cross-sell to existing banking clients rather than national acquisition; predictable cash flows fund ~$500–700M annual technology R&D investment.

- Large base: ~10M customers

- Contribution: ~15–20% of net income (2024 est)

- ROAA: mid–high single digits

- R&D funding: $500–700M/year

- Strategy: retention + cross-sell, not national expansion

Indirect Auto Lending

Truist’s indirect auto lending, delivered via a nationwide dealer network, is a classic cash cow: high origination volume (roughly $37 billion in outstanding auto loans at year-end 2024) with mature market growth under 2% annually, yielding steady interest income.

Underwriting and servicing processes are streamlined, keeping charge-offs near 1% and net interest margins healthy, so it generates reliable free cash flow without heavy marketing spend.

It requires minimal strategic shifts and supports capital allocation to higher-growth units while sustaining stable fee and interest revenue.

- ~$37B loans outstanding (2024)

- Market growth <2% annually

- Charge-offs ≈1%

- Low promo spend, high operational efficiency

Truist’s Southeast cash cows: steady deposits, cards, MSR & loans fueling strategic growth

Truist’s cash cows—Southeastern branch deposits (~$450B retail deposits, 1,700 branches, 2025), C&I loans (≈$6.2B C&I NII, 2024), mortgage servicing (~$400B UPB, 2025 est), credit cards (~10M customers, 15–20% net income, 2024 est), and indirect auto loans (~$37B outstanding, 2024)—produce stable, low-growth cash flow funding strategic investments.

| Business | Key metric (year) | Role |

|---|---|---|

| Branch deposits | $450B retail (2024) | Cheap funding |

| C&I loans | $6.2B NII (2024) | Stable income |

| MSR | $400B UPB (2025 est) | Predictable fees |

| Credit cards | 10M cust; 15–20% net income (2024 est) | High-margin fees |

| Auto loans | $37B outstanding (2024) | Reliable interest |

Full Transparency, Always

Truist Financial BCG Matrix

The file you're previewing is the exact Truist Financial BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content, just the fully formatted, analysis-ready document tailored for strategic use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Truist Financial’s BCG Matrix preview highlights where its core segments—consumer banking, commercial lending, wealth management, and insurance—likely fall among Stars, Cash Cows, Dogs, or Question Marks given recent market share and growth trends; this snapshot identifies key opportunities and pressure points for capital allocation. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel files to guide confident investment and strategic decisions.

Stars

Digital Banking and Mobile Platforms

Truist has modernized its digital ecosystem to capture mobile-first consumers, migrating about 68% of active customers to integrated retail and commercial platforms by Q4 2025, up from 42% in 2022.

These platforms need ongoing reinvestment—Truist budgeted $1.1B for technology and cybersecurity in 2025—but they deliver strong market share among Sunbelt tech-savvy demographics, driving ~22% deposit growth in those states year-over-year.

Sunbelt Commercial Real Estate Lending

Sunbelt Commercial Real Estate Lending operates in high-growth Southeastern markets, letting Truist capture large CRE development volume; Florida, Texas, and North Carolina accounted for roughly 45% of regional CRE loan originations in 2024, per Truist filings.

Rapid population influx—Florida +1.2M, Texas +1.0M, North Carolina +400k (2020–2024 census estimates)—drives steady demand for infrastructure and housing projects.

Truist holds a leading regional market share, leveraging deep local relationships and sector expertise to underwrite complex developments; average CRE loan size exceeded $18M in 2024.

The unit is capital-intensive, funding large-scale projects, yet delivered higher returns with portfolio yield ~210 basis points above national CRE averages in 2024 as Sunbelt growth outpaced the U.S.

Wealth Management and Private Banking

Wealth Management and Private Banking sits in the BCG Matrix high-growth, strong-share quadrant after Truist grew AUM to $370 billion by FY2024, leveraging a 2,800-branch retail footprint to upsell HNW services and capture share in core Southeast markets.

Integrating advisory with deposit and lending products raised client retention and fees, pushing fee revenue for wealth to 28% of segment revenue in 2024, while demand for personalized planning and estate services keeps growth elevated.

To defend this star position against national firms, Truist plans continued advisor recruitment (targeting 500 hires 2025) and upgraded digital portfolio tools, requiring ongoing investment to sustain market-leading growth.

Sustainable Finance and ESG Advisory

Truist ranks this segment as a Star: it led $8.2bn in renewable and sustainability-linked loans in 2024, tapping a US market growing ~12% CAGR to 2030 driven by corporate net-zero commitments and tighter regulation.

The bank offers project finance and ESG advisory for wind, solar, grid and green bonds, winning large corporates and hauling fee income and deposit growth while requiring specialist teams and marketing to hold share.

- 2024 originations $8.2bn

- US sustainable finance market ≈12% CAGR to 2030

- High advisory fees, specialist headcount needed

- Strong corporate client partnerships, fast growth

Payments and Treasury Management

The shift to real-time payments and integrated treasury solutions is a high-growth area where Truist holds a strong position, serving corporate clients with real-time ACH and RTP rails and growing treasury revenues ~8–10% annually in 2024.

Truist’s cash-management tools help businesses optimize liquidity amid volatile rates; commercial deposit balances rose 6% YoY to $120B in 2024, boosting fee income and float management.

Digital transformation demands ongoing tech investment to counter fintechs; Truist increased tech spend to $2.1B in 2024, focusing on APIs, ERP integrations, and fraud controls.

High market share in the Mid-Atlantic and Southeast—top-3 deposit share in North Carolina and Florida—keeps Truist a primary partner for regional enterprises.

- Real-time payments growth: +8–10% revenue (2024)

- Commercial deposits: $120B (2024), +6% YoY

- Tech spend: $2.1B (2024)

- Strong regional market share: top-3 in NC and FL

Truist: 68% Digital Adoption, $1.1B Tech Spend, $370B AUM — CRE, Wealth & Sustainable Growth

Truist’s Stars: digital migration 68% of actives (Q4 2025), tech spend $1.1B (2025); CRE/Wealth/sustainable finance AUM $370B (2024), CRE avg loan $18M (2024), sustainable originations $8.2B (2024); commercial deposits $120B (2024), treasury rev growth 8–10% (2024).

| Metric | Value |

|---|---|

| Digital adoption | 68% (Q4 2025) |

| Tech spend | $1.1B (2025) |

| AUM Wealth | $370B (2024) |

| CRE avg loan | $18M (2024) |

| Sustainable originations | $8.2B (2024) |

| Commercial deposits | $120B (2024) |

What is included in the product

BCG Matrix mapping Truist's businesses into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Truist BCG matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Southeastern Retail Deposit Base

Truist’s Southeastern branch network—about 1,700 branches as of 2025—generates a deep, low-cost deposit base (~$450B retail deposits in 2024), yielding stable, cheap funding to support lending and dividends.

Growth upside is limited in this mature market, but high share ensures steady liquidity; upkeep costs are low versus digital-acquisition spend, making these legacy accounts classic BCG cash cows.

Commercial and Industrial Lending

The Commercial and Industrial loan portfolio is a cornerstone of Truist Financial’s profitability, generating stable net interest income—about $6.2 billion of C&I-related NII in 2024 (Truist 2024 10-K)—and serving established firms with recurring credit needs.

This mature segment tracks GDP; Truist saw ~3–4% annual loan growth in C&I from 2022–2024, reflecting steady but low growth versus higher-yielding lines.

Truist’s multidecade client ties and regional footprint create a defensive moat, limiting new-entrant disruption and keeping C&I net charge-offs low (0.25% in 2024).

Cash from C&I interest and fees underwrote ~$1.1 billion in strategic investments and loss provisions in 2024, funding the bank’s more speculative ventures.

Residential Mortgage Servicing

Truist’s residential mortgage servicing handles roughly $400 billion in unpaid principal balance (2025 estimate), producing steady servicing fees that convert to predictable cash flow even as originations drop with rising rates.

Servicing is low-growth but high-margin: existing infrastructure keeps ROE elevated and capital needs minimal, so the unit acts as a cash cow and a reliable hedge during slow GDP growth.

Consumer Credit Card Operations

The Consumer Credit Card Operations generate steady interest and fee income from Truist’s ~10 million retail customers, delivering mid- to high-single-digit ROAA and covering ~15–20% of Truist’s annual net income (2024 est), despite a saturated US card market with low organic growth.

Marketing centers on retention and cross-sell to existing banking clients rather than national acquisition; predictable cash flows fund ~$500–700M annual technology R&D investment.

- Large base: ~10M customers

- Contribution: ~15–20% of net income (2024 est)

- ROAA: mid–high single digits

- R&D funding: $500–700M/year

- Strategy: retention + cross-sell, not national expansion

Indirect Auto Lending

Truist’s indirect auto lending, delivered via a nationwide dealer network, is a classic cash cow: high origination volume (roughly $37 billion in outstanding auto loans at year-end 2024) with mature market growth under 2% annually, yielding steady interest income.

Underwriting and servicing processes are streamlined, keeping charge-offs near 1% and net interest margins healthy, so it generates reliable free cash flow without heavy marketing spend.

It requires minimal strategic shifts and supports capital allocation to higher-growth units while sustaining stable fee and interest revenue.

- ~$37B loans outstanding (2024)

- Market growth <2% annually

- Charge-offs ≈1%

- Low promo spend, high operational efficiency

Truist’s Southeast cash cows: steady deposits, cards, MSR & loans fueling strategic growth

Truist’s cash cows—Southeastern branch deposits (~$450B retail deposits, 1,700 branches, 2025), C&I loans (≈$6.2B C&I NII, 2024), mortgage servicing (~$400B UPB, 2025 est), credit cards (~10M customers, 15–20% net income, 2024 est), and indirect auto loans (~$37B outstanding, 2024)—produce stable, low-growth cash flow funding strategic investments.

| Business | Key metric (year) | Role |

|---|---|---|

| Branch deposits | $450B retail (2024) | Cheap funding |

| C&I loans | $6.2B NII (2024) | Stable income |

| MSR | $400B UPB (2025 est) | Predictable fees |

| Credit cards | 10M cust; 15–20% net income (2024 est) | High-margin fees |

| Auto loans | $37B outstanding (2024) | Reliable interest |

Full Transparency, Always

Truist Financial BCG Matrix

The file you're previewing is the exact Truist Financial BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content, just the fully formatted, analysis-ready document tailored for strategic use.