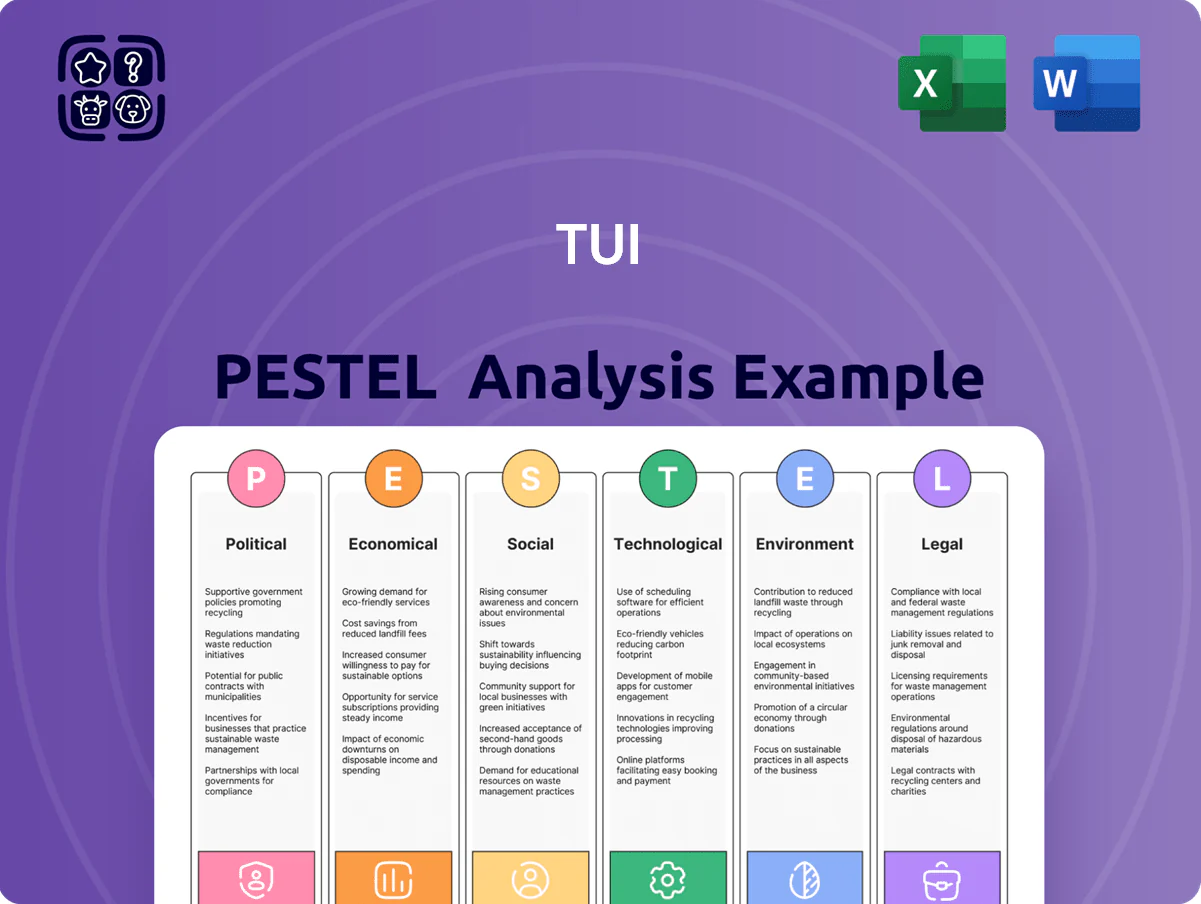

TUI PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic cycles, and emerging tech shape TUI’s prospects with our concise PESTLE snapshot—perfect for investors and strategists seeking clarity fast; purchase the full analysis for detailed, actionable insights you can apply to forecasts and strategic plans.

Political factors

Geopolitical stability in key Mediterranean and Middle Eastern markets

TUI Group remains highly sensitive to regional conflicts in Egypt, Turkey and North Africa; these markets accounted for about 18% of summer 2024 bednights and 12% of Mediterranean flight capacity, so disruptions materially hit revenue.

As of late 2025 the company must keep flexible capacity management—TUI reported a 9% contingency uplift in charter flexibility and €120m liquidity buffer in 2024—to reroute operations away from high‑risk zones.

Analysts monitor political shifts closely because a 1–3 week disruption in key markets historically reduces TUI’s quarterly EBITDA by up to 6–8% due to integrated hotel and flight exposure.

Post-Brexit regulatory alignment and UK-EU travel relations

Post-Brexit UK-EU relations shape TUI’s largest markets via visa rules and aviation agreements; in 2024 UK tourists accounted for ~22% of TUI Group bookings, making smooth cross-border travel critical.

Negotiations on border controls and seasonal worker mobility impact staffing costs—UK-based TUI fly and retail rely on roughly 10,000 seasonal hires, with labor-related costs rising an estimated 6% in 2023–24.

Any tightening of travel regulations or air service agreements could increase operational expenses and cancelation risks, threatening the seamless package-holiday experience that drives TUI’s ancillary revenue streams.

Government incentives and subsidies for green aviation transitions

Political pressure to decarbonize aviation has driven EU and national schemes—including the EU ReFuelEU Aviation mandate and €2.5bn EU Innovation Fund allocations—creating subsidies and SAF blending incentives that reduce TUI’s fuel-transition costs.

TUI leverages grants and tax credits to defray fleet modernization and SAF premiums, mitigating capital outlays that can exceed tens of millions per aircraft retrofit.

With EU ETS tightening and 2030/2050 targets, TUI’s profitability increasingly depends on securing public support; failure to capture available subsidies risks higher unit costs and margin pressure.

Global trade policies and visa liberalization initiatives

Global trade agreements and visa liberalization shape TUI's expansion: eased visa rules in markets like India and Indonesia, which saw 35% and 28% growth in outbound travel in 2023–24, can boost bookings and diversify TUI's customer base.

Protectionist policies or diplomatic strains raise administrative costs and limit access; for example, increased travel restrictions in 2022–23 contributed to a 7% decline in some European outbound segments and higher compliance spending.

- Visa easing in India/Indonesia → +35%/+28% outbound travel (2023–24)

- Protectionism/diplomatic tensions → −7% in affected segments (2022–23)

- Regulatory complexity increases compliance/admin costs for TUI

Public health policy and international travel protocols

In response to recent pandemics, governments increased health surveillance and emergency travel rules; 2023 WHO/IATA guidelines led 78% of EU states to enforce port health inspections affecting cruise turnarounds and hotel check-ins.

TUI must update operational standards to meet dynamic mandates—noncompliance risks abrupt suspensions that in 2021 caused industry revenue drops up to 60% in peak quarters.

Permanent coordination with WHO, ECDC and national authorities is strategic: TUI should embed real-time reporting and crisis playbooks into board oversight and CAPEX planning (0.5–1% revenue contingency recommended).

- 78% EU states adopted stricter port/airport health inspections by 2023

- 2021 industry peak-quarter revenue fell ~60% during travel bans

- Recommend 0.5–1% revenue contingency for health-response CAPEX

Geopolitics, rules & labor risks could swing quarterly EBITDA 6–8%

Political risk concentrates around MENA instability (18% summer 2024 bednights), UK‑EU travel rules (UK = ~22% bookings 2024), labor/visa shifts (≈10,000 seasonal hires; labor costs +6% 2023–24), EU decarbonization support (ReFuelEU, €2.5bn Innovation Fund) and health mandates (78% EU states port inspections 2023) — each can swing quarterly EBITDA by ~6–8% on short disruptions.

| Metric | Value |

|---|---|

| MENA share | 18% |

| UK bookings | 22% |

| Seasonal hires | ≈10,000 |

| Labour cost rise | +6% |

| EU port inspections | 78% |

What is included in the product

Explores how macro-environmental factors uniquely affect TUI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for TUI that’s easy to drop into presentations, share across teams, and adapt with region-specific notes to streamline risk discussions and strategic planning.

Economic factors

Impact of global inflation on consumer discretionary spending

Persistent global inflation—CPI running near 5% in 2024 across major EU markets—has pushed TUI to absorb higher fuel and staffing costs while facing price-sensitive customers; management reported 2024 Q3 yields up but margin pressure remains.

Luxury cruise and premium segments show resilience with average booking values rising ~8% YoY in 2024, while mass-market package holidays saw volumes soften as UK real disposable incomes fell ~2% in 2024.

TUI leverages strategic pricing and all-inclusive promotions—increasing package penetration to ~42% of bookings in 2024—to offer cost certainty and defend demand among budget-conscious travelers.

Volatility in jet fuel prices and energy costs

Fluctuations in global oil markets directly compress TUI's airline and cruise margins, forcing reliance on sophisticated fuel hedging; TUI hedged roughly 60% of projected jet fuel exposure for 2025 at an average $85/barrel, compared with spot Brent swinging between $70–$95 in 2025. As of end-2025, energy-price volatility remains a key risk that can erode benefits of high load factors—TUI reported post-hedge fuel cost per ASK up ~8% YoY in H2 2025. The group’s ability to pass costs to customers via surcharges is constrained by intense low-cost carrier competition and price sensitivity in core markets.

Exchange rate fluctuations between the Euro and British Pound

TUI’s Euro reporting makes it sensitive to EUR/GBP moves: a 10% pound depreciation versus the euro would cut translated UK operating profits materially, with UK tourism accounting for about 30% of group revenue in 2024 (€16.2bn of total €54bn reported FY2023/24 provisional figures).

Currency swings also affect contract costs for overseas hotels and suppliers priced in USD/GBP; EUR/USD volatility (±8% in 2024) drove notable margin pressure on long-haul bookings during 2024 peak season.

Treasury focuses on hedging and natural offsets; as of Dec 2024 TUI reported hedges covering roughly 65% of projected FX exposure for 2025, aiming to stabilize EBITDA conversion across currencies.

Interest rate environments and corporate debt servicing

Higher global policy rates in late 2025 — ECB deposit rate at 4.00% and BoE base rate at 5.25% — lift TUI’s weighted average cost of capital, raising interest expense on €4.2bn net debt (H1 2025) and slowing financing for aircraft and hotel capex.

Elevated rates make new lease and acquisition funding costlier, potentially delaying capital-intensive expansion; investors track TUI’s leverage (net debt/EBITDA ~6.0x H1 2025) and its credit metrics for refinancing risk and rating outlook.

- ECB rate 4.00% / BoE 5.25% (late 2025)

- TUI net debt €4.2bn; net debt/EBITDA ~6.0x (H1 2025)

- Higher financing costs slow aircraft/hotel acquisitions

- Leverage and ratings closely monitored by investors

Economic growth and middle-class expansion in emerging markets

Long-term growth for TUI ties to rising middle-class purchasing power in emerging markets; World Bank projects global middle class to reach 4.2bn by 2030, with Asia accounting for ~66% of growth, offering meaningful demand beyond Europe.

Economic stability in source markets like India (GDP growth ~7% in 2024) and Brazil (2024 GDP ~3.1%) lets TUI diversify revenue and lower dependency on mature European markets where travel demand is plateauing.

Capturing this requires targeted marketing and local brand adaptation—TUI must tailor price points and packages to local spending habits; in 2024 OTAs and local tour operators captured ~45% of bookings in APAC, signaling need for localized strategies.

- Middle-class reach: 4.2bn by 2030 (World Bank)

- High-growth markets: India ~7% GDP (2024), Brazil ~3.1% (2024)

- Local channels strong: ~45% APAC bookings via OTAs/local operators (2024)

Margins squeezed by inflation, FX and fuel; high debt amid growth from emerging middle class

Inflation, energy and FX tighten margins: 2024 CPI ~5% (EU), fuel hedged ~60% for 2025 at ~$85/bbl, post-hedge fuel/ASK +8% H2 2025; EUR sensitivity: UK = ~30% group revenue (€16.2bn of €54bn FY23/24); rates lift WACC (ECB 4.00%, BoE 5.25% late-2025), net debt €4.2bn, net debt/EBITDA ~6.0x (H1 2025); growth driven by emerging middle class (4.2bn by 2030).

| Metric | 2024/25 |

|---|---|

| CPI (EU) | ~5% |

| Fuel hedge | ~60% @$85/bbl |

| Net debt | €4.2bn |

| Net debt/EBITDA | ~6.0x |

What You See Is What You Get

TUI PESTLE Analysis

The preview shown here is the exact TUI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are identical to the file you’ll download immediately after payment.

Everything displayed is part of the final product, providing a complete, actionable PESTLE assessment for TUI.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic cycles, and emerging tech shape TUI’s prospects with our concise PESTLE snapshot—perfect for investors and strategists seeking clarity fast; purchase the full analysis for detailed, actionable insights you can apply to forecasts and strategic plans.

Political factors

Geopolitical stability in key Mediterranean and Middle Eastern markets

TUI Group remains highly sensitive to regional conflicts in Egypt, Turkey and North Africa; these markets accounted for about 18% of summer 2024 bednights and 12% of Mediterranean flight capacity, so disruptions materially hit revenue.

As of late 2025 the company must keep flexible capacity management—TUI reported a 9% contingency uplift in charter flexibility and €120m liquidity buffer in 2024—to reroute operations away from high‑risk zones.

Analysts monitor political shifts closely because a 1–3 week disruption in key markets historically reduces TUI’s quarterly EBITDA by up to 6–8% due to integrated hotel and flight exposure.

Post-Brexit regulatory alignment and UK-EU travel relations

Post-Brexit UK-EU relations shape TUI’s largest markets via visa rules and aviation agreements; in 2024 UK tourists accounted for ~22% of TUI Group bookings, making smooth cross-border travel critical.

Negotiations on border controls and seasonal worker mobility impact staffing costs—UK-based TUI fly and retail rely on roughly 10,000 seasonal hires, with labor-related costs rising an estimated 6% in 2023–24.

Any tightening of travel regulations or air service agreements could increase operational expenses and cancelation risks, threatening the seamless package-holiday experience that drives TUI’s ancillary revenue streams.

Government incentives and subsidies for green aviation transitions

Political pressure to decarbonize aviation has driven EU and national schemes—including the EU ReFuelEU Aviation mandate and €2.5bn EU Innovation Fund allocations—creating subsidies and SAF blending incentives that reduce TUI’s fuel-transition costs.

TUI leverages grants and tax credits to defray fleet modernization and SAF premiums, mitigating capital outlays that can exceed tens of millions per aircraft retrofit.

With EU ETS tightening and 2030/2050 targets, TUI’s profitability increasingly depends on securing public support; failure to capture available subsidies risks higher unit costs and margin pressure.

Global trade policies and visa liberalization initiatives

Global trade agreements and visa liberalization shape TUI's expansion: eased visa rules in markets like India and Indonesia, which saw 35% and 28% growth in outbound travel in 2023–24, can boost bookings and diversify TUI's customer base.

Protectionist policies or diplomatic strains raise administrative costs and limit access; for example, increased travel restrictions in 2022–23 contributed to a 7% decline in some European outbound segments and higher compliance spending.

- Visa easing in India/Indonesia → +35%/+28% outbound travel (2023–24)

- Protectionism/diplomatic tensions → −7% in affected segments (2022–23)

- Regulatory complexity increases compliance/admin costs for TUI

Public health policy and international travel protocols

In response to recent pandemics, governments increased health surveillance and emergency travel rules; 2023 WHO/IATA guidelines led 78% of EU states to enforce port health inspections affecting cruise turnarounds and hotel check-ins.

TUI must update operational standards to meet dynamic mandates—noncompliance risks abrupt suspensions that in 2021 caused industry revenue drops up to 60% in peak quarters.

Permanent coordination with WHO, ECDC and national authorities is strategic: TUI should embed real-time reporting and crisis playbooks into board oversight and CAPEX planning (0.5–1% revenue contingency recommended).

- 78% EU states adopted stricter port/airport health inspections by 2023

- 2021 industry peak-quarter revenue fell ~60% during travel bans

- Recommend 0.5–1% revenue contingency for health-response CAPEX

Geopolitics, rules & labor risks could swing quarterly EBITDA 6–8%

Political risk concentrates around MENA instability (18% summer 2024 bednights), UK‑EU travel rules (UK = ~22% bookings 2024), labor/visa shifts (≈10,000 seasonal hires; labor costs +6% 2023–24), EU decarbonization support (ReFuelEU, €2.5bn Innovation Fund) and health mandates (78% EU states port inspections 2023) — each can swing quarterly EBITDA by ~6–8% on short disruptions.

| Metric | Value |

|---|---|

| MENA share | 18% |

| UK bookings | 22% |

| Seasonal hires | ≈10,000 |

| Labour cost rise | +6% |

| EU port inspections | 78% |

What is included in the product

Explores how macro-environmental factors uniquely affect TUI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for TUI that’s easy to drop into presentations, share across teams, and adapt with region-specific notes to streamline risk discussions and strategic planning.

Economic factors

Impact of global inflation on consumer discretionary spending

Persistent global inflation—CPI running near 5% in 2024 across major EU markets—has pushed TUI to absorb higher fuel and staffing costs while facing price-sensitive customers; management reported 2024 Q3 yields up but margin pressure remains.

Luxury cruise and premium segments show resilience with average booking values rising ~8% YoY in 2024, while mass-market package holidays saw volumes soften as UK real disposable incomes fell ~2% in 2024.

TUI leverages strategic pricing and all-inclusive promotions—increasing package penetration to ~42% of bookings in 2024—to offer cost certainty and defend demand among budget-conscious travelers.

Volatility in jet fuel prices and energy costs

Fluctuations in global oil markets directly compress TUI's airline and cruise margins, forcing reliance on sophisticated fuel hedging; TUI hedged roughly 60% of projected jet fuel exposure for 2025 at an average $85/barrel, compared with spot Brent swinging between $70–$95 in 2025. As of end-2025, energy-price volatility remains a key risk that can erode benefits of high load factors—TUI reported post-hedge fuel cost per ASK up ~8% YoY in H2 2025. The group’s ability to pass costs to customers via surcharges is constrained by intense low-cost carrier competition and price sensitivity in core markets.

Exchange rate fluctuations between the Euro and British Pound

TUI’s Euro reporting makes it sensitive to EUR/GBP moves: a 10% pound depreciation versus the euro would cut translated UK operating profits materially, with UK tourism accounting for about 30% of group revenue in 2024 (€16.2bn of total €54bn reported FY2023/24 provisional figures).

Currency swings also affect contract costs for overseas hotels and suppliers priced in USD/GBP; EUR/USD volatility (±8% in 2024) drove notable margin pressure on long-haul bookings during 2024 peak season.

Treasury focuses on hedging and natural offsets; as of Dec 2024 TUI reported hedges covering roughly 65% of projected FX exposure for 2025, aiming to stabilize EBITDA conversion across currencies.

Interest rate environments and corporate debt servicing

Higher global policy rates in late 2025 — ECB deposit rate at 4.00% and BoE base rate at 5.25% — lift TUI’s weighted average cost of capital, raising interest expense on €4.2bn net debt (H1 2025) and slowing financing for aircraft and hotel capex.

Elevated rates make new lease and acquisition funding costlier, potentially delaying capital-intensive expansion; investors track TUI’s leverage (net debt/EBITDA ~6.0x H1 2025) and its credit metrics for refinancing risk and rating outlook.

- ECB rate 4.00% / BoE 5.25% (late 2025)

- TUI net debt €4.2bn; net debt/EBITDA ~6.0x (H1 2025)

- Higher financing costs slow aircraft/hotel acquisitions

- Leverage and ratings closely monitored by investors

Economic growth and middle-class expansion in emerging markets

Long-term growth for TUI ties to rising middle-class purchasing power in emerging markets; World Bank projects global middle class to reach 4.2bn by 2030, with Asia accounting for ~66% of growth, offering meaningful demand beyond Europe.

Economic stability in source markets like India (GDP growth ~7% in 2024) and Brazil (2024 GDP ~3.1%) lets TUI diversify revenue and lower dependency on mature European markets where travel demand is plateauing.

Capturing this requires targeted marketing and local brand adaptation—TUI must tailor price points and packages to local spending habits; in 2024 OTAs and local tour operators captured ~45% of bookings in APAC, signaling need for localized strategies.

- Middle-class reach: 4.2bn by 2030 (World Bank)

- High-growth markets: India ~7% GDP (2024), Brazil ~3.1% (2024)

- Local channels strong: ~45% APAC bookings via OTAs/local operators (2024)

Margins squeezed by inflation, FX and fuel; high debt amid growth from emerging middle class

Inflation, energy and FX tighten margins: 2024 CPI ~5% (EU), fuel hedged ~60% for 2025 at ~$85/bbl, post-hedge fuel/ASK +8% H2 2025; EUR sensitivity: UK = ~30% group revenue (€16.2bn of €54bn FY23/24); rates lift WACC (ECB 4.00%, BoE 5.25% late-2025), net debt €4.2bn, net debt/EBITDA ~6.0x (H1 2025); growth driven by emerging middle class (4.2bn by 2030).

| Metric | 2024/25 |

|---|---|

| CPI (EU) | ~5% |

| Fuel hedge | ~60% @$85/bbl |

| Net debt | €4.2bn |

| Net debt/EBITDA | ~6.0x |

What You See Is What You Get

TUI PESTLE Analysis

The preview shown here is the exact TUI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are identical to the file you’ll download immediately after payment.

Everything displayed is part of the final product, providing a complete, actionable PESTLE assessment for TUI.