Tubos Reunidos PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our focused PESTLE Analysis of Tubos Reunidos—uncover how political shifts, economic cycles, regulatory pressures, technological change, social trends, and environmental policies will shape its trajectory; purchase the full report for granular insights, ready-to-use charts, and actionable recommendations to inform investment, strategy, or competitive analysis.

Political factors

EU Energy Security and Independence Policies

The REPowerEU package and allied national schemes through 2025 channel over €300bn in investments toward European energy independence, prioritizing domestic manufacturing of pipelines and storage; Tubos Reunidos stands to gain as an EU/Spain supplier of seamless steel tubes used in hydrogen, gas and LNG projects.

Global Trade Protectionism and Tariffs

Trade tensions between the US, EU and major blocs have sustained anti-dumping duties and tariffs on steel—US Section 232 and EU safeguard measures—supporting Tubos Reunidos by reducing low-cost imports from regions with weaker environmental/labor standards; in 2024 Spain exported €1.9bn in steel tubes, with Tubos Reunidos relying on exports ~60% of sales.

Geopolitical Stability in Key Energy Regions

Political instability in the Middle East and Eastern Europe in late 2025 has delayed or reprioritized energy projects, with global oil and gas capex forecasts cut about 7% year-on-year, squeezing near-term demand for tubes used in pipelines.

As a supplier to oil and gas, Tubos Reunidos remains sensitive to diplomatic shifts that can halt or accelerate projects; roughly 28% of its 2024 revenue was linked to energy-sector contracts, exposing it to regional disruptions.

The company mitigates localized risk through a diversified footprint across Europe, Latin America and the Middle East, aiming to keep project exposure balanced and protect its order book against single-region upheavals.

Spanish Industrial Support and Subsidies

The Spanish government’s recovery and transformation funds have allocated over €10bn to industrial decarbonization programs (2023–2025), enabling Tubos Reunidos to obtain low-interest EU-aligned loans and grants to modernize Basque Country plants.

Alignment with national industrial strategies remains critical to access direct subsidies and financing; Tubos Reunidos reported capital expenditure plans of ~€45m in 2024 for technological upgrades tied to these programs.

- €10bn+ national decarbonization funds (2023–2025)

- Tubos Reunidos capex ~€45m in 2024 for modernization

- Access to low-interest loans and direct grants depends on policy alignment

International Carbon Policy Alignment

As global leaders align on climate goals into 2026, political pressure on steel makers to cut CO2 has risen; EU Carbon Border Adjustment Mechanism and tightened ETS rates push effective carbon costs for steel up ~25% vs 2021 levels, pressuring Tubos Reunidos to decarbonize.

Tubos Reunidos faces stricter rules mandating carbon accounting and verified emissions reductions; public disclosures and scope 1–3 reporting are increasingly required across EU and export markets.

Mandatory green procurement in public infrastructure—estimated €500+ billion EU pipeline 2024–26—creates demand for low-carbon premium tubular products, posing both compliance costs and revenue upside for higher-margin green lines.

- Rising carbon costs (~+25% vs 2021)

- Mandatory scope 1–3 reporting

- €500B+ EU green infrastructure pipeline (2024–26)

Tubos Reunidos Poised for Green Boom as €300bn EU Funds and €500B+ Pipeline Drive Demand

EU energy funding (€300bn) and Spain decarbonization funds (€10bn+) boost Tubos Reunidos’ green pipeline opportunities; exports (~60% sales) gain from trade protections (US Section 232, EU safeguards) while geopolitical shocks trimmed oil/gas capex ~7% y/y; carbon costs up ~25% vs 2021, mandatory scope 1–3 reporting and €500B+ EU green procurement drive demand for low‑carbon tubes.

| Metric | Value |

|---|---|

| EU energy fund | €300bn |

| Spain decarb funds | €10bn+ |

| Exports share (2024) | ~60% |

| Energy revenue (2024) | ~28% |

| Oil/gas capex change | -7% y/y |

| Carbon cost vs 2021 | +25% |

| EU green pipeline (2024–26) | €500B+ |

What is included in the product

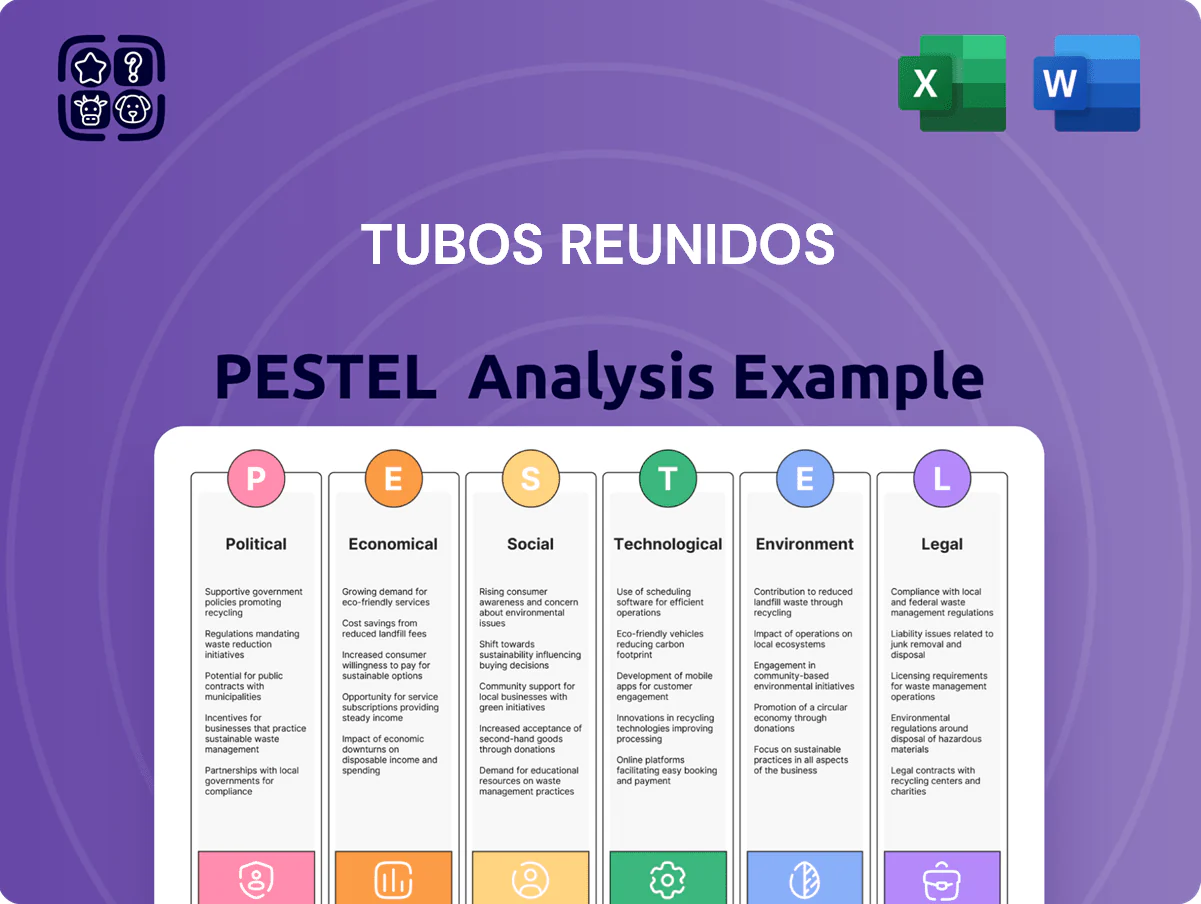

Explores how external macro-environmental factors uniquely affect Tubos Reunidos across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trends to identify threats, opportunities and forward-looking scenarios tailored to its steel/tube manufacturing markets and region.

Condenses Tubos Reunidos' PESTLE into a clean, shareable summary that highlights key external risks and opportunities for quick reference in meetings, presentations, or client reports.

Economic factors

Volatility in Raw Material and Scrap Prices

At end-2025 Tubos Reunidos' margins remain highly sensitive to steel scrap and alloy costs, with scrap prices averaging about $420/ton in 2025 Q4 versus $360/ton a year earlier, driving raw-material cost swings of ~8–12% on COGS; the firm uses futures, physical forward buys and pass-through pricing to manage this, while recovery in EU and US manufacturing (PMI averaging ~51–53 in 2025) tightened supply and pushed alloy premiums up ~15% year-on-year.

Energy Cost Fluctuations in the European Market

Despite stabilization from 2022 peaks, Spain industrial electricity prices averaged about 120 EUR/MWh in 2024 and EU wholesale gas settled near 30 EUR/MWh, keeping energy a major cost for Tubos Reunidos’ steel operations.

The company has invested over EUR 25m since 2021 in efficiency projects and signed long‑term PPAs covering an estimated 40% of its electricity demand to hedge price spikes.

Profitability remains sensitive to regional energy transition progress and grid stability, with a 5–10% swing in energy costs able to materially affect EBITDA margins in energy‑intensive lines.

Interest Rate Environment and Debt Servicing

The late-2025 Euro area average deposit rate around 3.5–4.0% and ECB policy rates near 4.25% raise Tubos Reunidos’ refinancing costs, likely lifting annual interest expenses and compressing free cash flow for capex and R&D given the company’s net debt of about €300–€350m (2024 reported range).

Global Oil and Gas Capital Expenditure Trends

The economic health of Tubos Reunidos is tightly tied to CAPEX from energy majors and NOCs; global oil and gas CAPEX rose to about $320 billion in 2024 and is projected near $340 billion in 2025, supporting tubular demand.

A balanced spend between fossil and new energy kept tubular orders stable in 2024–25, while shifts to deep-water and complex extraction—now ~22% of upstream spend—favor high-margin, high-performance tubulars.

- 2024 global upstream CAPEX ≈ $320bn; 2025 est ≈ $340bn

- Deep-water/complex projects ≈ 22% of upstream spend

- Higher-margin tubular demand rising with complex extraction

Currency Exchange Rate Fluctuations

With roughly 40–50% of Tubos Reunidos’ sales invoiced in US dollars while major costs remain in euros, EUR/USD moves create material transaction and translation exposure that affected 2024 EBITDA margins by an estimated 60–120 basis points when the euro strengthened ~6% vs USD.

Exchange-rate shifts alter export competitiveness into Americas and influence consolidated net income; hedging and active FX management—including forwards and natural hedges—remain central to protect cash flow and reported results.

- ~40–50% revenues USD-denominated

- ~6% EUR appreciation in 2024 moved EBITDA by 60–120 bps

- Primary mitigants: forwards, natural hedges, currency policy

Commodity, energy & FX swings tighten margins as rates and debt raise financing costs

Economic factors: raw-material volatility (2025 scrap ~$420/t vs $360/t in 2024) and energy costs (Spain 2024 avg ~120 EUR/MWh) materially swing COGS and EBITDA; EUR policy rates ~4.25% and late‑2025 deposit rates 3.5–4.0% increase financing costs vs net debt €300–350m; global upstream CAPEX ~€300bn–€320bn (2024–25) supports tubular demand; ~40–50% revenues USD‑denominated causing 60–120bps EBITDA FX sensitivity.

| Metric | Value |

|---|---|

| Scrap price (Q4 2025) | $420/t |

| Spain power (2024 avg) | 120 EUR/MWh |

| Net debt (2024) | €300–350m |

| Upstream CAPEX (2024–25) | $320–340bn |

| USD revenue share | 40–50% |

Preview the Actual Deliverable

Tubos Reunidos PESTLE Analysis

The preview shown here is the exact Tubos Reunidos PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the file you’ll download immediately after checkout—no placeholders or surprises.

Everything displayed here is part of the final product, providing a complete PESTLE overview for Tubos Reunidos to support your strategic decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our focused PESTLE Analysis of Tubos Reunidos—uncover how political shifts, economic cycles, regulatory pressures, technological change, social trends, and environmental policies will shape its trajectory; purchase the full report for granular insights, ready-to-use charts, and actionable recommendations to inform investment, strategy, or competitive analysis.

Political factors

EU Energy Security and Independence Policies

The REPowerEU package and allied national schemes through 2025 channel over €300bn in investments toward European energy independence, prioritizing domestic manufacturing of pipelines and storage; Tubos Reunidos stands to gain as an EU/Spain supplier of seamless steel tubes used in hydrogen, gas and LNG projects.

Global Trade Protectionism and Tariffs

Trade tensions between the US, EU and major blocs have sustained anti-dumping duties and tariffs on steel—US Section 232 and EU safeguard measures—supporting Tubos Reunidos by reducing low-cost imports from regions with weaker environmental/labor standards; in 2024 Spain exported €1.9bn in steel tubes, with Tubos Reunidos relying on exports ~60% of sales.

Geopolitical Stability in Key Energy Regions

Political instability in the Middle East and Eastern Europe in late 2025 has delayed or reprioritized energy projects, with global oil and gas capex forecasts cut about 7% year-on-year, squeezing near-term demand for tubes used in pipelines.

As a supplier to oil and gas, Tubos Reunidos remains sensitive to diplomatic shifts that can halt or accelerate projects; roughly 28% of its 2024 revenue was linked to energy-sector contracts, exposing it to regional disruptions.

The company mitigates localized risk through a diversified footprint across Europe, Latin America and the Middle East, aiming to keep project exposure balanced and protect its order book against single-region upheavals.

Spanish Industrial Support and Subsidies

The Spanish government’s recovery and transformation funds have allocated over €10bn to industrial decarbonization programs (2023–2025), enabling Tubos Reunidos to obtain low-interest EU-aligned loans and grants to modernize Basque Country plants.

Alignment with national industrial strategies remains critical to access direct subsidies and financing; Tubos Reunidos reported capital expenditure plans of ~€45m in 2024 for technological upgrades tied to these programs.

- €10bn+ national decarbonization funds (2023–2025)

- Tubos Reunidos capex ~€45m in 2024 for modernization

- Access to low-interest loans and direct grants depends on policy alignment

International Carbon Policy Alignment

As global leaders align on climate goals into 2026, political pressure on steel makers to cut CO2 has risen; EU Carbon Border Adjustment Mechanism and tightened ETS rates push effective carbon costs for steel up ~25% vs 2021 levels, pressuring Tubos Reunidos to decarbonize.

Tubos Reunidos faces stricter rules mandating carbon accounting and verified emissions reductions; public disclosures and scope 1–3 reporting are increasingly required across EU and export markets.

Mandatory green procurement in public infrastructure—estimated €500+ billion EU pipeline 2024–26—creates demand for low-carbon premium tubular products, posing both compliance costs and revenue upside for higher-margin green lines.

- Rising carbon costs (~+25% vs 2021)

- Mandatory scope 1–3 reporting

- €500B+ EU green infrastructure pipeline (2024–26)

Tubos Reunidos Poised for Green Boom as €300bn EU Funds and €500B+ Pipeline Drive Demand

EU energy funding (€300bn) and Spain decarbonization funds (€10bn+) boost Tubos Reunidos’ green pipeline opportunities; exports (~60% sales) gain from trade protections (US Section 232, EU safeguards) while geopolitical shocks trimmed oil/gas capex ~7% y/y; carbon costs up ~25% vs 2021, mandatory scope 1–3 reporting and €500B+ EU green procurement drive demand for low‑carbon tubes.

| Metric | Value |

|---|---|

| EU energy fund | €300bn |

| Spain decarb funds | €10bn+ |

| Exports share (2024) | ~60% |

| Energy revenue (2024) | ~28% |

| Oil/gas capex change | -7% y/y |

| Carbon cost vs 2021 | +25% |

| EU green pipeline (2024–26) | €500B+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tubos Reunidos across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trends to identify threats, opportunities and forward-looking scenarios tailored to its steel/tube manufacturing markets and region.

Condenses Tubos Reunidos' PESTLE into a clean, shareable summary that highlights key external risks and opportunities for quick reference in meetings, presentations, or client reports.

Economic factors

Volatility in Raw Material and Scrap Prices

At end-2025 Tubos Reunidos' margins remain highly sensitive to steel scrap and alloy costs, with scrap prices averaging about $420/ton in 2025 Q4 versus $360/ton a year earlier, driving raw-material cost swings of ~8–12% on COGS; the firm uses futures, physical forward buys and pass-through pricing to manage this, while recovery in EU and US manufacturing (PMI averaging ~51–53 in 2025) tightened supply and pushed alloy premiums up ~15% year-on-year.

Energy Cost Fluctuations in the European Market

Despite stabilization from 2022 peaks, Spain industrial electricity prices averaged about 120 EUR/MWh in 2024 and EU wholesale gas settled near 30 EUR/MWh, keeping energy a major cost for Tubos Reunidos’ steel operations.

The company has invested over EUR 25m since 2021 in efficiency projects and signed long‑term PPAs covering an estimated 40% of its electricity demand to hedge price spikes.

Profitability remains sensitive to regional energy transition progress and grid stability, with a 5–10% swing in energy costs able to materially affect EBITDA margins in energy‑intensive lines.

Interest Rate Environment and Debt Servicing

The late-2025 Euro area average deposit rate around 3.5–4.0% and ECB policy rates near 4.25% raise Tubos Reunidos’ refinancing costs, likely lifting annual interest expenses and compressing free cash flow for capex and R&D given the company’s net debt of about €300–€350m (2024 reported range).

Global Oil and Gas Capital Expenditure Trends

The economic health of Tubos Reunidos is tightly tied to CAPEX from energy majors and NOCs; global oil and gas CAPEX rose to about $320 billion in 2024 and is projected near $340 billion in 2025, supporting tubular demand.

A balanced spend between fossil and new energy kept tubular orders stable in 2024–25, while shifts to deep-water and complex extraction—now ~22% of upstream spend—favor high-margin, high-performance tubulars.

- 2024 global upstream CAPEX ≈ $320bn; 2025 est ≈ $340bn

- Deep-water/complex projects ≈ 22% of upstream spend

- Higher-margin tubular demand rising with complex extraction

Currency Exchange Rate Fluctuations

With roughly 40–50% of Tubos Reunidos’ sales invoiced in US dollars while major costs remain in euros, EUR/USD moves create material transaction and translation exposure that affected 2024 EBITDA margins by an estimated 60–120 basis points when the euro strengthened ~6% vs USD.

Exchange-rate shifts alter export competitiveness into Americas and influence consolidated net income; hedging and active FX management—including forwards and natural hedges—remain central to protect cash flow and reported results.

- ~40–50% revenues USD-denominated

- ~6% EUR appreciation in 2024 moved EBITDA by 60–120 bps

- Primary mitigants: forwards, natural hedges, currency policy

Commodity, energy & FX swings tighten margins as rates and debt raise financing costs

Economic factors: raw-material volatility (2025 scrap ~$420/t vs $360/t in 2024) and energy costs (Spain 2024 avg ~120 EUR/MWh) materially swing COGS and EBITDA; EUR policy rates ~4.25% and late‑2025 deposit rates 3.5–4.0% increase financing costs vs net debt €300–350m; global upstream CAPEX ~€300bn–€320bn (2024–25) supports tubular demand; ~40–50% revenues USD‑denominated causing 60–120bps EBITDA FX sensitivity.

| Metric | Value |

|---|---|

| Scrap price (Q4 2025) | $420/t |

| Spain power (2024 avg) | 120 EUR/MWh |

| Net debt (2024) | €300–350m |

| Upstream CAPEX (2024–25) | $320–340bn |

| USD revenue share | 40–50% |

Preview the Actual Deliverable

Tubos Reunidos PESTLE Analysis

The preview shown here is the exact Tubos Reunidos PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the file you’ll download immediately after checkout—no placeholders or surprises.

Everything displayed here is part of the final product, providing a complete PESTLE overview for Tubos Reunidos to support your strategic decisions.