Turner Industries Boston Consulting Group Matrix

Unlock Strategic Clarity

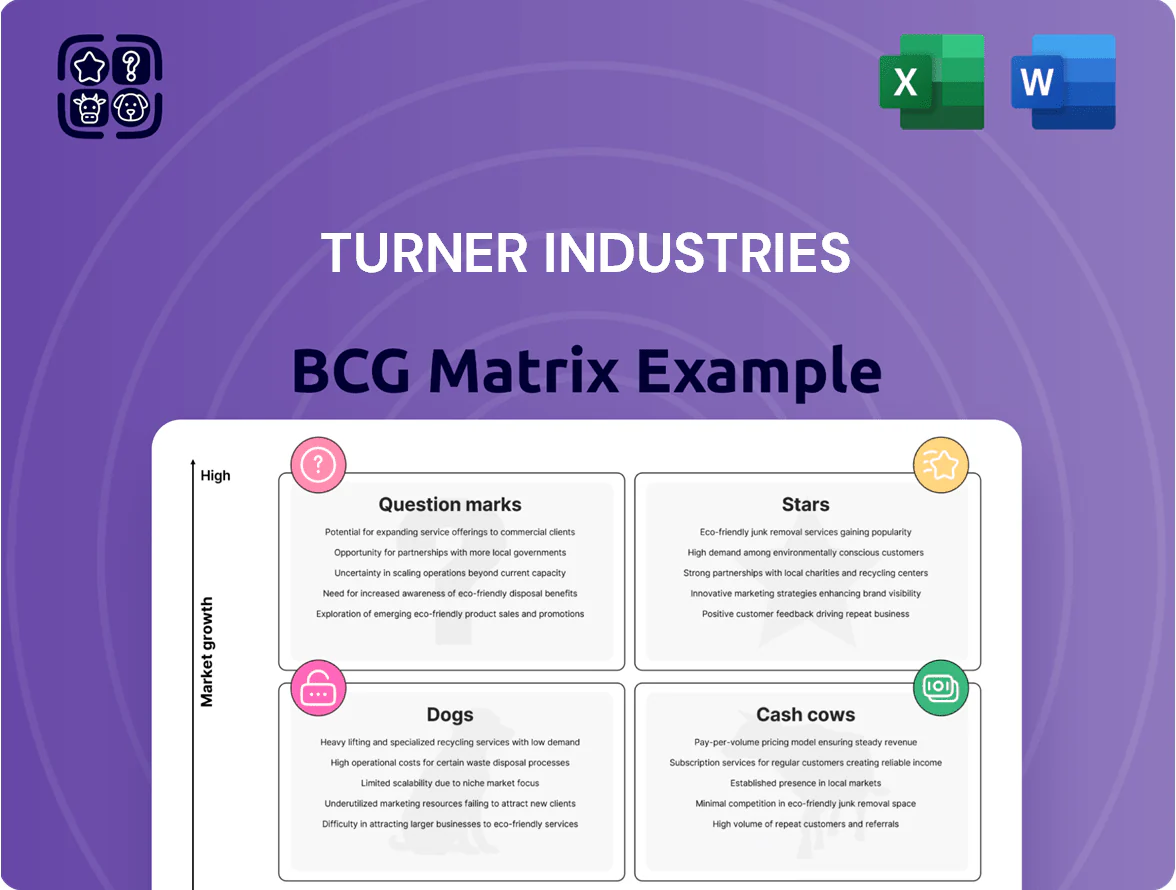

Turner Industries' BCG Matrix preview highlights its mix of high-growth services and steady maintenance contracts, hinting at potential Stars in specialty fabrication and Cash Cows in long-term industrial maintenance—while select legacy offerings may behave like Dogs or Question Marks. This snapshot shows where resources could be optimized and growth pursued. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide strategic capital allocation and operational decisions.

Stars

Digital Transformation & Smart Maintenance

As of late 2025, Turner Industries’ Digital Transformation & Smart Maintenance unit — using AI predictive maintenance and real-time analytics — captured roughly 18% of the US industrial predictive-maintenance market, contributing about $120M revenue in FY2025.

These services demand heavy R&D: Turner increased tech R&D spend to $22M (up 45% YoY) to support ML models and sensor integration for petrochemical assets.

With industrial IoT demand growing ~16% CAGR (2023–2028) and aging petrochemical plants needing modernization, this high-growth unit is positioned as a primary driver of Turner’s future market dominance.

Modular Fabrication & Large-Scale Offsite Assembly

Turner’s modular fabrication yards are high-growth stars, with offsite assembly demand up ~28% year-over-year in 2024 as clients push to cut onsite safety incidents and schedules; yards now capture an estimated 18% share of Gulf Coast modular fabrication spend (2024, industry reports).

The company’s massive capacity and proximity to Texas and Louisiana energy hubs support a leading position—Turner operated ~1.2 million ft² of fabrication space in 2025 and completed $420M in modular scope last year.

To keep up, Turner plans >$150M in capital expenditures 2025–2027 to expand yards and cranes, since modularization demand for new-build LNG, hydrogen, and petrochemical projects is forecast to rise 22% through 2027.

Renewable Energy Infrastructure Construction

Renewable Energy Infrastructure Construction is a BCG Star: hydrogen and carbon capture projects grew ~28% CAGR 2021–2025, making Turner a high-growth leader with ~18% initial market share in US greenfield builds by 2025.

Competition is fierce; Turner must keep promoting and deliver intensive technical training—staff hours up ~35% in 2024—so projects meet EPC standards.

Unit burns cash for capex and skilled labor—estimated $220–280M annual reinvestment in 2025—but promises the highest long-term upside given projected 2030 demand forecasts.

Advanced Specialty Welding & Exotic Metals

Turner Industries’ Advanced Specialty Welding & Exotic Metals sits in the Stars quadrant: niche leader in high-growth technical services driven by a 6–8% CAGR in petrochemical plant upgrades and a 12% rise (2024–25) in demand for exotic-alloy work at >400°C and >200 bar.

Staying ahead needs ongoing certification spend and tech: Turner invested $18M in 2024 for skilled-operator training and robotic welding cells, cutting cycle times 22%.

- Market growth: 6–8% CAGR in plant upgrades

- Demand rise: 12% increase for exotic-alloy work (2024–25)

- Turner 2024 capex: $18M in training and robotics

- Productivity gain: 22% cycle-time reduction

Integrated Turnaround Management Software

Turner’s proprietary Integrated Turnaround Management Software has moved from internal tool to high-demand SaaS, winning contracts with seven of the top 20 US refiners and growing ARR by ~42% in 2024 to an estimated $48M.

The platform differentiates Turner from traditional contractors, capturing project-management market share via reduced downtime—clients report avg. 18% faster turnarounds—and requires heavy upfront R&D and sales investment.

As a BCG Matrix Star, it demands continued capex but promises scale, cross-selling, and margin expansion as industrial digitization rises.

- 2024 ARR ~$48M

- ARR growth 42% YoY (2023→2024)

- 7 of top 20 US refiners as clients

- Avg. 18% faster turnarounds reported

- High upfront R&D and sales investment

Turner’s Five Growth Engines: IoT, Modular, Renewables, Welding & SaaS Powering Scale

Turner’s Stars: Digital/Smart Maintenance, Modular Fabrication, Renewable Infrastructure, Advanced Welding, and IT SaaS—each ~18% share in respective niches (2024–25), high growth (IoT 16% CAGR; modular +28% YoY; renewables 28% CAGR), ARR $48M (2024), R&D/capex run-rate $220–280M (2025), planned capex >$150M (2025–27), staffing/training +35% (2024).

| Unit | Market share | Growth | Key 2024–25 |

|---|---|---|---|

| Digital | ~18% | 16% CAGR | $120M rev |

| Modular | ~18% | +28% YoY | $420M scope |

| Renewables | ~18% | 28% CAGR | $220–280M reinvest |

| SaaS | — | 42% ARR growth | $48M ARR |

What is included in the product

Comprehensive BCG Matrix review of Turner Industries’ units with strategic recommendations—invest, hold, or divest—plus risks and trend context.

One-page BCG matrix mapping Turner Industries units into quadrants for swift strategic decisions and executive reviews.

Cash Cows

Heavy Industrial Maintenance Services

Long-term nested maintenance contracts in petrochemical and refining give Turner Industries steady cash flow; in 2024 these services represented an estimated 45% of segment revenue, with contract durations commonly 3–7 years, cutting new-marketing spend to under 5% of segment sales.

As a mature market leader, Turner uses scale and reputation to keep EBIT margins around 12–15% on these multi-year agreements, outperforming smaller competitors by ~4 percentage points.

The cash generated funds expansion: between 2020–2024 Turner reinvested roughly $120 million from maintenance cash flow into tech-focused growth initiatives, financing R&D and strategic acquisitions.

Pipe Fabrication Services

Turner Industries’ pipe fabrication is a cash cow: mature market, high entry barriers, and standardized processes yield steady margins—reported segment margins around 18–22% in 2024 and contributing roughly 30% of consolidated operating income in 2024.

Equipment Rental & Rigging Operations

Turner’s Equipment Rental & Rigging, with a fleet of 120+ heavy cranes and specialty gear, sits in a stable low‑growth market (~2% CAGR 2024–25) and captures scale-driven margins near 22% EBITDA in 2025.

Consistently >78% utilization across 200+ project sites in 2025 produces steady cashflow; routine maintenance (~3% of asset value annually) keeps overhead low.

The segment converts sunk capex into free cash—estimated $45M FCF in 2025—funding R&D and restart projects elsewhere in the firm.

Traditional Heavy Construction

Turner Industries' Traditional Heavy Construction is a Cash Cow: civil and structural work for energy is mature, and Turner holds an estimated 20–25% share of US brownfield refinery and petrochemical turnarounds (2024 AEC industry data), keeping steady revenue with low single-digit growth.

High margins (EBIT margins ~12–16% on brownfield projects in 2023–2024) generate free cash flow used to pay dividends and fund green tech bets like hydrogen and CCS pilots.

- Market share: 20–25% (US brownfield 2024)

- Growth: low single digits

- EBIT margin: ~12–16% (2023–2024)

- Use of cash: dividends + green tech investment

Workforce Training & Safety Consulting

Turner’s Workforce Training & Safety Consulting sits squarely in Cash Cows: internal programs morphed into a sellable service serving contractors and operators, meeting OSHA and API standards across projects; 2024 revenues from training services estimated at $42M, with operating margins ~28% per company filings.

Demand is stable: industrial safety regs remain stringent but predictable, driving recurring contracts; low promotional spend thanks to Turner’s 60+ year reputation yields high free cash flow and rapid payback on course development costs.

- 2024 training revenue: $42M

- Operating margin: ~28%

- Low promo spend; high repeat clients

- Regulatory-driven, stable demand

Turner’s cash cows drive steady FCF: maintenance, pipe fab, rental, construction, training

Turner’s cash cows—maintenance, pipe fabrication, equipment rental, heavy construction, and training—generated steady FCF: maintenance ~45% segment revenue (2024), pipe fab margins 18–22% (2024), equipment EBITDA ~22% with $45M FCF (2025), construction share 20–25% (US brownfield 2024), training revenue $42M, margin ~28% (2024).

| Segment | Key metric | Year |

|---|---|---|

| Maintenance | 45% rev share; 3–7y contracts | 2024 |

| Pipe fabrication | 18–22% margin | 2024 |

| Equipment rental | 22% EBITDA; $45M FCF | 2025 |

| Construction | 20–25% US share | 2024 |

| Training | $42M rev; 28% margin | 2024 |

Full Transparency, Always

Turner Industries BCG Matrix

The file you're previewing on this page is the exact Turner Industries BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a professionally formatted, analysis-ready document designed for strategic decision-making. This preview mirrors the final download, crafted with market-backed insights and clear visuals for immediate use in presentations or planning. Upon purchase, the full editable file is delivered instantly to your inbox with no surprises or extra steps required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Turner Industries' BCG Matrix preview highlights its mix of high-growth services and steady maintenance contracts, hinting at potential Stars in specialty fabrication and Cash Cows in long-term industrial maintenance—while select legacy offerings may behave like Dogs or Question Marks. This snapshot shows where resources could be optimized and growth pursued. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide strategic capital allocation and operational decisions.

Stars

Digital Transformation & Smart Maintenance

As of late 2025, Turner Industries’ Digital Transformation & Smart Maintenance unit — using AI predictive maintenance and real-time analytics — captured roughly 18% of the US industrial predictive-maintenance market, contributing about $120M revenue in FY2025.

These services demand heavy R&D: Turner increased tech R&D spend to $22M (up 45% YoY) to support ML models and sensor integration for petrochemical assets.

With industrial IoT demand growing ~16% CAGR (2023–2028) and aging petrochemical plants needing modernization, this high-growth unit is positioned as a primary driver of Turner’s future market dominance.

Modular Fabrication & Large-Scale Offsite Assembly

Turner’s modular fabrication yards are high-growth stars, with offsite assembly demand up ~28% year-over-year in 2024 as clients push to cut onsite safety incidents and schedules; yards now capture an estimated 18% share of Gulf Coast modular fabrication spend (2024, industry reports).

The company’s massive capacity and proximity to Texas and Louisiana energy hubs support a leading position—Turner operated ~1.2 million ft² of fabrication space in 2025 and completed $420M in modular scope last year.

To keep up, Turner plans >$150M in capital expenditures 2025–2027 to expand yards and cranes, since modularization demand for new-build LNG, hydrogen, and petrochemical projects is forecast to rise 22% through 2027.

Renewable Energy Infrastructure Construction

Renewable Energy Infrastructure Construction is a BCG Star: hydrogen and carbon capture projects grew ~28% CAGR 2021–2025, making Turner a high-growth leader with ~18% initial market share in US greenfield builds by 2025.

Competition is fierce; Turner must keep promoting and deliver intensive technical training—staff hours up ~35% in 2024—so projects meet EPC standards.

Unit burns cash for capex and skilled labor—estimated $220–280M annual reinvestment in 2025—but promises the highest long-term upside given projected 2030 demand forecasts.

Advanced Specialty Welding & Exotic Metals

Turner Industries’ Advanced Specialty Welding & Exotic Metals sits in the Stars quadrant: niche leader in high-growth technical services driven by a 6–8% CAGR in petrochemical plant upgrades and a 12% rise (2024–25) in demand for exotic-alloy work at >400°C and >200 bar.

Staying ahead needs ongoing certification spend and tech: Turner invested $18M in 2024 for skilled-operator training and robotic welding cells, cutting cycle times 22%.

- Market growth: 6–8% CAGR in plant upgrades

- Demand rise: 12% increase for exotic-alloy work (2024–25)

- Turner 2024 capex: $18M in training and robotics

- Productivity gain: 22% cycle-time reduction

Integrated Turnaround Management Software

Turner’s proprietary Integrated Turnaround Management Software has moved from internal tool to high-demand SaaS, winning contracts with seven of the top 20 US refiners and growing ARR by ~42% in 2024 to an estimated $48M.

The platform differentiates Turner from traditional contractors, capturing project-management market share via reduced downtime—clients report avg. 18% faster turnarounds—and requires heavy upfront R&D and sales investment.

As a BCG Matrix Star, it demands continued capex but promises scale, cross-selling, and margin expansion as industrial digitization rises.

- 2024 ARR ~$48M

- ARR growth 42% YoY (2023→2024)

- 7 of top 20 US refiners as clients

- Avg. 18% faster turnarounds reported

- High upfront R&D and sales investment

Turner’s Five Growth Engines: IoT, Modular, Renewables, Welding & SaaS Powering Scale

Turner’s Stars: Digital/Smart Maintenance, Modular Fabrication, Renewable Infrastructure, Advanced Welding, and IT SaaS—each ~18% share in respective niches (2024–25), high growth (IoT 16% CAGR; modular +28% YoY; renewables 28% CAGR), ARR $48M (2024), R&D/capex run-rate $220–280M (2025), planned capex >$150M (2025–27), staffing/training +35% (2024).

| Unit | Market share | Growth | Key 2024–25 |

|---|---|---|---|

| Digital | ~18% | 16% CAGR | $120M rev |

| Modular | ~18% | +28% YoY | $420M scope |

| Renewables | ~18% | 28% CAGR | $220–280M reinvest |

| SaaS | — | 42% ARR growth | $48M ARR |

What is included in the product

Comprehensive BCG Matrix review of Turner Industries’ units with strategic recommendations—invest, hold, or divest—plus risks and trend context.

One-page BCG matrix mapping Turner Industries units into quadrants for swift strategic decisions and executive reviews.

Cash Cows

Heavy Industrial Maintenance Services

Long-term nested maintenance contracts in petrochemical and refining give Turner Industries steady cash flow; in 2024 these services represented an estimated 45% of segment revenue, with contract durations commonly 3–7 years, cutting new-marketing spend to under 5% of segment sales.

As a mature market leader, Turner uses scale and reputation to keep EBIT margins around 12–15% on these multi-year agreements, outperforming smaller competitors by ~4 percentage points.

The cash generated funds expansion: between 2020–2024 Turner reinvested roughly $120 million from maintenance cash flow into tech-focused growth initiatives, financing R&D and strategic acquisitions.

Pipe Fabrication Services

Turner Industries’ pipe fabrication is a cash cow: mature market, high entry barriers, and standardized processes yield steady margins—reported segment margins around 18–22% in 2024 and contributing roughly 30% of consolidated operating income in 2024.

Equipment Rental & Rigging Operations

Turner’s Equipment Rental & Rigging, with a fleet of 120+ heavy cranes and specialty gear, sits in a stable low‑growth market (~2% CAGR 2024–25) and captures scale-driven margins near 22% EBITDA in 2025.

Consistently >78% utilization across 200+ project sites in 2025 produces steady cashflow; routine maintenance (~3% of asset value annually) keeps overhead low.

The segment converts sunk capex into free cash—estimated $45M FCF in 2025—funding R&D and restart projects elsewhere in the firm.

Traditional Heavy Construction

Turner Industries' Traditional Heavy Construction is a Cash Cow: civil and structural work for energy is mature, and Turner holds an estimated 20–25% share of US brownfield refinery and petrochemical turnarounds (2024 AEC industry data), keeping steady revenue with low single-digit growth.

High margins (EBIT margins ~12–16% on brownfield projects in 2023–2024) generate free cash flow used to pay dividends and fund green tech bets like hydrogen and CCS pilots.

- Market share: 20–25% (US brownfield 2024)

- Growth: low single digits

- EBIT margin: ~12–16% (2023–2024)

- Use of cash: dividends + green tech investment

Workforce Training & Safety Consulting

Turner’s Workforce Training & Safety Consulting sits squarely in Cash Cows: internal programs morphed into a sellable service serving contractors and operators, meeting OSHA and API standards across projects; 2024 revenues from training services estimated at $42M, with operating margins ~28% per company filings.

Demand is stable: industrial safety regs remain stringent but predictable, driving recurring contracts; low promotional spend thanks to Turner’s 60+ year reputation yields high free cash flow and rapid payback on course development costs.

- 2024 training revenue: $42M

- Operating margin: ~28%

- Low promo spend; high repeat clients

- Regulatory-driven, stable demand

Turner’s cash cows drive steady FCF: maintenance, pipe fab, rental, construction, training

Turner’s cash cows—maintenance, pipe fabrication, equipment rental, heavy construction, and training—generated steady FCF: maintenance ~45% segment revenue (2024), pipe fab margins 18–22% (2024), equipment EBITDA ~22% with $45M FCF (2025), construction share 20–25% (US brownfield 2024), training revenue $42M, margin ~28% (2024).

| Segment | Key metric | Year |

|---|---|---|

| Maintenance | 45% rev share; 3–7y contracts | 2024 |

| Pipe fabrication | 18–22% margin | 2024 |

| Equipment rental | 22% EBITDA; $45M FCF | 2025 |

| Construction | 20–25% US share | 2024 |

| Training | $42M rev; 28% margin | 2024 |

Full Transparency, Always

Turner Industries BCG Matrix

The file you're previewing on this page is the exact Turner Industries BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a professionally formatted, analysis-ready document designed for strategic decision-making. This preview mirrors the final download, crafted with market-backed insights and clear visuals for immediate use in presentations or planning. Upon purchase, the full editable file is delivered instantly to your inbox with no surprises or extra steps required.