Tubos Reunidos SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Tubos Reunidos shows resilience through technical know-how and diversified steel tube offerings, but faces cyclicality, raw-material exposure, and competitive pressure that could limit margin recovery.

Discover the full SWOT analysis for a detailed, research-backed breakdown, editable Word and Excel deliverables, and actionable strategies to inform investment, competitive positioning, or operational planning—available instantly for purchase.

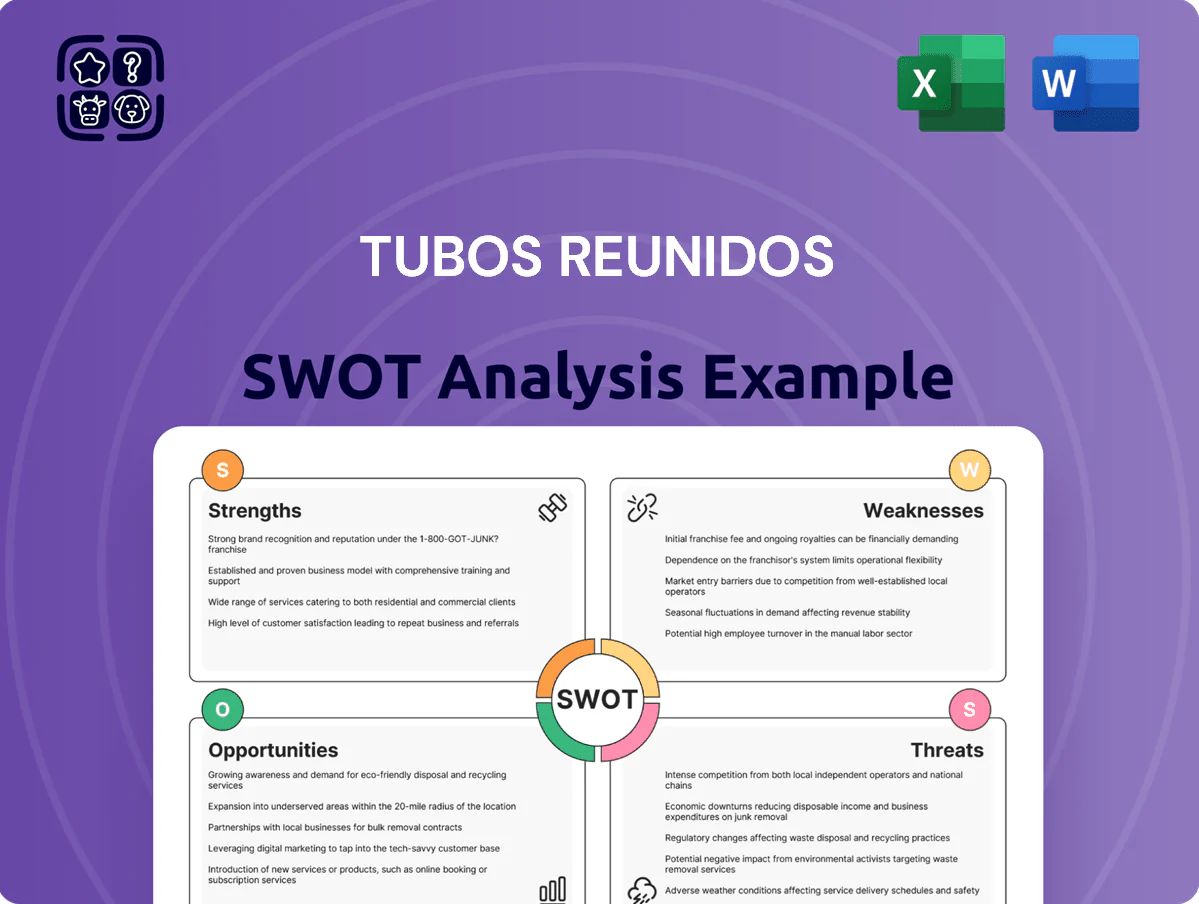

Strengths

Specialized High-Value Product Portfolio

Tubos Reunidos focuses on high-performance seamless steel tubes for energy and petrochemicals, with premium hot-finished and cold-drawn lines accounting for roughly 68% of 2024 sales, boosting average selling prices 22% above commodity peers. This specialization supports higher margins (EBITDA margin 11.5% in 2024) and long-term contracts with blue-chip clients like Repsol and TotalEnergies, strengthening pricing power and repeat-orders.

Successful Financial Restructuring and Debt Profile

By end-2025 Tubos Reunidos cut net debt to €48m from €210m in 2022 after SEPI (Sociedad Estatal de Participaciones Industriales) support and restructuring, lifting net-debt/EBITDA to 0.9x versus 3.8x in 2022 and restoring investor confidence.

Improved cash flow funded €25m capex plan for 2026 and reduced interest expense by €12m yearly, giving the firm greater resilience across steel-cycle downturns than in the prior decade.

Advanced Technological and Operational Efficiency

Integration of electric arc furnace (EAF) technology cut Tubos Reunidos’ CO2 intensity by about 40% vs blast-furnace peers, supporting 2024 scope-1 reductions and aligning with EU ETS targets; EAFs also reduced energy cost per tonne by ~18%, improving 2024 gross margin by an estimated 120 bps. EAFs enable flexible batch production, meeting varied specifications for oil & gas and mechanical engineering exports. This tech keeps unit costs competitive while easing compliance with tighter EU carbon caps and customer decarbonization specs.

Strong Global Export Footprint

Tubos Reunidos generates roughly 60% of 2024 revenue from outside Spain, with strong sales in North America and the Middle East, boosting resilience against regional downturns.

Geographic diversification lets the company tap diverse energy-market growth—oil & gas, power, and hydrogen—reducing revenue volatility and improving order visibility.

Established distribution and local technical teams ensure on-time delivery and field support for large projects, cutting implementation delays and warranty costs.

- ~60% 2024 revenue from international markets

- Key markets: North America, Middle East

- Distribution + local tech support = faster delivery

- Reduces regional demand risk, increases order visibility

Commitment to Decarbonization and ESG Standards

Tubos Reunidos has made decarbonization central to its strategy, targeting a 35% CO2 intensity reduction by 2030 and adopting circular-economy steps like 60% recycled steel feed by 2025, which strengthened ESG credentials and cut energy costs 8% in 2024.

By end-2025 those credentials attracted institutional investors (ESG funds now ~12% of free float) and met large buyers’ green procurement rules, giving Tubos a clear edge in a high-carbon sector.

- 35% CO2 intensity cut target by 2030

- 60% recycled steel feed by 2025

- 8% lower energy cost in 2024

- ESG funds ≈12% of free float by 2025

High-value tube niche boosts margins, cuts debt and CO2—global growth & ESG traction

Strong niche in high-value seamless tubes (68% of 2024 sales) drove 22% higher ASPs and 11.5% EBITDA margin in 2024; net debt cut to €48m by end-2025 (net-debt/EBITDA 0.9x). EAF adoption cut CO2 intensity ~40% vs blast-furnace peers, saved ~18% energy cost per tonne, and raised ESG funds to ~12% of free float. ~60% 2024 revenue international, key markets North America and Middle East.

| Metric | 2024/End-2025 |

|---|---|

| High-value sales | 68% of 2024 sales |

| EBITDA margin | 11.5% (2024) |

| Net debt | €48m (end-2025) |

| Net-debt/EBITDA | 0.9x (end-2025) |

| CO2 intensity cut vs peers | ~40% |

| Energy cost/tonne | ~18% lower |

| International revenue | ~60% (2024) |

| ESG funds | ~12% of free float (2025) |

What is included in the product

Provides a concise SWOT overview of Tubos Reunidos, highlighting its operational strengths and weaknesses alongside market opportunities and external threats shaping its strategic outlook.

Provides a clear, compact SWOT summary of Tubos Reunidos to speed strategic alignment and support rapid stakeholder briefings.

Weaknesses

Susceptibility to Energy Price Fluctuations

As an energy‑intensive steel-tube maker, Tubos Reunidos faces high exposure to EU electricity and natural gas swings; European industrial power prices rose ~45% year‑on‑year in 2022 and remain 20–30% above 2019 levels, which can quickly erase margins. Despite €25m–€40m annual efficiency savings since 2020, sudden spikes (e.g., 2022 peaks) disrupted forecasts and pushed EBITDA margins down. Long-term hedges cover only portions of consumption, leaving structural cost instability hard to eliminate.

Exposure to Cyclical Industry Trends

Demand for seamless tubes at Tubos Reunidos is tightly tied to oil, gas and power capex cycles; global oil prices fell ~45% in 2020 and capex returned slowly, cutting tubulars orders and causing 2020 group sales to drop 28% to €293m.

When Brent drops, exploration activity falls and order volumes decline; in 2024 E&P capex remained ~15% below 2019 levels, keeping tubular demand volatile and hurting consistent year-over-year growth.

This cyclicality forces cautious inventory and working-capital management—emptying backlogs fast raises stock-out risk, while excess inventory ties up the €100m+ yearly procurement spend and compresses margins.

Concentration Risk in Specific Export Markets

While Tubos Reunidos has global sales, 48% of 2024 exports went to North America, creating concentration risk if USMCA shifts or US tariff moves occur.

New tariffs or protectionist steps could cut margins and sales; a 5% tariff on steel pipes would erase roughly €12–18m in annual EBITDA based on 2024 margins.

Diversifying clients remains urgent; management aims to reduce North American share below 35% over three years, but execution and new commercial wins are still pending.

Operational Sensitivity to Raw Material Costs

The company’s EBITDA is highly sensitive to steel scrap and alloy prices used in its electric-arc furnaces; steel scrap rose ~18% year-on-year in 2024, squeezing margins when prices spike.

Global scrap volatility means input costs can jump before contract prices adjust, creating margin pressure—Tubos Reunidos reported negative operating leverage in H1 2024 during a raw-materials surge.

Lagged cost recovery during rapid commodity inflation can cut operating margins by several percentage points within quarters.

- Steel scrap +18% YoY in 2024

- H1 2024: negative operating leverage noted

- Rapid inflation can trim margins by multiple percentage points

Moderate Scale Compared to Global Giants

Tubos Reunidos is smaller than global steel-tube giants—2024 revenue ~€600m vs. ArcelorMittal’s €50bn—so it has weaker supplier bargaining and R&D budget, limiting scale advantages.

This size forces a niche focus on industrial and oil & gas tubes, but exposes TR to aggressive price cuts by larger players with deeper capacity and cash reserves.

- 2024 revenue ~€600m vs. peers’ multibillion scale

- Smaller R&D spend per revenue, less tech leverage

- Higher vulnerability to price competition

High EU energy risk, volatile tubular demand and North America concentration threaten margins

Weaknesses: high exposure to EU energy swings (power +20–30% vs 2019; 2022 spike cut EBITDA), volatile tubular demand tied to E&P capex (2020 sales -28% to €293m; 2024 revenue ~€600m), input-cost sensitivity (steel scrap +18% YoY 2024; H1 2024 negative operating leverage), North America concentration (48% exports 2024) and smaller scale vs peers.

| Metric | 2024 |

|---|---|

| Revenue | ~€600m |

| Exports to N.A. | 48% |

| Steel scrap YoY | +18% |

| 2020 sales | €293m (-28%) |

Preview the Actual Deliverable

Tubos Reunidos SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the entire, editable version is unlocked and ready to download. You’re viewing a live excerpt of the real file, structured for immediate use in strategic planning or valuation. Buy now to access the complete, detailed report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Tubos Reunidos shows resilience through technical know-how and diversified steel tube offerings, but faces cyclicality, raw-material exposure, and competitive pressure that could limit margin recovery.

Discover the full SWOT analysis for a detailed, research-backed breakdown, editable Word and Excel deliverables, and actionable strategies to inform investment, competitive positioning, or operational planning—available instantly for purchase.

Strengths

Specialized High-Value Product Portfolio

Tubos Reunidos focuses on high-performance seamless steel tubes for energy and petrochemicals, with premium hot-finished and cold-drawn lines accounting for roughly 68% of 2024 sales, boosting average selling prices 22% above commodity peers. This specialization supports higher margins (EBITDA margin 11.5% in 2024) and long-term contracts with blue-chip clients like Repsol and TotalEnergies, strengthening pricing power and repeat-orders.

Successful Financial Restructuring and Debt Profile

By end-2025 Tubos Reunidos cut net debt to €48m from €210m in 2022 after SEPI (Sociedad Estatal de Participaciones Industriales) support and restructuring, lifting net-debt/EBITDA to 0.9x versus 3.8x in 2022 and restoring investor confidence.

Improved cash flow funded €25m capex plan for 2026 and reduced interest expense by €12m yearly, giving the firm greater resilience across steel-cycle downturns than in the prior decade.

Advanced Technological and Operational Efficiency

Integration of electric arc furnace (EAF) technology cut Tubos Reunidos’ CO2 intensity by about 40% vs blast-furnace peers, supporting 2024 scope-1 reductions and aligning with EU ETS targets; EAFs also reduced energy cost per tonne by ~18%, improving 2024 gross margin by an estimated 120 bps. EAFs enable flexible batch production, meeting varied specifications for oil & gas and mechanical engineering exports. This tech keeps unit costs competitive while easing compliance with tighter EU carbon caps and customer decarbonization specs.

Strong Global Export Footprint

Tubos Reunidos generates roughly 60% of 2024 revenue from outside Spain, with strong sales in North America and the Middle East, boosting resilience against regional downturns.

Geographic diversification lets the company tap diverse energy-market growth—oil & gas, power, and hydrogen—reducing revenue volatility and improving order visibility.

Established distribution and local technical teams ensure on-time delivery and field support for large projects, cutting implementation delays and warranty costs.

- ~60% 2024 revenue from international markets

- Key markets: North America, Middle East

- Distribution + local tech support = faster delivery

- Reduces regional demand risk, increases order visibility

Commitment to Decarbonization and ESG Standards

Tubos Reunidos has made decarbonization central to its strategy, targeting a 35% CO2 intensity reduction by 2030 and adopting circular-economy steps like 60% recycled steel feed by 2025, which strengthened ESG credentials and cut energy costs 8% in 2024.

By end-2025 those credentials attracted institutional investors (ESG funds now ~12% of free float) and met large buyers’ green procurement rules, giving Tubos a clear edge in a high-carbon sector.

- 35% CO2 intensity cut target by 2030

- 60% recycled steel feed by 2025

- 8% lower energy cost in 2024

- ESG funds ≈12% of free float by 2025

High-value tube niche boosts margins, cuts debt and CO2—global growth & ESG traction

Strong niche in high-value seamless tubes (68% of 2024 sales) drove 22% higher ASPs and 11.5% EBITDA margin in 2024; net debt cut to €48m by end-2025 (net-debt/EBITDA 0.9x). EAF adoption cut CO2 intensity ~40% vs blast-furnace peers, saved ~18% energy cost per tonne, and raised ESG funds to ~12% of free float. ~60% 2024 revenue international, key markets North America and Middle East.

| Metric | 2024/End-2025 |

|---|---|

| High-value sales | 68% of 2024 sales |

| EBITDA margin | 11.5% (2024) |

| Net debt | €48m (end-2025) |

| Net-debt/EBITDA | 0.9x (end-2025) |

| CO2 intensity cut vs peers | ~40% |

| Energy cost/tonne | ~18% lower |

| International revenue | ~60% (2024) |

| ESG funds | ~12% of free float (2025) |

What is included in the product

Provides a concise SWOT overview of Tubos Reunidos, highlighting its operational strengths and weaknesses alongside market opportunities and external threats shaping its strategic outlook.

Provides a clear, compact SWOT summary of Tubos Reunidos to speed strategic alignment and support rapid stakeholder briefings.

Weaknesses

Susceptibility to Energy Price Fluctuations

As an energy‑intensive steel-tube maker, Tubos Reunidos faces high exposure to EU electricity and natural gas swings; European industrial power prices rose ~45% year‑on‑year in 2022 and remain 20–30% above 2019 levels, which can quickly erase margins. Despite €25m–€40m annual efficiency savings since 2020, sudden spikes (e.g., 2022 peaks) disrupted forecasts and pushed EBITDA margins down. Long-term hedges cover only portions of consumption, leaving structural cost instability hard to eliminate.

Exposure to Cyclical Industry Trends

Demand for seamless tubes at Tubos Reunidos is tightly tied to oil, gas and power capex cycles; global oil prices fell ~45% in 2020 and capex returned slowly, cutting tubulars orders and causing 2020 group sales to drop 28% to €293m.

When Brent drops, exploration activity falls and order volumes decline; in 2024 E&P capex remained ~15% below 2019 levels, keeping tubular demand volatile and hurting consistent year-over-year growth.

This cyclicality forces cautious inventory and working-capital management—emptying backlogs fast raises stock-out risk, while excess inventory ties up the €100m+ yearly procurement spend and compresses margins.

Concentration Risk in Specific Export Markets

While Tubos Reunidos has global sales, 48% of 2024 exports went to North America, creating concentration risk if USMCA shifts or US tariff moves occur.

New tariffs or protectionist steps could cut margins and sales; a 5% tariff on steel pipes would erase roughly €12–18m in annual EBITDA based on 2024 margins.

Diversifying clients remains urgent; management aims to reduce North American share below 35% over three years, but execution and new commercial wins are still pending.

Operational Sensitivity to Raw Material Costs

The company’s EBITDA is highly sensitive to steel scrap and alloy prices used in its electric-arc furnaces; steel scrap rose ~18% year-on-year in 2024, squeezing margins when prices spike.

Global scrap volatility means input costs can jump before contract prices adjust, creating margin pressure—Tubos Reunidos reported negative operating leverage in H1 2024 during a raw-materials surge.

Lagged cost recovery during rapid commodity inflation can cut operating margins by several percentage points within quarters.

- Steel scrap +18% YoY in 2024

- H1 2024: negative operating leverage noted

- Rapid inflation can trim margins by multiple percentage points

Moderate Scale Compared to Global Giants

Tubos Reunidos is smaller than global steel-tube giants—2024 revenue ~€600m vs. ArcelorMittal’s €50bn—so it has weaker supplier bargaining and R&D budget, limiting scale advantages.

This size forces a niche focus on industrial and oil & gas tubes, but exposes TR to aggressive price cuts by larger players with deeper capacity and cash reserves.

- 2024 revenue ~€600m vs. peers’ multibillion scale

- Smaller R&D spend per revenue, less tech leverage

- Higher vulnerability to price competition

High EU energy risk, volatile tubular demand and North America concentration threaten margins

Weaknesses: high exposure to EU energy swings (power +20–30% vs 2019; 2022 spike cut EBITDA), volatile tubular demand tied to E&P capex (2020 sales -28% to €293m; 2024 revenue ~€600m), input-cost sensitivity (steel scrap +18% YoY 2024; H1 2024 negative operating leverage), North America concentration (48% exports 2024) and smaller scale vs peers.

| Metric | 2024 |

|---|---|

| Revenue | ~€600m |

| Exports to N.A. | 48% |

| Steel scrap YoY | +18% |

| 2020 sales | €293m (-28%) |

Preview the Actual Deliverable

Tubos Reunidos SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the entire, editable version is unlocked and ready to download. You’re viewing a live excerpt of the real file, structured for immediate use in strategic planning or valuation. Buy now to access the complete, detailed report.