Tupperware PESTLE Analysis

Skip the Research. Get the Strategy.

Get a concise PESTLE snapshot of Tupperware—highlighting regulatory pressures, shifting consumer behavior, supply-chain risks, and tech-driven opportunities that will shape near-term strategy; download the full PESTLE for a detailed, actionable roadmap and ready-to-use insights to inform investment or strategic decisions.

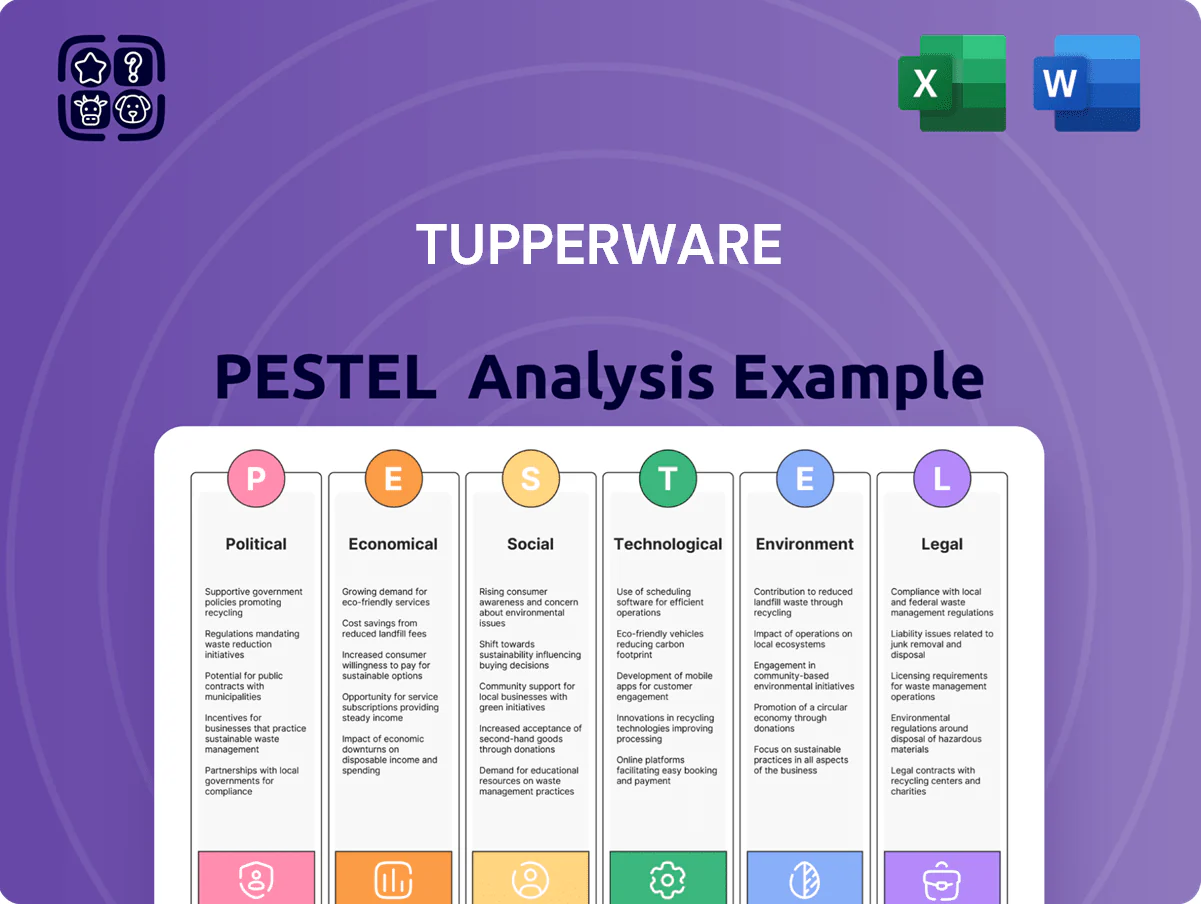

Political factors

Global Trade and Tariff Policies

Tupperware’s global manufacturing footprint in Mexico, Brazil and China exposes it to shifting trade agreements and tariffs that raised COGS by an estimated 3–6% during recent US-China and regional trade frictions; 2024 cross-border logistics accounted for roughly 18% of operating costs. Management must monitor protectionist moves—tariff hikes or import restrictions in key markets can compress margins and force price adjustments for kitchenware. Strategic sourcing and nearshoring initiatives aim to stabilize supply-chain costs and preserve competitive pricing.

Geopolitical Stability in Emerging Markets

Tupperware's heavy exposure in emerging markets—about 35% of FY2024 net sales—means political volatility can sharply disrupt direct-sales channels and logistics.

Sudden government changes or unrest have in past cases forced temporary market closures and limited movement for the ~200,000 independent representatives active in those regions.

Regularly reassessing political risk, using country-risk ratings and scenario stress-tests, is essential to protect assets and sustain projected regional growth.

Direct Selling Regulatory Oversight

Governments worldwide are tightening direct selling oversight to curb predatory practices and false earnings claims; EU member states and the US FTC increased enforcement actions 18% in 2024 versus 2022, impacting MLM disclosures.

Shifts in political leadership often bring stricter consumer protection enforcement that affects independent consultants’ recruitment and compensation rules, seen in 2023–25 rule updates across 12 jurisdictions.

Tupperware must proactively engage policymakers and trade groups to advocate clear rules distinguishing legitimate multi-level marketing from prohibited pyramid schemes to protect its salesforce and revenue streams.

Reshoring and Local Content Requirements

Reshoring trends in the US and EU—where 2024 reports show a 12–18% increase in nearshoring incentives—push Tupperware to reassess global manufacturing to protect supply-chain resilience and domestic jobs.

Local content mandates and tax credits could raise production costs but unlock subsidies; adapting footprint may preserve market access and government relationships.

- 2024 nearshoring incentive growth: 12–18%

- Potential trade-offs: higher unit costs vs. subsidies

- Strategic need: relocate/partner to meet local-content rules

Governmental Health and Safety Mandates

Governmental updates to food-grade material standards—such as EU REACH amendments and FDA guidance—force Tupperware to reformulate products; regulatory changes in 2024 affected over 12% of polymer approvals, pressuring supply chains and raising compliance costs.

Legislative bans on additives like certain phthalates require rapid production line changes, which in 2025 could add an estimated $8–12 million in retooling expenses for mid-sized manufacturers.

Proactive engagement with standards bodies and participation in three regulatory committees in 2024 allowed Tupperware-like firms to anticipate shifts, reducing recall-related losses by up to 30%.

- Regulatory-driven reformulation impacts materials, costs, and timelines

- Potential $8–12M retooling burden from additive bans

- Active committee engagement cut recall losses ≈30%

Tupperware under pressure: tariffs, nearshoring & enforcement threaten 35% EM sales

Tupperware faces tariff and nearshoring pressures (2024 cross-border logistics ≈18% of ops costs; nearshoring incentives +12–18%), regulatory shifts raising compliance/retooling costs (~$8–12M potential), and increased enforcement on direct-selling (FTC/EU actions +18% vs 2022) risking 35% FY2024 sales in emerging markets; active policy engagement and supply-chain reshaping mitigate these risks.

| Metric | 2024/25 Data |

|---|---|

| Cross-border logistics | ≈18% ops costs |

| Emerging market sales | ≈35% net sales |

| Nearshoring incentives | +12–18% |

| FTC/EU enforcement | +18% vs 2022 |

| Retooling cost estimate | $8–12M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tupperware across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise Tupperware PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline discussions on external risks, market positioning, and strategic planning.

Economic factors

Post-Restructuring Financial Stability

Post-restructuring, Tupperware emerged from Chapter 11 in late 2024 with roughly $350 million of reorganized debt and reduced annual interest expense, operating under a leaner capital structure; its ability to fund growth hinges on interest rates, where a 1% rise could add ~ $3.5 million in annual interest. Investors track 2025 trailing-12M free cash flow (reported ~$60M) and a post-exit debt-to-equity near 1.2x to gauge long-term viability.

Inflationary Pressures on Raw Materials

Rising inflation pushed global resin prices up about 18% year-over-year in 2024, with HDPE and PP costs closely tracking crude oil (Brent averaged ~$85/barrel in 2024) and natural gas volatility; for Tupperware this amplifies unit production costs and can compress margins if retail pricing is limited.

In 2024 Tupperware reported gross margin pressures amid commodity-driven cost increases, so sustained energy market volatility requires disciplined hedging and tighter inventory turnover to stabilize input costs and protect EBITDA.

Currency Exchange Rate Volatility

As Tupperware generates roughly 60% of net sales outside the US, currency exchange volatility poses material risk; a 10% strengthening of the US dollar in 2024 would cut translated revenue by about 6 percentage points, echoing Q3 2024 FX headwinds that trimmed EPS by $0.12. The firm uses hedging instruments and localized pricing—hedges covered approximately 45% of forecasted FX exposure in FY 2024—to dampen translation losses and protect margins.

Consumer Disposable Income Trends

Demand for premium kitchenware and home storage is tied to discretionary income; US real disposable personal income fell 0.4% year-over-year in 2024 Q3, pressuring premium sales for brands like Tupperware.

Economic stagnation or wage compression drives downtrading to generic alternatives; 2024 retail data showed private-label gains of 2.1% versus branded declines of 1.3%.

Monitoring unemployment (US 2025 Jan 3.7%) and consumer confidence (Conference Board 2025 Jan 99.1) is vital to forecast geographic sales volatility.

- Disposable income trends directly affect premium purchase frequency

- Downtrading risk amid wage stagnation and lower DPI

- Unemployment and consumer confidence are leading indicators for sales

Global Supply Chain and Logistics Costs

Economic shifts in shipping and freight directly affect Tupperware’s global distribution; ocean freight rates averaged about 1,200 USD/FEU in 2024 versus peak 14,000 in 2021, reducing but still volatile, influencing margin stability.

Rising fuel costs and logistics labor shortages pushed inland surcharges up ~12% in 2024 and extended lead times by 10–18%, increasing working capital needs.

Restructuring prioritizes optimizing distribution—nearshoring and consolidating hubs to cut transit distances and lower transport cost per unit by an estimated 8–15%.

- Ocean freight avg ~1,200 USD/FEU (2024)

- Inland surcharges +12% (2024)

- Lead times +10–18%

- Target transport cost reduction 8–15%

Tupperware 2024: $350M reorg debt, ~1.2x D/E, $60M FCF — cost pressures & 45% FX hedge

Tupperware’s 2024 post-exit capital structure: $350M reorganized debt, ~1.2x debt/equity, 2025 LTM FCF ~$60M; 1% rate hike ≈ $3.5M extra interest. Resin costs +18% YoY (2024), Brent ~$85/bbl; ocean freight ≈ $1,200/FEU, inland surcharges +12%, lead times +10–18%; FX hedges covered ~45% of exposure; US DPI down, consumer confidence 99.1 (Jan 2025).

| Metric | 2024/25 |

|---|---|

| Reorg debt | $350M |

| Debt/Equity | ~1.2x |

| FCF (LTM 2025) | $60M |

| Resin cost YoY | +18% |

| Brent avg | $85/bbl |

| Ocean freight | $1,200/FEU |

| FX hedge cover | ~45% |

Preview Before You Purchase

Tupperware PESTLE Analysis

The preview shown here is the exact Tupperware PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Get a concise PESTLE snapshot of Tupperware—highlighting regulatory pressures, shifting consumer behavior, supply-chain risks, and tech-driven opportunities that will shape near-term strategy; download the full PESTLE for a detailed, actionable roadmap and ready-to-use insights to inform investment or strategic decisions.

Political factors

Global Trade and Tariff Policies

Tupperware’s global manufacturing footprint in Mexico, Brazil and China exposes it to shifting trade agreements and tariffs that raised COGS by an estimated 3–6% during recent US-China and regional trade frictions; 2024 cross-border logistics accounted for roughly 18% of operating costs. Management must monitor protectionist moves—tariff hikes or import restrictions in key markets can compress margins and force price adjustments for kitchenware. Strategic sourcing and nearshoring initiatives aim to stabilize supply-chain costs and preserve competitive pricing.

Geopolitical Stability in Emerging Markets

Tupperware's heavy exposure in emerging markets—about 35% of FY2024 net sales—means political volatility can sharply disrupt direct-sales channels and logistics.

Sudden government changes or unrest have in past cases forced temporary market closures and limited movement for the ~200,000 independent representatives active in those regions.

Regularly reassessing political risk, using country-risk ratings and scenario stress-tests, is essential to protect assets and sustain projected regional growth.

Direct Selling Regulatory Oversight

Governments worldwide are tightening direct selling oversight to curb predatory practices and false earnings claims; EU member states and the US FTC increased enforcement actions 18% in 2024 versus 2022, impacting MLM disclosures.

Shifts in political leadership often bring stricter consumer protection enforcement that affects independent consultants’ recruitment and compensation rules, seen in 2023–25 rule updates across 12 jurisdictions.

Tupperware must proactively engage policymakers and trade groups to advocate clear rules distinguishing legitimate multi-level marketing from prohibited pyramid schemes to protect its salesforce and revenue streams.

Reshoring and Local Content Requirements

Reshoring trends in the US and EU—where 2024 reports show a 12–18% increase in nearshoring incentives—push Tupperware to reassess global manufacturing to protect supply-chain resilience and domestic jobs.

Local content mandates and tax credits could raise production costs but unlock subsidies; adapting footprint may preserve market access and government relationships.

- 2024 nearshoring incentive growth: 12–18%

- Potential trade-offs: higher unit costs vs. subsidies

- Strategic need: relocate/partner to meet local-content rules

Governmental Health and Safety Mandates

Governmental updates to food-grade material standards—such as EU REACH amendments and FDA guidance—force Tupperware to reformulate products; regulatory changes in 2024 affected over 12% of polymer approvals, pressuring supply chains and raising compliance costs.

Legislative bans on additives like certain phthalates require rapid production line changes, which in 2025 could add an estimated $8–12 million in retooling expenses for mid-sized manufacturers.

Proactive engagement with standards bodies and participation in three regulatory committees in 2024 allowed Tupperware-like firms to anticipate shifts, reducing recall-related losses by up to 30%.

- Regulatory-driven reformulation impacts materials, costs, and timelines

- Potential $8–12M retooling burden from additive bans

- Active committee engagement cut recall losses ≈30%

Tupperware under pressure: tariffs, nearshoring & enforcement threaten 35% EM sales

Tupperware faces tariff and nearshoring pressures (2024 cross-border logistics ≈18% of ops costs; nearshoring incentives +12–18%), regulatory shifts raising compliance/retooling costs (~$8–12M potential), and increased enforcement on direct-selling (FTC/EU actions +18% vs 2022) risking 35% FY2024 sales in emerging markets; active policy engagement and supply-chain reshaping mitigate these risks.

| Metric | 2024/25 Data |

|---|---|

| Cross-border logistics | ≈18% ops costs |

| Emerging market sales | ≈35% net sales |

| Nearshoring incentives | +12–18% |

| FTC/EU enforcement | +18% vs 2022 |

| Retooling cost estimate | $8–12M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tupperware across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise Tupperware PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline discussions on external risks, market positioning, and strategic planning.

Economic factors

Post-Restructuring Financial Stability

Post-restructuring, Tupperware emerged from Chapter 11 in late 2024 with roughly $350 million of reorganized debt and reduced annual interest expense, operating under a leaner capital structure; its ability to fund growth hinges on interest rates, where a 1% rise could add ~ $3.5 million in annual interest. Investors track 2025 trailing-12M free cash flow (reported ~$60M) and a post-exit debt-to-equity near 1.2x to gauge long-term viability.

Inflationary Pressures on Raw Materials

Rising inflation pushed global resin prices up about 18% year-over-year in 2024, with HDPE and PP costs closely tracking crude oil (Brent averaged ~$85/barrel in 2024) and natural gas volatility; for Tupperware this amplifies unit production costs and can compress margins if retail pricing is limited.

In 2024 Tupperware reported gross margin pressures amid commodity-driven cost increases, so sustained energy market volatility requires disciplined hedging and tighter inventory turnover to stabilize input costs and protect EBITDA.

Currency Exchange Rate Volatility

As Tupperware generates roughly 60% of net sales outside the US, currency exchange volatility poses material risk; a 10% strengthening of the US dollar in 2024 would cut translated revenue by about 6 percentage points, echoing Q3 2024 FX headwinds that trimmed EPS by $0.12. The firm uses hedging instruments and localized pricing—hedges covered approximately 45% of forecasted FX exposure in FY 2024—to dampen translation losses and protect margins.

Consumer Disposable Income Trends

Demand for premium kitchenware and home storage is tied to discretionary income; US real disposable personal income fell 0.4% year-over-year in 2024 Q3, pressuring premium sales for brands like Tupperware.

Economic stagnation or wage compression drives downtrading to generic alternatives; 2024 retail data showed private-label gains of 2.1% versus branded declines of 1.3%.

Monitoring unemployment (US 2025 Jan 3.7%) and consumer confidence (Conference Board 2025 Jan 99.1) is vital to forecast geographic sales volatility.

- Disposable income trends directly affect premium purchase frequency

- Downtrading risk amid wage stagnation and lower DPI

- Unemployment and consumer confidence are leading indicators for sales

Global Supply Chain and Logistics Costs

Economic shifts in shipping and freight directly affect Tupperware’s global distribution; ocean freight rates averaged about 1,200 USD/FEU in 2024 versus peak 14,000 in 2021, reducing but still volatile, influencing margin stability.

Rising fuel costs and logistics labor shortages pushed inland surcharges up ~12% in 2024 and extended lead times by 10–18%, increasing working capital needs.

Restructuring prioritizes optimizing distribution—nearshoring and consolidating hubs to cut transit distances and lower transport cost per unit by an estimated 8–15%.

- Ocean freight avg ~1,200 USD/FEU (2024)

- Inland surcharges +12% (2024)

- Lead times +10–18%

- Target transport cost reduction 8–15%

Tupperware 2024: $350M reorg debt, ~1.2x D/E, $60M FCF — cost pressures & 45% FX hedge

Tupperware’s 2024 post-exit capital structure: $350M reorganized debt, ~1.2x debt/equity, 2025 LTM FCF ~$60M; 1% rate hike ≈ $3.5M extra interest. Resin costs +18% YoY (2024), Brent ~$85/bbl; ocean freight ≈ $1,200/FEU, inland surcharges +12%, lead times +10–18%; FX hedges covered ~45% of exposure; US DPI down, consumer confidence 99.1 (Jan 2025).

| Metric | 2024/25 |

|---|---|

| Reorg debt | $350M |

| Debt/Equity | ~1.2x |

| FCF (LTM 2025) | $60M |

| Resin cost YoY | +18% |

| Brent avg | $85/bbl |

| Ocean freight | $1,200/FEU |

| FX hedge cover | ~45% |

Preview Before You Purchase

Tupperware PESTLE Analysis

The preview shown here is the exact Tupperware PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.