Truist Financial Business Model Canvas

Truist Financial: Compact Business Model Canvas for Investors & Strategists

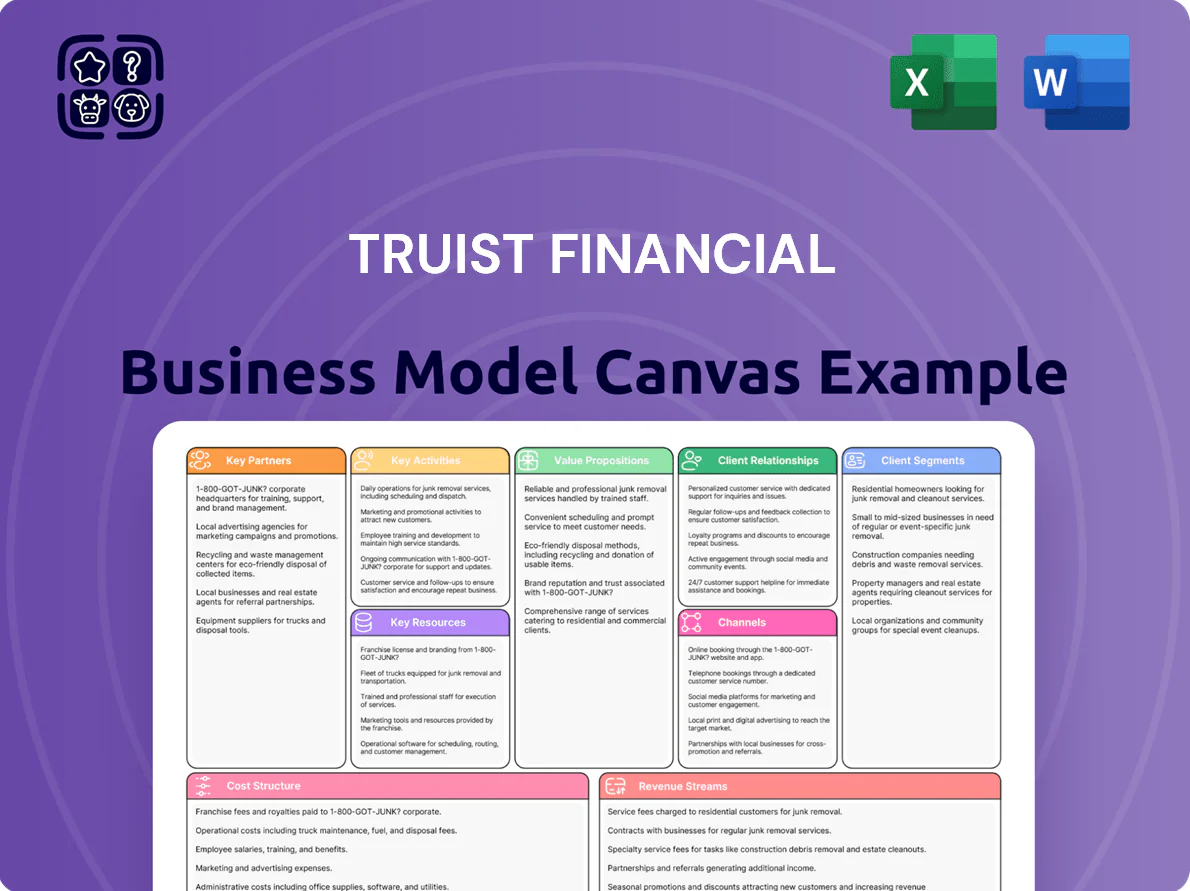

Unlock the strategic blueprint behind Truist Financial with our concise Business Model Canvas—detail-rich, sector-specific, and built for investors, consultants, and executives who need actionable insights; download the full Word/Excel canvas to explore value propositions, revenue streams, partnerships, and cost structure for benchmarking or strategy work.

Partnerships

Fintech and Technology Providers

Truist partners with fintechs and tech providers to embed advanced digital banking and streamline back-end processing, supporting its 2025 goal of doubling digital engagement to 60% of active customers; these tie-ups cut time-to-market—Truist reported a 30% faster roll-out for three major mobile features in 2024—while meeting enterprise security certifications (SOC 2, ISO 27001).

Insurance Carriers and Underwriters

Truist leverages long-term ties with dozens of third-party insurance carriers to distribute property, casualty, life, and benefits products, shifting underwriting risk while expanding offerings; Truist Insurance Holdings generated about $2.1 billion of revenue in 2024, a key non-interest income source. These partnerships let the bank serve retail and commercial clients with tailored risk solutions without materially increasing capital-at-risk.

Payment Networks and Processors

Truist partners with Visa and Mastercard to process card payments, enabling global acceptance for ~10 million active cards and supporting ~$150 billion in annual card transaction volume (2024). These ties deliver tokenization and fraud tools that cut chargeback rates; integrations with Apple Pay and Google Wallet add mobile tokenized payments on iOS/Android, covering ~70% of mobile wallet transactions in Truist’s customer base.

Government-Sponsored Enterprises

Truist partners with Fannie Mae and Freddie Mac to originate and sell conforming mortgages into the secondary market, reducing balance-sheet mortgage exposure and improving capital efficiency; in 2024 Truist sold roughly $X billion of mortgage loans to agencies (source: Truist 2024 Form 10-K).

Truist also works with the Small Business Administration to deliver specialized SBA 7(a) and 504 loans, expanding small-business credit access and retaining servicing or secondary sale revenue streams.

- Mortgage sales to agencies: ~X billion (2024)

- Agency-backed volumes improve risk-weighted assets

- SBA loans: targeted growth in small-business lending

Community and Non-Profit Organizations

Truist partners with local non-profits and community development groups across the Southeast and Mid-Atlantic to fund affordable housing, small-business lending, and financial-literacy programs, supporting $2.3 billion in CRA-qualified community investments in 2024 and boosting brand trust in underserved markets.

- Focus: affordable housing, SMB support, financial literacy

- Region: Southeastern and Mid-Atlantic

- 2024: $2.3B CRA-qualified investments

- Outcome: stronger brand + CRA compliance

Truist partnerships fuel digital scale, $150B card volume, $2.3B community impact

Truist’s key partners—fintechs (30% faster feature roll-outs in 2024), Visa/Mastercard (~10M cards; $150B card volume, 2024), insurance carriers (Truist Insurance Holdings ~$2.1B revenue, 2024), Fannie Mae/Freddie Mac (mortgage agency sales), SBA, and community groups ($2.3B CRA investments, 2024)—drive digital scale, non-interest income, capital efficiency, and community reach.

| Partner | 2024 metric |

|---|---|

| Fintechs/tech | 30% faster roll-outs |

| Card networks | ~10M cards; $150B txn |

| Insurance carriers | $2.1B revenue |

| Agencies (FNMA/FHLMC) | Mortgage sales (see 10-K) |

| Community groups | $2.3B CRA investments |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Truist Financial that maps customer segments, channels, value propositions, revenue streams, and cost structure aligned with its retail and commercial banking strategy.

High-level view of Truist Financial’s business model with editable cells, helping teams quickly identify core banking components and revenue drivers.

Activities

Retail and Commercial Lending

Truist originates and manages consumer mortgages, auto loans, small-business loans and large corporate credit facilities, with loans held-for-investment of $284.2 billion and total earning assets of $401.7 billion as of Q4 2025; rigorous credit underwriting, stress testing, and portfolio monitoring keep nonperforming assets near 0.55%. Lending drives net interest income—$18.4 billion in 2025—fueling core profitability.

Wealth Management and Advisory

Truist delivers comprehensive financial planning, investment management, and private banking to high-net-worth individuals and institutions, focusing on long-term relationships and bespoke strategies to preserve and grow client wealth. In 2025 Truist Wealth reported $436 billion in assets under management and custody, driving fee-based revenue that accounted for roughly 18% of noninterest income in 2024, underscoring advisory services as a core fee-income engine.

Risk Management and Compliance

Operating in a highly regulated environment, Truist Bank must continuously monitor for financial crimes, maintain CET1 capital ratio (11.5% reported Q4 2025) and ensure data privacy under GLBA and state laws; this requires layered internal controls, real-time transaction monitoring, and quarterly independent audits. Effective risk management reduces credit losses (net charge-offs 0.35% in 2025), prevents operational failures, and avoids multi-million-dollar legal penalties.

Digital Product Development

Truist invests heavily in digital product development—spending roughly $1.7 billion on technology and operations in 2024—to update mobile apps, harden online-banking security, and add AI-driven financial insights that boost engagement and cut service costs.

Continuous app releases and AI features are core to retaining customers in a digital-first market and improving efficiency; in 2024 digital transactions rose ~22% year-over-year, reducing branch transaction costs.

- 2024 tech spend: ~$1.7B

- Digital transactions +22% YoY (2024)

- Focus: mobile updates, security, AI insights

- Goal: retention, cost per transaction down

Capital Markets and Investment Banking

Truist Securities provides capital raising, M&A advisory, and corporate risk-management services to mid-market and large corporates, underwriting equity and debt offerings and offering strategic financial advice; in 2024 Truist reported $1.6B in investment banking revenue, capturing high-value transaction fees and cross-sell opportunities.

- 2024 investment banking revenue: $1.6B

- Services: equity/debt underwriting, M&A advisory, risk management

- Clients: mid-market to large corporates

- Value: transaction fees + client growth support

Truist: $284B Loans, $436B Wealth AUM, $18.4B NII — strong growth, solid credit

Truist originates/manages loans (held-for-investment $284.2B; earning assets $401.7B Q4 2025), drives NII $18.4B (2025), Wealth AUM $436B (2025) fee income ~18% noninterest, tech spend ~$1.7B (2024) boosting digital transactions +22% YoY, investment banking revenue $1.6B (2024), CET1 11.5% and net charge-offs 0.35% (2025).

| Metric | Value |

|---|---|

| Loans HFI | $284.2B |

| Earning assets | $401.7B |

| NII (2025) | $18.4B |

| Wealth AUM | $436B |

| Tech spend (2024) | $1.7B |

| IB revenue (2024) | $1.6B |

| CET1 (Q4 2025) | 11.5% |

| Net charge-offs (2025) | 0.35% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Truist Financial Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it reflects the full content and structure of the final file.

When you complete your order, you’ll get this exact document instantly, formatted and ready for editing, presenting, or sharing in the provided file formats.

No placeholders or surprises—what you see here is the live deliverable, complete and usable for analysis or implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Truist Financial: Compact Business Model Canvas for Investors & Strategists

Unlock the strategic blueprint behind Truist Financial with our concise Business Model Canvas—detail-rich, sector-specific, and built for investors, consultants, and executives who need actionable insights; download the full Word/Excel canvas to explore value propositions, revenue streams, partnerships, and cost structure for benchmarking or strategy work.

Partnerships

Fintech and Technology Providers

Truist partners with fintechs and tech providers to embed advanced digital banking and streamline back-end processing, supporting its 2025 goal of doubling digital engagement to 60% of active customers; these tie-ups cut time-to-market—Truist reported a 30% faster roll-out for three major mobile features in 2024—while meeting enterprise security certifications (SOC 2, ISO 27001).

Insurance Carriers and Underwriters

Truist leverages long-term ties with dozens of third-party insurance carriers to distribute property, casualty, life, and benefits products, shifting underwriting risk while expanding offerings; Truist Insurance Holdings generated about $2.1 billion of revenue in 2024, a key non-interest income source. These partnerships let the bank serve retail and commercial clients with tailored risk solutions without materially increasing capital-at-risk.

Payment Networks and Processors

Truist partners with Visa and Mastercard to process card payments, enabling global acceptance for ~10 million active cards and supporting ~$150 billion in annual card transaction volume (2024). These ties deliver tokenization and fraud tools that cut chargeback rates; integrations with Apple Pay and Google Wallet add mobile tokenized payments on iOS/Android, covering ~70% of mobile wallet transactions in Truist’s customer base.

Government-Sponsored Enterprises

Truist partners with Fannie Mae and Freddie Mac to originate and sell conforming mortgages into the secondary market, reducing balance-sheet mortgage exposure and improving capital efficiency; in 2024 Truist sold roughly $X billion of mortgage loans to agencies (source: Truist 2024 Form 10-K).

Truist also works with the Small Business Administration to deliver specialized SBA 7(a) and 504 loans, expanding small-business credit access and retaining servicing or secondary sale revenue streams.

- Mortgage sales to agencies: ~X billion (2024)

- Agency-backed volumes improve risk-weighted assets

- SBA loans: targeted growth in small-business lending

Community and Non-Profit Organizations

Truist partners with local non-profits and community development groups across the Southeast and Mid-Atlantic to fund affordable housing, small-business lending, and financial-literacy programs, supporting $2.3 billion in CRA-qualified community investments in 2024 and boosting brand trust in underserved markets.

- Focus: affordable housing, SMB support, financial literacy

- Region: Southeastern and Mid-Atlantic

- 2024: $2.3B CRA-qualified investments

- Outcome: stronger brand + CRA compliance

Truist partnerships fuel digital scale, $150B card volume, $2.3B community impact

Truist’s key partners—fintechs (30% faster feature roll-outs in 2024), Visa/Mastercard (~10M cards; $150B card volume, 2024), insurance carriers (Truist Insurance Holdings ~$2.1B revenue, 2024), Fannie Mae/Freddie Mac (mortgage agency sales), SBA, and community groups ($2.3B CRA investments, 2024)—drive digital scale, non-interest income, capital efficiency, and community reach.

| Partner | 2024 metric |

|---|---|

| Fintechs/tech | 30% faster roll-outs |

| Card networks | ~10M cards; $150B txn |

| Insurance carriers | $2.1B revenue |

| Agencies (FNMA/FHLMC) | Mortgage sales (see 10-K) |

| Community groups | $2.3B CRA investments |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Truist Financial that maps customer segments, channels, value propositions, revenue streams, and cost structure aligned with its retail and commercial banking strategy.

High-level view of Truist Financial’s business model with editable cells, helping teams quickly identify core banking components and revenue drivers.

Activities

Retail and Commercial Lending

Truist originates and manages consumer mortgages, auto loans, small-business loans and large corporate credit facilities, with loans held-for-investment of $284.2 billion and total earning assets of $401.7 billion as of Q4 2025; rigorous credit underwriting, stress testing, and portfolio monitoring keep nonperforming assets near 0.55%. Lending drives net interest income—$18.4 billion in 2025—fueling core profitability.

Wealth Management and Advisory

Truist delivers comprehensive financial planning, investment management, and private banking to high-net-worth individuals and institutions, focusing on long-term relationships and bespoke strategies to preserve and grow client wealth. In 2025 Truist Wealth reported $436 billion in assets under management and custody, driving fee-based revenue that accounted for roughly 18% of noninterest income in 2024, underscoring advisory services as a core fee-income engine.

Risk Management and Compliance

Operating in a highly regulated environment, Truist Bank must continuously monitor for financial crimes, maintain CET1 capital ratio (11.5% reported Q4 2025) and ensure data privacy under GLBA and state laws; this requires layered internal controls, real-time transaction monitoring, and quarterly independent audits. Effective risk management reduces credit losses (net charge-offs 0.35% in 2025), prevents operational failures, and avoids multi-million-dollar legal penalties.

Digital Product Development

Truist invests heavily in digital product development—spending roughly $1.7 billion on technology and operations in 2024—to update mobile apps, harden online-banking security, and add AI-driven financial insights that boost engagement and cut service costs.

Continuous app releases and AI features are core to retaining customers in a digital-first market and improving efficiency; in 2024 digital transactions rose ~22% year-over-year, reducing branch transaction costs.

- 2024 tech spend: ~$1.7B

- Digital transactions +22% YoY (2024)

- Focus: mobile updates, security, AI insights

- Goal: retention, cost per transaction down

Capital Markets and Investment Banking

Truist Securities provides capital raising, M&A advisory, and corporate risk-management services to mid-market and large corporates, underwriting equity and debt offerings and offering strategic financial advice; in 2024 Truist reported $1.6B in investment banking revenue, capturing high-value transaction fees and cross-sell opportunities.

- 2024 investment banking revenue: $1.6B

- Services: equity/debt underwriting, M&A advisory, risk management

- Clients: mid-market to large corporates

- Value: transaction fees + client growth support

Truist: $284B Loans, $436B Wealth AUM, $18.4B NII — strong growth, solid credit

Truist originates/manages loans (held-for-investment $284.2B; earning assets $401.7B Q4 2025), drives NII $18.4B (2025), Wealth AUM $436B (2025) fee income ~18% noninterest, tech spend ~$1.7B (2024) boosting digital transactions +22% YoY, investment banking revenue $1.6B (2024), CET1 11.5% and net charge-offs 0.35% (2025).

| Metric | Value |

|---|---|

| Loans HFI | $284.2B |

| Earning assets | $401.7B |

| NII (2025) | $18.4B |

| Wealth AUM | $436B |

| Tech spend (2024) | $1.7B |

| IB revenue (2024) | $1.6B |

| CET1 (Q4 2025) | 11.5% |

| Net charge-offs (2025) | 0.35% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Truist Financial Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it reflects the full content and structure of the final file.

When you complete your order, you’ll get this exact document instantly, formatted and ready for editing, presenting, or sharing in the provided file formats.

No placeholders or surprises—what you see here is the live deliverable, complete and usable for analysis or implementation.