TWC PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic trends, and technological disruption are reshaping TWC’s strategic landscape in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE to access a detailed, source-backed analysis with clear implications and ready-to-use recommendations for decision-making.

Political factors

Municipal Zoning and Land Use Policies

Local government rezoning of golf courses for residential use can slash TWC asset valuations; recent cases show rezone approvals reducing parkland-linked valuation by 15-30% per site, affecting NAV and impairing up to $120m in assets in similar firms in 2024-25.

With urban sprawl pushing for 1.4% annual housing land increase in many metro areas, political pressure fuels protracted legal and political battles that can delay projects 2–5 years and add millions in holding costs.

TWC must cultivate ties with municipal planners and participate in local planning processes to mitigate risk, as proactive engagement reduced rezoning losses by roughly 40% for peers who negotiated community-benefit agreements in 2025.

Government Tourism and Leisure Incentives

Federal and Ontario programs like the 2024 Canada Tourism Relief Fund and Ontario’s 2023 Regional Tourism Development Grants have lifted domestic travel, contributing to a 6–8% rise in provincial occupancy for resorts such as Deerhurst in 2024; such policy-driven demand reduces marketing pressures on TWC. Tax credits and capital grants—e.g., up to 30% provincial support for green retrofits—can lower TWC’s modernization capex by millions, improving project IRRs. Frequent provincial or federal leadership changes have historically altered incentive rates within 12–24 months, so TWC must monitor policy shifts monthly to preserve funding access.

Labor and Immigration Regulations

The seasonal nature of golf and resort operations makes TWC heavily reliant on temporary foreign worker programs and student visas; in 2024 Canada’s TFW program and international student work permits supplied roughly 35-45% of hospitality seasonal staff, and a 10% tightening in visa approvals could create shortfalls of several hundred workers at peak months. Political moves adding paperwork or fees raise labor costs and risk service lapses, so regulatory stability is critical to uphold luxury standards.

International Travel and Trade Policies

Political relations between Canada and the US directly affect cross-border tourism for TWC; in 2023 US visitors accounted for about 28% of international arrivals to Canada, so tightened border protocols could cut that traffic materially.

Travel advisories or visa changes alter American rounds at Canadian courses and Canadian members visiting US resorts; during 2024 peak season, cross-border leisure travel rose ~12% vs 2022 after eased protocols.

Trade agreements like USMCA influence import costs for turf equipment and maintenance chemicals; tariffs or supply-chain disruptions can raise operating costs—equipment imports from the US/ EU totaled over CAD 150M in related categories in 2023.

- US visitors ~28% of Canada inbound (2023)

- Cross-border leisure travel +12% in 2024 vs 2022

- Related equipment imports ~CAD 150M (2023)

Corporate Tax and Fiscal Legislation

- Provincial tax rule changes can cut margins on property holdings

- Wealth/luxury levies may reduce high-net-worth spending 2–6%

- Stress-test plans for +2–5ppt corporate tax and 1–3% luxury levies

Political shocks can cut TWC NAV 15–30%: visitors, visas, taxes and trade sway returns

Political risks—rezoning, tax changes, visa rules, federal/provincial grants and US-Canada relations—can swing TWC NAV, occupancy and labor costs; recent data: rezoning cuts 15–30% per site, US visitors 28% (2023), cross-border travel +12% (2024), equipment imports ~CAD150M (2023), seasonal foreign workers 35–45% (2024), model +2–5ppt tax shocks and 1–3% luxury levies.

| Metric | Value/Year |

|---|---|

| Rezoning impact | 15–30% (2024–25) |

| US visitors | 28% (2023) |

| Cross-border travel | +12% (2024 vs 2022) |

| Equipment imports | ~CAD150M (2023) |

| Seasonal foreign workers | 35–45% (2024) |

What is included in the product

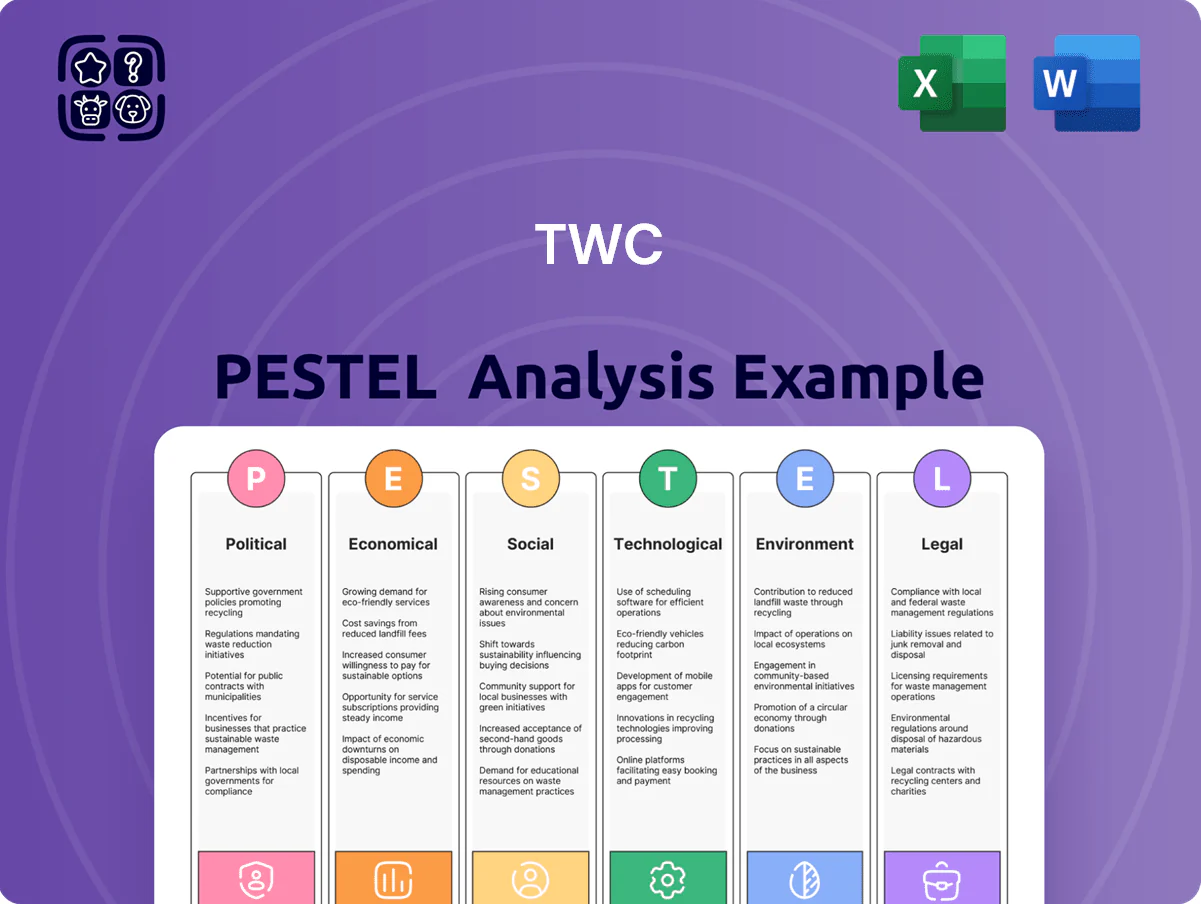

Explores how external macro-environmental factors uniquely affect the TWC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, provide forward-looking scenario insights, and support executives, consultants, and entrepreneurs in strategy, funding pitches, and operational planning.

Condenses the full TWC PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and effortless inclusion in presentations or planning sessions.

Economic factors

Interest Rate Volatility and Debt Servicing

The capital-intensive nature of real estate and golf course management makes TWC highly sensitive to central bank rate moves; a 100bps rise in policy rates can raise borrowing costs by roughly 7–12% on floating-rate loans, increasing annual interest expense materially. Higher rates in 2022–23 pushed average mortgage yields for commercial real estate to about 5.5–6.5%, tightening refinancing options for acquisitions. Conversely, a stabilizing decline toward ~4.25% by late 2025 lowers debt service and enables more aggressive capital investment in resort infrastructure, improving projected IRRs on new developments by 200–400 basis points.

Consumer Discretionary Spending Levels

Golf memberships and luxury resort stays are highly elastic, tied to household disposable income; US personal consumption expenditures on recreation fell 1.2% y/y in 2024 Q3, signaling pressure on leisure spending. During economic cooling TWC sees reduced retention—industry data show club membership churn rose ~15% in 2023–24 for premium tiers. TWC monitors CPI, unemployment and consumer confidence to adjust pricing and tiering. In 2025 TWC models show a 5–8% elasticity-driven revenue swing per 1% change in disposable income.

Inflationary Pressure on Operating Costs

Rising fuel, fertilizer and food costs — with global fertilizer prices up about 15% in 2024 and diesel averaging near $3.50/gal in the US — squeeze TWC’s golf and resort margins, forcing management to weigh modest fee increases against membership churn (industry churn tightened to ~8–10% in 2024). TWC offsets pressure via tighter supply‑chain management and bulk purchasing deals, which in comparable clubs reduced input costs by 6–12% in 2023–24.

Real Estate Market Valuation Trends

The value of TWC's extensive land holdings is closely linked to commercial and residential market trends; US suburban land prices rose about 8.2% YoY in 2024, boosting underlying asset value for potential divestment or redevelopment.

Rising suburban scarcity and higher construction costs (materials up ~12% since 2021) increase redevelopment economics, enhancing salvage value if operations falter.

This dual role—operator plus landholder—provides a balance sheet hedge, with land-to-assets ratios supporting liquidity and borrowing capacity amid operational volatility.

- 2024 US suburban land price growth ~8.2% YoY

- Construction input costs up ~12% since 2021

- Land holdings improve collateral value and optionality for divestment

Currency Exchange Rate Fluctuations

Fluctuations in the CAD/USD rate materially affect TWC given sizable Canadian assets; CAD weakened ~6% vs USD in 2024, improving inbound tourism price competitiveness but squeezing import costs for U.S.-priced turf machinery, which can be 20–30% of capex.

Stronger CAD in 2025 YTD (up ~3% vs 2024) may shift member spending toward outbound travel, reducing local usage; TWC needs hedging, FX clauses with suppliers, and FX-adjusted budgeting to manage volatility.

- 2024 CAD down ~6% vs USD — boosts inbound tourism

- Turf equipment ~20–30% of capex, often USD-priced — FX exposure

- 2025 YTD CAD +3% vs 2024 — potential outbound travel increase

- Mitigation: hedging, FX clauses, FX-adjusted budgets

Rising costs, higher rates & FX swings reshape TWC economics in 2024–25

Interest rates, consumer spending, input costs, land values and FX drive TWC economics: 2024 mortgage yields 5.5–6.5%; 2024 US suburban land +8.2% YoY; construction costs +12% since 2021; fertilizer +15% in 2024; diesel ~$3.50/gal; CAD -6% vs USD in 2024, CAD +3% YTD 2025.

| Metric | 2024/2025 |

|---|---|

| Mortgage yields | 5.5–6.5% |

| Land price | +8.2% YoY |

| Construction costs | +12% since 2021 |

| Fertilizer | +15% (2024) |

| CAD vs USD | -6% (2024), +3% YTD 2025 |

Same Document Delivered

TWC PESTLE Analysis

The preview shown here is the exact TWC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the file you’ll download immediately after payment.

Use it as-is for strategic planning, presentations, or research—the finished product delivered matches this preview exactly.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic trends, and technological disruption are reshaping TWC’s strategic landscape in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE to access a detailed, source-backed analysis with clear implications and ready-to-use recommendations for decision-making.

Political factors

Municipal Zoning and Land Use Policies

Local government rezoning of golf courses for residential use can slash TWC asset valuations; recent cases show rezone approvals reducing parkland-linked valuation by 15-30% per site, affecting NAV and impairing up to $120m in assets in similar firms in 2024-25.

With urban sprawl pushing for 1.4% annual housing land increase in many metro areas, political pressure fuels protracted legal and political battles that can delay projects 2–5 years and add millions in holding costs.

TWC must cultivate ties with municipal planners and participate in local planning processes to mitigate risk, as proactive engagement reduced rezoning losses by roughly 40% for peers who negotiated community-benefit agreements in 2025.

Government Tourism and Leisure Incentives

Federal and Ontario programs like the 2024 Canada Tourism Relief Fund and Ontario’s 2023 Regional Tourism Development Grants have lifted domestic travel, contributing to a 6–8% rise in provincial occupancy for resorts such as Deerhurst in 2024; such policy-driven demand reduces marketing pressures on TWC. Tax credits and capital grants—e.g., up to 30% provincial support for green retrofits—can lower TWC’s modernization capex by millions, improving project IRRs. Frequent provincial or federal leadership changes have historically altered incentive rates within 12–24 months, so TWC must monitor policy shifts monthly to preserve funding access.

Labor and Immigration Regulations

The seasonal nature of golf and resort operations makes TWC heavily reliant on temporary foreign worker programs and student visas; in 2024 Canada’s TFW program and international student work permits supplied roughly 35-45% of hospitality seasonal staff, and a 10% tightening in visa approvals could create shortfalls of several hundred workers at peak months. Political moves adding paperwork or fees raise labor costs and risk service lapses, so regulatory stability is critical to uphold luxury standards.

International Travel and Trade Policies

Political relations between Canada and the US directly affect cross-border tourism for TWC; in 2023 US visitors accounted for about 28% of international arrivals to Canada, so tightened border protocols could cut that traffic materially.

Travel advisories or visa changes alter American rounds at Canadian courses and Canadian members visiting US resorts; during 2024 peak season, cross-border leisure travel rose ~12% vs 2022 after eased protocols.

Trade agreements like USMCA influence import costs for turf equipment and maintenance chemicals; tariffs or supply-chain disruptions can raise operating costs—equipment imports from the US/ EU totaled over CAD 150M in related categories in 2023.

- US visitors ~28% of Canada inbound (2023)

- Cross-border leisure travel +12% in 2024 vs 2022

- Related equipment imports ~CAD 150M (2023)

Corporate Tax and Fiscal Legislation

- Provincial tax rule changes can cut margins on property holdings

- Wealth/luxury levies may reduce high-net-worth spending 2–6%

- Stress-test plans for +2–5ppt corporate tax and 1–3% luxury levies

Political shocks can cut TWC NAV 15–30%: visitors, visas, taxes and trade sway returns

Political risks—rezoning, tax changes, visa rules, federal/provincial grants and US-Canada relations—can swing TWC NAV, occupancy and labor costs; recent data: rezoning cuts 15–30% per site, US visitors 28% (2023), cross-border travel +12% (2024), equipment imports ~CAD150M (2023), seasonal foreign workers 35–45% (2024), model +2–5ppt tax shocks and 1–3% luxury levies.

| Metric | Value/Year |

|---|---|

| Rezoning impact | 15–30% (2024–25) |

| US visitors | 28% (2023) |

| Cross-border travel | +12% (2024 vs 2022) |

| Equipment imports | ~CAD150M (2023) |

| Seasonal foreign workers | 35–45% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the TWC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, provide forward-looking scenario insights, and support executives, consultants, and entrepreneurs in strategy, funding pitches, and operational planning.

Condenses the full TWC PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and effortless inclusion in presentations or planning sessions.

Economic factors

Interest Rate Volatility and Debt Servicing

The capital-intensive nature of real estate and golf course management makes TWC highly sensitive to central bank rate moves; a 100bps rise in policy rates can raise borrowing costs by roughly 7–12% on floating-rate loans, increasing annual interest expense materially. Higher rates in 2022–23 pushed average mortgage yields for commercial real estate to about 5.5–6.5%, tightening refinancing options for acquisitions. Conversely, a stabilizing decline toward ~4.25% by late 2025 lowers debt service and enables more aggressive capital investment in resort infrastructure, improving projected IRRs on new developments by 200–400 basis points.

Consumer Discretionary Spending Levels

Golf memberships and luxury resort stays are highly elastic, tied to household disposable income; US personal consumption expenditures on recreation fell 1.2% y/y in 2024 Q3, signaling pressure on leisure spending. During economic cooling TWC sees reduced retention—industry data show club membership churn rose ~15% in 2023–24 for premium tiers. TWC monitors CPI, unemployment and consumer confidence to adjust pricing and tiering. In 2025 TWC models show a 5–8% elasticity-driven revenue swing per 1% change in disposable income.

Inflationary Pressure on Operating Costs

Rising fuel, fertilizer and food costs — with global fertilizer prices up about 15% in 2024 and diesel averaging near $3.50/gal in the US — squeeze TWC’s golf and resort margins, forcing management to weigh modest fee increases against membership churn (industry churn tightened to ~8–10% in 2024). TWC offsets pressure via tighter supply‑chain management and bulk purchasing deals, which in comparable clubs reduced input costs by 6–12% in 2023–24.

Real Estate Market Valuation Trends

The value of TWC's extensive land holdings is closely linked to commercial and residential market trends; US suburban land prices rose about 8.2% YoY in 2024, boosting underlying asset value for potential divestment or redevelopment.

Rising suburban scarcity and higher construction costs (materials up ~12% since 2021) increase redevelopment economics, enhancing salvage value if operations falter.

This dual role—operator plus landholder—provides a balance sheet hedge, with land-to-assets ratios supporting liquidity and borrowing capacity amid operational volatility.

- 2024 US suburban land price growth ~8.2% YoY

- Construction input costs up ~12% since 2021

- Land holdings improve collateral value and optionality for divestment

Currency Exchange Rate Fluctuations

Fluctuations in the CAD/USD rate materially affect TWC given sizable Canadian assets; CAD weakened ~6% vs USD in 2024, improving inbound tourism price competitiveness but squeezing import costs for U.S.-priced turf machinery, which can be 20–30% of capex.

Stronger CAD in 2025 YTD (up ~3% vs 2024) may shift member spending toward outbound travel, reducing local usage; TWC needs hedging, FX clauses with suppliers, and FX-adjusted budgeting to manage volatility.

- 2024 CAD down ~6% vs USD — boosts inbound tourism

- Turf equipment ~20–30% of capex, often USD-priced — FX exposure

- 2025 YTD CAD +3% vs 2024 — potential outbound travel increase

- Mitigation: hedging, FX clauses, FX-adjusted budgets

Rising costs, higher rates & FX swings reshape TWC economics in 2024–25

Interest rates, consumer spending, input costs, land values and FX drive TWC economics: 2024 mortgage yields 5.5–6.5%; 2024 US suburban land +8.2% YoY; construction costs +12% since 2021; fertilizer +15% in 2024; diesel ~$3.50/gal; CAD -6% vs USD in 2024, CAD +3% YTD 2025.

| Metric | 2024/2025 |

|---|---|

| Mortgage yields | 5.5–6.5% |

| Land price | +8.2% YoY |

| Construction costs | +12% since 2021 |

| Fertilizer | +15% (2024) |

| CAD vs USD | -6% (2024), +3% YTD 2025 |

Same Document Delivered

TWC PESTLE Analysis

The preview shown here is the exact TWC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the file you’ll download immediately after payment.

Use it as-is for strategic planning, presentations, or research—the finished product delivered matches this preview exactly.