Trustmark PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

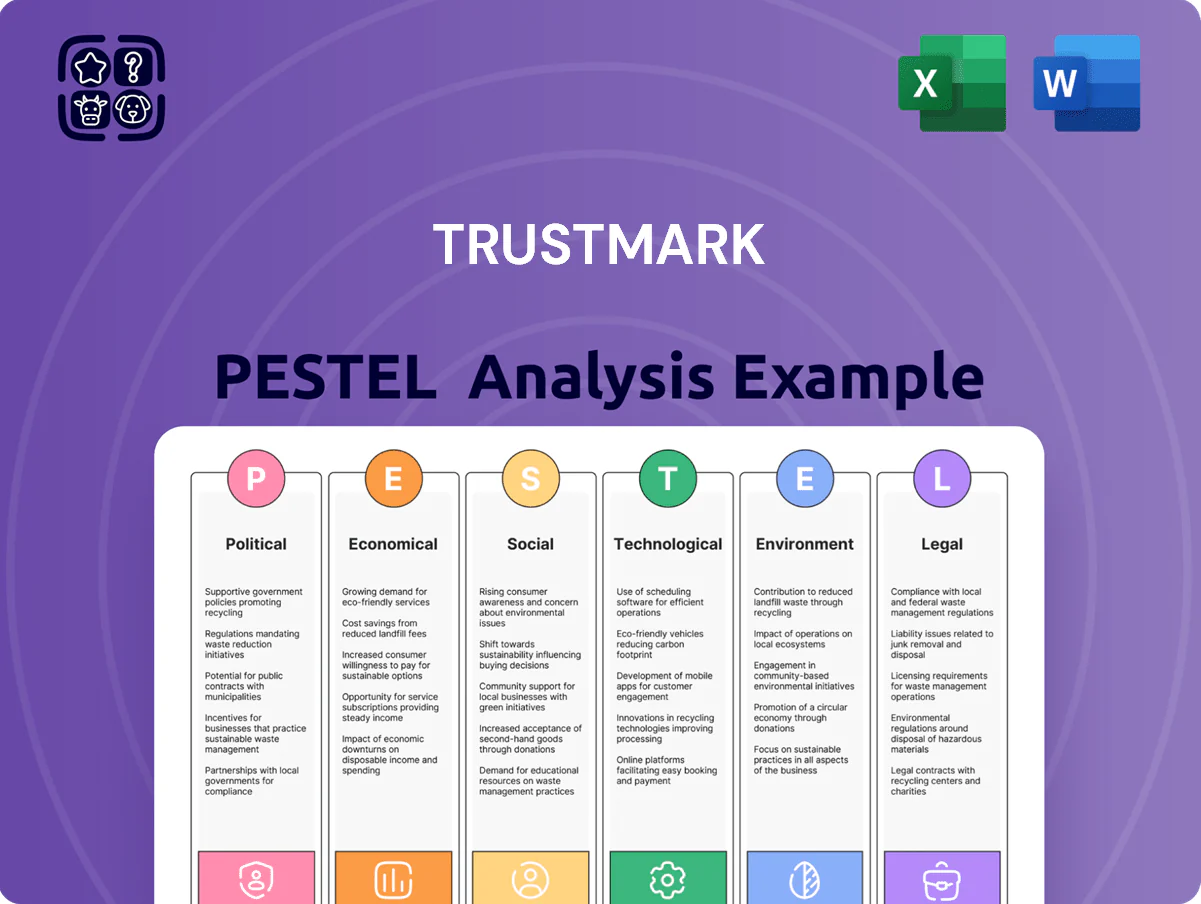

Unlock strategic foresight with our PESTLE Analysis of Trustmark—concise, expert-driven insights into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors, advisors, and planners, this ready-to-use report saves time and sharpens decision-making. Purchase the full analysis now to access the complete, editable breakdown and actionable recommendations.

Political factors

Post-Election Regulatory Trajectory

By end-2025 the US political landscape post-2024 has set regulatory tone: a pro-growth administration may push deregulation lowering compliance costs by an estimated 5–10% for regional banks, while a stability-focused regime could raise CET1 ratio expectations by 50–150 bps; Trustmark must adapt to potential shifts in FDIC/FRB oversight and stress-test frequency.

Southeastern Regional Political Stability

As a major regional bank, Trustmark is exposed to political climates in MS, AL, TN, TX, and FL where 2024 GDP growth ranged from 1.8% (MS) to 3.1% (TX), affecting loan demand and risk profiles.

State economic development incentives and 2024 business tax changes—e.g., TX and FL corporate-friendly policies—facilitate expansion of Trustmark’s commercial loan book, which grew 6.2% YoY in 2024.

Consistent political stability across these states supported a 2024 small-business lending uptick and encourages long-term corporate investment, benefiting Trustmark’s net interest income and credit quality.

Government-Backed Lending Programs

The continued availability and structure of government-sponsored programs, notably SBA lending, remain vital to Trustmark’s lending strategy, with SBA-backed loans accounting for an estimated 8–10% of small business originations industry-wide in 2024.

Political decisions on funding and program scope—Congress allotted roughly $1.5 billion to SBA disaster and small business programs in FY2024—directly affect Trustmark’s capacity to finance local entrepreneurs.

Trustmark monitors proposed legislative changes and regulatory guidance closely to maximize program utility for its diverse client base, aligning origination pipelines to shifts in eligibility and guarantee levels.

Geopolitical Influence on Monetary Policy

By late 2025, elevated global political tensions have pushed oil prices to roughly $90–$100/barrel and disrupted key supply chains, prompting the Federal Reserve to keep the federal funds rate near 5.25%–5.50% to tame inflation—directly affecting Trustmark’s funding costs and deposit pricing.

As a regional bank, Trustmark’s net interest margin and the competitiveness of its wealth-management yields are influenced by Fed policy shifts driven by geopolitical shocks and investor risk aversion.

- Oil: $90–$100/barrel (late 2025)

- Fed funds rate: ~5.25%–5.50% (late 2025)

- Impact: higher cost of funds, pressure on NIM, demand for higher-yield wealth products

Infrastructure and Community Investment Acts

Federal and state pushes for infrastructure renewal—backed by the 2021 Bipartisan Infrastructure Law ($550B new spending) and $120B in recent Southern state allocations for transportation/tech hubs—create public-private partnership opportunities for Trustmark to finance projects and provide advisory services.

These initiatives increase demand for commercial lending and ABL; Trustmark can target municipal bonds, construction loans, and treasury services to capture a share of projected multi-billion-dollar regional pipelines.

- 2021 federal law: $550B new infrastructure spending

- Southern state allocations ~ $120B for transport/tech (recent packages)

- Opportunities: municipal bonds, construction lending, advisory, treasury services

Trustmark Faces Margin Pressure, Regulatory CET1 Shock, and Mixed Regional Growth

Political shifts post-2024 affect Trustmark via regulatory stance (possible 50–150 bps CET1 change), regional GDP variance (2024: MS 1.8%, AL 2.0%, TN 2.6%, TX 3.1%, FL 2.9%), SBA funding (~$1.5B FY2024) and infrastructure allocations (~$120B regional); Fed rates ~5.25–5.50% (late-2025) raise funding costs and compress NIM.

| Factor | 2024/2025 Data |

|---|---|

| Regional GDP | MS 1.8%, AL 2.0%, TN 2.6%, TX 3.1%, FL 2.9% |

| Regulatory impact | +50–150 bps CET1 (stress) |

| SBA funding | $1.5B FY2024 |

| Fed funds | 5.25–5.50% (late-2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Trustmark across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed sub-points and examples specific to the business.

Condenses Trustmark's PESTLE insights into a clean, easily sharable summary that teams can drop into presentations or planning sessions to align quickly on external risks and strategic priorities.

Economic factors

Interest Rate Environment Stabilization

Regional Economic Growth Trends

The Sunbelt's economic strength—Texas and Florida GDP growth of 3.5% and 2.9% in 2024 respectively—drives Trustmark's organic expansion through rising deposits and loan demand as corporate relocations and net migration boost retail and commercial volumes.

Trustmark's regional branches leverage local market expertise to capture higher average deposit balances and commercial loan originations while hedging concentration risk via diversified product mix and stress-tested capital buffers.

Inflation and Consumer Spending Power

Persistent inflation around 3.5–4.0% in 2024–25 reduces real incomes for Trustmark’s retail customers, constraining borrowing capacity and lowering discretionary spending. Rising food and energy prices have pushed household debt-service ratios higher, shifting demand from personal and auto loans toward debt consolidation and lower-risk credit products. Trustmark adjusts credit underwriting—tightening LTV and DTI thresholds—and targets marketing to promote savings, insurance, and consolidation offerings based on CPI and consumer credit trends.

Real Estate Market Dynamics

Real estate market health across the Southeast—where Trustmark concentrates—directly shapes mortgage and construction lending; Q4 2025 metro home prices in the Sun Belt rose ~3.5% YoY while office vacancy in major Southern metros averaged ~18%, affecting collateral values and demand.

Trustmark’s portfolio sensitivity is managed via rigorous stress tests modeling 20–30% price corrections and higher vacancy scenarios to preserve CET1 and loss reserves.

- SE home price change Q4 2025: +3.5% YoY

- Major Southern office vacancy: ~18%

- Stress-test shock scenarios: 20–30% price decline

Labor Market and Wage Inflation

Tight labor markets in financial services through late 2025 push Trustmark to offer competitive pay; US job openings in finance remained elevated at ~4.2 million in Q3 2025, raising retention costs.

Rising wages increase personnel expenses—Trustmark must balance higher salary spend with automation investments; industry automation adoption projected to cut back-office costs by 15% by 2026.

Regional labor health affects client credit performance: Mississippi and Tennessee unemployment rates near 3.8%–4.2% in 2025, supporting loan servicing but leaving vulnerability to shocks.

- Competitive pay needed amid ~4.2M finance job openings (Q3 2025)

- Automation could reduce back-office costs ~15% by 2026

- Regional unemployment ~3.8%–4.2% supports but risks loan performance

Fed rates tighten NIM; Sunbelt growth and housing aid loans as CRE risks rise

Higher Fed rates (~5.25%–5.50% by end-2025) compress Trustmark NIM (~3.10% FY2024) while Sunbelt GDP (TX 3.5%, FL 2.9% in 2024) and Q4 2025 SE home prices +3.5% YoY support deposit and loan growth; office vacancy ~18% raises CRE risk; regional unemployment ~3.8%–4.2% aids credit but wage inflation and ~4.2M finance job openings push personnel costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25%–5.50% |

| NIM FY2024 | ~3.10% |

| SE home prices Q4 2025 | +3.5% YoY |

| Office vacancy | ~18% |

| Regional unemployment | 3.8%–4.2% |

Full Version Awaits

Trustmark PESTLE Analysis

The preview shown here is the exact Trustmark PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our PESTLE Analysis of Trustmark—concise, expert-driven insights into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors, advisors, and planners, this ready-to-use report saves time and sharpens decision-making. Purchase the full analysis now to access the complete, editable breakdown and actionable recommendations.

Political factors

Post-Election Regulatory Trajectory

By end-2025 the US political landscape post-2024 has set regulatory tone: a pro-growth administration may push deregulation lowering compliance costs by an estimated 5–10% for regional banks, while a stability-focused regime could raise CET1 ratio expectations by 50–150 bps; Trustmark must adapt to potential shifts in FDIC/FRB oversight and stress-test frequency.

Southeastern Regional Political Stability

As a major regional bank, Trustmark is exposed to political climates in MS, AL, TN, TX, and FL where 2024 GDP growth ranged from 1.8% (MS) to 3.1% (TX), affecting loan demand and risk profiles.

State economic development incentives and 2024 business tax changes—e.g., TX and FL corporate-friendly policies—facilitate expansion of Trustmark’s commercial loan book, which grew 6.2% YoY in 2024.

Consistent political stability across these states supported a 2024 small-business lending uptick and encourages long-term corporate investment, benefiting Trustmark’s net interest income and credit quality.

Government-Backed Lending Programs

The continued availability and structure of government-sponsored programs, notably SBA lending, remain vital to Trustmark’s lending strategy, with SBA-backed loans accounting for an estimated 8–10% of small business originations industry-wide in 2024.

Political decisions on funding and program scope—Congress allotted roughly $1.5 billion to SBA disaster and small business programs in FY2024—directly affect Trustmark’s capacity to finance local entrepreneurs.

Trustmark monitors proposed legislative changes and regulatory guidance closely to maximize program utility for its diverse client base, aligning origination pipelines to shifts in eligibility and guarantee levels.

Geopolitical Influence on Monetary Policy

By late 2025, elevated global political tensions have pushed oil prices to roughly $90–$100/barrel and disrupted key supply chains, prompting the Federal Reserve to keep the federal funds rate near 5.25%–5.50% to tame inflation—directly affecting Trustmark’s funding costs and deposit pricing.

As a regional bank, Trustmark’s net interest margin and the competitiveness of its wealth-management yields are influenced by Fed policy shifts driven by geopolitical shocks and investor risk aversion.

- Oil: $90–$100/barrel (late 2025)

- Fed funds rate: ~5.25%–5.50% (late 2025)

- Impact: higher cost of funds, pressure on NIM, demand for higher-yield wealth products

Infrastructure and Community Investment Acts

Federal and state pushes for infrastructure renewal—backed by the 2021 Bipartisan Infrastructure Law ($550B new spending) and $120B in recent Southern state allocations for transportation/tech hubs—create public-private partnership opportunities for Trustmark to finance projects and provide advisory services.

These initiatives increase demand for commercial lending and ABL; Trustmark can target municipal bonds, construction loans, and treasury services to capture a share of projected multi-billion-dollar regional pipelines.

- 2021 federal law: $550B new infrastructure spending

- Southern state allocations ~ $120B for transport/tech (recent packages)

- Opportunities: municipal bonds, construction lending, advisory, treasury services

Trustmark Faces Margin Pressure, Regulatory CET1 Shock, and Mixed Regional Growth

Political shifts post-2024 affect Trustmark via regulatory stance (possible 50–150 bps CET1 change), regional GDP variance (2024: MS 1.8%, AL 2.0%, TN 2.6%, TX 3.1%, FL 2.9%), SBA funding (~$1.5B FY2024) and infrastructure allocations (~$120B regional); Fed rates ~5.25–5.50% (late-2025) raise funding costs and compress NIM.

| Factor | 2024/2025 Data |

|---|---|

| Regional GDP | MS 1.8%, AL 2.0%, TN 2.6%, TX 3.1%, FL 2.9% |

| Regulatory impact | +50–150 bps CET1 (stress) |

| SBA funding | $1.5B FY2024 |

| Fed funds | 5.25–5.50% (late-2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Trustmark across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed sub-points and examples specific to the business.

Condenses Trustmark's PESTLE insights into a clean, easily sharable summary that teams can drop into presentations or planning sessions to align quickly on external risks and strategic priorities.

Economic factors

Interest Rate Environment Stabilization

Regional Economic Growth Trends

The Sunbelt's economic strength—Texas and Florida GDP growth of 3.5% and 2.9% in 2024 respectively—drives Trustmark's organic expansion through rising deposits and loan demand as corporate relocations and net migration boost retail and commercial volumes.

Trustmark's regional branches leverage local market expertise to capture higher average deposit balances and commercial loan originations while hedging concentration risk via diversified product mix and stress-tested capital buffers.

Inflation and Consumer Spending Power

Persistent inflation around 3.5–4.0% in 2024–25 reduces real incomes for Trustmark’s retail customers, constraining borrowing capacity and lowering discretionary spending. Rising food and energy prices have pushed household debt-service ratios higher, shifting demand from personal and auto loans toward debt consolidation and lower-risk credit products. Trustmark adjusts credit underwriting—tightening LTV and DTI thresholds—and targets marketing to promote savings, insurance, and consolidation offerings based on CPI and consumer credit trends.

Real Estate Market Dynamics

Real estate market health across the Southeast—where Trustmark concentrates—directly shapes mortgage and construction lending; Q4 2025 metro home prices in the Sun Belt rose ~3.5% YoY while office vacancy in major Southern metros averaged ~18%, affecting collateral values and demand.

Trustmark’s portfolio sensitivity is managed via rigorous stress tests modeling 20–30% price corrections and higher vacancy scenarios to preserve CET1 and loss reserves.

- SE home price change Q4 2025: +3.5% YoY

- Major Southern office vacancy: ~18%

- Stress-test shock scenarios: 20–30% price decline

Labor Market and Wage Inflation

Tight labor markets in financial services through late 2025 push Trustmark to offer competitive pay; US job openings in finance remained elevated at ~4.2 million in Q3 2025, raising retention costs.

Rising wages increase personnel expenses—Trustmark must balance higher salary spend with automation investments; industry automation adoption projected to cut back-office costs by 15% by 2026.

Regional labor health affects client credit performance: Mississippi and Tennessee unemployment rates near 3.8%–4.2% in 2025, supporting loan servicing but leaving vulnerability to shocks.

- Competitive pay needed amid ~4.2M finance job openings (Q3 2025)

- Automation could reduce back-office costs ~15% by 2026

- Regional unemployment ~3.8%–4.2% supports but risks loan performance

Fed rates tighten NIM; Sunbelt growth and housing aid loans as CRE risks rise

Higher Fed rates (~5.25%–5.50% by end-2025) compress Trustmark NIM (~3.10% FY2024) while Sunbelt GDP (TX 3.5%, FL 2.9% in 2024) and Q4 2025 SE home prices +3.5% YoY support deposit and loan growth; office vacancy ~18% raises CRE risk; regional unemployment ~3.8%–4.2% aids credit but wage inflation and ~4.2M finance job openings push personnel costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25%–5.50% |

| NIM FY2024 | ~3.10% |

| SE home prices Q4 2025 | +3.5% YoY |

| Office vacancy | ~18% |

| Regional unemployment | 3.8%–4.2% |

Full Version Awaits

Trustmark PESTLE Analysis

The preview shown here is the exact Trustmark PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll download immediately after payment.