TUI Boston Consulting Group Matrix

Download Your Competitive Advantage

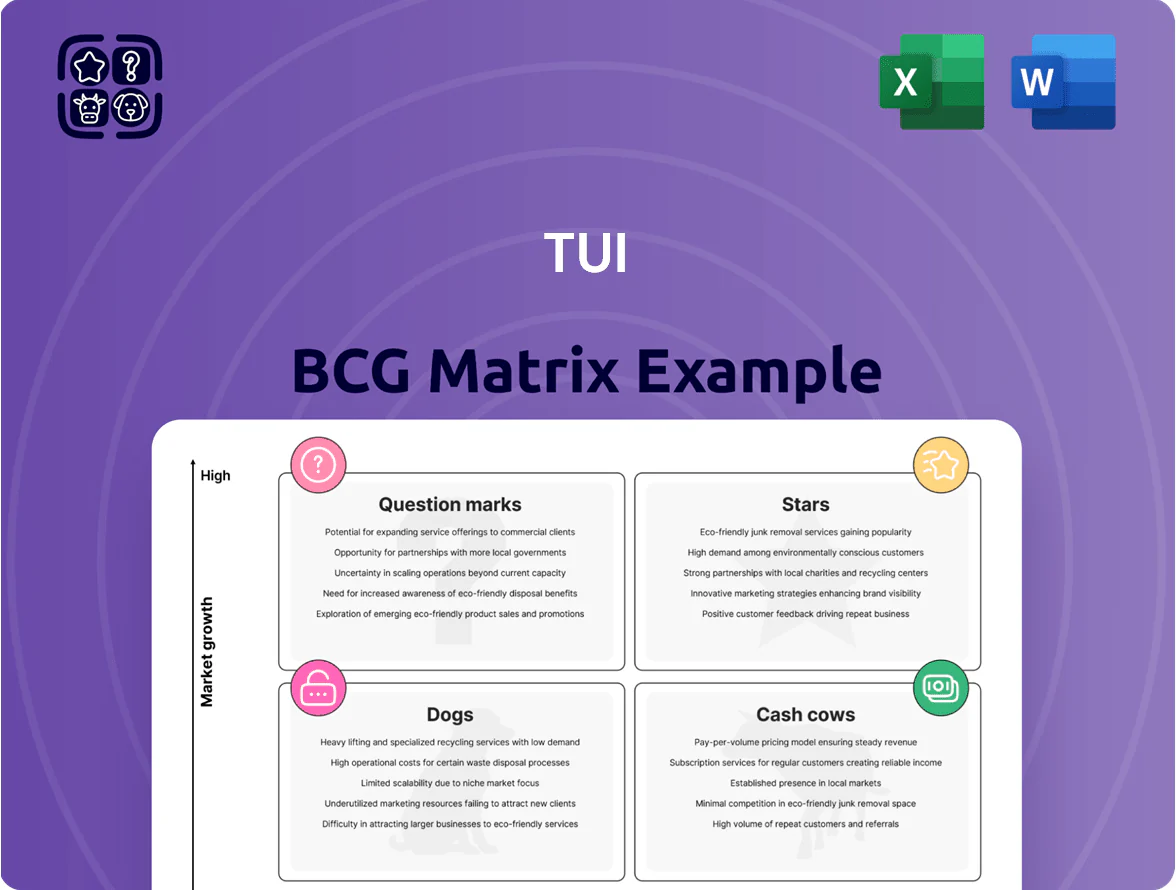

TUI’s BCG Matrix preview highlights how its core travel segments map across market growth and relative share—spotting potential Stars in niche experiential travel, Cash Cows in established package holidays, and areas at risk of becoming Dogs. This snapshot teases strategic shifts in pricing, capacity, and digital investment that could reshape long-term returns. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-driven recommendations, and deliverables in Word and Excel to act on immediately.

Stars

TUI Musement Experiences

TUI Musement Experiences is a star in TUI’s BCG matrix: by end-2025 it led global online tours & activities with ~€1.1bn GMV and ~€420m revenue, growing ~28% YoY. Significant capex and OPEX continue to flow—TUI allocated ~€150m in 2025 for tech scaling and inventory partnerships—so it consumes cash while outgrowing peers. It drives digital transformation and long-term engagement via personalized offers and repeat-booking uplift.

Mein Schiff Fleet Expansion

TUI Cruises, the TUI AG–Royal Caribbean joint venture, expanded with modern ships like Mein Schiff Relax (delivered 2023) to meet premium demand; the German-speaking cruise segment held ~40% share of regional bookings in 2024 and grew ~6% CAGR 2021–2024, continuing robustly into 2025.

These new ships need large capex—ships cost ~€600–900m each—yet achieve >90% occupancy and command ~20–30% premium fares versus mainstream lines, pushing them toward cash cow status as capex amortizes.

Maintaining Mein Schiff lines is essential for TUI’s luxury positioning and competitive edge in the German market, supporting margin expansion and higher yield per passenger through 2025.

Lifestyle Hotel Brands

Stars: Lifestyle Hotel Brands like TUI Blue have rapidly expanded into 20+ new destinations by 2025 to capture younger, lifestyle-focused travelers, driving segment revenue growth of ~28% YoY and rising market share in the boutique hotel niche.

High marketing and development spend—about €120–150m cumulative 2023–2025—keeps customer acquisition costs elevated while competing with established chains; ROI targets aim for EBITDA margins >18% within 3–5 years.

These hotels are central to TUI’s shift to an asset-right, brand-heavy model, where franchising and management contracts now comprise ~60% of the hotel portfolio to scale brand presence with lower capital outlay.

Dynamic Packaging Technology

Dynamic Packaging Technology: TUI’s shift to flexible, real-time holiday assembly captured roughly 28% of the independent traveler market by 2024 and is growing at ~22% CAGR vs 3% for pre-packaged tours to 2025, driven by on-demand customization.

Maintaining leadership requires heavy capex—TUI invested about €180m in cloud and AI from 2022–2024—and ongoing spend to optimize dynamic pricing and inventory allocation.

The platform bridges traditional tour operating and OTAs, increasing average booking value by ~14% and reducing time-to-book by 40% vs legacy systems.

- 28% market share (2024)

- ~22% CAGR to 2025 vs 3%

- €180m cloud/AI spend (2022–24)

- +14% booking value, −40% booking time

Sustainability-Certified Resorts

TUI’s Sustainability-Certified Resorts are high-growth Stars: certified properties grew 35% from 2022–2024 and achieved average room-rate premiums of ~18% in 2024, driven by rising eco-conscious demand.

These resorts attract higher occupancy (2024 avg 78% vs group 64%) and higher ancillary spend, so ongoing investment in green certifications and renewables is required to meet tightening EU and UN-aligned rules.

This segment positions TUI as a leader in the hospitality green transition and targets further margin expansion as global sustainable travel grows ~12% CAGR to 2028.

- 35% portfolio growth (2022–24)

- 18% avg rate premium (2024)

- 78% occupancy vs 64% group (2024)

- 12% projected sustainable travel CAGR to 2028

TUI Stars 2025: High-growth Musement & Cruises drive premium returns and strong occupancy

TUI Stars (2025): leading segments—Musement (€1.1bn GMV; €420m rev; +28% YoY), Cruises (40% DE share; >90% occ; 20–30% fare premium), Lifestyle hotels (+28% YoY; 20+ destinations), Dynamic packaging (28% market share; ~22% CAGR), Sustainable resorts (35% growth; 78% occ; +18% rate). Capex/Opex 2022–25: tech €180m, Musement €150m, hotels €120–150m.

| Segment | Key 2025 | Metric |

|---|---|---|

| Musement | €1.1bn GMV | +28% YoY |

| Cruises | >90% occ | 20–30% premium |

What is included in the product

Comprehensive BCG Matrix review of TUI’s units with strategic actions—invest, hold, or divest—plus threats and trend context per quadrant

One-page TUI BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

RIU Hotels and Resorts

RIU Hotels and Resorts is TUI’s cash cow, delivering steady EBITDA margins around 28% in 2024 and contributing roughly €420m in operating profit to TUI that year, reflecting mature market leadership in sun-and-beach destinations.

The brand holds dominant share in Spain and Caribbean resorts with repeat-booking rates above 65%, generating high brand loyalty and predictable occupancy of ~78% in 2024.

RIU needs minimal incremental capex versus returns—group capex per bed under RIU ~€1,200 in 2024—so excess cash frequently funds Stars and Question Marks across TUI’s portfolio.

Traditional Package Tours

The core business of selling integrated holiday packages in Europe is a mature segment where TUI (TUI Group SE) holds a leading market share—around 20–25% in key markets in 2024—delivering low growth but high operating margins (EBIT margin ~8–10% in 2024) thanks to decades of scale and yield management.

Operational efficiency generates steady free cash flow (TUI reported €1.2bn FCF in FY 2023/24), which funds net debt reduction (net debt ~€2.6bn mid‑2024) and digital investments to compete with fragmented online rivals.

This unit remains the bedrock of TUI’s brand and liquidity, underwriting strategic shifts while facing pressure from online disintermediation and younger travelers preferring bespoke options.

Robinson Club Resorts

Robinson Club Resorts leads the premium club holiday segment in the DACH region, with repeat rates around 60–65% and average occupancy >85% in 2024, making it a market leader.

It sits in a mature, low-marketing-cost market; promotional spend below 3% of revenue sustains occupancy and margins.

Consistent EBITDA margins (~22% in FY2024) generate steady cash flows that subsidize TUI Group’s broader operations.

Central European Market Dominance

TUI’s market share in Germany and neighbors—around 30–35% of European package-tour revenue in 2024—creates steady, low-growth cash flows from a saturated market with ~1–2% annual volume growth.

Established infrastructure and strong brand recall yield high margin and operational efficiency; maintenance capex (~1–2% of regional revenue) preserves position versus minor rivals.

This segment funds expansion: surplus cash supported TUI’s 2023–24 emerging-market investments and covers working capital for new routes and partnerships.

- Stable cash generator: ~30–35% regional share (2024)

- Low growth: ~1–2% annual volume growth

- Maintenance capex ~1–2% regional revenue

- Primary funding source for emerging-market expansion

TUI Airline Operations

TUI Airline Operations primarily serves TUI Group tour customers, sustaining high load factors (circa 85–90% in 2024) and stable internal demand, so it acts as a cash cow within the BCG matrix.

Operating in a mature European market, the unit prioritizes cost efficiency and route optimization to support package holidays rather than pursuing standalone expansion, delivering steady free cash flow (estimated €300–450m annual pre-tax in 2023–24 range).

Close integration with TUI hotels and cruises reduces external marketing spend for flight-only seats and improves yield management, minimizing volatility and capital needs.

- High load factors ~85–90% (2024)

- Supports package margins, not standalone growth

- Estimated free cash flow €300–450m (2023–24)

- Route optimization + hotel/cruise integration cuts marketing costs

TUI's RIU, Robinson & Airlines drove €1.2bn FCF, slashing net debt to ~€2.6bn

TUI cash cows (RIU, Robinson, Airlines) delivered steady high margins and cash: RIU EBITDA ~28% (€420m OP 2024), Robinson EBITDA ~22% (occupancy >85%), Airlines load factor ~85–90% (FCF €300–450m 2023–24); together they funded €1.2bn FCF (FY2023/24) and cut net debt to ~€2.6bn mid‑2024.

| Unit | Key metric 2024 |

|---|---|

| RIU | EBITDA 28%, €420m OP |

| Robinson | EBITDA 22%, occ >85% |

| Airlines | LF 85–90%, FCF €300–450m |

Preview = Final Product

TUI BCG Matrix

The file you're previewing is the exact TUI BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted strategic analysis tailored for clarity and decision-making.

This preview mirrors the final deliverable: a market-informed BCG Matrix with precise positioning, actionable insights, and clean visuals, ready for immediate use in presentations or planning.

Upon purchase you’ll get the same editable document sent directly to your inbox—no surprises, no extra edits required.

Designed by strategy professionals, the report is print-ready and structured to integrate seamlessly into your business reviews, investor decks, or client reports.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

TUI’s BCG Matrix preview highlights how its core travel segments map across market growth and relative share—spotting potential Stars in niche experiential travel, Cash Cows in established package holidays, and areas at risk of becoming Dogs. This snapshot teases strategic shifts in pricing, capacity, and digital investment that could reshape long-term returns. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-driven recommendations, and deliverables in Word and Excel to act on immediately.

Stars

TUI Musement Experiences

TUI Musement Experiences is a star in TUI’s BCG matrix: by end-2025 it led global online tours & activities with ~€1.1bn GMV and ~€420m revenue, growing ~28% YoY. Significant capex and OPEX continue to flow—TUI allocated ~€150m in 2025 for tech scaling and inventory partnerships—so it consumes cash while outgrowing peers. It drives digital transformation and long-term engagement via personalized offers and repeat-booking uplift.

Mein Schiff Fleet Expansion

TUI Cruises, the TUI AG–Royal Caribbean joint venture, expanded with modern ships like Mein Schiff Relax (delivered 2023) to meet premium demand; the German-speaking cruise segment held ~40% share of regional bookings in 2024 and grew ~6% CAGR 2021–2024, continuing robustly into 2025.

These new ships need large capex—ships cost ~€600–900m each—yet achieve >90% occupancy and command ~20–30% premium fares versus mainstream lines, pushing them toward cash cow status as capex amortizes.

Maintaining Mein Schiff lines is essential for TUI’s luxury positioning and competitive edge in the German market, supporting margin expansion and higher yield per passenger through 2025.

Lifestyle Hotel Brands

Stars: Lifestyle Hotel Brands like TUI Blue have rapidly expanded into 20+ new destinations by 2025 to capture younger, lifestyle-focused travelers, driving segment revenue growth of ~28% YoY and rising market share in the boutique hotel niche.

High marketing and development spend—about €120–150m cumulative 2023–2025—keeps customer acquisition costs elevated while competing with established chains; ROI targets aim for EBITDA margins >18% within 3–5 years.

These hotels are central to TUI’s shift to an asset-right, brand-heavy model, where franchising and management contracts now comprise ~60% of the hotel portfolio to scale brand presence with lower capital outlay.

Dynamic Packaging Technology

Dynamic Packaging Technology: TUI’s shift to flexible, real-time holiday assembly captured roughly 28% of the independent traveler market by 2024 and is growing at ~22% CAGR vs 3% for pre-packaged tours to 2025, driven by on-demand customization.

Maintaining leadership requires heavy capex—TUI invested about €180m in cloud and AI from 2022–2024—and ongoing spend to optimize dynamic pricing and inventory allocation.

The platform bridges traditional tour operating and OTAs, increasing average booking value by ~14% and reducing time-to-book by 40% vs legacy systems.

- 28% market share (2024)

- ~22% CAGR to 2025 vs 3%

- €180m cloud/AI spend (2022–24)

- +14% booking value, −40% booking time

Sustainability-Certified Resorts

TUI’s Sustainability-Certified Resorts are high-growth Stars: certified properties grew 35% from 2022–2024 and achieved average room-rate premiums of ~18% in 2024, driven by rising eco-conscious demand.

These resorts attract higher occupancy (2024 avg 78% vs group 64%) and higher ancillary spend, so ongoing investment in green certifications and renewables is required to meet tightening EU and UN-aligned rules.

This segment positions TUI as a leader in the hospitality green transition and targets further margin expansion as global sustainable travel grows ~12% CAGR to 2028.

- 35% portfolio growth (2022–24)

- 18% avg rate premium (2024)

- 78% occupancy vs 64% group (2024)

- 12% projected sustainable travel CAGR to 2028

TUI Stars 2025: High-growth Musement & Cruises drive premium returns and strong occupancy

TUI Stars (2025): leading segments—Musement (€1.1bn GMV; €420m rev; +28% YoY), Cruises (40% DE share; >90% occ; 20–30% fare premium), Lifestyle hotels (+28% YoY; 20+ destinations), Dynamic packaging (28% market share; ~22% CAGR), Sustainable resorts (35% growth; 78% occ; +18% rate). Capex/Opex 2022–25: tech €180m, Musement €150m, hotels €120–150m.

| Segment | Key 2025 | Metric |

|---|---|---|

| Musement | €1.1bn GMV | +28% YoY |

| Cruises | >90% occ | 20–30% premium |

What is included in the product

Comprehensive BCG Matrix review of TUI’s units with strategic actions—invest, hold, or divest—plus threats and trend context per quadrant

One-page TUI BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

RIU Hotels and Resorts

RIU Hotels and Resorts is TUI’s cash cow, delivering steady EBITDA margins around 28% in 2024 and contributing roughly €420m in operating profit to TUI that year, reflecting mature market leadership in sun-and-beach destinations.

The brand holds dominant share in Spain and Caribbean resorts with repeat-booking rates above 65%, generating high brand loyalty and predictable occupancy of ~78% in 2024.

RIU needs minimal incremental capex versus returns—group capex per bed under RIU ~€1,200 in 2024—so excess cash frequently funds Stars and Question Marks across TUI’s portfolio.

Traditional Package Tours

The core business of selling integrated holiday packages in Europe is a mature segment where TUI (TUI Group SE) holds a leading market share—around 20–25% in key markets in 2024—delivering low growth but high operating margins (EBIT margin ~8–10% in 2024) thanks to decades of scale and yield management.

Operational efficiency generates steady free cash flow (TUI reported €1.2bn FCF in FY 2023/24), which funds net debt reduction (net debt ~€2.6bn mid‑2024) and digital investments to compete with fragmented online rivals.

This unit remains the bedrock of TUI’s brand and liquidity, underwriting strategic shifts while facing pressure from online disintermediation and younger travelers preferring bespoke options.

Robinson Club Resorts

Robinson Club Resorts leads the premium club holiday segment in the DACH region, with repeat rates around 60–65% and average occupancy >85% in 2024, making it a market leader.

It sits in a mature, low-marketing-cost market; promotional spend below 3% of revenue sustains occupancy and margins.

Consistent EBITDA margins (~22% in FY2024) generate steady cash flows that subsidize TUI Group’s broader operations.

Central European Market Dominance

TUI’s market share in Germany and neighbors—around 30–35% of European package-tour revenue in 2024—creates steady, low-growth cash flows from a saturated market with ~1–2% annual volume growth.

Established infrastructure and strong brand recall yield high margin and operational efficiency; maintenance capex (~1–2% of regional revenue) preserves position versus minor rivals.

This segment funds expansion: surplus cash supported TUI’s 2023–24 emerging-market investments and covers working capital for new routes and partnerships.

- Stable cash generator: ~30–35% regional share (2024)

- Low growth: ~1–2% annual volume growth

- Maintenance capex ~1–2% regional revenue

- Primary funding source for emerging-market expansion

TUI Airline Operations

TUI Airline Operations primarily serves TUI Group tour customers, sustaining high load factors (circa 85–90% in 2024) and stable internal demand, so it acts as a cash cow within the BCG matrix.

Operating in a mature European market, the unit prioritizes cost efficiency and route optimization to support package holidays rather than pursuing standalone expansion, delivering steady free cash flow (estimated €300–450m annual pre-tax in 2023–24 range).

Close integration with TUI hotels and cruises reduces external marketing spend for flight-only seats and improves yield management, minimizing volatility and capital needs.

- High load factors ~85–90% (2024)

- Supports package margins, not standalone growth

- Estimated free cash flow €300–450m (2023–24)

- Route optimization + hotel/cruise integration cuts marketing costs

TUI's RIU, Robinson & Airlines drove €1.2bn FCF, slashing net debt to ~€2.6bn

TUI cash cows (RIU, Robinson, Airlines) delivered steady high margins and cash: RIU EBITDA ~28% (€420m OP 2024), Robinson EBITDA ~22% (occupancy >85%), Airlines load factor ~85–90% (FCF €300–450m 2023–24); together they funded €1.2bn FCF (FY2023/24) and cut net debt to ~€2.6bn mid‑2024.

| Unit | Key metric 2024 |

|---|---|

| RIU | EBITDA 28%, €420m OP |

| Robinson | EBITDA 22%, occ >85% |

| Airlines | LF 85–90%, FCF €300–450m |

Preview = Final Product

TUI BCG Matrix

The file you're previewing is the exact TUI BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted strategic analysis tailored for clarity and decision-making.

This preview mirrors the final deliverable: a market-informed BCG Matrix with precise positioning, actionable insights, and clean visuals, ready for immediate use in presentations or planning.

Upon purchase you’ll get the same editable document sent directly to your inbox—no surprises, no extra edits required.

Designed by strategy professionals, the report is print-ready and structured to integrate seamlessly into your business reviews, investor decks, or client reports.