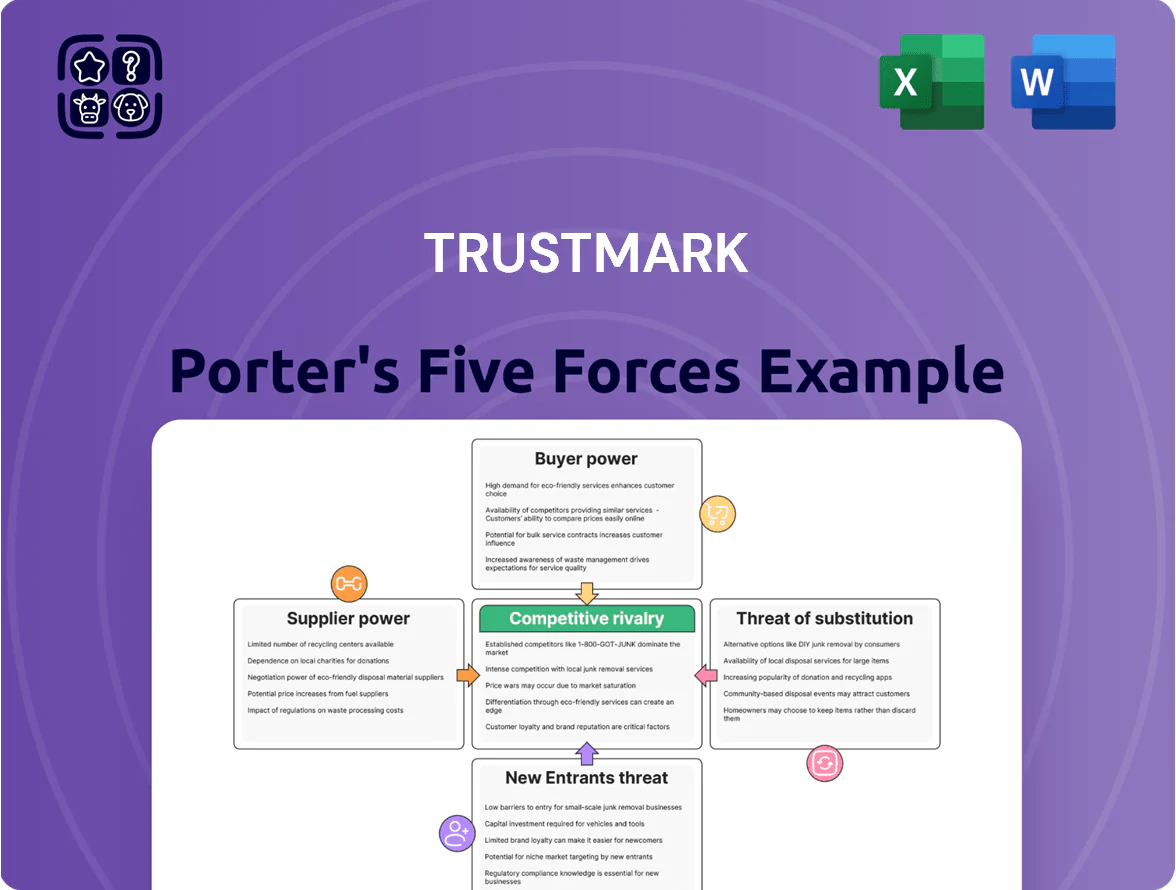

Trustmark Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Trustmark faces moderate buyer power, regulatory-driven supplier constraints, and evolving fintech substitutes that together shape its competitive landscape; this snapshot highlights key pressures but omits force-by-force ratings, visuals, and tactical implications.

Suppliers Bargaining Power

Cost of Core Deposit Funding

Depositors are Trustmark’s main capital suppliers and their bargaining power is high at end-2025 because digital rate transparency lets customers compare yields instantly, forcing Trustmark to match market rates; national average 1-year CD yield rose to 4.2% in 2025 while regional competitors offered 4.0–4.5%, pressuring margins.

Technology and Fintech Vendors

Trustmark depends on third-party providers for core banking, cybersecurity, and digital platforms, raising supplier power because switching costs exceed $10m–$50m per migration and integration timelines often take 12–24 months. Specialized vendors command leverage as AI-driven services reached ~40% adoption in US retail banking by 2025, forcing Trustmark to keep cutting-edge tools to stay competitive and increasing contract concentration risk.

Highly Skilled Financial Talent

The supply of experienced commercial lenders, wealth managers, and cybersecurity experts is a critical input for Trustmark operations, and in 2025 the U.S. market reports a 4.2% shortfall in fintech-related cybersecurity roles and a 6% vacancy rate for senior commercial lenders, giving top-tier talent measurable leverage in pay and benefits.

Regulatory and Compliance Services

Regulatory consultants and legal firms are essential for Trustmark to meet bank licensing and compliance; losing them risks fines or restrictions so their bargaining power is high.

As of December 2025, U.S. bank enforcement actions rose 14% year-over-year, keeping demand—and pricing—strong for specialist compliance services, with average hourly rates for top firms near $600–$900.

- Mandatory services: maintain license

- High switching cost: regulatory risk

- Pricing power: rates ~$600–$900/hr

Liquidity from Capital Markets

Trustmark supplements retail deposits with wholesale funding and capital-market issuance to fund loans; in 2025 Trustmark reported securities borrowing and long-term debt comprising about 12% of liabilities, boosting reliance on institutional lenders.

The bargaining power of these lenders hinges on macro conditions and Trustmark’s credit profile; after its A3/BBB+ ratings in 2024, a one-notch downgrade would raise funding spreads by ~30–60 bps, per historical bank data.

Fed rate moves and market sentiment drive costs: a 100 bp Fed hike in 2022 raised regional banks’ average wholesale funding costs by ~45 bps, so shifts materially affect Trustmark’s margin and loan pricing.

- Wholesale funding ≈12% of liabilities (2025)

- Ratings A3/BBB+ (2024); 1-notch = ~30–60 bps spread impact

- 100 bp Fed hike → ~45 bps wholesale cost rise (regional banks)

Trustmark 2025: Depositors, vendors wield strong leverage—costly vendor exits & tight funding

Depositors and specialist vendors hold high bargaining power for Trustmark in 2025: retail rates averaged 4.2% for 1‑yr CDs vs regional 4.0–4.5%, wholesale funding ≈12% of liabilities, A3/BBB+ ratings (2024) imply 1‑notch = ~30–60 bps spread, vendor migration costs $10m–$50m and 12–24 month timelines, compliance counsel fees $600–$900/hr, talent vacancy ~4–6%.

| Item | 2025 value |

|---|---|

| 1‑yr CD avg | 4.2% |

| Wholesale funding | ≈12% liabilities |

| Ratings (2024) | A3/BBB+ |

| Vendor switch cost | $10m–$50m |

| Compliance rates | $600–$900/hr |

What is included in the product

Tailored Porter's Five Forces assessment for Trustmark that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats—designed for integration into strategy decks, investor materials, or academic work.

Clear, one-sheet Porter's Five Forces tailored for Trustmark—instantly highlights competitive pressures and strategic levers to ease decision-making and boardroom discussion.

Customers Bargaining Power

Low Switching Costs for Retail Users

The rise of digital banking and open finance has cut switching friction: by Q4 2025 account-to-account portability and mobile-first onboarding let retail customers move primary banks in minutes, raising customer bargaining power. Studies show 38% of US consumers used a fintech switch tool in 2024 and churn rates rose ~12% in mobile-first cohorts. Trustmark must double down on superior service and localized branches to retain clients.

Demand for Personalized Wealth Management

Corporate Borrower Leverage

Price Sensitivity in Insurance Products

Trustmark’s insurance customers are highly price-sensitive; 72% of US shoppers used comparison tools for health or life insurance in 2024, pushing rates down and increasing policy shopping frequency.

Online aggregators boost transparency, enabling buyers to demand lower premiums or tailored terms, forcing Trustmark to offer competitive pricing while protecting underwriting margins.

In 2024 Trustmark’s medical loss ratio trends and a 6–8% target margin guided pricing decisions to balance competitiveness and profitability.

- 72% of shoppers used comparison tools (2024)

- Aggregators raise rate transparency

- Must balance competitive premiums vs 6–8% margin

Expectation for Seamless Digital Integration

Customers in 2025 expect advanced digital banking as a basic service; 72% of US consumers prefer banks with seamless omnichannel features, per a 2024 J.D. Power study, so Trustmark risks churn if its app and branch integration lag.

Tech-savvy users will migrate quickly to neobanks and big-tech offerings, giving customers leverage to force faster tech spending and prioritize UX investments in Trustmark’s roadmap.

- 72% of US consumers expect seamless omnichannel (J.D. Power 2024)

- Neobanks grew deposits by ~18% in 2024 — a migration signal

- Customer demand now dictates pace of tech capex and UX upgrades

Customers Surge Power: UX, Personalization & Local Banking Vital to Protect 6–8% Margins

Customers wield high bargaining power: digital switching (38% fintech tool use in 2024) and neobank deposit growth (~18% in 2024) raise churn; HNW clients (72% value personalization) control ~$84T globally; corporates drew $1.2T syndicated loans in 2024, pressuring spreads; insurance shoppers (72% comparison-tool use) force price transparency—Trustmark must invest in UX, personalization, and local relationship banking to protect 6–8% target margins.

| Metric | 2024/2025 |

|---|---|

| Fintech switch use | 38% (2024) |

| Neobank deposit growth | ~18% (2024) |

| HNW assets | $84T (UBS/PwC 2024) |

| Syndicated loans | $1.2T (2024) |

| Comparison-tool shoppers | 72% (2024) |

| Target margin | 6–8% |

What You See Is What You Get

Trustmark Porter's Five Forces Analysis

This preview shows the exact Trustmark Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples; it’s the complete, professionally formatted document ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Trustmark faces moderate buyer power, regulatory-driven supplier constraints, and evolving fintech substitutes that together shape its competitive landscape; this snapshot highlights key pressures but omits force-by-force ratings, visuals, and tactical implications.

Suppliers Bargaining Power

Cost of Core Deposit Funding

Depositors are Trustmark’s main capital suppliers and their bargaining power is high at end-2025 because digital rate transparency lets customers compare yields instantly, forcing Trustmark to match market rates; national average 1-year CD yield rose to 4.2% in 2025 while regional competitors offered 4.0–4.5%, pressuring margins.

Technology and Fintech Vendors

Trustmark depends on third-party providers for core banking, cybersecurity, and digital platforms, raising supplier power because switching costs exceed $10m–$50m per migration and integration timelines often take 12–24 months. Specialized vendors command leverage as AI-driven services reached ~40% adoption in US retail banking by 2025, forcing Trustmark to keep cutting-edge tools to stay competitive and increasing contract concentration risk.

Highly Skilled Financial Talent

The supply of experienced commercial lenders, wealth managers, and cybersecurity experts is a critical input for Trustmark operations, and in 2025 the U.S. market reports a 4.2% shortfall in fintech-related cybersecurity roles and a 6% vacancy rate for senior commercial lenders, giving top-tier talent measurable leverage in pay and benefits.

Regulatory and Compliance Services

Regulatory consultants and legal firms are essential for Trustmark to meet bank licensing and compliance; losing them risks fines or restrictions so their bargaining power is high.

As of December 2025, U.S. bank enforcement actions rose 14% year-over-year, keeping demand—and pricing—strong for specialist compliance services, with average hourly rates for top firms near $600–$900.

- Mandatory services: maintain license

- High switching cost: regulatory risk

- Pricing power: rates ~$600–$900/hr

Liquidity from Capital Markets

Trustmark supplements retail deposits with wholesale funding and capital-market issuance to fund loans; in 2025 Trustmark reported securities borrowing and long-term debt comprising about 12% of liabilities, boosting reliance on institutional lenders.

The bargaining power of these lenders hinges on macro conditions and Trustmark’s credit profile; after its A3/BBB+ ratings in 2024, a one-notch downgrade would raise funding spreads by ~30–60 bps, per historical bank data.

Fed rate moves and market sentiment drive costs: a 100 bp Fed hike in 2022 raised regional banks’ average wholesale funding costs by ~45 bps, so shifts materially affect Trustmark’s margin and loan pricing.

- Wholesale funding ≈12% of liabilities (2025)

- Ratings A3/BBB+ (2024); 1-notch = ~30–60 bps spread impact

- 100 bp Fed hike → ~45 bps wholesale cost rise (regional banks)

Trustmark 2025: Depositors, vendors wield strong leverage—costly vendor exits & tight funding

Depositors and specialist vendors hold high bargaining power for Trustmark in 2025: retail rates averaged 4.2% for 1‑yr CDs vs regional 4.0–4.5%, wholesale funding ≈12% of liabilities, A3/BBB+ ratings (2024) imply 1‑notch = ~30–60 bps spread, vendor migration costs $10m–$50m and 12–24 month timelines, compliance counsel fees $600–$900/hr, talent vacancy ~4–6%.

| Item | 2025 value |

|---|---|

| 1‑yr CD avg | 4.2% |

| Wholesale funding | ≈12% liabilities |

| Ratings (2024) | A3/BBB+ |

| Vendor switch cost | $10m–$50m |

| Compliance rates | $600–$900/hr |

What is included in the product

Tailored Porter's Five Forces assessment for Trustmark that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats—designed for integration into strategy decks, investor materials, or academic work.

Clear, one-sheet Porter's Five Forces tailored for Trustmark—instantly highlights competitive pressures and strategic levers to ease decision-making and boardroom discussion.

Customers Bargaining Power

Low Switching Costs for Retail Users

The rise of digital banking and open finance has cut switching friction: by Q4 2025 account-to-account portability and mobile-first onboarding let retail customers move primary banks in minutes, raising customer bargaining power. Studies show 38% of US consumers used a fintech switch tool in 2024 and churn rates rose ~12% in mobile-first cohorts. Trustmark must double down on superior service and localized branches to retain clients.

Demand for Personalized Wealth Management

Corporate Borrower Leverage

Price Sensitivity in Insurance Products

Trustmark’s insurance customers are highly price-sensitive; 72% of US shoppers used comparison tools for health or life insurance in 2024, pushing rates down and increasing policy shopping frequency.

Online aggregators boost transparency, enabling buyers to demand lower premiums or tailored terms, forcing Trustmark to offer competitive pricing while protecting underwriting margins.

In 2024 Trustmark’s medical loss ratio trends and a 6–8% target margin guided pricing decisions to balance competitiveness and profitability.

- 72% of shoppers used comparison tools (2024)

- Aggregators raise rate transparency

- Must balance competitive premiums vs 6–8% margin

Expectation for Seamless Digital Integration

Customers in 2025 expect advanced digital banking as a basic service; 72% of US consumers prefer banks with seamless omnichannel features, per a 2024 J.D. Power study, so Trustmark risks churn if its app and branch integration lag.

Tech-savvy users will migrate quickly to neobanks and big-tech offerings, giving customers leverage to force faster tech spending and prioritize UX investments in Trustmark’s roadmap.

- 72% of US consumers expect seamless omnichannel (J.D. Power 2024)

- Neobanks grew deposits by ~18% in 2024 — a migration signal

- Customer demand now dictates pace of tech capex and UX upgrades

Customers Surge Power: UX, Personalization & Local Banking Vital to Protect 6–8% Margins

Customers wield high bargaining power: digital switching (38% fintech tool use in 2024) and neobank deposit growth (~18% in 2024) raise churn; HNW clients (72% value personalization) control ~$84T globally; corporates drew $1.2T syndicated loans in 2024, pressuring spreads; insurance shoppers (72% comparison-tool use) force price transparency—Trustmark must invest in UX, personalization, and local relationship banking to protect 6–8% target margins.

| Metric | 2024/2025 |

|---|---|

| Fintech switch use | 38% (2024) |

| Neobank deposit growth | ~18% (2024) |

| HNW assets | $84T (UBS/PwC 2024) |

| Syndicated loans | $1.2T (2024) |

| Comparison-tool shoppers | 72% (2024) |

| Target margin | 6–8% |

What You See Is What You Get

Trustmark Porter's Five Forces Analysis

This preview shows the exact Trustmark Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples; it’s the complete, professionally formatted document ready for immediate download and use.