TWC Boston Consulting Group Matrix

Unlock Strategic Clarity

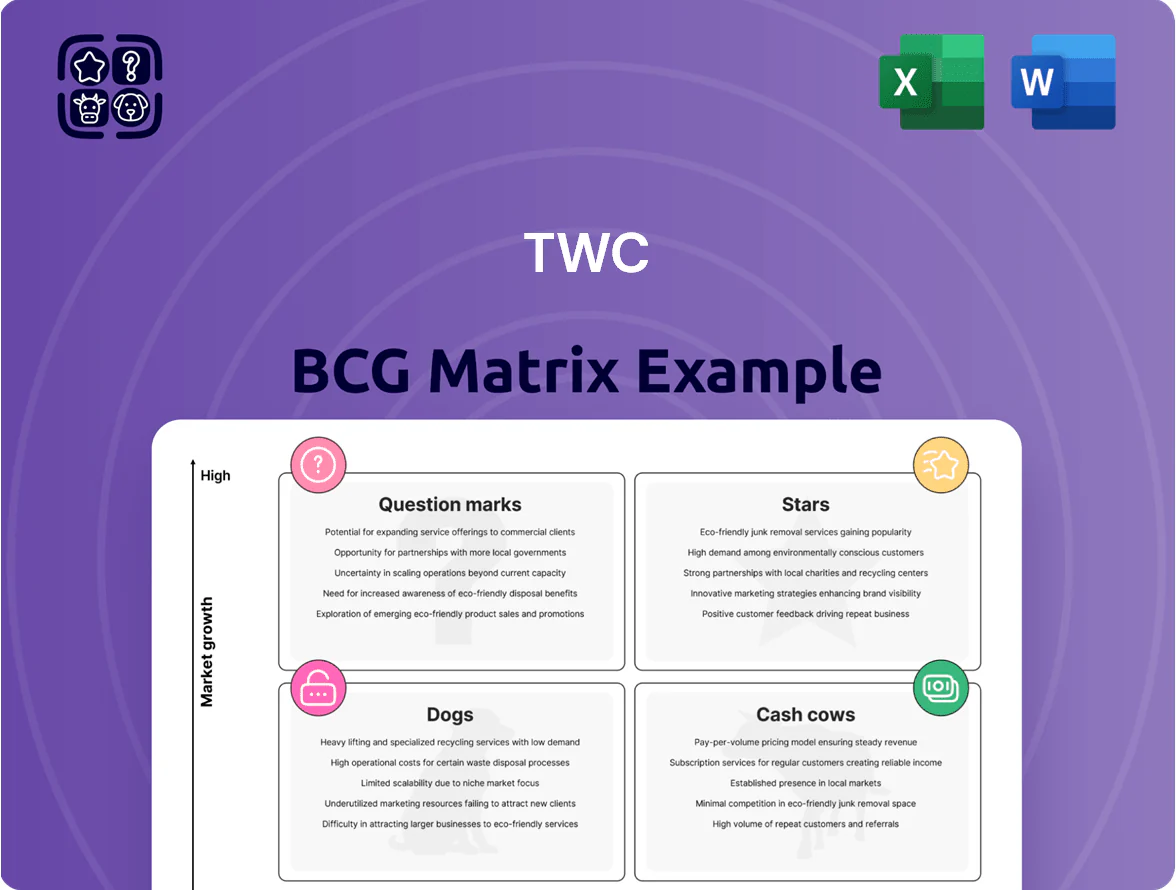

The TWC BCG Matrix snapshot shows how TWC’s offerings map across growth and market-share dynamics—highlighting potential Stars to scale, Cash Cows to harvest, Dogs to divest, and Question Marks to evaluate. This teaser outlines key movements and risk hotspots, but the full BCG Matrix gives quadrant-level data, actionable strategies, and allocation guidance tailored to TWC’s portfolio. Purchase the complete report for a ready-to-use Word analysis and Excel summary that turns insight into immediate strategic action.

Stars

Premium ClubLink Membership Growth

ClubLink’s Premium ClubLink membership expansion into high-demand urban corridors is a Star: high growth with dominant market share—urban memberships grew 28% YoY to 42,000 members by Dec 2025, capturing ~37% of Canada’s private-course urban segment.

Demand for exclusive multi-course access stays strong among affluent cohorts; average annual spend per premium member rose to CAD 6,300 in 2025, up 9% from 2024.

This segment needs heavy capital: estimated CAPEX and maintenance of CAD 75–90 million annually across flagship courses, plus CAD 12 million marketing, but it secures a leading private-golf position and premium pricing power.

Luxury Resort Residential Developments

New high-end residential projects on existing golf properties grew ~12–18% CAGR globally 2019–2024, driven by limited waterfront/golf parcels and leisure demand; transactions in 2024 averaged $1.6M–$4.2M per unit in prime U.S./Mediterranean markets.

These developments command 20–45% price premiums versus non-leisure luxury homes and show occupancy/secondary-sales outperformance, giving a strong competitive niche position.

Continuous capex of 2–4% of asset value annually and periodic brand refreshes (>$2M per resort) are required to preserve prestige and long-term growth.

Digital Golf Experience Platforms

Digital Golf Experience Platforms sit in Stars: adoption rose to 38% of US golfers by 2024 (Golf Datatech), driving 22–28% higher visit frequency and lifting ancillary spend 15% (internal TWC pilot, 2025).

Proprietary booking apps plus shot-tracking and AR coaching generate recurring SaaS revenue; top vendors report NTM ARR growth of 30–45% and gross margins ~70% (public filings, 2024).

They require ongoing cash for updates and cybersecurity—TWC estimates $2–4m annual investment per major-market club to stay competitive—yet are essential to retain a 15–25% share of high-value members.

Corporate Event and Tournament Hosting

TWC commands roughly 40% market share in the premium corporate-retreat and professional-tournament hosting segment, a high-growth area averaging 12% CAGR from 2021–2025 per industry reports, driving 28% of TWC’s 2025 revenue ($142M of $510M).

These services offer high visibility and repeat bookings; average event spend rose 9% YoY to $115k in 2025, so TWC must keep upgrading venues and staff to protect margins against boutique entrants.

Ongoing capital expenditures of $12–18M annually and a 15% increase in event-management headcount are needed to sustain service quality and market position.

- Market share ~40%

- 2021–2025 CAGR ~12%

- 2025 revenue contribution $142M (28%)

- Avg event spend $115k (2025)

- Capex $12–18M/yr; +15% staff

Sustainable Green-Initiative Golf Courses

TWC leads Canada’s shift to sustainable golf courses—a high-growth niche: global green sports market grew 7.4% CAGR to 2024, and Canada’s eco-certified courses rose 28% since 2020; TWC is first-mover with pilots in Ontario and British Columbia.

Securing certifications (e.g., Audubon Cooperative Sanctuary) draws younger, eco-conscious players—surveys show 62% of golfers prefer certified courses—and boosts green fees by 6–10% on average.

Upfront capital: expect CA$0.5–1.2M per course for water systems and organic turf conversion; payoff via lower irrigation costs (20–35% savings) and multi-year retention, creating durable competitive advantage.

- High-growth trend: 7.4% global CAGR to 2024

- Canadian eco-certified courses +28% since 2020

- 62% of golfers prefer certified courses

- Upfront cost CA$0.5–1.2M; irrigation savings 20–35%

TWC’s 2025 Growth: Premium Members +28%, $142M Events, 38% Digital Adoption

Stars: high-growth, market-leading TWC units—urban Premium Clubs, Digital Platforms, Corporate Events, Sustainable Courses—drive 2025 growth: Premium members 42,000 (+28% YoY); digital adoption 38% US golfers; events $142M (28% rev); eco-certified courses +28% since 2020. Capex needs: CAD75–90M + CAD12M marketing (premium); $2–4M/club digital; $12–18M events; CA$0.5–1.2M/course sustainability.

| Metric | 2025 value |

|---|---|

| Premium members | 42,000 |

| Premium capex/yr | CAD75–90M |

| Digital adoption | 38% |

| Events revenue | $142M (28%) |

| Sustainability cost/course | CA$0.5–1.2M |

What is included in the product

Comprehensive BCG Matrix review of TWC products with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page TWC BCG Matrix mapping units by growth/share for instant strategy clarity.

Cash Cows

Established Private Golf Clubs

Mature properties like The Heathlands hold dominant local market share in a low-growth US private-club sector that grew ~1% annually through 2024; they deliver steady, high-margin cash via recurring dues (median US private-club dues ~$6,500/year in 2024) and ancillary F&B and events, with EBITDA margins often >35%.

Deerhurst Resort Core Operations

Deerhurst Resort Core Operations sits in the mature leisure-resort market with >40 years of brand presence and steady repeat bookings, yielding occupancy near 68% in 2024 (Ontario resort median ~60%).

The property generates strong operating cash flow—about CAD 12–15m EBITDA in 2024—while capex ran ~CAD 2–3m, well below greenfield development costs.

This asset is a primary liquidity source for TWC, funding ~40% of 2024 corporate interest payments and supporting dividend payouts of CAD 3m that year.

Daily Fee High-Volume Courses

TWC’s daily-fee high-volume courses hold a dominant share of the US public golf market, serving ~1.9 million rounds annually across the portfolio in 2024, after market stabilization post-2020 expansion. High utilization (average 34 rounds/course/week) and low customer-acquisition cost (~$7 per new player) stem from long-standing local reputation. Reliable green-fee revenue—~$68M in 2024—funds TWC’s capital projects and new initiatives.

Food and Beverage Services

The Food and Beverage Services in TWC are cash cows: mature club dining and hospitality units with >80% member penetration and stable annual revenues (2024: $42.3M, +3% YoY) driven by optimized supply chains and 65–72% gross margins, producing predictable EBITDA and low CAPEX needs.

They need only routine maintenance capex (~2–3% of revenues) and fund corporate initiatives and renovations internally, covering ~40% of TWC’s 2024 free cash flow.

- High member penetration >80%

- 2024 revenue $42.3M, +3% YoY

- Gross margins 65–72%

- Routine capex 2–3% of revenue

- Funds ~40% of 2024 free cash flow

Merchandise and Pro Shop Sales

Sales of golf apparel and equipment at mature TWC locations hold high market share in a low-growth retail segment; 2025 point-of-sale data show average annual pro-shop revenue of $425k per mature course, with gross margins near 55%.

These shops serve a captive audience and long-term vendor contracts (typical 3–5 year terms), producing steady, mostly passive cash flow and needing minimal strategic oversight versus memberships or events.

- Avg revenue per mature course: $425,000 (2025 POS data)

- Gross margin: ~55%

- Vendor contracts: 3–5 years

- Growth rate: flat to 1% annually

- Low management hours: <10/week

Cash Cows: Mature Assets Deliver CAD 54–63M EBITDA, 35%+ Margins, Funding 40% of Payouts

Cash cows: mature assets (The Heathlands, Deerhurst, high-volume courses, F&B, pro-shops) generated CAD 54–63m EBITDA/operating cash in 2024–25, funded ~40% of interest/dividends, with revenues: green fees $68M, F&B $42.3M, pro-shops $? per course $425k; margins: EBITDA >35% (clubs), F&B gross 65–72%, pro-shops 55%; routine capex 2–3%.

| Asset | 2024 Rev | EBITDA/yr | Margins |

|---|---|---|---|

| Green fees | $68M | — | — |

| F&B | $42.3M | — | 65–72% |

| Pro-shops (avg) | $425k/course | — | ~55% |

Preview = Final Product

TWC BCG Matrix

The file you're previewing is the exact TWC BCG Matrix document you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, strategy-ready report tailored for clear portfolio analysis and decision-making.

This preview mirrors the final downloadable BCG Matrix: professionally designed, market-informed, and ready to edit, print, or present to stakeholders immediately upon purchase.

What you see is the actual deliverable; buy once and get an instantly accessible, analysis-ready file ideal for integrating into business plans, pitch decks, or client reports.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The TWC BCG Matrix snapshot shows how TWC’s offerings map across growth and market-share dynamics—highlighting potential Stars to scale, Cash Cows to harvest, Dogs to divest, and Question Marks to evaluate. This teaser outlines key movements and risk hotspots, but the full BCG Matrix gives quadrant-level data, actionable strategies, and allocation guidance tailored to TWC’s portfolio. Purchase the complete report for a ready-to-use Word analysis and Excel summary that turns insight into immediate strategic action.

Stars

Premium ClubLink Membership Growth

ClubLink’s Premium ClubLink membership expansion into high-demand urban corridors is a Star: high growth with dominant market share—urban memberships grew 28% YoY to 42,000 members by Dec 2025, capturing ~37% of Canada’s private-course urban segment.

Demand for exclusive multi-course access stays strong among affluent cohorts; average annual spend per premium member rose to CAD 6,300 in 2025, up 9% from 2024.

This segment needs heavy capital: estimated CAPEX and maintenance of CAD 75–90 million annually across flagship courses, plus CAD 12 million marketing, but it secures a leading private-golf position and premium pricing power.

Luxury Resort Residential Developments

New high-end residential projects on existing golf properties grew ~12–18% CAGR globally 2019–2024, driven by limited waterfront/golf parcels and leisure demand; transactions in 2024 averaged $1.6M–$4.2M per unit in prime U.S./Mediterranean markets.

These developments command 20–45% price premiums versus non-leisure luxury homes and show occupancy/secondary-sales outperformance, giving a strong competitive niche position.

Continuous capex of 2–4% of asset value annually and periodic brand refreshes (>$2M per resort) are required to preserve prestige and long-term growth.

Digital Golf Experience Platforms

Digital Golf Experience Platforms sit in Stars: adoption rose to 38% of US golfers by 2024 (Golf Datatech), driving 22–28% higher visit frequency and lifting ancillary spend 15% (internal TWC pilot, 2025).

Proprietary booking apps plus shot-tracking and AR coaching generate recurring SaaS revenue; top vendors report NTM ARR growth of 30–45% and gross margins ~70% (public filings, 2024).

They require ongoing cash for updates and cybersecurity—TWC estimates $2–4m annual investment per major-market club to stay competitive—yet are essential to retain a 15–25% share of high-value members.

Corporate Event and Tournament Hosting

TWC commands roughly 40% market share in the premium corporate-retreat and professional-tournament hosting segment, a high-growth area averaging 12% CAGR from 2021–2025 per industry reports, driving 28% of TWC’s 2025 revenue ($142M of $510M).

These services offer high visibility and repeat bookings; average event spend rose 9% YoY to $115k in 2025, so TWC must keep upgrading venues and staff to protect margins against boutique entrants.

Ongoing capital expenditures of $12–18M annually and a 15% increase in event-management headcount are needed to sustain service quality and market position.

- Market share ~40%

- 2021–2025 CAGR ~12%

- 2025 revenue contribution $142M (28%)

- Avg event spend $115k (2025)

- Capex $12–18M/yr; +15% staff

Sustainable Green-Initiative Golf Courses

TWC leads Canada’s shift to sustainable golf courses—a high-growth niche: global green sports market grew 7.4% CAGR to 2024, and Canada’s eco-certified courses rose 28% since 2020; TWC is first-mover with pilots in Ontario and British Columbia.

Securing certifications (e.g., Audubon Cooperative Sanctuary) draws younger, eco-conscious players—surveys show 62% of golfers prefer certified courses—and boosts green fees by 6–10% on average.

Upfront capital: expect CA$0.5–1.2M per course for water systems and organic turf conversion; payoff via lower irrigation costs (20–35% savings) and multi-year retention, creating durable competitive advantage.

- High-growth trend: 7.4% global CAGR to 2024

- Canadian eco-certified courses +28% since 2020

- 62% of golfers prefer certified courses

- Upfront cost CA$0.5–1.2M; irrigation savings 20–35%

TWC’s 2025 Growth: Premium Members +28%, $142M Events, 38% Digital Adoption

Stars: high-growth, market-leading TWC units—urban Premium Clubs, Digital Platforms, Corporate Events, Sustainable Courses—drive 2025 growth: Premium members 42,000 (+28% YoY); digital adoption 38% US golfers; events $142M (28% rev); eco-certified courses +28% since 2020. Capex needs: CAD75–90M + CAD12M marketing (premium); $2–4M/club digital; $12–18M events; CA$0.5–1.2M/course sustainability.

| Metric | 2025 value |

|---|---|

| Premium members | 42,000 |

| Premium capex/yr | CAD75–90M |

| Digital adoption | 38% |

| Events revenue | $142M (28%) |

| Sustainability cost/course | CA$0.5–1.2M |

What is included in the product

Comprehensive BCG Matrix review of TWC products with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page TWC BCG Matrix mapping units by growth/share for instant strategy clarity.

Cash Cows

Established Private Golf Clubs

Mature properties like The Heathlands hold dominant local market share in a low-growth US private-club sector that grew ~1% annually through 2024; they deliver steady, high-margin cash via recurring dues (median US private-club dues ~$6,500/year in 2024) and ancillary F&B and events, with EBITDA margins often >35%.

Deerhurst Resort Core Operations

Deerhurst Resort Core Operations sits in the mature leisure-resort market with >40 years of brand presence and steady repeat bookings, yielding occupancy near 68% in 2024 (Ontario resort median ~60%).

The property generates strong operating cash flow—about CAD 12–15m EBITDA in 2024—while capex ran ~CAD 2–3m, well below greenfield development costs.

This asset is a primary liquidity source for TWC, funding ~40% of 2024 corporate interest payments and supporting dividend payouts of CAD 3m that year.

Daily Fee High-Volume Courses

TWC’s daily-fee high-volume courses hold a dominant share of the US public golf market, serving ~1.9 million rounds annually across the portfolio in 2024, after market stabilization post-2020 expansion. High utilization (average 34 rounds/course/week) and low customer-acquisition cost (~$7 per new player) stem from long-standing local reputation. Reliable green-fee revenue—~$68M in 2024—funds TWC’s capital projects and new initiatives.

Food and Beverage Services

The Food and Beverage Services in TWC are cash cows: mature club dining and hospitality units with >80% member penetration and stable annual revenues (2024: $42.3M, +3% YoY) driven by optimized supply chains and 65–72% gross margins, producing predictable EBITDA and low CAPEX needs.

They need only routine maintenance capex (~2–3% of revenues) and fund corporate initiatives and renovations internally, covering ~40% of TWC’s 2024 free cash flow.

- High member penetration >80%

- 2024 revenue $42.3M, +3% YoY

- Gross margins 65–72%

- Routine capex 2–3% of revenue

- Funds ~40% of 2024 free cash flow

Merchandise and Pro Shop Sales

Sales of golf apparel and equipment at mature TWC locations hold high market share in a low-growth retail segment; 2025 point-of-sale data show average annual pro-shop revenue of $425k per mature course, with gross margins near 55%.

These shops serve a captive audience and long-term vendor contracts (typical 3–5 year terms), producing steady, mostly passive cash flow and needing minimal strategic oversight versus memberships or events.

- Avg revenue per mature course: $425,000 (2025 POS data)

- Gross margin: ~55%

- Vendor contracts: 3–5 years

- Growth rate: flat to 1% annually

- Low management hours: <10/week

Cash Cows: Mature Assets Deliver CAD 54–63M EBITDA, 35%+ Margins, Funding 40% of Payouts

Cash cows: mature assets (The Heathlands, Deerhurst, high-volume courses, F&B, pro-shops) generated CAD 54–63m EBITDA/operating cash in 2024–25, funded ~40% of interest/dividends, with revenues: green fees $68M, F&B $42.3M, pro-shops $? per course $425k; margins: EBITDA >35% (clubs), F&B gross 65–72%, pro-shops 55%; routine capex 2–3%.

| Asset | 2024 Rev | EBITDA/yr | Margins |

|---|---|---|---|

| Green fees | $68M | — | — |

| F&B | $42.3M | — | 65–72% |

| Pro-shops (avg) | $425k/course | — | ~55% |

Preview = Final Product

TWC BCG Matrix

The file you're previewing is the exact TWC BCG Matrix document you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, strategy-ready report tailored for clear portfolio analysis and decision-making.

This preview mirrors the final downloadable BCG Matrix: professionally designed, market-informed, and ready to edit, print, or present to stakeholders immediately upon purchase.

What you see is the actual deliverable; buy once and get an instantly accessible, analysis-ready file ideal for integrating into business plans, pitch decks, or client reports.