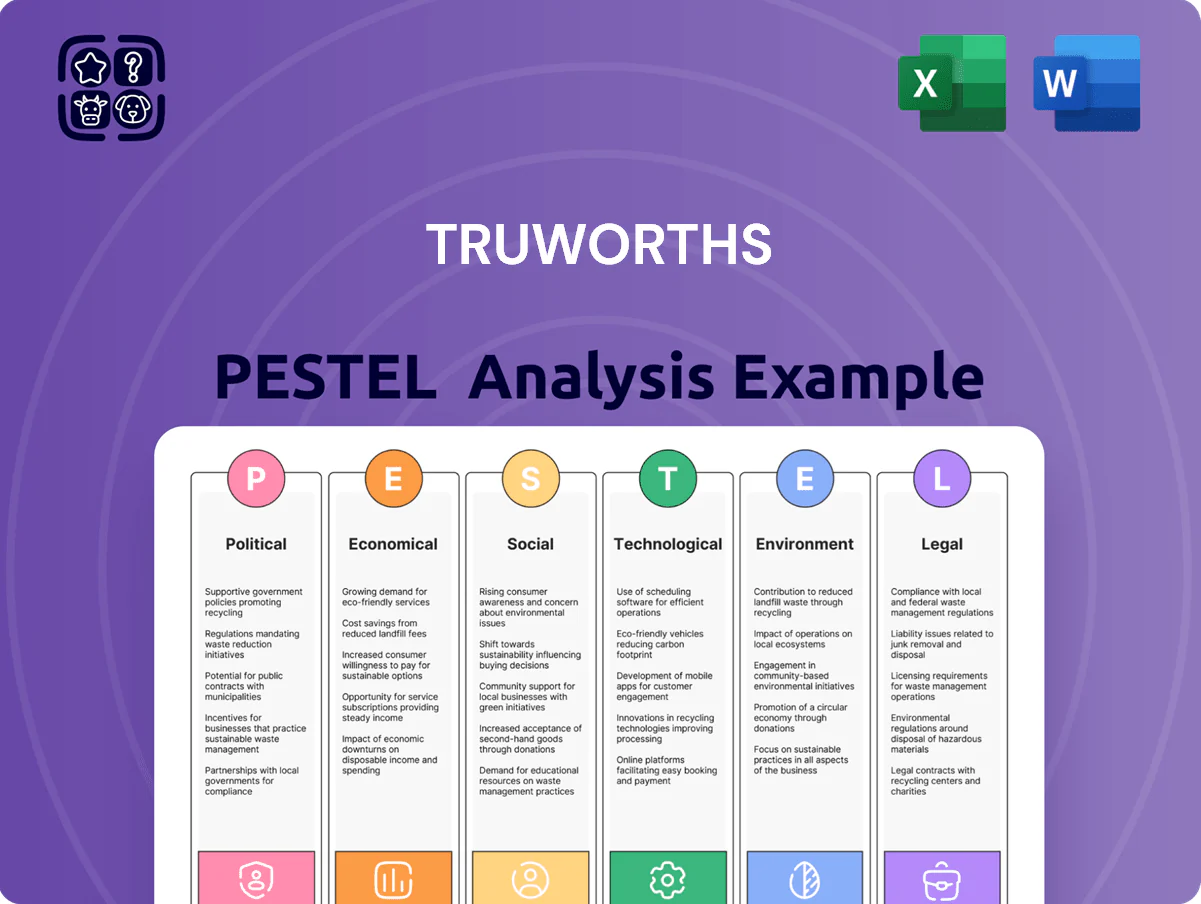

Truworths PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Truworths faces shifting consumer sentiment, tightening regulations, and digital disruption that together reshape its retail edge—our PESTLE snapshot highlights these forces and what they mean for strategy and risk.

Political factors

South African Policy Stability

The Government of National Unity formed in late 2024 has improved policy stability into 2025, reducing immediate risk of radical regulatory shifts for retailers such as Truworths; South Africa’s 2025 CPI is projected near 4.8% and GDP growth forecasts sit around 1.6–2.0%, supporting consumer demand.

UK Trade Relations Post-Brexit

Through ownership of Office, Truworths remains exposed to the evolving UK regulatory and trade environment; UK goods trade with the EU fell 13% in 2023 vs 2019 levels, raising customs frictions that affect footwear imports and average landed costs. New UK-EU trade rules and VAT checks have added border delays—UK imports from EU in 2024 showed a 6% rise in administrative costs for retailers. For Truworths International, these shifts directly pressure margins on Office, which accounted for roughly 18% of group revenue in FY2024. Navigating tariffs, rules of origin and logistics is essential to protect profitability.

Logistics and State-Owned Enterprises

Political pressure to reform Transnet and boost port efficiency is pivotal for Truworths; Transnet recorded a 5% throughput shortfall in 2024 causing average ship waiting times to rise 12%, amplifying import delays for seasonal fashion lines.

Import delays have driven stockouts during peak months—retailers reported SKU availability drops up to 8% in 2024—directly impacting Truworths’ sales timing and margin realization.

Continued government intervention in logistics infrastructure, including a ZAR 100 billion transport investment plan announced in 2024, remains a primary determinant of Truworths’ operational fluidity and inventory lead times.

Regional Geopolitical Volatility

Truworths faces regional geopolitical volatility across African markets where unrest has caused sudden currency devaluations (e.g., ZAR swings of ±8% vs USD in 2023) and episodic store closures; such events can compress margins and raise working capital needs. Monitoring neighboring political climates is essential to manage cross-border supply chain and cash repatriation risks. Expansion is often repriced—projects delayed or scaled back—based on country risk ratings and governance metrics.

- 2023 ZAR volatility ±8% vs USD

- Store closures correlate with spikes in political unrest incidents

- Expansion adjusted by country-risk scores and governance indices

Labor Union Dynamics

The political influence of labor unions in South Africa drives wage negotiations in retail/textiles; COSATU-linked actions and a 2024 wage bill debate pressured employers as minimum wage proposals targeted a national minimum around ZAR 28–32/hour for vulnerable sectors.

Truworths must manage union relations to prevent strikes in stores, head office and distribution centers; 2023 retail sector strike disruptions affected revenues—retail sales grew 3.9% y/y in 2024 but store closures risk margin erosion.

Legislative shifts on worker rights (e.g., expanded bargaining council scope) are influenced by state-union talks, so Truworths monitors policy changes to model labor cost sensitivity in budgets.

- Union bargaining power: high—potential wage uplift ZAR 10–20k/month across workforce segments

- Operational risk: strikes at DCs/stores can cut weekly sales by mid-single digits

- Regulatory watch: proposed minimums and bargaining council rulings to increase labor cost base

SA political stability eases risk; inflation 4.8% but logistics, ZAR volatility, wage strikes bite

Political stability since the 2024 Government of National Unity has lowered regulatory risk; SA 2025 CPI ~4.8% and GDP growth 1.6–2.0% support demand. Transnet throughput shortfall 5% (2024) and ZAR ±8% volatility (2023) raise import delays and working capital needs; Office (18% FY2024 revenue) faces 6% higher admin import costs (2024). Union wage pressure targets ZAR 28–32/hr; strikes can cut weekly sales by mid-single digits.

| Indicator | Value |

|---|---|

| SA CPI 2025 | 4.8% |

| SA GDP growth 2025 | 1.6–2.0% |

| Transnet shortfall 2024 | −5% |

| ZAR volatility 2023 | ±8% vs USD |

| Office revenue share FY2024 | 18% |

| UK admin import cost rise 2024 | +6% |

| Proposed min wage 2024 | ZAR 28–32/hr |

What is included in the product

Explores how external macro-environmental factors uniquely affect Truworths across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section grounded in current market data and regional industry trends to reveal risks and opportunities.

Summarized PESTLE insights for Truworths, formatted for quick reference in meetings or presentations to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Trajectory

As a major provider of consumer credit, Truworths is highly exposed to SARB rate moves in 2025; the repo rate stood at 8.25% in Dec 2024 and markets pencilled limited cuts into 2025, affecting affordability for cardholders. Lower rates typically boost disposable income and lower store-account servicing costs, supporting sales—Truworths reported 2024 credit sales contributing ~40% of group turnover. A sustained high-rate environment increases pressure on the credit book and raised South African household debt-service ratios (around 8.6% in 2024), heightening bad-debt risk.

Consumer Credit Health

The financial health of South Africa's middle class directly affects Truworths' interest-bearing account business; with household debt-to-disposable-income at about 64% in 2024 and unemployment around 32.9% (Q4 2024), higher delinquency risk pressures provisions for doubtful debts. Truworths reported impairments of R1.2bn in FY2024, highlighting the need to balance credit growth against maintaining a high-quality, low-risk debtor book.

Currency Exchange Rate Fluctuations

The South African Rand weakened ~8% vs the US Dollar in 2023 and traded around 18–19 ZAR/USD in 2024, raising imported merchandise costs for Truworths and squeezing gross margins if costs are absorbed.

A ~5% decline vs the British Pound in 2024 similarly increased cost of UK-sourced inventory, forcing potential price rises for consumers.

Active FX hedging is vital: Truworths reported using forward contracts and options in 2023–24 to stabilize margins amid exchange rate volatility.

Inflationary Pressures on Costs

Rising electricity, fuel and wage costs increased Truworths Group operating expenses, with South African CPI averaging 5.8% in 2024 and retail electricity tariffs up ~15% y/y; transport fuel rises pushed logistics costs higher across its ~800-store network.

Persistent inflation eroded purchasing power, reducing discretionary spend and shifting customers to essentials, evidenced by lower apparel volume growth in 2024 and elevated credit default rates in the retail sector.

Truworths mitigated impacts by optimizing supply chain operations, increasing inventory turnover, and expanding value-led ranges and promotions to protect sales and margin.

- SA CPI 2024: 5.8%

- Electricity tariffs ~15% y/y (2024)

- Store network: ~800 outlets

- Strategy: supply-chain efficiency, value-driven SKU mix

UK Economic Performance

UK GDP grew 0.5% q/q in Q4 2025, aiding Office footwear sales as consumer confidence rose; retail sales were up 2.0% y/y in 2025, cushioning Truworths against South African currency and demand volatility.

Higher UK spending hedges SA risks but links performance to UK cycles—unemployment 4.2% (2025) and inflation 3.8% affect margins and pricing for the Office brand.

- UK GDP Q4 2025 +0.5% q/q

- Retail sales +2.0% y/y 2025

- Unemployment 4.2% 2025, inflation 3.8% 2025

Truworths faces SA credit pressure, FX-driven cost rise; UK retail offers partial relief

High SA interest rates (repo 8.25% Dec 2024) and household debt (64% DTI, debt-service ~8.6%) heighten Truworths credit risk; FY2024 impairments R1.2bn. FX weakness (ZAR ~18–19/USD 2024; GBP up ~5% 2024) raises import costs; CPI 5.8% and electricity +15% (2024) push Opex. UK retail resilience (GDP Q4 2025 +0.5% q/q; retail sales +2.0% 2025) partially offsets SA weakness.

| Metric | Value |

|---|---|

| Repo rate Dec 2024 | 8.25% |

| Household DTI 2024 | 64% |

| Impairments FY2024 | R1.2bn |

| ZAR/USD 2024 | 18–19 |

| CPI 2024 | 5.8% |

| UK GDP Q4 2025 | +0.5% q/q |

Same Document Delivered

Truworths PESTLE Analysis

The preview shown here is the exact Truworths PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Truworths faces shifting consumer sentiment, tightening regulations, and digital disruption that together reshape its retail edge—our PESTLE snapshot highlights these forces and what they mean for strategy and risk.

Political factors

South African Policy Stability

The Government of National Unity formed in late 2024 has improved policy stability into 2025, reducing immediate risk of radical regulatory shifts for retailers such as Truworths; South Africa’s 2025 CPI is projected near 4.8% and GDP growth forecasts sit around 1.6–2.0%, supporting consumer demand.

UK Trade Relations Post-Brexit

Through ownership of Office, Truworths remains exposed to the evolving UK regulatory and trade environment; UK goods trade with the EU fell 13% in 2023 vs 2019 levels, raising customs frictions that affect footwear imports and average landed costs. New UK-EU trade rules and VAT checks have added border delays—UK imports from EU in 2024 showed a 6% rise in administrative costs for retailers. For Truworths International, these shifts directly pressure margins on Office, which accounted for roughly 18% of group revenue in FY2024. Navigating tariffs, rules of origin and logistics is essential to protect profitability.

Logistics and State-Owned Enterprises

Political pressure to reform Transnet and boost port efficiency is pivotal for Truworths; Transnet recorded a 5% throughput shortfall in 2024 causing average ship waiting times to rise 12%, amplifying import delays for seasonal fashion lines.

Import delays have driven stockouts during peak months—retailers reported SKU availability drops up to 8% in 2024—directly impacting Truworths’ sales timing and margin realization.

Continued government intervention in logistics infrastructure, including a ZAR 100 billion transport investment plan announced in 2024, remains a primary determinant of Truworths’ operational fluidity and inventory lead times.

Regional Geopolitical Volatility

Truworths faces regional geopolitical volatility across African markets where unrest has caused sudden currency devaluations (e.g., ZAR swings of ±8% vs USD in 2023) and episodic store closures; such events can compress margins and raise working capital needs. Monitoring neighboring political climates is essential to manage cross-border supply chain and cash repatriation risks. Expansion is often repriced—projects delayed or scaled back—based on country risk ratings and governance metrics.

- 2023 ZAR volatility ±8% vs USD

- Store closures correlate with spikes in political unrest incidents

- Expansion adjusted by country-risk scores and governance indices

Labor Union Dynamics

The political influence of labor unions in South Africa drives wage negotiations in retail/textiles; COSATU-linked actions and a 2024 wage bill debate pressured employers as minimum wage proposals targeted a national minimum around ZAR 28–32/hour for vulnerable sectors.

Truworths must manage union relations to prevent strikes in stores, head office and distribution centers; 2023 retail sector strike disruptions affected revenues—retail sales grew 3.9% y/y in 2024 but store closures risk margin erosion.

Legislative shifts on worker rights (e.g., expanded bargaining council scope) are influenced by state-union talks, so Truworths monitors policy changes to model labor cost sensitivity in budgets.

- Union bargaining power: high—potential wage uplift ZAR 10–20k/month across workforce segments

- Operational risk: strikes at DCs/stores can cut weekly sales by mid-single digits

- Regulatory watch: proposed minimums and bargaining council rulings to increase labor cost base

SA political stability eases risk; inflation 4.8% but logistics, ZAR volatility, wage strikes bite

Political stability since the 2024 Government of National Unity has lowered regulatory risk; SA 2025 CPI ~4.8% and GDP growth 1.6–2.0% support demand. Transnet throughput shortfall 5% (2024) and ZAR ±8% volatility (2023) raise import delays and working capital needs; Office (18% FY2024 revenue) faces 6% higher admin import costs (2024). Union wage pressure targets ZAR 28–32/hr; strikes can cut weekly sales by mid-single digits.

| Indicator | Value |

|---|---|

| SA CPI 2025 | 4.8% |

| SA GDP growth 2025 | 1.6–2.0% |

| Transnet shortfall 2024 | −5% |

| ZAR volatility 2023 | ±8% vs USD |

| Office revenue share FY2024 | 18% |

| UK admin import cost rise 2024 | +6% |

| Proposed min wage 2024 | ZAR 28–32/hr |

What is included in the product

Explores how external macro-environmental factors uniquely affect Truworths across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section grounded in current market data and regional industry trends to reveal risks and opportunities.

Summarized PESTLE insights for Truworths, formatted for quick reference in meetings or presentations to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Trajectory

As a major provider of consumer credit, Truworths is highly exposed to SARB rate moves in 2025; the repo rate stood at 8.25% in Dec 2024 and markets pencilled limited cuts into 2025, affecting affordability for cardholders. Lower rates typically boost disposable income and lower store-account servicing costs, supporting sales—Truworths reported 2024 credit sales contributing ~40% of group turnover. A sustained high-rate environment increases pressure on the credit book and raised South African household debt-service ratios (around 8.6% in 2024), heightening bad-debt risk.

Consumer Credit Health

The financial health of South Africa's middle class directly affects Truworths' interest-bearing account business; with household debt-to-disposable-income at about 64% in 2024 and unemployment around 32.9% (Q4 2024), higher delinquency risk pressures provisions for doubtful debts. Truworths reported impairments of R1.2bn in FY2024, highlighting the need to balance credit growth against maintaining a high-quality, low-risk debtor book.

Currency Exchange Rate Fluctuations

The South African Rand weakened ~8% vs the US Dollar in 2023 and traded around 18–19 ZAR/USD in 2024, raising imported merchandise costs for Truworths and squeezing gross margins if costs are absorbed.

A ~5% decline vs the British Pound in 2024 similarly increased cost of UK-sourced inventory, forcing potential price rises for consumers.

Active FX hedging is vital: Truworths reported using forward contracts and options in 2023–24 to stabilize margins amid exchange rate volatility.

Inflationary Pressures on Costs

Rising electricity, fuel and wage costs increased Truworths Group operating expenses, with South African CPI averaging 5.8% in 2024 and retail electricity tariffs up ~15% y/y; transport fuel rises pushed logistics costs higher across its ~800-store network.

Persistent inflation eroded purchasing power, reducing discretionary spend and shifting customers to essentials, evidenced by lower apparel volume growth in 2024 and elevated credit default rates in the retail sector.

Truworths mitigated impacts by optimizing supply chain operations, increasing inventory turnover, and expanding value-led ranges and promotions to protect sales and margin.

- SA CPI 2024: 5.8%

- Electricity tariffs ~15% y/y (2024)

- Store network: ~800 outlets

- Strategy: supply-chain efficiency, value-driven SKU mix

UK Economic Performance

UK GDP grew 0.5% q/q in Q4 2025, aiding Office footwear sales as consumer confidence rose; retail sales were up 2.0% y/y in 2025, cushioning Truworths against South African currency and demand volatility.

Higher UK spending hedges SA risks but links performance to UK cycles—unemployment 4.2% (2025) and inflation 3.8% affect margins and pricing for the Office brand.

- UK GDP Q4 2025 +0.5% q/q

- Retail sales +2.0% y/y 2025

- Unemployment 4.2% 2025, inflation 3.8% 2025

Truworths faces SA credit pressure, FX-driven cost rise; UK retail offers partial relief

High SA interest rates (repo 8.25% Dec 2024) and household debt (64% DTI, debt-service ~8.6%) heighten Truworths credit risk; FY2024 impairments R1.2bn. FX weakness (ZAR ~18–19/USD 2024; GBP up ~5% 2024) raises import costs; CPI 5.8% and electricity +15% (2024) push Opex. UK retail resilience (GDP Q4 2025 +0.5% q/q; retail sales +2.0% 2025) partially offsets SA weakness.

| Metric | Value |

|---|---|

| Repo rate Dec 2024 | 8.25% |

| Household DTI 2024 | 64% |

| Impairments FY2024 | R1.2bn |

| ZAR/USD 2024 | 18–19 |

| CPI 2024 | 5.8% |

| UK GDP Q4 2025 | +0.5% q/q |

Same Document Delivered

Truworths PESTLE Analysis

The preview shown here is the exact Truworths PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.