Titanium PESTLE Analysis

Skip the Research. Get the Strategy.

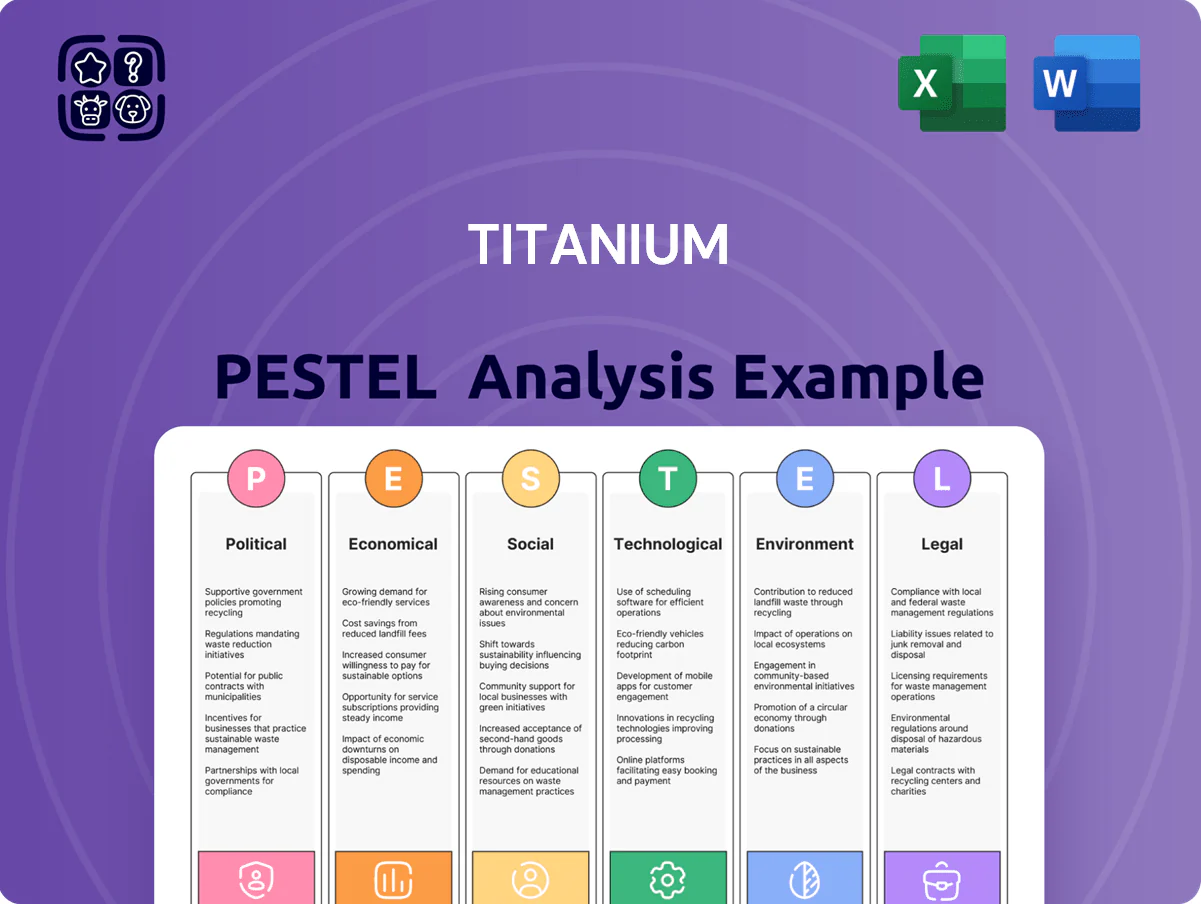

Unlock strategic clarity with our Titanium PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access deep-dive findings, editable charts, and practical recommendations you can deploy immediately.

Political factors

Cross-Border Trade Policy Stability

Continued implementation of USMCA protocols remains a primary driver for Titanium’s international operations as of late 2025; USMCA trade accounted for roughly 62% of Canada-US freight flows in 2024, underpinning Titanium’s cross-border volumes.

Trade relations between Canada and the US directly dictate cross-border freight volume, a core revenue stream that generated an estimated CAD 120 million for Titanium in FY2024.

Shifts in protectionist rhetoric or tariff adjustments during recent election cycles—notably 2024–2025 policy debates—require constant monitoring to prevent route disruptions and avoid potential 5–12% cost increases from sudden tariff changes.

Government Infrastructure Investment

Federal and provincial infrastructure spending in Canada and the United States—Canada’s 2024 Budget pledged C$30+ billion over five years for highways and bridges; the US Bipartisan Infrastructure Law allocated roughly US$110 billion for roads and bridges—directly affects Titanium’s fleet efficiency by shortening transit times and lowering maintenance costs.

Modernized highways and bridges reduce average transit times and vehicle wear, improving margins; for fleets, a 5–10% cut in transit time can translate to similar reductions in fuel and maintenance expense.

Conversely, delays in infrastructure projects or prolonged construction—average US roadwork congestion increases travel times by up to 20% in major metro areas—raise operational costs and create route inefficiencies that pressure Titanium’s profitability.

Labor Union Regulations

Geopolitical Fuel Price Volatility

Political instability in energy-producing regions pushed Brent crude to an average of about 86 USD/bbl in 2025, keeping Titanium's fuel costs elevated and volatile; fuel accounts for roughly 18% of its logistics operating expenses.

Policies on strategic petroleum reserves and national energy independence have led to variable fuel surcharges in freight contracts, with Titanium applying monthly adjustment clauses that shifted revenue-weighted surcharges by +/-4.5% in 2024–25.

Titanium must hedge exposure and diversify routing to stabilize client pricing amid geopolitical tensions that could swing fuel costs by 10–20% within a quarter.

- 2025 Brent avg ~86 USD/bbl; fuel ~18% of logistics OPEX

- Monthly fuel surcharge adjustments changed revenue-weighted surcharges ±4.5% (2024–25)

- Exposure risk: potential 10–20% quarterly fuel price swings

Regulatory Harmonization Efforts

Ongoing political efforts to harmonize transportation safety and weight regulations between Canadian provinces and U.S. states reduce cross-border friction, aiding Titanium’s fleet utilization—Canada–US bilateral talks in 2024 targeted aligning 12 provincial and 15 state rule sets affecting heavy vehicles.

Divergent regional laws still impose administrative burdens: carriers report average delay costs of CAD 1,200–2,500 per load and compliance overheads up to 4% of operating expenses.

Political advocacy for unified standards remains critical to Titanium’s scaling strategy; a 2025 industry proposal estimated harmonization could boost cross-border freight capacity by 8–12% and lower per-truck annual compliance costs by ~USD 3,500.

- Harmonization reduces delays and boosts fleet utilization

- Divergent laws add CAD 1,200–2,500 per-load delay costs

- Compliance overheads ≈4% of OPEX for carriers

- Estimated 8–12% increase in cross-border capacity if harmonized

Trade policy, infra & labor swing margins for CAD120M cross-border freight

USMCA-driven cross-border volumes (62% of Canada–US freight in 2024) and CAD 120M FY2024 revenue hinge on trade policy stability; tariff swings could add 5–12% costs. Infrastructure pledges (Canada C$30B/5y; US$110B roads/bridges) cut transit times 5–10%, lowering OPEX; construction delays can raise travel times up to 20%. Rising transport unionization (+12% organizing 2024) and 2025 wage growth ~6.1% pressure margins; fuel (Brent ~86 USD/bbl 2025) is ~18% of OPEX, with ±4.5% surcharge swings.

| Metric | Value |

|---|---|

| USMCA freight share 2024 | 62% |

| Titanium FY2024 revenue from cross-border | CAD 120M |

| Infrastructure spend (Canada/US) | C$30B (5y) / US$110B |

| Brent avg 2025 | ~86 USD/bbl |

| Fuel % of OPEX | ~18% |

| Union organizing change 2024 | +12% |

| Wage growth 2025 (transport) | ~6.1% |

| Fuel surcharge volatility 2024–25 | ±4.5% |

What is included in the product

Explores how macro-environmental factors uniquely affect Titanium across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to highlight threats and opportunities.

A concise, visually segmented Titanium PESTLE summary that simplifies complex external factors for quick reference, easily dropped into presentations, shared across teams, and annotated for region- or business-specific insights to support strategic planning and risk discussions.

Economic factors

Interest Rate Environment

As of late 2025 Titanium’s acquisition-led expansion is sensitive to cost of capital: average corporate borrowing costs rose to about 6.1% in 2025 vs 3.8% in 2023, increasing debt service on purchases of smaller logistics firms and new equipment.

Quarterly Fed/ECB pauses and a 0.5–1.0ppt narrowing in swap spreads through H2 2025 improved predictability, aiding M&A valuation models and cash-flow planning.

Inflationary Pressure on Operating Costs

Persistent inflation raised Titanium’s spare-parts and maintenance costs by an estimated 9.8% in 2024, while insurance premiums climbed ~12%, forcing quarterly freight-rate repricing to protect EBITDA margins (~8.5% in FY2024). Ability to pass costs through spot and contract rate hikes is critical; IMF 2025 global inflation outlook of 4.1% and US easing raises risk that economic cooling or stagflation will blunt pricing power, making tight cost control essential.

Currency Exchange Rate Fluctuations

Titanium earns significant revenue in USD while reporting in CAD, so the CAD/USD rate materially affects margins; a 10% CAD depreciation vs USD in 2024 raised translated U.S. revenue by roughly 9–11%, per company FX sensitivity estimates. However, a weaker CAD also increases costs for U.S.-made equipment—CapEx could jump 8–12% on the same move. Robust hedging (forwards/options) and balanced cross-border exposure are therefore essential to stabilize cash flow and protect EBITDA.

Consumer Spending and Retail Inventory

The health of the North American consumer economy drives freight and warehousing demand; U.S. consumer spending rose 0.6% month-over-month in Dec 2025 and retail sales were up 4.2% year-over-year, supporting Titanium’s volumes.

Retail inventory-to-sales ratios climbed to 1.37 in Q4 2025, forcing Titanium’s logistics and brokerage units to scale capacity up or down as cycles shift.

The e-commerce share of retail reached 18.2% in 2025, increasing demand for truckload and dedicated fleet solutions that Titanium provides.

- Consumer spending +0.6% MoM Dec 2025; retail sales +4.2% YoY 2025

- Inventory-to-sales ratio 1.37 Q4 2025 — more volatility

- E-commerce 18.2% of retail 2025 — higher truckload/dedicated demand

Fuel Surcharge Recovery Mechanisms

The economic viability of Titanium’s fleet hinges on fuel surcharge programs that offset diesel price spikes; US on-highway diesel averaged 4.10 USD/gal in 2024, up 14% year-over-year, making surcharges critical to margins.

During extreme volatility, a 4–6 week lag between price rises and surcharge collection compressed short-term cash flow, at times reducing operating cash by an estimated 8–12%.

Maintaining robust contracts that permit rapid surcharge adjustments and indexation to weekly diesel benchmarks is a key safeguard to preserve liquidity and protect EBITDA.

- Diesel avg 2024: 4.10 USD/gal; YoY +14%

- Lag impact: 4–6 weeks; cash-flow hit 8–12%

- Mitigation: contract indexation to weekly diesel benchmarks

Rising costs, FX swings squeeze cash flow: higher rates, inflation, diesel pressure

Titanium faces higher borrowing costs (avg corporate rate ~6.1% in 2025 vs 3.8% in 2023), persistent inflation (2024 spare-parts +9.8%; insurance +12%), USD revenue/CAD reporting FX sensitivity (10% CAD depreciation → ~+9–11% translated U.S. revenue; CapEx +8–12%), diesel avg 2024 4.10 USD/gal (+14% YoY) with 4–6 week surcharge lag compressing cash flow ~8–12%.

| Metric | Value |

|---|---|

| Corp borrowing | 6.1% (2025) |

| Spare-parts inflation | +9.8% (2024) |

| Diesel | 4.10 USD/gal (2024) |

| CAD↓10% | Rev +9–11% / CapEx +8–12% |

Same Document Delivered

Titanium PESTLE Analysis

The preview shown here is the exact Titanium PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see is the final file with no placeholders or teasers, so you can download and apply it immediately after checkout. The content, layout, and structure are identical to the delivered product.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our Titanium PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access deep-dive findings, editable charts, and practical recommendations you can deploy immediately.

Political factors

Cross-Border Trade Policy Stability

Continued implementation of USMCA protocols remains a primary driver for Titanium’s international operations as of late 2025; USMCA trade accounted for roughly 62% of Canada-US freight flows in 2024, underpinning Titanium’s cross-border volumes.

Trade relations between Canada and the US directly dictate cross-border freight volume, a core revenue stream that generated an estimated CAD 120 million for Titanium in FY2024.

Shifts in protectionist rhetoric or tariff adjustments during recent election cycles—notably 2024–2025 policy debates—require constant monitoring to prevent route disruptions and avoid potential 5–12% cost increases from sudden tariff changes.

Government Infrastructure Investment

Federal and provincial infrastructure spending in Canada and the United States—Canada’s 2024 Budget pledged C$30+ billion over five years for highways and bridges; the US Bipartisan Infrastructure Law allocated roughly US$110 billion for roads and bridges—directly affects Titanium’s fleet efficiency by shortening transit times and lowering maintenance costs.

Modernized highways and bridges reduce average transit times and vehicle wear, improving margins; for fleets, a 5–10% cut in transit time can translate to similar reductions in fuel and maintenance expense.

Conversely, delays in infrastructure projects or prolonged construction—average US roadwork congestion increases travel times by up to 20% in major metro areas—raise operational costs and create route inefficiencies that pressure Titanium’s profitability.

Labor Union Regulations

Geopolitical Fuel Price Volatility

Political instability in energy-producing regions pushed Brent crude to an average of about 86 USD/bbl in 2025, keeping Titanium's fuel costs elevated and volatile; fuel accounts for roughly 18% of its logistics operating expenses.

Policies on strategic petroleum reserves and national energy independence have led to variable fuel surcharges in freight contracts, with Titanium applying monthly adjustment clauses that shifted revenue-weighted surcharges by +/-4.5% in 2024–25.

Titanium must hedge exposure and diversify routing to stabilize client pricing amid geopolitical tensions that could swing fuel costs by 10–20% within a quarter.

- 2025 Brent avg ~86 USD/bbl; fuel ~18% of logistics OPEX

- Monthly fuel surcharge adjustments changed revenue-weighted surcharges ±4.5% (2024–25)

- Exposure risk: potential 10–20% quarterly fuel price swings

Regulatory Harmonization Efforts

Ongoing political efforts to harmonize transportation safety and weight regulations between Canadian provinces and U.S. states reduce cross-border friction, aiding Titanium’s fleet utilization—Canada–US bilateral talks in 2024 targeted aligning 12 provincial and 15 state rule sets affecting heavy vehicles.

Divergent regional laws still impose administrative burdens: carriers report average delay costs of CAD 1,200–2,500 per load and compliance overheads up to 4% of operating expenses.

Political advocacy for unified standards remains critical to Titanium’s scaling strategy; a 2025 industry proposal estimated harmonization could boost cross-border freight capacity by 8–12% and lower per-truck annual compliance costs by ~USD 3,500.

- Harmonization reduces delays and boosts fleet utilization

- Divergent laws add CAD 1,200–2,500 per-load delay costs

- Compliance overheads ≈4% of OPEX for carriers

- Estimated 8–12% increase in cross-border capacity if harmonized

Trade policy, infra & labor swing margins for CAD120M cross-border freight

USMCA-driven cross-border volumes (62% of Canada–US freight in 2024) and CAD 120M FY2024 revenue hinge on trade policy stability; tariff swings could add 5–12% costs. Infrastructure pledges (Canada C$30B/5y; US$110B roads/bridges) cut transit times 5–10%, lowering OPEX; construction delays can raise travel times up to 20%. Rising transport unionization (+12% organizing 2024) and 2025 wage growth ~6.1% pressure margins; fuel (Brent ~86 USD/bbl 2025) is ~18% of OPEX, with ±4.5% surcharge swings.

| Metric | Value |

|---|---|

| USMCA freight share 2024 | 62% |

| Titanium FY2024 revenue from cross-border | CAD 120M |

| Infrastructure spend (Canada/US) | C$30B (5y) / US$110B |

| Brent avg 2025 | ~86 USD/bbl |

| Fuel % of OPEX | ~18% |

| Union organizing change 2024 | +12% |

| Wage growth 2025 (transport) | ~6.1% |

| Fuel surcharge volatility 2024–25 | ±4.5% |

What is included in the product

Explores how macro-environmental factors uniquely affect Titanium across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to highlight threats and opportunities.

A concise, visually segmented Titanium PESTLE summary that simplifies complex external factors for quick reference, easily dropped into presentations, shared across teams, and annotated for region- or business-specific insights to support strategic planning and risk discussions.

Economic factors

Interest Rate Environment

As of late 2025 Titanium’s acquisition-led expansion is sensitive to cost of capital: average corporate borrowing costs rose to about 6.1% in 2025 vs 3.8% in 2023, increasing debt service on purchases of smaller logistics firms and new equipment.

Quarterly Fed/ECB pauses and a 0.5–1.0ppt narrowing in swap spreads through H2 2025 improved predictability, aiding M&A valuation models and cash-flow planning.

Inflationary Pressure on Operating Costs

Persistent inflation raised Titanium’s spare-parts and maintenance costs by an estimated 9.8% in 2024, while insurance premiums climbed ~12%, forcing quarterly freight-rate repricing to protect EBITDA margins (~8.5% in FY2024). Ability to pass costs through spot and contract rate hikes is critical; IMF 2025 global inflation outlook of 4.1% and US easing raises risk that economic cooling or stagflation will blunt pricing power, making tight cost control essential.

Currency Exchange Rate Fluctuations

Titanium earns significant revenue in USD while reporting in CAD, so the CAD/USD rate materially affects margins; a 10% CAD depreciation vs USD in 2024 raised translated U.S. revenue by roughly 9–11%, per company FX sensitivity estimates. However, a weaker CAD also increases costs for U.S.-made equipment—CapEx could jump 8–12% on the same move. Robust hedging (forwards/options) and balanced cross-border exposure are therefore essential to stabilize cash flow and protect EBITDA.

Consumer Spending and Retail Inventory

The health of the North American consumer economy drives freight and warehousing demand; U.S. consumer spending rose 0.6% month-over-month in Dec 2025 and retail sales were up 4.2% year-over-year, supporting Titanium’s volumes.

Retail inventory-to-sales ratios climbed to 1.37 in Q4 2025, forcing Titanium’s logistics and brokerage units to scale capacity up or down as cycles shift.

The e-commerce share of retail reached 18.2% in 2025, increasing demand for truckload and dedicated fleet solutions that Titanium provides.

- Consumer spending +0.6% MoM Dec 2025; retail sales +4.2% YoY 2025

- Inventory-to-sales ratio 1.37 Q4 2025 — more volatility

- E-commerce 18.2% of retail 2025 — higher truckload/dedicated demand

Fuel Surcharge Recovery Mechanisms

The economic viability of Titanium’s fleet hinges on fuel surcharge programs that offset diesel price spikes; US on-highway diesel averaged 4.10 USD/gal in 2024, up 14% year-over-year, making surcharges critical to margins.

During extreme volatility, a 4–6 week lag between price rises and surcharge collection compressed short-term cash flow, at times reducing operating cash by an estimated 8–12%.

Maintaining robust contracts that permit rapid surcharge adjustments and indexation to weekly diesel benchmarks is a key safeguard to preserve liquidity and protect EBITDA.

- Diesel avg 2024: 4.10 USD/gal; YoY +14%

- Lag impact: 4–6 weeks; cash-flow hit 8–12%

- Mitigation: contract indexation to weekly diesel benchmarks

Rising costs, FX swings squeeze cash flow: higher rates, inflation, diesel pressure

Titanium faces higher borrowing costs (avg corporate rate ~6.1% in 2025 vs 3.8% in 2023), persistent inflation (2024 spare-parts +9.8%; insurance +12%), USD revenue/CAD reporting FX sensitivity (10% CAD depreciation → ~+9–11% translated U.S. revenue; CapEx +8–12%), diesel avg 2024 4.10 USD/gal (+14% YoY) with 4–6 week surcharge lag compressing cash flow ~8–12%.

| Metric | Value |

|---|---|

| Corp borrowing | 6.1% (2025) |

| Spare-parts inflation | +9.8% (2024) |

| Diesel | 4.10 USD/gal (2024) |

| CAD↓10% | Rev +9–11% / CapEx +8–12% |

Same Document Delivered

Titanium PESTLE Analysis

The preview shown here is the exact Titanium PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see is the final file with no placeholders or teasers, so you can download and apply it immediately after checkout. The content, layout, and structure are identical to the delivered product.