Trupanion Porter's Five Forces Analysis

From Overview to Strategy Blueprint

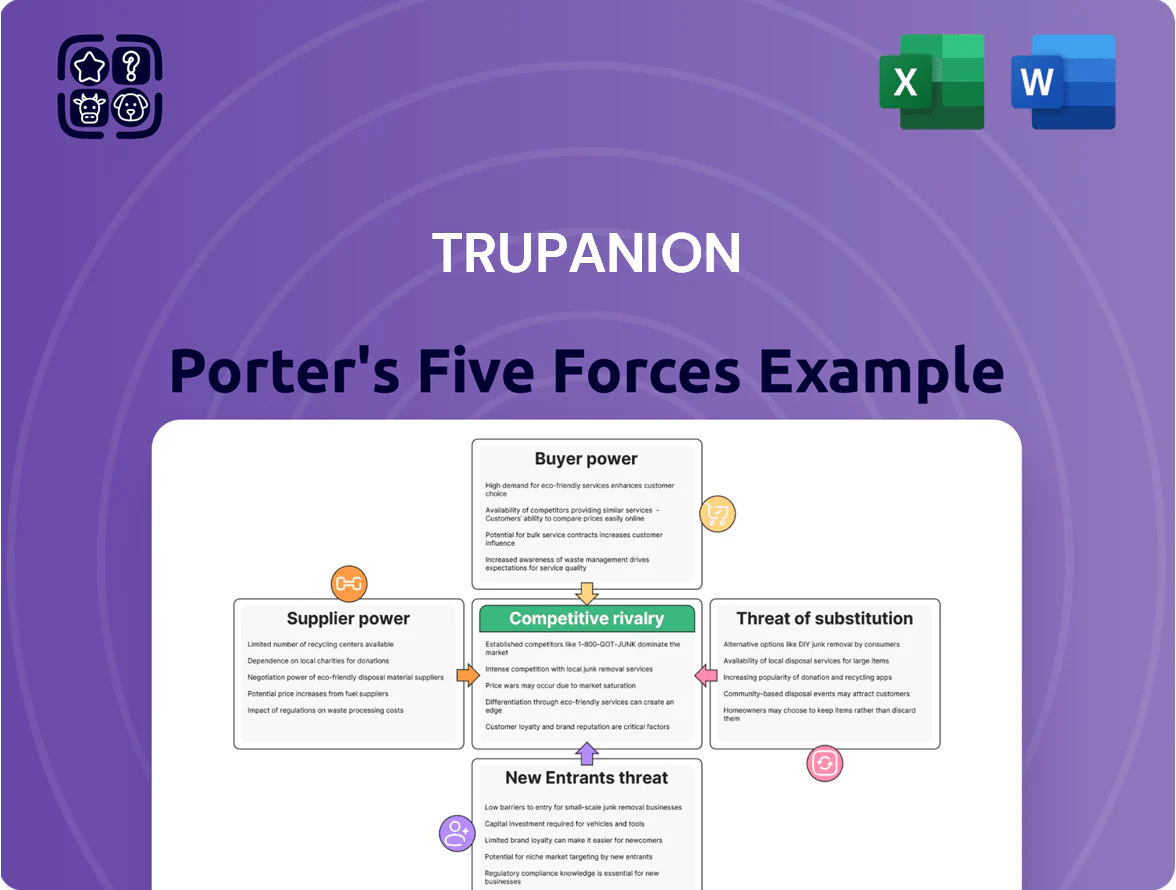

Trupanion faces moderate supplier power, niche buyer segments with growing bargaining leverage, and intensifying rivalry from insurers and insurtech entrants—while regulatory and substitute risks remain manageable but evolving; this snapshot highlights strategic fault lines and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Trupanion.

Suppliers Bargaining Power

Veterinary Service Providers

Reinsurance Capital Markets

Trupanion uses reinsurance to smooth capital volatility and cede portions of underwriting risk to global reinsurers; in 2024 reinsurance ceded reduced net retained loss exposure by roughly 18% versus gross, helping stabilize statutory capital.

Reinsurance capacity and cost track macro factors and global P&C results—2023–24 industry combined ratios rose above 103%, tightening capacity and lifting premium rates about 10–15% in specialty lines.

If reinsurers demand higher rates or cut limits, Trupanion would face pressure on its capital ratios and likely raise policy pricing or retain more risk, which could reduce earnings unless loss trends improve.

Specialized Labor and Veterinary Technicians

Trupanion depends on specialized staff—veterinary technicians and trained claims adjusters—to process complex medical claims; in 2025 demand is high as vet clinics and insurtechs compete for the same talent pool.

Industry data shows U.S. veterinary technician median pay rose 12% from 2020–2024 to about $40,000 in 2024, pressuring Trupanion’s labor costs and margins.

Specialized training needs and rising wages increase supplier bargaining power and raise per-claim processing costs, challenging unit economics.

Data and Cloud Infrastructure Partners

Trupanion relies on proprietary software plus third-party data and cloud partners for real-time claims adjudication; these vendors are critical to the Vet Direct Pay system that drives faster payouts and higher retention.

In 2024 Trupanion reported ~78% of claims paid via Vet Direct Pay and depends on specialized tech stacks where a 10–20% vendor price hike or multi-hour outage could cut perceived service quality and raise operating costs.

- High dependency: proprietary+third-party tech

- Service risk: outages hit Vet Direct Pay speed

- Price risk: 10–20% vendor hikes raise costs

Regulatory Oversight Bodies

State insurance commissioners and regulators control approval of Trupanion’s rate filings and policy changes, so Trupanion cannot unilaterally raise premiums to match costs.

With 2025 veterinary inflation near 8–10% nationally, the speed of regulatory approvals directly determines Trupanion’s ability to pass costs to customers.

This approval bottleneck reduces Trupanion’s short-term revenue flexibility and increases lag-driven margin pressure when claim costs rise faster than approved rates.

- Regulators approve rate changes

- 2025 vet inflation ~8–10%

- Approval delays = revenue lag

- Limits rapid margin recovery

Supplier squeeze: rising vet costs, reinsurance drag and wage pressure cut Trupanion margins

Suppliers (vets, reinsurers, tech, labor, regulators) hold high leverage: 2024–25 vet inflation ~6.5%→8–10%, reinsurance ceded ~18% of loss exposure, Vet Direct Pay processed ~78% claims, vet tech median pay ~$40,000 (2024). These factors raise input costs and limit Trupanion’s short-term pricing flexibility, pressuring margins unless rates or loss trends change.

| Supplier | Key 2024–25 Metric |

|---|---|

| Veterinary inflation | 6.5% (thru 2024); ~8–10% (2025) |

| Reinsurance | Ceded ≈18% of gross loss exposure (2024) |

| Vet Direct Pay | ~78% claims paid (2024) |

| Vet tech pay | Median $40,000 (2024, +12% since 2020) |

What is included in the product

Tailored Porter's Five Forces analysis for Trupanion that uncovers competitive intensity, buyer/supplier leverage, entry barriers, and substitute threats—highlighting disruptive risks, pricing power, and strategic levers to protect and grow market share.

Concise Trupanion Porter’s Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to relieve decision-making pain.

Customers Bargaining Power

Switching Costs for Chronic Conditions

Existing Trupanion policyholders with pets having chronic or pre-existing conditions face very high switching costs because new insurers typically exclude those conditions, creating strong lock-in; this lowers bargaining power for a large share of customers — Trupanion reported 1.12 million enrolled pets in 2024, many with renewals carrying prior-condition coverage.

Price Sensitivity and Household Budgets

Despite strong pet-owner ties, 2025 veterinary inflation hit ~11% year-over-year, pushing Trupanion premiums up and sharpening customer price sensitivity; as monthly costs rise, many choose higher deductibles or lower payout options to cut premiums.

If perceived cost-to-value falls, churn will likely climb among younger, healthier pets—these cohorts made up ~42% of new policies in 2024, so retention risk is material.

Information Transparency and Comparison Tools

The 2025 market shows high transparency: over 65% of US pet owners use comparison sites (2024 APPA survey) to compare quotes in seconds, pushing shoppers toward lowest intro rates and flexible terms.

New owners often pick plans on price and short-term perks, raising churn risk for incumbents with higher premiums.

Trupanion leans on features like no payout caps and 90% reimbursement to defend premium positioning versus limited-benefit, low-cost rivals.

Veterinary Channel Influence

A large share of Trupanion’s new policies come via veterinary clinic referrals, shifting bargaining power from the individual to the vet at point of sale; in 2024 vets influenced roughly 55% of new enrollments per company disclosures.

When a trusted veterinarian recommends Trupanion, customers accept plan terms more readily and price sensitivity falls, reducing typical comparison shopping and haggling.

This placement in the clinical workflow creates a durable buffer versus consumer-led bargaining and supports higher retention—Trupanion reported a 91% policy retention rate in 2024 for clinic-origin customers.

- ~55% new enrollments via vet referrals (2024)

- 91% retention for clinic-origin policies (2024)

- Lower price-shopping at point of vet recommendation

Brand Loyalty and Trust

Trupanion’s 2025 positioning emphasizes medical reliability over low price, attracting high-net-worth owners and committed enthusiasts who value the direct-pay feature that covers veterinary bills instantly; this reduces price sensitivity and weakens customer bargaining on premiums.

Brand equity and claims-paid trust lowered churn to ~6.2% in 2024–25 among top-tier policyholders, creating a loyal segment less likely to shop solely on monthly cost.

- Direct-pay reduces out-of-pocket friction

- Lower churn ~6.2% for premium segment

- High-net-worth owners show weaker price sensitivity

Moderate customer leverage: clinic lock‑in offsets vet inflation and price‑shopping risks

Customers’ bargaining power is moderate: strong lock-in for pets with prior conditions (1.12M enrolled pets, 2024) and clinic referrals (~55% of new enrollments, 2024) reduce price pressure, while rising veterinary inflation (~11% YoY, 2025) and heavy price-shopping (65% use comparison sites, 2024 APPA) raise sensitivity and churn risk among younger, healthier cohorts (42% of 2024 new policies).

| Metric | Value |

|---|---|

| Enrolled pets (2024) | 1.12M |

| Vets influence new enrollments (2024) | ~55% |

| Clinic-origin retention (2024) | 91% |

| Overall churn (2024–25) | ~6.2% |

| Vet inflation (2025) | ~11% YoY |

| Use comparison sites (2024) | ~65% |

Full Version Awaits

Trupanion Porter's Five Forces Analysis

This preview shows the exact Trupanion Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Trupanion faces moderate supplier power, niche buyer segments with growing bargaining leverage, and intensifying rivalry from insurers and insurtech entrants—while regulatory and substitute risks remain manageable but evolving; this snapshot highlights strategic fault lines and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Trupanion.

Suppliers Bargaining Power

Veterinary Service Providers

Reinsurance Capital Markets

Trupanion uses reinsurance to smooth capital volatility and cede portions of underwriting risk to global reinsurers; in 2024 reinsurance ceded reduced net retained loss exposure by roughly 18% versus gross, helping stabilize statutory capital.

Reinsurance capacity and cost track macro factors and global P&C results—2023–24 industry combined ratios rose above 103%, tightening capacity and lifting premium rates about 10–15% in specialty lines.

If reinsurers demand higher rates or cut limits, Trupanion would face pressure on its capital ratios and likely raise policy pricing or retain more risk, which could reduce earnings unless loss trends improve.

Specialized Labor and Veterinary Technicians

Trupanion depends on specialized staff—veterinary technicians and trained claims adjusters—to process complex medical claims; in 2025 demand is high as vet clinics and insurtechs compete for the same talent pool.

Industry data shows U.S. veterinary technician median pay rose 12% from 2020–2024 to about $40,000 in 2024, pressuring Trupanion’s labor costs and margins.

Specialized training needs and rising wages increase supplier bargaining power and raise per-claim processing costs, challenging unit economics.

Data and Cloud Infrastructure Partners

Trupanion relies on proprietary software plus third-party data and cloud partners for real-time claims adjudication; these vendors are critical to the Vet Direct Pay system that drives faster payouts and higher retention.

In 2024 Trupanion reported ~78% of claims paid via Vet Direct Pay and depends on specialized tech stacks where a 10–20% vendor price hike or multi-hour outage could cut perceived service quality and raise operating costs.

- High dependency: proprietary+third-party tech

- Service risk: outages hit Vet Direct Pay speed

- Price risk: 10–20% vendor hikes raise costs

Regulatory Oversight Bodies

State insurance commissioners and regulators control approval of Trupanion’s rate filings and policy changes, so Trupanion cannot unilaterally raise premiums to match costs.

With 2025 veterinary inflation near 8–10% nationally, the speed of regulatory approvals directly determines Trupanion’s ability to pass costs to customers.

This approval bottleneck reduces Trupanion’s short-term revenue flexibility and increases lag-driven margin pressure when claim costs rise faster than approved rates.

- Regulators approve rate changes

- 2025 vet inflation ~8–10%

- Approval delays = revenue lag

- Limits rapid margin recovery

Supplier squeeze: rising vet costs, reinsurance drag and wage pressure cut Trupanion margins

Suppliers (vets, reinsurers, tech, labor, regulators) hold high leverage: 2024–25 vet inflation ~6.5%→8–10%, reinsurance ceded ~18% of loss exposure, Vet Direct Pay processed ~78% claims, vet tech median pay ~$40,000 (2024). These factors raise input costs and limit Trupanion’s short-term pricing flexibility, pressuring margins unless rates or loss trends change.

| Supplier | Key 2024–25 Metric |

|---|---|

| Veterinary inflation | 6.5% (thru 2024); ~8–10% (2025) |

| Reinsurance | Ceded ≈18% of gross loss exposure (2024) |

| Vet Direct Pay | ~78% claims paid (2024) |

| Vet tech pay | Median $40,000 (2024, +12% since 2020) |

What is included in the product

Tailored Porter's Five Forces analysis for Trupanion that uncovers competitive intensity, buyer/supplier leverage, entry barriers, and substitute threats—highlighting disruptive risks, pricing power, and strategic levers to protect and grow market share.

Concise Trupanion Porter’s Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to relieve decision-making pain.

Customers Bargaining Power

Switching Costs for Chronic Conditions

Existing Trupanion policyholders with pets having chronic or pre-existing conditions face very high switching costs because new insurers typically exclude those conditions, creating strong lock-in; this lowers bargaining power for a large share of customers — Trupanion reported 1.12 million enrolled pets in 2024, many with renewals carrying prior-condition coverage.

Price Sensitivity and Household Budgets

Despite strong pet-owner ties, 2025 veterinary inflation hit ~11% year-over-year, pushing Trupanion premiums up and sharpening customer price sensitivity; as monthly costs rise, many choose higher deductibles or lower payout options to cut premiums.

If perceived cost-to-value falls, churn will likely climb among younger, healthier pets—these cohorts made up ~42% of new policies in 2024, so retention risk is material.

Information Transparency and Comparison Tools

The 2025 market shows high transparency: over 65% of US pet owners use comparison sites (2024 APPA survey) to compare quotes in seconds, pushing shoppers toward lowest intro rates and flexible terms.

New owners often pick plans on price and short-term perks, raising churn risk for incumbents with higher premiums.

Trupanion leans on features like no payout caps and 90% reimbursement to defend premium positioning versus limited-benefit, low-cost rivals.

Veterinary Channel Influence

A large share of Trupanion’s new policies come via veterinary clinic referrals, shifting bargaining power from the individual to the vet at point of sale; in 2024 vets influenced roughly 55% of new enrollments per company disclosures.

When a trusted veterinarian recommends Trupanion, customers accept plan terms more readily and price sensitivity falls, reducing typical comparison shopping and haggling.

This placement in the clinical workflow creates a durable buffer versus consumer-led bargaining and supports higher retention—Trupanion reported a 91% policy retention rate in 2024 for clinic-origin customers.

- ~55% new enrollments via vet referrals (2024)

- 91% retention for clinic-origin policies (2024)

- Lower price-shopping at point of vet recommendation

Brand Loyalty and Trust

Trupanion’s 2025 positioning emphasizes medical reliability over low price, attracting high-net-worth owners and committed enthusiasts who value the direct-pay feature that covers veterinary bills instantly; this reduces price sensitivity and weakens customer bargaining on premiums.

Brand equity and claims-paid trust lowered churn to ~6.2% in 2024–25 among top-tier policyholders, creating a loyal segment less likely to shop solely on monthly cost.

- Direct-pay reduces out-of-pocket friction

- Lower churn ~6.2% for premium segment

- High-net-worth owners show weaker price sensitivity

Moderate customer leverage: clinic lock‑in offsets vet inflation and price‑shopping risks

Customers’ bargaining power is moderate: strong lock-in for pets with prior conditions (1.12M enrolled pets, 2024) and clinic referrals (~55% of new enrollments, 2024) reduce price pressure, while rising veterinary inflation (~11% YoY, 2025) and heavy price-shopping (65% use comparison sites, 2024 APPA) raise sensitivity and churn risk among younger, healthier cohorts (42% of 2024 new policies).

| Metric | Value |

|---|---|

| Enrolled pets (2024) | 1.12M |

| Vets influence new enrollments (2024) | ~55% |

| Clinic-origin retention (2024) | 91% |

| Overall churn (2024–25) | ~6.2% |

| Vet inflation (2025) | ~11% YoY |

| Use comparison sites (2024) | ~65% |

Full Version Awaits

Trupanion Porter's Five Forces Analysis

This preview shows the exact Trupanion Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.