Truist Financial PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid fintech innovation are reshaping Truist Financial’s strategic landscape—our concise PESTLE snapshot highlights key external risks and opportunities you can act on today. Purchase the full PESTLE Analysis to access a detailed, editable report with evidence-backed insights for investors, strategists, and advisors. Get the complete breakdown instantly and make smarter, faster decisions.

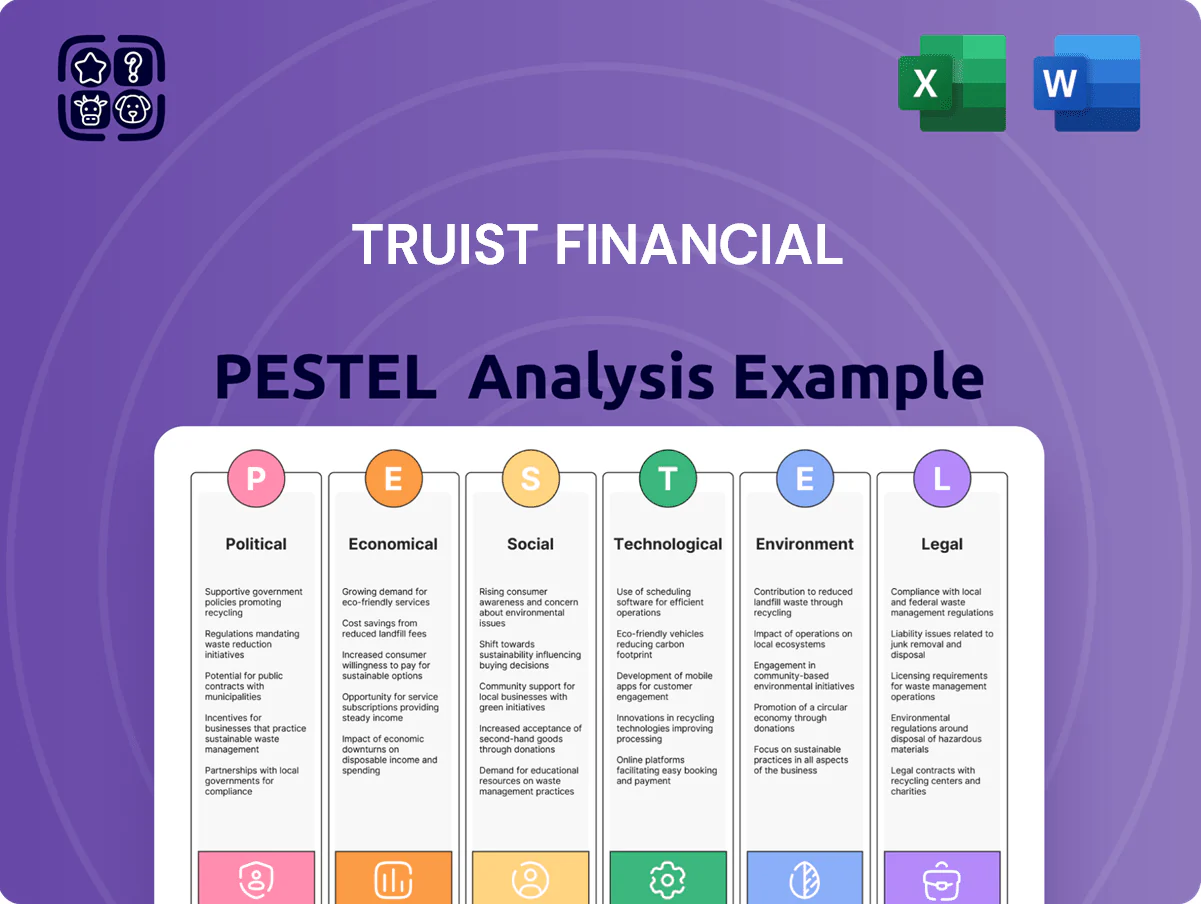

Political factors

Federal Regulatory Oversight

The 2024 administration shift tightened oversight for large regional banks; the FDIC and OCC signaled stress-test expansions impacting banks with assets above $100 billion, including Truist (2023 assets $563.8B). Policymakers aim to balance stability and competition, pressuring higher capital buffers—Truist reported CET1 ratio 10.9% (2024 Q3). Truist must align capital planning and growth targets with evolving executive directives to remain compliant and competitive.

Tax Policy Transitions

Adjustments to corporate tax structures in late 2025 reduced Truist’s effective tax rate from 20.8% in FY2024 to an estimated 18.5%, compressing reported net income by roughly $420 million annually and forcing reallocation of capital toward tax-efficient instruments.

Revisions to federal and state tax credits for banks cut qualifying credits by about 15% in 2025, prompting Truist to intensify tax planning to preserve shareholder ROE near its 12.4% target.

These fiscal shifts have increased Truist’s preference for Southeast-focused tax-advantaged municipal bonds and low-tax lease financing, which comprised 22% of new investments in 2025.

Geopolitical Market Volatility

Ongoing global geopolitical tensions—including elevated US-China strategic rivalry and the 2024 Middle East conflicts—are increasing capital-market volatility, pressuring Truist’s investment banking fees and wealth-management AUM flows; global equity VIX spiked to averages ~22–28 in 2024 versus ~17 in 2023, reducing transaction volumes. Fluctuations in trade policy and sanctions can abruptly cut market liquidity and shift investor sentiment, impacting underwriting and cross-border M&A. Truist actively monitors macro-political events, deploying scenario analyses and stress tests to advise corporate clients navigating a fragmented global economy and to protect fee-based revenue streams.

Regional Legislative Influence

Regional legislative climates in the Southeast and Mid-Atlantic materially shape Truist’s operations, with the bank’s core markets—Georgia, North Carolina, Virginia, and Florida—accounting for over 60% of its branch network and significant deposit base as of 2025.

Pro-business statutes and state tax incentives have driven corporate relocations, bolstering demand for Truist’s commercial lending and deposit services, evidenced by regional CRE loan growth of roughly 7% YoY in 2024.

Maintaining close ties with governors and legislatures is critical for navigating state banking statutes, economic development programs, and public-private financing initiatives that directly affect Truist’s loan origination and fee income.

- 60%+ branch/deposit concentration in core states (2025)

- Regional CRE loan growth ~7% YoY (2024)

- Reliance on state tax/incentive policy for commercial demand

Government Infrastructure Spending

Bank weathers tighter oversight as tax cuts, CRE growth and infrastructure boost loans

Political shifts tightened bank oversight (assets $563.8B, CET1 10.9% 2024 Q3), tax changes cut effective rate from 20.8% to ~18.5% (2025), regional pro-business policies drove CRE loan growth ~7% YoY (2024), infrastructure funding >$1.2T expanded project finance (commercial loans +6.5% YoY 2024); geopolitical volatility raised VIX to ~22–28 (2024).

| Metric | Value |

|---|---|

| Assets (2023) | $563.8B |

| CET1 (2024 Q3) | 10.9% |

| Eff. tax rate (2024→2025) | 20.8%→18.5% |

| CRE loan growth (2024) | ~7% YoY |

| Commercial loans (YoY 2024) | +6.5% |

| VIX (avg 2024) | ~22–28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Truist Financial, with data-driven trends, forward-looking insights, and actionable implications to support executives, consultants, and investors in strategy, risk management, and funding decisions.

A concise Truist Financial PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Interest Rate Environment

As the Fed stabilizes rates near 5.25–5.50% by late 2025, Truist faces pressure to protect a net interest margin that averaged 2.79% in 2024; plateauing rates compress potential yield pickup on new loans while deposit costs, which rose to a cost of funds around 1.10% in 2024, remain elevated. Truist must balance asset yields and rising deposit costs through tactical repricing, strategic hedging, and active asset-liability management to sustain profitability and CET1 ratios.

Southeastern Economic Resilience

The Southeast grew about 2.8% in 2024 versus a 2.0% US average, bolstering Truist’s footprint across NC, GA and FL; state GDP gains and 2023–24 net migration added roughly 1.1 million residents to those states, expanding retail deposit bases.

Strong business investment—Georgia and North Carolina saw 6–8% annual capex increases in 2023–24—feeds commercial lending opportunities for Truist.

Regional resilience reduced portfolio volatility during 2023–24 national slowdowns, helping Truist sustain long-term revenue targets tied to retail deposit growth and commercial loan origination.

Inflationary Cost Management

Persistent inflation through 2024–25 raised Truist’s operating costs, notably talent and tech spend; Truist reported noninterest expense of $11.1B in 2024, prompting efficiency programs targeting $1B in annual savings while maintaining $2.0B+ annual technology investment to accelerate digital transformation.

Credit Quality and Risk Modeling

By late 2025 Truist increased loan loss reserves to 1.25% of loans amid signs of cycle maturity, directing capital toward credit quality and forward-looking provisioning.

The bank applies machine-learning models across a $460bn loan book to track PD and LGD by segment, improving early-warning detection for small business and corporate exposures.

Proactive risk actions—sector limits and stress-tested capital buffers—help maintain CET1 above 10.5%, cushioning localized downturns.

- Loan loss reserves 1.25% of loans

- $460bn loan portfolio monitored

- CET1 ratio >10.5%

Capital Markets Recovery

Resurgent M&A and IPO markets in late 2025 lifted Truist’s non-interest income, with investment banking fees rising ~18% YoY as deal volume recovered to pre-2023 levels.

Higher market valuations and steadier corporate earnings spurred strategic transactions and capital raises, increasing underwriting activity by ~22% in Q4 2025.

Truist Securities gained share in mid-market and large corporate advisory, supporting a 15% increase in advisory mandates and strengthening fee diversification.

- Investment banking fees +18% YoY (late 2025)

- Underwriting activity +22% in Q4 2025

- Advisory mandates +15% year-end 2025

Truist: ALM, hedging crucial as NIMs compress; Southeast growth fuels deposits

Fed rates near 5.25–5.50% through late 2025 compress NIM (2.79% in 2024) while deposit costs (~1.10% in 2024) stay elevated; Truist’s ALM, hedging, and repricing are key to protect margins and CET1 (>10.5%). Southeast GDP growth ~2.8% in 2024 and net migration (+1.1M) expand retail deposits; capex up 6–8% in GA/NC boosts commercial lending. Noninterest expense $11.1B (2024) spurred $1B efficiency target; loan loss reserves 1.25% of loans on $460B book.

| Metric | Value |

|---|---|

| NIM (2024) | 2.79% |

| Cost of funds (2024) | ~1.10% |

| Noninterest expense (2024) | $11.1B |

| Loan book | $460B |

| LLR | 1.25% of loans |

| CET1 | >10.5% |

| Southeast GDP growth (2024) | ~2.8% |

What You See Is What You Get

Truist Financial PESTLE Analysis

The preview shown here is the exact Truist Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid fintech innovation are reshaping Truist Financial’s strategic landscape—our concise PESTLE snapshot highlights key external risks and opportunities you can act on today. Purchase the full PESTLE Analysis to access a detailed, editable report with evidence-backed insights for investors, strategists, and advisors. Get the complete breakdown instantly and make smarter, faster decisions.

Political factors

Federal Regulatory Oversight

The 2024 administration shift tightened oversight for large regional banks; the FDIC and OCC signaled stress-test expansions impacting banks with assets above $100 billion, including Truist (2023 assets $563.8B). Policymakers aim to balance stability and competition, pressuring higher capital buffers—Truist reported CET1 ratio 10.9% (2024 Q3). Truist must align capital planning and growth targets with evolving executive directives to remain compliant and competitive.

Tax Policy Transitions

Adjustments to corporate tax structures in late 2025 reduced Truist’s effective tax rate from 20.8% in FY2024 to an estimated 18.5%, compressing reported net income by roughly $420 million annually and forcing reallocation of capital toward tax-efficient instruments.

Revisions to federal and state tax credits for banks cut qualifying credits by about 15% in 2025, prompting Truist to intensify tax planning to preserve shareholder ROE near its 12.4% target.

These fiscal shifts have increased Truist’s preference for Southeast-focused tax-advantaged municipal bonds and low-tax lease financing, which comprised 22% of new investments in 2025.

Geopolitical Market Volatility

Ongoing global geopolitical tensions—including elevated US-China strategic rivalry and the 2024 Middle East conflicts—are increasing capital-market volatility, pressuring Truist’s investment banking fees and wealth-management AUM flows; global equity VIX spiked to averages ~22–28 in 2024 versus ~17 in 2023, reducing transaction volumes. Fluctuations in trade policy and sanctions can abruptly cut market liquidity and shift investor sentiment, impacting underwriting and cross-border M&A. Truist actively monitors macro-political events, deploying scenario analyses and stress tests to advise corporate clients navigating a fragmented global economy and to protect fee-based revenue streams.

Regional Legislative Influence

Regional legislative climates in the Southeast and Mid-Atlantic materially shape Truist’s operations, with the bank’s core markets—Georgia, North Carolina, Virginia, and Florida—accounting for over 60% of its branch network and significant deposit base as of 2025.

Pro-business statutes and state tax incentives have driven corporate relocations, bolstering demand for Truist’s commercial lending and deposit services, evidenced by regional CRE loan growth of roughly 7% YoY in 2024.

Maintaining close ties with governors and legislatures is critical for navigating state banking statutes, economic development programs, and public-private financing initiatives that directly affect Truist’s loan origination and fee income.

- 60%+ branch/deposit concentration in core states (2025)

- Regional CRE loan growth ~7% YoY (2024)

- Reliance on state tax/incentive policy for commercial demand

Government Infrastructure Spending

Bank weathers tighter oversight as tax cuts, CRE growth and infrastructure boost loans

Political shifts tightened bank oversight (assets $563.8B, CET1 10.9% 2024 Q3), tax changes cut effective rate from 20.8% to ~18.5% (2025), regional pro-business policies drove CRE loan growth ~7% YoY (2024), infrastructure funding >$1.2T expanded project finance (commercial loans +6.5% YoY 2024); geopolitical volatility raised VIX to ~22–28 (2024).

| Metric | Value |

|---|---|

| Assets (2023) | $563.8B |

| CET1 (2024 Q3) | 10.9% |

| Eff. tax rate (2024→2025) | 20.8%→18.5% |

| CRE loan growth (2024) | ~7% YoY |

| Commercial loans (YoY 2024) | +6.5% |

| VIX (avg 2024) | ~22–28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Truist Financial, with data-driven trends, forward-looking insights, and actionable implications to support executives, consultants, and investors in strategy, risk management, and funding decisions.

A concise Truist Financial PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Interest Rate Environment

As the Fed stabilizes rates near 5.25–5.50% by late 2025, Truist faces pressure to protect a net interest margin that averaged 2.79% in 2024; plateauing rates compress potential yield pickup on new loans while deposit costs, which rose to a cost of funds around 1.10% in 2024, remain elevated. Truist must balance asset yields and rising deposit costs through tactical repricing, strategic hedging, and active asset-liability management to sustain profitability and CET1 ratios.

Southeastern Economic Resilience

The Southeast grew about 2.8% in 2024 versus a 2.0% US average, bolstering Truist’s footprint across NC, GA and FL; state GDP gains and 2023–24 net migration added roughly 1.1 million residents to those states, expanding retail deposit bases.

Strong business investment—Georgia and North Carolina saw 6–8% annual capex increases in 2023–24—feeds commercial lending opportunities for Truist.

Regional resilience reduced portfolio volatility during 2023–24 national slowdowns, helping Truist sustain long-term revenue targets tied to retail deposit growth and commercial loan origination.

Inflationary Cost Management

Persistent inflation through 2024–25 raised Truist’s operating costs, notably talent and tech spend; Truist reported noninterest expense of $11.1B in 2024, prompting efficiency programs targeting $1B in annual savings while maintaining $2.0B+ annual technology investment to accelerate digital transformation.

Credit Quality and Risk Modeling

By late 2025 Truist increased loan loss reserves to 1.25% of loans amid signs of cycle maturity, directing capital toward credit quality and forward-looking provisioning.

The bank applies machine-learning models across a $460bn loan book to track PD and LGD by segment, improving early-warning detection for small business and corporate exposures.

Proactive risk actions—sector limits and stress-tested capital buffers—help maintain CET1 above 10.5%, cushioning localized downturns.

- Loan loss reserves 1.25% of loans

- $460bn loan portfolio monitored

- CET1 ratio >10.5%

Capital Markets Recovery

Resurgent M&A and IPO markets in late 2025 lifted Truist’s non-interest income, with investment banking fees rising ~18% YoY as deal volume recovered to pre-2023 levels.

Higher market valuations and steadier corporate earnings spurred strategic transactions and capital raises, increasing underwriting activity by ~22% in Q4 2025.

Truist Securities gained share in mid-market and large corporate advisory, supporting a 15% increase in advisory mandates and strengthening fee diversification.

- Investment banking fees +18% YoY (late 2025)

- Underwriting activity +22% in Q4 2025

- Advisory mandates +15% year-end 2025

Truist: ALM, hedging crucial as NIMs compress; Southeast growth fuels deposits

Fed rates near 5.25–5.50% through late 2025 compress NIM (2.79% in 2024) while deposit costs (~1.10% in 2024) stay elevated; Truist’s ALM, hedging, and repricing are key to protect margins and CET1 (>10.5%). Southeast GDP growth ~2.8% in 2024 and net migration (+1.1M) expand retail deposits; capex up 6–8% in GA/NC boosts commercial lending. Noninterest expense $11.1B (2024) spurred $1B efficiency target; loan loss reserves 1.25% of loans on $460B book.

| Metric | Value |

|---|---|

| NIM (2024) | 2.79% |

| Cost of funds (2024) | ~1.10% |

| Noninterest expense (2024) | $11.1B |

| Loan book | $460B |

| LLR | 1.25% of loans |

| CET1 | >10.5% |

| Southeast GDP growth (2024) | ~2.8% |

What You See Is What You Get

Truist Financial PESTLE Analysis

The preview shown here is the exact Truist Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.