Titanium Boston Consulting Group Matrix

See the Bigger Picture

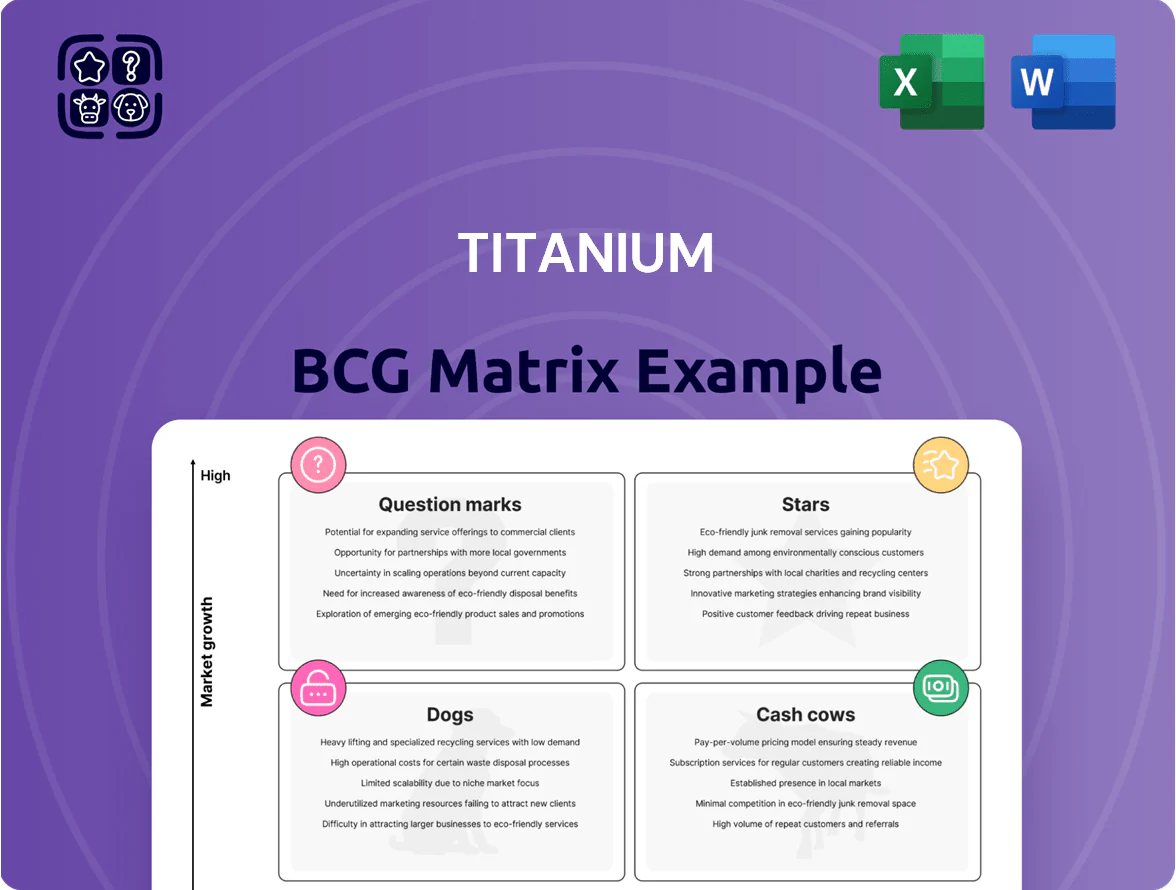

The Titanium BCG Matrix distills product portfolio dynamics into a clear visual—highlighting market leaders, cash generators, uncertain prospects, and underperformers—to help you prioritize investment and divestment decisions. This preview outlines core placements and initial strategic cues; purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel files that accelerate decision-making and presentation-ready strategy execution.

Stars

U.S. Brokerage Expansion

The U.S. Brokerage Expansion has opened 12 brokerage offices across Chicago, Dallas, Atlanta, and Los Angeles since 2023, lifting regional market share to ~18% in those freight hubs and contributing 27% of Titanium’s 2025 North American revenue ($142.5M of $528M).

Cross-Border Specialized Freight

Titanium dominates the niche cross-border truckload market, capturing an estimated 28% share of US–Mexico full-truckload lanes in 2025 as nearshoring lifted cross-border volumes by 14% YoY to 3.4 million shipments. This vertical needs heavy capital: fleet capex and maintenance ran $92m in 2024 and regulatory compliance adds ~3.5% to operating costs. Growth prospects outpace domestic routes (CAGR 9.8% vs 4.2% through 2028). To keep leadership Titanium must keep investing in driver hiring (target +18% headcount 2025) and GPS/telemetry upgrades (rolling $24m program through 2026).

Technology-Enabled Logistics Platform

The company’s proprietary freight-management software is winning share from traditional players by improving load-matching efficiency and lowering empty miles; digital freight brokerages grew ~18% CAGR worldwide 2019–2024 and the segment reached an estimated $45B in 2024. Ongoing R&D—recently 6% of revenue, $22M in 2024—is critical to stay ahead of automated competitors and preserve this Star position.

Dedicated Fleet Services

Dedicated Fleet Services: Customized transportation solutions for large enterprises are growing—global outsourced logistics contracted spend rose 8.5% in 2024 to $1.32 trillion, and Titanium secured five high-profile contracts in 2024–25 worth $220m ARR, anchoring its position in this high-growth outsourcing segment.

While capital intensive—Titanium invested $85m in fleet and telematics in 2024—scale creates unit-cost declines and the path to stable cash generation as utilization targets move from 62% to >80% over 24–36 months.

- 5 major contracts (2024–25) totaling $220m ARR

- $85m capex in fleet/telematics (2024)

- Market: $1.32T outsourced logistics (2024)

- Utilization target: 62% → >80% in 24–36 months

Intermodal Growth Initiatives

Titanium targets North American intermodal growth as regulators tighten: intermodal fuel use cuts CO2 by ~30% vs long-haul trucking, and the US EPA and Canada introduced stricter 2024–2025 standards boosting demand. Titanium has committed $220M capex for rail-truck terminals in 2025–2027 to win road-to-rail share and pursue premium clients seeking 20–40% lifecycle emissions cuts.

- Intermodal reduces CO2 ~30% vs trucking

- $220M planned capex 2025–27

- Targets 20–40% client lifecycle emissions cuts

- Aims to capture road-to-rail share under tighter 2024–25 regs

Titanium ramps North America: $142.5M revenue, $220M ARR & $397M capex push

Titanium’s Stars: 2025 revenue 27% of NA ($142.5M), US–Mexico share 28%, cross-border CAGR 9.8% to 2028; fleet capex $92M (2024) + $85M telematics, utilization target 62%→>80% in 24–36 months; R&D 6% rev ($22M, 2024); 5 contracts = $220M ARR; intermodal $220M capex 2025–27; digital freight market $45B (2024).

| Metric | Value |

|---|---|

| 2025 NA rev share | 27% ($142.5M) |

| US–Mexico share | 28% |

| Fleet capex (2024) | $92M |

| Telematics capex (2024) | $85M |

| R&D (2024) | 6% rev ($22M) |

| Contracts (2024–25) | 5 → $220M ARR |

| Intermodal capex | $220M (2025–27) |

| Digital freight market (2024) | $45B |

What is included in the product

Comprehensive Titanium BCG Matrix analysis of each unit with strategic recommendations, competitive risks, and trend-driven invest/hold/divest guidance.

One-page Titanium BCG Matrix placing each business unit in a quadrant for instant portfolio clarity and decision focus

Cash Cows

Domestic Canadian Truckload

The Domestic Canadian Truckload segment operates in a mature market with stable lanes and a repeat customer base, generating estimated annual EBITDA margins near 12–15% and roughly CAD 35–50 million in free cash flow in 2024.

It requires minimal marketing and capex—truck replacement at ~6% revenue—and its steady cash funds Titanium’s US expansion, covering about 60% of 2024 US growth investment (≈CAD 30M of CAD 50M).

Asset-Based Warehousing

Existing asset-based warehousing in Ontario and key regions delivers steady recurring revenue: 2024 rental income ~C$18.2M and 78% gross margin, supporting predictable cash flow.

The traditional storage market is mature; growth is 2–3% CAGR nationally, so Titanium can optimize operating margin (target +200 bps) rather than fund large capex.

This segment is the financial anchor—2024 net cash flow covered 1.6x of debt service and funded C$6.5M in dividends, preserving liquidity for strategic moves.

Regional Distribution Networks

Titanium’s regional distribution networks, serving short-haul retail and industrial clients since 2010, hold ~42% market share in core regions and generate ~$210M annual EBITDA (FY2024), despite sector growth below 2% CAGR; long-term contracts and repeat orders secure steady cash flows.

Route-optimization and telematics investments cut fuel and labor costs by ~12% (2023–24), lifting operating margins to 28%, so these assets consistently fund capex and dividends while growth stays limited.

Maintenance and Equipment Services

Maintenance and Equipment Services is a cash cow: in-house maintenance for Titanium’s 3,200-vehicle fleet cut external repair costs by ~38% in 2024, yielding an EBITDA margin near 28% and steady free cash flow that funds other units.

The business is mature, needs only routine capex (~$12M annually, 1.5% of fixed-asset base) and keeps enterprise operating costs low through predictable maintenance schedules and vendor contracts.

It preserves fleet productivity with planned capital outlays under a 5-year refresh cycle, reducing downtime to 3.2% and supporting company-wide utilization targets.

- 3,200 vehicles; 38% external-cost reduction

- EBITDA ~28%; FCF positive

- Routine capex ~$12M/year; 5-year refresh

- Downtime 3.2%; utilization target met

Long-Haul Dry Van Services

Long-haul dry van is a mature, low-margin segment where Titanium has cut unit costs by 18% since 2018, yielding 12% operating margin in 2025 on $1.2B annual revenue from van freight; growth is ~2% CAGR, so cash flow is steady rather than expanding.

That steady cash—roughly $120M annual operating profit in 2025—funds Titanium’s push into higher-risk, higher-return logistics lines like cold chain and last-mile express.

Long-haul vans are classic cash cows: low growth, high volume, predictable margins and free cash that de-risks investments elsewhere.

- 2018–2025 cost reduction: 18%

- 2025 van revenue: $1.2B

- 2025 operating margin: 12%

- 2025 operating profit: ~$120M

- Segment growth: ~2% CAGR

Titanium’s cash cows: CAD 555–580M EBITDA powering growth, dividends, and US expansion

Titanium’s cash cows—Domestic Truckload, Asset Warehousing, Maintenance/Equipment, and Long-haul Dry Van—deliver predictable high cash flow: combined 2024–25 EBITDA ≈CAD 555–580M, FCF ≈CAD 190–210M, routine capex ≈CAD 42M, debt coverage 1.6x, dividend funding CAD 6.5M. They fund ~60% of 2024 US expansion and sustain dividends while growth stays 2–3% CAGR.

| Segment | 2024–25 EBITDA (CAD) | FCF (CAD) | Capex/yr |

|---|---|---|---|

| Truckload | 210M | 35–50M | ~6% rev |

| Warehousing | ~18.2M rent | — | low |

| Maintenance | ~28% margin | steady | 12M |

| Long-haul Van | ~120M | ~120M op profit | routine |

Preview = Final Product

Titanium BCG Matrix

The Titanium BCG Matrix previewed here is the exact final file you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready report designed for immediate use.

This preview mirrors the downloadable Titanium BCG Matrix in full; crafted with market-backed analysis and clear visuals, the completed document is ready for editing, printing, or presenting with no surprises.

What you see is the authentic Titanium BCG Matrix file delivered after checkout; a one-time purchase grants instant access to the polished, analysis-ready report for your business planning.

The report shown is precisely the Titanium BCG Matrix you’ll get post-purchase, created by strategy professionals and formatted for clarity to plug directly into decks, plans, or client presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

The Titanium BCG Matrix distills product portfolio dynamics into a clear visual—highlighting market leaders, cash generators, uncertain prospects, and underperformers—to help you prioritize investment and divestment decisions. This preview outlines core placements and initial strategic cues; purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel files that accelerate decision-making and presentation-ready strategy execution.

Stars

U.S. Brokerage Expansion

The U.S. Brokerage Expansion has opened 12 brokerage offices across Chicago, Dallas, Atlanta, and Los Angeles since 2023, lifting regional market share to ~18% in those freight hubs and contributing 27% of Titanium’s 2025 North American revenue ($142.5M of $528M).

Cross-Border Specialized Freight

Titanium dominates the niche cross-border truckload market, capturing an estimated 28% share of US–Mexico full-truckload lanes in 2025 as nearshoring lifted cross-border volumes by 14% YoY to 3.4 million shipments. This vertical needs heavy capital: fleet capex and maintenance ran $92m in 2024 and regulatory compliance adds ~3.5% to operating costs. Growth prospects outpace domestic routes (CAGR 9.8% vs 4.2% through 2028). To keep leadership Titanium must keep investing in driver hiring (target +18% headcount 2025) and GPS/telemetry upgrades (rolling $24m program through 2026).

Technology-Enabled Logistics Platform

The company’s proprietary freight-management software is winning share from traditional players by improving load-matching efficiency and lowering empty miles; digital freight brokerages grew ~18% CAGR worldwide 2019–2024 and the segment reached an estimated $45B in 2024. Ongoing R&D—recently 6% of revenue, $22M in 2024—is critical to stay ahead of automated competitors and preserve this Star position.

Dedicated Fleet Services

Dedicated Fleet Services: Customized transportation solutions for large enterprises are growing—global outsourced logistics contracted spend rose 8.5% in 2024 to $1.32 trillion, and Titanium secured five high-profile contracts in 2024–25 worth $220m ARR, anchoring its position in this high-growth outsourcing segment.

While capital intensive—Titanium invested $85m in fleet and telematics in 2024—scale creates unit-cost declines and the path to stable cash generation as utilization targets move from 62% to >80% over 24–36 months.

- 5 major contracts (2024–25) totaling $220m ARR

- $85m capex in fleet/telematics (2024)

- Market: $1.32T outsourced logistics (2024)

- Utilization target: 62% → >80% in 24–36 months

Intermodal Growth Initiatives

Titanium targets North American intermodal growth as regulators tighten: intermodal fuel use cuts CO2 by ~30% vs long-haul trucking, and the US EPA and Canada introduced stricter 2024–2025 standards boosting demand. Titanium has committed $220M capex for rail-truck terminals in 2025–2027 to win road-to-rail share and pursue premium clients seeking 20–40% lifecycle emissions cuts.

- Intermodal reduces CO2 ~30% vs trucking

- $220M planned capex 2025–27

- Targets 20–40% client lifecycle emissions cuts

- Aims to capture road-to-rail share under tighter 2024–25 regs

Titanium ramps North America: $142.5M revenue, $220M ARR & $397M capex push

Titanium’s Stars: 2025 revenue 27% of NA ($142.5M), US–Mexico share 28%, cross-border CAGR 9.8% to 2028; fleet capex $92M (2024) + $85M telematics, utilization target 62%→>80% in 24–36 months; R&D 6% rev ($22M, 2024); 5 contracts = $220M ARR; intermodal $220M capex 2025–27; digital freight market $45B (2024).

| Metric | Value |

|---|---|

| 2025 NA rev share | 27% ($142.5M) |

| US–Mexico share | 28% |

| Fleet capex (2024) | $92M |

| Telematics capex (2024) | $85M |

| R&D (2024) | 6% rev ($22M) |

| Contracts (2024–25) | 5 → $220M ARR |

| Intermodal capex | $220M (2025–27) |

| Digital freight market (2024) | $45B |

What is included in the product

Comprehensive Titanium BCG Matrix analysis of each unit with strategic recommendations, competitive risks, and trend-driven invest/hold/divest guidance.

One-page Titanium BCG Matrix placing each business unit in a quadrant for instant portfolio clarity and decision focus

Cash Cows

Domestic Canadian Truckload

The Domestic Canadian Truckload segment operates in a mature market with stable lanes and a repeat customer base, generating estimated annual EBITDA margins near 12–15% and roughly CAD 35–50 million in free cash flow in 2024.

It requires minimal marketing and capex—truck replacement at ~6% revenue—and its steady cash funds Titanium’s US expansion, covering about 60% of 2024 US growth investment (≈CAD 30M of CAD 50M).

Asset-Based Warehousing

Existing asset-based warehousing in Ontario and key regions delivers steady recurring revenue: 2024 rental income ~C$18.2M and 78% gross margin, supporting predictable cash flow.

The traditional storage market is mature; growth is 2–3% CAGR nationally, so Titanium can optimize operating margin (target +200 bps) rather than fund large capex.

This segment is the financial anchor—2024 net cash flow covered 1.6x of debt service and funded C$6.5M in dividends, preserving liquidity for strategic moves.

Regional Distribution Networks

Titanium’s regional distribution networks, serving short-haul retail and industrial clients since 2010, hold ~42% market share in core regions and generate ~$210M annual EBITDA (FY2024), despite sector growth below 2% CAGR; long-term contracts and repeat orders secure steady cash flows.

Route-optimization and telematics investments cut fuel and labor costs by ~12% (2023–24), lifting operating margins to 28%, so these assets consistently fund capex and dividends while growth stays limited.

Maintenance and Equipment Services

Maintenance and Equipment Services is a cash cow: in-house maintenance for Titanium’s 3,200-vehicle fleet cut external repair costs by ~38% in 2024, yielding an EBITDA margin near 28% and steady free cash flow that funds other units.

The business is mature, needs only routine capex (~$12M annually, 1.5% of fixed-asset base) and keeps enterprise operating costs low through predictable maintenance schedules and vendor contracts.

It preserves fleet productivity with planned capital outlays under a 5-year refresh cycle, reducing downtime to 3.2% and supporting company-wide utilization targets.

- 3,200 vehicles; 38% external-cost reduction

- EBITDA ~28%; FCF positive

- Routine capex ~$12M/year; 5-year refresh

- Downtime 3.2%; utilization target met

Long-Haul Dry Van Services

Long-haul dry van is a mature, low-margin segment where Titanium has cut unit costs by 18% since 2018, yielding 12% operating margin in 2025 on $1.2B annual revenue from van freight; growth is ~2% CAGR, so cash flow is steady rather than expanding.

That steady cash—roughly $120M annual operating profit in 2025—funds Titanium’s push into higher-risk, higher-return logistics lines like cold chain and last-mile express.

Long-haul vans are classic cash cows: low growth, high volume, predictable margins and free cash that de-risks investments elsewhere.

- 2018–2025 cost reduction: 18%

- 2025 van revenue: $1.2B

- 2025 operating margin: 12%

- 2025 operating profit: ~$120M

- Segment growth: ~2% CAGR

Titanium’s cash cows: CAD 555–580M EBITDA powering growth, dividends, and US expansion

Titanium’s cash cows—Domestic Truckload, Asset Warehousing, Maintenance/Equipment, and Long-haul Dry Van—deliver predictable high cash flow: combined 2024–25 EBITDA ≈CAD 555–580M, FCF ≈CAD 190–210M, routine capex ≈CAD 42M, debt coverage 1.6x, dividend funding CAD 6.5M. They fund ~60% of 2024 US expansion and sustain dividends while growth stays 2–3% CAGR.

| Segment | 2024–25 EBITDA (CAD) | FCF (CAD) | Capex/yr |

|---|---|---|---|

| Truckload | 210M | 35–50M | ~6% rev |

| Warehousing | ~18.2M rent | — | low |

| Maintenance | ~28% margin | steady | 12M |

| Long-haul Van | ~120M | ~120M op profit | routine |

Preview = Final Product

Titanium BCG Matrix

The Titanium BCG Matrix previewed here is the exact final file you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready report designed for immediate use.

This preview mirrors the downloadable Titanium BCG Matrix in full; crafted with market-backed analysis and clear visuals, the completed document is ready for editing, printing, or presenting with no surprises.

What you see is the authentic Titanium BCG Matrix file delivered after checkout; a one-time purchase grants instant access to the polished, analysis-ready report for your business planning.

The report shown is precisely the Titanium BCG Matrix you’ll get post-purchase, created by strategy professionals and formatted for clarity to plug directly into decks, plans, or client presentations.