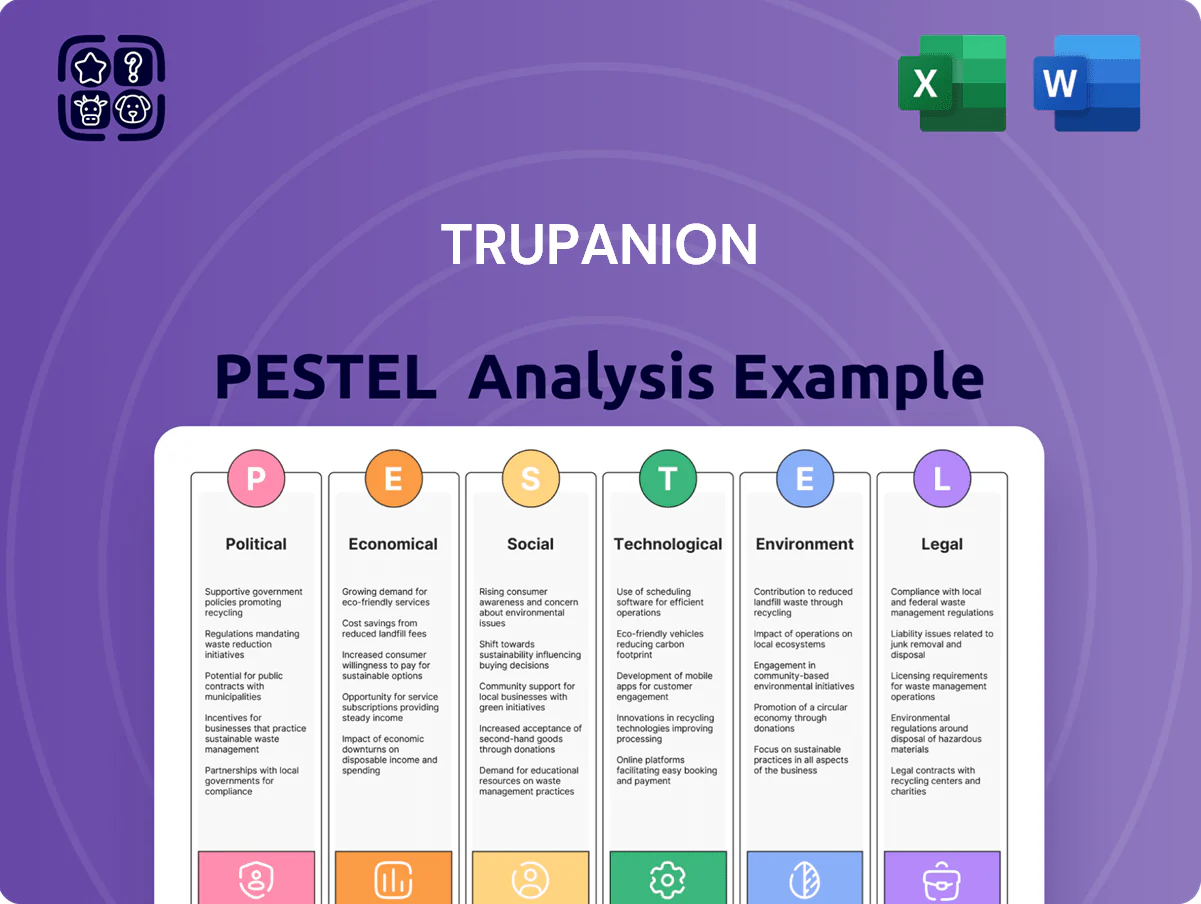

Trupanion PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how regulatory shifts, pet-owner demographics, and tech-driven claims processing are reshaping Trupanion’s growth and risk profile—our PESTLE distills these forces into strategic insights you can act on. Purchase the full analysis to access detailed implications, scenario planning, and ready-to-use slides for investment decisions or boardroom strategy.

Political factors

Regulatory oversight of insurance rate filings

State insurance departments wield direct control over Trupanion by approving or denying rate filings; in 2024 Trupanion secured roughly 6–8% average annual premium increases in contested states, but approvals vary widely by jurisdiction.

As of late 2025 the political focus on consumer protection demands transparent claims and loss-ratio data—Trupanion reported a 2024 medical loss ratio near 82%, a key metric regulators scrutinize to justify rate hikes.

Regulatory delays compress margins when veterinary cost inflation, which rose about 9% YoY in 2023–24, outpaces permitted premium growth, forcing temporary earnings pressure reflected in quarterly underwriting losses.

International trade and expansion policies

Trupanion, active across North America and expanding into Europe and Asia, faces reliance on stable trade agreements; EU pet insurance regulation alignment and post-Brexit UK rules affect market entry and pricing, with 2025 revenue from international operations targeted at roughly 10-12% of total (Trupanion guidance 2024–2025). Political shifts in foreign investment laws or licensing can add regulatory compliance costs and delay launches, potentially increasing CAC by an estimated 5–15%. Navigating diverse geopolitical risks—sanctions, data-localization, and tariff changes—remains a core executive challenge for scaling profitably.

Governmental healthcare policy shifts

Shifts in human healthcare policy can ripple into veterinary care; for example, US proposals to cap medical fees could inspire analogous state bills affecting vet reimbursement, pushing Trupanion's loss ratios (2024 combined ratio ~84%) if average claim severity rises above its 20% premium growth in 2023–24. Monitoring licensure/regulation trends—14 states considered vet licensure bills in 2024—helps forecast actuarial impacts on pricing and reserves.

Taxation policies and corporate incentives

Changes in corporate tax rates or new financial services levies in the US and Canada can erode Trupanion’s net margin; a 1% effective tax increase on 2025 projected premiums (~$1.1B in gross written premiums 2024) could reduce net income by millions.

Ongoing policy debates on whether pet insurance premiums or employer-provided pet benefits are tax-deductible affect uptake in employer-sponsored channels that drove ~20% of new subscriptions in 2024.

Trupanion must update its state/province-level financial models to reflect differing tax treatments and potential surtaxes, using scenario analyses to stress-test profitability under varying tax regimes.

- 1% tax rise ≈ multimillion-dollar net income hit vs 2024 GWP $1.1B

- Employer channel ~20% of 2024 new subscriptions; tax deductibility shifts demand

- State/province scenario modeling required for accurate pricing and reserve planning

Advocacy for animal welfare legislation

Political momentum for animal welfare drives stricter pet-care laws; 2024 saw 18 US states consider microchipping or anti-cruelty bills, raising owner duties and regulatory compliance costs for clinics.

Mandated microchipping and health checks increase veterinary visits—U.S. vet visits rose 6% in 2023 to 162 million, likely boosting Trupanion claim frequency and premium uptake.

Elevating pets to family status correlates with higher insurance demand; U.S. pet insurance penetration rose to ~4.0% in 2024, benefiting Trupanion’s revenue growth trajectory.

- Stricter laws → more vet care, higher claims

- 2023 vet visits: 162M (+6%) → higher utilization

- 2024 pet insurance penetration ~4.0% → market tailwind for Trupanion

Rate caps vs 9% vet cost inflation squeeze Trupanion margins as MLR hits ~82%

Regulatory rate approvals vary by state—2024 avg contested increases ~6–8%—and regulators scrutinize Trupanion’s 2024 medical loss ratio ~82%, pressuring margins when vet cost inflation (~9% YoY 2023–24) outpaces allowed premiums.

| Metric | 2023–2024 |

|---|---|

| Contested rate approvals | 6–8% |

| Medical loss ratio | ~82% |

| Vet cost inflation | ~9% YoY |

| GWP | $1.1B (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Trupanion across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios tailored to the pet insurance market.

Condensed PESTLE insights for Trupanion, organized by category for quick reference during meetings or presentations and easily dropped into slides or shared across teams.

Economic factors

Impact of veterinary medical inflation

The rise in advanced veterinary procedures has pushed average claim costs up about 7–9% annually through 2024, directly pressuring Trupanion’s loss ratio and prompting mid-2024 rate increases averaging ~8% across plans.

As sophisticated diagnostics and specialty care raise per-claim severity—U.S. pet medical spending reached $37.2B in 2023—Trupanion requires continual actuarial resets to sustain margins.

Trupanion’s data-driven pricing and proprietary claims dataset, which supported a 2023 combined ratio improvement to ~103%, underpin its ability to offset medical inflation and serve as a competitive moat.

Discretionary spending and consumer confidence

Pet insurance is semi-discretionary, so Trupanion is sensitive to disposable income swings; in 2024 US consumer confidence averaged 99.0 and household savings rates fell to ~3.8%, risking slower new enrollments during downturns. Trupanion’s net retention remained strong—2025 YTD policy renewal rates ~95%—indicating existing members prioritize coverage. Economic stability through end-2025 is critical to sustain historical pet enrollment growth (~10–12% annual).

Interest rate environment and investment income

The prevailing interest rate environment materially affects Trupanion’s investment income on float and capital reserves; higher U.S. short-term rates (Fed funds at 5.25–5.50% in 2024) boosted investment yield, helping produce roughly $92 million of investment income in 2024 and buffering operating costs. Elevated yields support the balance sheet and can offset underwriting shortfalls, while a prolonged low-rate scenario would force greater reliance on underwriting margins to sustain profitability.

Labor market dynamics for veterinary professionals

Shortages of veterinarians and technicians have pushed average clinic wage growth to about 6–8% annually in 2023–2024, driving higher treatment prices that are often shifted to pet owners and insurers like Trupanion.

Competition for skilled medical staff across specialty and general practice raises claim costs; Trupanion reported claim severity increases consistent with labor-driven price pressures in its 2024 filings.

The company tracks regional employment metrics and licensure trends to model expected veterinary service cost changes and adjust pricing, reserving, and underwriting assumptions accordingly.

- Wage growth 2023–24: ~6–8%

- Claim severity rise linked to labor costs per Trupanion 2024 reports

- Regional employment monitoring informs pricing and reserves

Currency exchange rate fluctuations

As a multinational insurer with major markets in the US, Canada and parts of Europe, Trupanion faces FX volatility that can sway reported revenues; a 5% USD strength vs CAD would reduce translated Canadian revenue accordingly—Trupanion reported 2024 international premiums comprising about 12% of total revenue.

Management uses forward contracts and selective hedging plus local-currency pricing to stabilize margins and limit FX-driven earnings variability.

- Exposure: US vs CAD/EUR impacts reported revenue

- 2024: ~12% of premiums international

- Mitigation: forwards, hedges, local-currency pricing

Rising vet costs squeeze margins despite rate hikes; Trupanion steadies with data pricing

Rising advanced veterinary costs increased claim severity ~7–9% annually through 2024, pressuring loss ratios despite mid-2024 rate hikes ~8%; US pet medical spend hit $37.2B in 2023. Trupanion’s data-driven pricing improved combined ratio to ~103% in 2023 and net retention ~95% in 2025 YTD, while 2024 investment income (~$92M) benefited from Fed funds at 5.25–5.50%. International premiums ~12% of total; wage growth 6–8%.

| Metric | Value |

|---|---|

| Pet medical spend (2023) | $37.2B |

| Claim severity growth | 7–9% (through 2024) |

| Rate increases (mid‑2024) | ~8% |

| Combined ratio (2023) | ~103% |

| Net retention (2025 YTD) | ~95% |

| Investment income (2024) | ~$92M |

| Fed funds (2024) | 5.25–5.50% |

| Wage growth (2023–24) | 6–8% |

| International premiums (2024) | ~12% |

What You See Is What You Get

Trupanion PESTLE Analysis

The preview shown here is the exact Trupanion PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock how regulatory shifts, pet-owner demographics, and tech-driven claims processing are reshaping Trupanion’s growth and risk profile—our PESTLE distills these forces into strategic insights you can act on. Purchase the full analysis to access detailed implications, scenario planning, and ready-to-use slides for investment decisions or boardroom strategy.

Political factors

Regulatory oversight of insurance rate filings

State insurance departments wield direct control over Trupanion by approving or denying rate filings; in 2024 Trupanion secured roughly 6–8% average annual premium increases in contested states, but approvals vary widely by jurisdiction.

As of late 2025 the political focus on consumer protection demands transparent claims and loss-ratio data—Trupanion reported a 2024 medical loss ratio near 82%, a key metric regulators scrutinize to justify rate hikes.

Regulatory delays compress margins when veterinary cost inflation, which rose about 9% YoY in 2023–24, outpaces permitted premium growth, forcing temporary earnings pressure reflected in quarterly underwriting losses.

International trade and expansion policies

Trupanion, active across North America and expanding into Europe and Asia, faces reliance on stable trade agreements; EU pet insurance regulation alignment and post-Brexit UK rules affect market entry and pricing, with 2025 revenue from international operations targeted at roughly 10-12% of total (Trupanion guidance 2024–2025). Political shifts in foreign investment laws or licensing can add regulatory compliance costs and delay launches, potentially increasing CAC by an estimated 5–15%. Navigating diverse geopolitical risks—sanctions, data-localization, and tariff changes—remains a core executive challenge for scaling profitably.

Governmental healthcare policy shifts

Shifts in human healthcare policy can ripple into veterinary care; for example, US proposals to cap medical fees could inspire analogous state bills affecting vet reimbursement, pushing Trupanion's loss ratios (2024 combined ratio ~84%) if average claim severity rises above its 20% premium growth in 2023–24. Monitoring licensure/regulation trends—14 states considered vet licensure bills in 2024—helps forecast actuarial impacts on pricing and reserves.

Taxation policies and corporate incentives

Changes in corporate tax rates or new financial services levies in the US and Canada can erode Trupanion’s net margin; a 1% effective tax increase on 2025 projected premiums (~$1.1B in gross written premiums 2024) could reduce net income by millions.

Ongoing policy debates on whether pet insurance premiums or employer-provided pet benefits are tax-deductible affect uptake in employer-sponsored channels that drove ~20% of new subscriptions in 2024.

Trupanion must update its state/province-level financial models to reflect differing tax treatments and potential surtaxes, using scenario analyses to stress-test profitability under varying tax regimes.

- 1% tax rise ≈ multimillion-dollar net income hit vs 2024 GWP $1.1B

- Employer channel ~20% of 2024 new subscriptions; tax deductibility shifts demand

- State/province scenario modeling required for accurate pricing and reserve planning

Advocacy for animal welfare legislation

Political momentum for animal welfare drives stricter pet-care laws; 2024 saw 18 US states consider microchipping or anti-cruelty bills, raising owner duties and regulatory compliance costs for clinics.

Mandated microchipping and health checks increase veterinary visits—U.S. vet visits rose 6% in 2023 to 162 million, likely boosting Trupanion claim frequency and premium uptake.

Elevating pets to family status correlates with higher insurance demand; U.S. pet insurance penetration rose to ~4.0% in 2024, benefiting Trupanion’s revenue growth trajectory.

- Stricter laws → more vet care, higher claims

- 2023 vet visits: 162M (+6%) → higher utilization

- 2024 pet insurance penetration ~4.0% → market tailwind for Trupanion

Rate caps vs 9% vet cost inflation squeeze Trupanion margins as MLR hits ~82%

Regulatory rate approvals vary by state—2024 avg contested increases ~6–8%—and regulators scrutinize Trupanion’s 2024 medical loss ratio ~82%, pressuring margins when vet cost inflation (~9% YoY 2023–24) outpaces allowed premiums.

| Metric | 2023–2024 |

|---|---|

| Contested rate approvals | 6–8% |

| Medical loss ratio | ~82% |

| Vet cost inflation | ~9% YoY |

| GWP | $1.1B (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Trupanion across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios tailored to the pet insurance market.

Condensed PESTLE insights for Trupanion, organized by category for quick reference during meetings or presentations and easily dropped into slides or shared across teams.

Economic factors

Impact of veterinary medical inflation

The rise in advanced veterinary procedures has pushed average claim costs up about 7–9% annually through 2024, directly pressuring Trupanion’s loss ratio and prompting mid-2024 rate increases averaging ~8% across plans.

As sophisticated diagnostics and specialty care raise per-claim severity—U.S. pet medical spending reached $37.2B in 2023—Trupanion requires continual actuarial resets to sustain margins.

Trupanion’s data-driven pricing and proprietary claims dataset, which supported a 2023 combined ratio improvement to ~103%, underpin its ability to offset medical inflation and serve as a competitive moat.

Discretionary spending and consumer confidence

Pet insurance is semi-discretionary, so Trupanion is sensitive to disposable income swings; in 2024 US consumer confidence averaged 99.0 and household savings rates fell to ~3.8%, risking slower new enrollments during downturns. Trupanion’s net retention remained strong—2025 YTD policy renewal rates ~95%—indicating existing members prioritize coverage. Economic stability through end-2025 is critical to sustain historical pet enrollment growth (~10–12% annual).

Interest rate environment and investment income

The prevailing interest rate environment materially affects Trupanion’s investment income on float and capital reserves; higher U.S. short-term rates (Fed funds at 5.25–5.50% in 2024) boosted investment yield, helping produce roughly $92 million of investment income in 2024 and buffering operating costs. Elevated yields support the balance sheet and can offset underwriting shortfalls, while a prolonged low-rate scenario would force greater reliance on underwriting margins to sustain profitability.

Labor market dynamics for veterinary professionals

Shortages of veterinarians and technicians have pushed average clinic wage growth to about 6–8% annually in 2023–2024, driving higher treatment prices that are often shifted to pet owners and insurers like Trupanion.

Competition for skilled medical staff across specialty and general practice raises claim costs; Trupanion reported claim severity increases consistent with labor-driven price pressures in its 2024 filings.

The company tracks regional employment metrics and licensure trends to model expected veterinary service cost changes and adjust pricing, reserving, and underwriting assumptions accordingly.

- Wage growth 2023–24: ~6–8%

- Claim severity rise linked to labor costs per Trupanion 2024 reports

- Regional employment monitoring informs pricing and reserves

Currency exchange rate fluctuations

As a multinational insurer with major markets in the US, Canada and parts of Europe, Trupanion faces FX volatility that can sway reported revenues; a 5% USD strength vs CAD would reduce translated Canadian revenue accordingly—Trupanion reported 2024 international premiums comprising about 12% of total revenue.

Management uses forward contracts and selective hedging plus local-currency pricing to stabilize margins and limit FX-driven earnings variability.

- Exposure: US vs CAD/EUR impacts reported revenue

- 2024: ~12% of premiums international

- Mitigation: forwards, hedges, local-currency pricing

Rising vet costs squeeze margins despite rate hikes; Trupanion steadies with data pricing

Rising advanced veterinary costs increased claim severity ~7–9% annually through 2024, pressuring loss ratios despite mid-2024 rate hikes ~8%; US pet medical spend hit $37.2B in 2023. Trupanion’s data-driven pricing improved combined ratio to ~103% in 2023 and net retention ~95% in 2025 YTD, while 2024 investment income (~$92M) benefited from Fed funds at 5.25–5.50%. International premiums ~12% of total; wage growth 6–8%.

| Metric | Value |

|---|---|

| Pet medical spend (2023) | $37.2B |

| Claim severity growth | 7–9% (through 2024) |

| Rate increases (mid‑2024) | ~8% |

| Combined ratio (2023) | ~103% |

| Net retention (2025 YTD) | ~95% |

| Investment income (2024) | ~$92M |

| Fed funds (2024) | 5.25–5.50% |

| Wage growth (2023–24) | 6–8% |

| International premiums (2024) | ~12% |

What You See Is What You Get

Trupanion PESTLE Analysis

The preview shown here is the exact Trupanion PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.